Owner income$798K

Owner income$798KHow Much Does A Mirror Manufacturing Owner Make? $798K Modeled

Fully Editable

Instant Download

Professional Design

Pre-Built

No Expertise Is Needed

Description

Owner income$798K  Net margin59.2%

Net margin59.2% Revenue for target pay$1.35M

Revenue for target pay$1.35M Business difficultyHard

Business difficultyHard

Key Takeaways

- Higher volume lowers overhead per mirror only with demand.

- Pricing must protect margin, not just fill capacity.

- Scrap and rework can erase gross profit fast.

- Cash timing and fixed overhead drive owner take-home.

Owner income$798KNet margin59.2%Revenue for target pay$1.35MBusiness difficultyHardWant to test your mirror manufacturing owner income?

Owner income calculator

Estimate owner take-home and the target-pay gap from revenue, margin, costs, reserves, and target pay.

Planning note: This is a researched planning estimate, not guaranteed salary, tax advice, or owner distribution advice. Actual owner income depends on revenue, margins, payroll, taxes, debt, and reinvestment.

Want to check owner pay in the Mirror Manufacturing model?

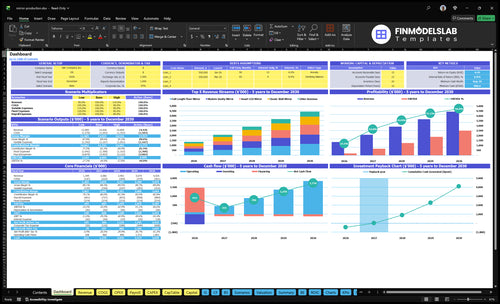

The dashboard shows revenue, units, gross margin, operating cash, and owner-pay capacity; open the Mirror Manufacturing Financial Model Template for the five-year view from $1,349M in Year 1 to $4,425M in Year 5.

Owner-income model highlights

- Owner pay capacity

- Revenue and margin

- Low, base, high

How much revenue does a mirror manufacturing business need to pay the owner?

Mirror Manufacturing needs about $340K in annual revenue to cover $2.688M of fixed overhead before owner pay, taxes, debt, and reserves. The model says Year 1 contribution after unit COGS, factory percentage costs, shipping, and commissions is about $1,067M, or 791% of revenue, so owner pay comes after that overhead floor is met. Add the owner’s target pay and any reserve buffer on top.

Revenue floor

- $2.688M fixed overhead

- $340K break-even revenue

- 791% contribution rate

- Owner pay comes after overhead

What to add

- Target owner salary on top

- Reserve cash on top

- Taxes and debt on top

- Use contribution, not gross revenue

What gross margin does a mirror manufacturing business need?

Mirror Manufacturing needs a high gross margin, because owner income depends more on margin than on sales volume. In Year 1, the model shows about 89% gross margin after direct unit COGS and 25% factory costs, then about 79% contribution margin after 70% shipping and 30% commissions. Direct unit COGS runs from $1,150 for a classic wall mirror to $4,000 for a smart LED mirror, and breakage, scrap, returns, and freight claims reduce distributable cash. If you want the startup budget side, see How Much Does It Cost To Launch Mirror Manufacturing Business?

Margin target

- Hold gross margin near 89%.

- Keep factory costs near 25%.

- Expect about 79% contribution.

- Margin matters more than volume.

Cash pressure

- Direct COGS runs from $1,150 to $4,000.

- Model 70% shipping.

- Model 30% commissions.

- Watch breakage and freight claims.

Is custom mirror manufacturing more profitable than wholesale mirror production?

Mirror Manufacturing is not automatically more profitable with custom work. Custom and premium mirrors can lift price from $150 classic wall mirrors to $450 smart LED mirrors in Year 1, but they also add labor, packaging, service time, and rework, so the real answer depends on margin after those costs and on how well you cover $2.688M in fixed overhead.

Why custom can pay more

- Higher selling price per unit

- Better fit for premium buyers

- Can support designer demand

- Raises margin if rework stays low

Why wholesale can win

- Improves plant utilization

- Spreads fixed overhead faster

- Can smooth cash flow timing

- Lower price can cut take-home

Want to see the main income drivers?

1

5.8K-16.5KVolume & Utilization

Year 1 starts at 5,800 units and Year 5 reaches 16,500, so fuller line use spreads plant cost and lifts EBITDA.

2

$1.35M-$4.43MMix & Pricing

Selling more full length and smart LED mirrors pushes revenue from about $1.35M to $4.43M, and that higher mix drives take-home.

3

89%Yield & Scrap

Keeping gross margin near 89% means less glass loss, fewer reworks, and more cash left after each mirror sold.

4

$520K-$680KLabor Productivity

Annual wage load rises from about $520K in Year 1 to $680K in Year 5, so automation has to keep pace with output.

5

10%-7%Channel Mix

Moving sales toward lower-fee channels can cut variable drag from 10% to 7%, which drops straight into profit.

6

$887KOverhead Control

The model bottoms out at $887K in month 8, so reserve discipline matters if you want to avoid outside funding and protect equity.

Mirror Manufacturing Core Six Income Drivers

Production Volume And Capacity Utilization

Production Volume And Capacity Utilization

When usable output rises, fixed overhead gets spread over more mirrors, so profit per unit improves. With 5,800 units in Year 1 and 16,500 units in Year 5, and fixed overhead held at $224K/month or $2.688M/year, overhead per unit falls from about $463 to $163.

That only helps owner income if demand, pricing, quality, and working capital keep up. More volume without margin control can trap cash in inventory and receivables, so the real test is sellable units, not just factory output. One clean metric: gross margin dollars per unit after overhead.

Track Usable Units, Not Just Starts

Track planned units, good units shipped, scrap, rework, and days in inventory. Here’s the quick math: $2.688M ÷ 5,800 = about $463 per unit; $2.688M ÷ 16,500 = about $163 per unit. If output rises but collections lag, owner pay can still shrink.

- Measure sell-through by line.

- Cap inventory before scaling.

- Test pricing before adding volume.

- Watch receivables and cash timing.

1

Product Mix And Pricing

Product Mix And Pricing

Year 1 pricing spans $150 classic wall, $180 decorative accent, $220 modern vanity, $350 full length, and $450 smart LED. When the mix shifts toward higher-priced units or custom work, average selling price goes up, so owner cash flow can improve even if unit count stays flat.

The key input is unit mix by style and channel. Here’s the quick math: ASP = total revenue ÷ units sold. Wholesale and builder packages can add volume, but if they push price down faster than they lower labor and overhead per unit, gross margin shrinks and less cash is left for owner pay.

Price For Margin, Not Just Volume

Track ASP, discount rate, and gross margin by product line. Split direct custom, wholesale, and builder orders so you can see which mix actually earns cash after labor, freight, and sales effort. If a low-price order only fills the factory, it still needs a floor margin or it can crowd out better work.

- Track mix by units and dollars.

- Set a margin floor before quoting.

- Charge custom work for extra labor.

- Review price cuts monthly.

A tilt toward $350 and $450 pieces can lift revenue per mirror fast, while too many $150 or bundled orders can soften cash flow. The owner’s draw depends on what stays after direct costs, not on how full the factory looks.

2

Material Yield And Scrap Control

Scrap Rate Control

Scrap rate hits owner income by burning glass, frames, backing, packaging, rework, returns, and freight claims. With modeled unit COGS of $1,150 to $4,000 before scrap adjustments, even small breakage or cut-loss can push gross margin down fast. The real hit is not just wasted material; it is also replacement labor, outbound freight, and customer credits.

Here’s the quick math: if a finished mirror fails after assembly, the loss can exceed the original unit cost because you still eat the redo, shipping, and service time. That means lower cash available for owner pay, especially when bad units also delay good orders and trap working capital in inventory.

Track Yield by Batch

Measure cut yield, breakage rate, rework rate, return rate, and freight claims by product line. Keep inspection tight, because cutting scrap costs by lowering quality usually backfires. A missed defect can erase the margin on one sale and add a second freight bill plus a customer credit.

- Track scrap dollars per unit.

- Review defects by line.

- Log replacement freight separately.

- Watch returns against shipments.

- Fix handling before scaling volume.

Use batch data to set a simple control rule: if one mirror style shows rising scrap, slow that line and find the cause in cutting, edging, packing, or transit. Safer handling and better yield protect gross margin, which is the cash pool that pays overhead and owner draw.

3

Labor Productivity And Process Efficiency

Labor Per Mirror

Direct labor is the hands-on cost to cut, edge, back, frame, inspect, pack, and ship each mirror. It is modeled at $200 for classic wall mirrors, $300 for modern vanity mirrors, $400 for full length mirrors, $250 for decorative mirrors, and $500 for smart LED mirrors. The higher the labor per unit, the tighter the gross margin and the less cash left for owner pay.

This driver moves income through the product mix. A smart LED mirror needs 2.5x the direct labor of a classic wall mirror, so a shift toward premium styles can raise revenue but also push up labor cost fast. Here’s the quick math: if labor falls by $25 across 5,800 units, that saves $145,000 a year before overhead. One bad process can eat that back quickly.

Track Labor By Unit

Measure labor hours per mirror, not just total payroll. Track labor by SKU, rework rate, and units per shift, then compare the result to the unit targets of $200 to $500. If one style keeps running over target, it is usually a setup, training, or inspection issue, not just a wage issue. What this estimate hides is overtime, rework, and handling loss.

Use automation only when the volume can cover the payment and upkeep. Do the math in plain terms: monthly labor savings must beat equipment payment plus maintenance. If it does not, manual flow is cheaper. Lock the process first, then automate the slowest step. That keeps cash free for profit, reserves, and the owner’s draw.

- Track labor cost by SKU.

- Watch rework and scrap.

- Compare savings to equipment payments.

- Test one bottleneck first.

4

Customer Channel And Sales Mix

Sales Channel Mix

Channel mix changes margin, cash timing, and how much time the owner spends on quotes, order follow-up, and service. In this model, shipping and logistics are 70% of Year 1 revenue and sales commissions are 30%, so the owner’s take-home depends on how much of each sale is kept after freight, commissions, and handling time.

Wholesale can steady factory load, but it usually comes with lower price. Direct custom work can lift margin, but it adds quoting and service hours. The key inputs are channel mix, average order value, commission rate, payment terms, and days to collect cash, because profit on paper does not pay the owner until money clears.

Track Cash by Channel

Split each order by channel, price, commission, freight, and days to cash. That tells you which sales actually fund owner pay. A channel that looks busy can still hurt income if it adds service time or slows collection.

Set a simple rule: track gross margin per channel, quote hours per order, and cash collected per week. If wholesale fills capacity but squeezes price, use it for volume only when it covers overhead and keeps cash moving. If direct sales pay more , cap custom work at the service hours the team can handle.

- Measure margin after freight.

- Watch commission as a percent.

- Track days sales outstanding.

- Limit low-margin custom quotes.

5

Overhead, Freight, Equipment, And Reserves

Overhead, Freight, and Reserves

$224K/month of fixed overhead hits owner income before any mirror is sold, so strong gross margin can still leave little cash to draw. That overhead includes factory rent and utilities, office rent, insurance, software, legal and accounting, and equipment maintenance. Add freight and commissions equal to 100% of Year 1 revenue, and profit can look fine on paper while cash stays tight.

Model owner pay from cash collected, not operating profit. Here’s the quick math: take gross profit, subtract $224K/month fixed overhead, then subtract freight, commissions, claims, repairs, breakage, slow receivables, and planned reinvestment. If reserves are not funded, the business may show earnings but still miss payroll, vendor bills, or distribution targets.

Track cash, not just margin

Build a monthly bridge from revenue to distributable cash. Track freight as % of revenue, commission rate, overhead run rate, equipment maintenance, claims, and days to collect receivables. Set a reserve target for breakage, repairs, and slow pay, then hold it before any owner draw. The key input is not just unit sales; it is how fast each sale turns into usable cash.

- Watch gross profit versus cash.

- Cap fixed overhead early.

- Fund reserves before draws.

- Review freight on every order.

- Collect receivables faster than payables.

6

Scenario objective: Compare low, base, and high mirror manufacturing owner-income cases

Owner income scenarios

Owner income moves with unit volume, mix, pricing, and collections. Fixed factory and office overhead stay on, so cash can swing fast between a thin year and a scaled year.

| Scenario | Low CaseDownside case | Base CaseCore plan | High CaseUpside case |

|---|---|---|---|

| Launch model | Owner income stays thin because demand, pricing, and collections all run below plan. | Owner income follows the modeled Year 1 run rate and then improves as volume builds. | Owner income scales stronger as volume reaches the Year 5 model and margins stay firm. |

| Typical setup | Volume sits below the Year 1 model, mix skews to lower-priced mirrors, shipping and sales commissions take more of each sale, and fixed overhead still gets paid. | The model starts at 5,800 units, about $1.349M revenue, roughly 89% gross margin, about 79% contribution margin, and about $798k before owner-level cash decisions. | The model reaches 16,500 units, about $4.425M revenue, about 89.8% gross margin, about 82.8% contribution margin, and about $3.395M before taxes, debt, reserves, and distributions. |

| Cost drivers |

|

|

|

| Owner income rangeBefore owner reserves | $0 - $193kTight cash | $193k - $798kMain case | $798k - $3.395MScale upside |

| Best fit | Use this to stress-test a slow launch and tight working capital. | Use this as the standard planning case for budgeting and lender talks. | Use this to test what strong demand and tight cost control can do for owner cash. |

Planning note: These scenario ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distribution plans.

Related Products

- Mirror Manufacturing Porter's Five Forces Analysis

- Mirror Manufacturing BCG Matrix

- Mirror Manufacturing Business Model Canvas

- Mirror Manufacturing KPIs: Tracking Production Efficiency and Margin

- Mirror Manufacturing Business Plan Template in Pre-Written Word

- 7 Proven Strategies to Boost Mirror Manufacturing Margins

- How to Budget and Control Operating Costs in Mirror Manufacturing

- Mirror Manufacturing Startup Costs for a 5,800-Unit Year 1 Launch

- Mirror Manufacturing Financial Model Template in Excel

- Start a Mirror Manufacturing Business With a 5-SKU Launch Plan

- How to Write a Mirror Manufacturing Business Plan in 7 Steps

- Mirror Manufacturing Marketing Mix

- Mirror Manufacturing Marketing Plan

- Mirror Manufacturing Business Proposal

- Mirror Manufacturing PESTEL Analysis

- Mirror Manufacturing Pitch Deck Example Editable PPTX

- Mirror Manufacturing Business SWOT Analysis

- Mirror Manufacturing Value Proposition Canvas

Frequently Asked Questions

Using the researched base case, Year 1 revenue is $1349M and modeled operating cash is about $798K before owner distributions, taxes, debt service, and reserves By Year 5, revenue reaches $4425M with about $3395M before those owner-level cash decisions Actual owner take-home depends on reserves and reinvestment