Owner income≈$279k/mo

Owner income≈$279k/moHow Much Mobile Empanada Stand Owners Make: $335M EBITDA Case

Fully Editable

Instant Download

Professional Design

Pre-Built

No Expertise Is Needed

Description

Owner income≈$279k/mo  Net margin53%

Net margin53% Revenue for target pay≈$528k/mo

Revenue for target pay≈$528k/mo Business difficultyMedium

Business difficultyMedium

You’re not trying to guess sales you’re trying to see what can actually become owner income In the researched case, annual EBITDA is $3351M in Year 1 and rises to $9769M in Year 5, but EBITDA is not owner take-home Results depend on demand, event schedule, pricing, food cost control, payroll, permits, commissary costs, reserves, and owner draw policy

Owner income≈$279k/moNet margin53%Revenue for target pay≈$528k/moBusiness difficultyMediumWant to test your owner pay?

Owner income calculator

Estimate owner take-home and target-pay gap from revenue, margin, costs, reserves, and target pay for a mobile empanada stand.

Planning note: Research-based planning estimate only. It is not guaranteed salary, tax advice, or owner distribution advice.

Want to stress-test the full Mobile Empanada Stand model?

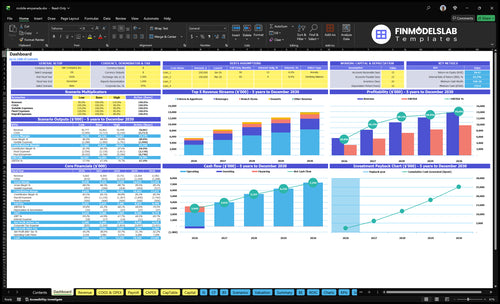

The dashboard shows revenue, EBITDA, breakeven, minimum cash, payback, and owner income in the Mobile Empanada Stand Financial Model Template; open it to test the assumptions.

Owner-income stress test

- Owner draw sensitivity

- Assumptions tab built in

- Covers, AOV, sales mix

- COGS, payroll, fixed costs

- Capex, permits, scenarios

- Year 1 vs 5 EBITDA

- Test food and labor

- Event volume and reserves

How many empanadas do I need to sell to hit target owner pay?

For Mobile Empanada Stand, don’t count empanadas first — model orders or covers, because the math is driven by average order value and contribution margin. Your owner-pay gap is desired owner draw + taxes + debt + reserves + fixed costs + payroll, then divide by the contribution margin; in Year 1, that margin is 83.5% after food, beverage, card fees, and marketing. If event fees, labor, or waste rise, the answer changes fast, so unit count only works if you know the real menu mix.

Use orders, not units

- Orders drive the model.

- Covers are the cleaner unit.

- 83.5% is the Year 1 margin.

- Units only help with real menu counts.

What changes the target

- Add owner draw first.

- Include taxes and debt.

- Include reserves and payroll.

- Watch event fees and waste.

How much can you make with a mobile empanada stand?

A Mobile Empanada Stand can make about $3.351M in Year 1 EBITDA, or roughly $279k per month, in the researched case; What Is The Most Important Indicator Of Success For Mobile Empanada Stand? is the KPI lens I’d use before calling that owner income. By Year 5, EBITDA reaches $9.769M under higher cover counts and average order value, but this is not a standard salary.

Earnings case

- Year 1 EBITDA: $3.351M

- Monthly EBITDA: $279k

- Year 5 EBITDA: $9.769M

- Driven by covers and AOV

Owner take-home

- Subtract taxes and debt service

- Fund depreciation and reserves

- Control payroll and fixed costs

- Watch permits, commissary, rent

Should I stay owner-operated or scale with staff and events?

For a Mobile Empanada Stand, stay owner-operated until demand clearly supports payroll. The quick math is simple: staff growth starts with $780k in Year 1 payroll and rises to $134M by Year 5, so you need real volume or your take-home drops fast.

Weekend demand helps a lot, with 220 Saturday covers versus 60 on Monday, so start there. Festivals and catering can lift revenue, but prep time, travel, permits, staffing, and sell-through risk can make high sales less useful if margins shrink.

Stay lean first

- Protect cash with owner labor.

- Use strong weekend traffic first.

- Test demand before hiring.

- Keep fixed costs low.

Scale only with proof

- Hire when volume is repeatable.

- Use events to fill gaps.

- Watch margins, not just sales.

- Count prep and permit time.

Want to see what moves owner income most?

1

60-440/daySelling Days

Covers run from 60 on Monday to 440 on Saturday by Year 5, so route choice and traffic placement drive most owner income.

2

$120-$170Average Ticket

Midweek tickets rise from $120 to $140 and weekends from $150 to $170, so upsells and combo pricing lift revenue without adding new sites.

3

88%-89.2%Gross Margin

Listed COGS stay near 10.8%-12.0% of sales, so portion control and supply pricing decide how much profit reaches the owner.

4

$30Weekend Premium

Weekend orders carry a $30 higher ticket than midweek in Year 1, so pushing more volume into Friday through Sunday lifts take-home fast.

5

17-31 FTELabor Load

Staffing scales from 17 to 31 FTE across the plan, so every extra shift has to earn more than its wage.

6

$35.5K/moFixed Overhead

Fixed costs run $35.5K a month, and minimum cash drops to $719K in Month 2, so reserve discipline protects owner draws.

Mobile Empanada Stand Core Six Income Drivers

Selling Days And Foot Traffic

Selling Days and Foot Traffic

Selling days are the days the stand can actually trade in a high-traffic spot. For this model, Year 1 ranges from 60 on Monday to 220 on Saturday, and Year 5 reaches 120 to 440. More qualified days raise revenue before fixed costs, so each extra order helps owner pay because it flows through contribution margin first.

The risk is weak traffic, not just weak demand. Weather, seasonality, location rules, market availability, and slow weekdays can cut volume fast. One line says it best: more foot traffic usually means more take-home cash, but only if the stand can stay in the right place at the right time.

Track Traffic by Day and Site

Measure orders per selling day, not just total sales. Break out Monday through Saturday, plus lunch stops, weekend events, and festivals, so you can see which locations produce the best sales density. Here’s the quick math: if a better site adds orders without adding much extra labor or rent, most of that gain should lift profit.

Use a simple field log: date, location, weather, hours open, foot traffic, orders, and sell-through. Then compare 60 versus 220 in Year 1 and 120 versus 440 in Year 5 by channel. If a site needs heavy staffing or has poor weekday flow, it may look busy but still hurt owner income.

- Track orders per selling day

- Compare weekday and weekend traffic

- Test lunch stops and events

- Drop low-yield locations fast

1

Average Ticket And Upsells

Average Ticket and Upsells

Average ticket, or average order value (AOV), is the dollars each guest spends per visit. For a mobile empanada stand, that means empanadas plus drinks, sauces, dessert items, and catering packs. Research shows AOV moving from $120 midweek and $150 on weekends in Year 1 to $140 and $170 in Year 5, a 16.7% lift midweek and 13.3% on weekends.

Here’s the quick math: the same traffic can earn more cash if each order is larger, and that extra revenue can feed owner pay after direct costs. But a price hike is not pure profit. If portions grow, demand slips, or ingredient cost rises, the gain can shrink fast, so watch contribution margin, meaning what’s left after direct variable costs.

Measure the Attach Rate

Track order count, AOV by day, and the attach rate for drinks, sauces, desserts, and bundles. Split weekday and weekend results, because the model already shows different ticket levels by day.

- Track AOV by daypart.

- Test bundles against single items.

- Price add-ons above food cost.

- Watch prep time and waste.

If an upsell uses spare prep capacity, it can lift profit with little extra labor. If it slows the line or adds waste, the owner may get more sales but less take-home income.

2

Food Cost And Packaging Margin

Food Cost And Packaging Margin

This driver decides how much of each empanada sale turns into gross profit. The research lists food and beverage COGS at 12% in Year 1 and 108% by Year 5; that Year 5 figure needs a check, because once COGS passes 100%, the item sells below cost. Recipe cost, portion size, batch prep, oil use, and packaging all move owner pay fast.

Gross margin is not net profit. After food and packaging, the owner still pays payroll, rent or commissary, permits, insurance, fuel, repairs, and reserves. So a tight menu can support owner draw, but waste or heavy sauce use can wipe out cash even when sales look strong.

Track Cost Per Order

Cost each recipe by unit and check the real build on every top seller. Include filling, fryer oil, sauce cups, containers, napkins, and waste. Here’s the quick math: if one order leaks cost on every sale, that loss hits contribution margin immediately and leaves less money for fixed costs and owner pay.

- Weigh portions during prep.

- Compare actual cost to recipe.

- Track packaging per order.

- Log waste by item and shift.

Test supplier pricing and batch prep first on the highest-volume items. If food COGS stays near the Year 1 12% target, more revenue can cover payroll, rent, and reserves. If oil or packaging creep up, raise price or cut waste before scaling the menu.

3

Event And Catering Mix

Event Mix and Income

Channel mix can lift sales, but it also changes margin and cash timing. Here, Friday to Sunday covers are stronger at 180, 220, and 140 versus 60 on Monday, so weekend events should drive more gross revenue. The catch is simple: private events and catering can steady income, but festivals add booth fees, staffing, travel, and unsold stock risk.

That means high revenue does not always mean high profit. The owner’s take-home pay depends on net dollars after event fees, labor, fuel, and waste. If a busy event has weak sell-through, the extra volume can still leave less cash than a smaller, cleaner catering job.

Track Net Profit by Channel

Measure each channel as sales minus event fees, labor, travel, and waste. Compare Monday street sales, weekend events, private catering, and festivals on the same basis so you can see which one really funds owner pay. The right metric is net profit per event, not just covers or topline revenue.

- Track sell-through and waste

- Log booth fees and travel

- Compare profit per labor hour

If a festival sells well but fees and staffing eat the margin, cut back or price higher. If catering is steady and low waste, push more of it into the mix because it usually improves predictability and protects cash flow.

4

Labor And Owner Role

Owner Labor

Owner labor can raise take-home in the short run because the founder covers prep, cashiering, and event shifts instead of paying staff. But it is still a real cost. Researched payroll is $780k in Year 1, $1116M in Year 3, and $134M in Year 5, so labor is one of the biggest cash drains on owner pay.

The key inputs are owner hours, paid prep help, cashiers, cooks, and event staff. If volume does not rise, hiring cuts cash fast. If service speed and order count rise enough, labor can protect sales and keep the stand moving. One clean rule: unpaid work is not free; it only hides the true cost.

Track Real Labor Cost

Track labor by role and by shift, then price the menu as if the owner were replaced. That means watching owner hours, paid hours, and cash payroll each week so profit does not look better just because the founder worked free. Separate business profit from unpaid owner labor before setting owner draw.

- Owner hours by task

- Paid prep and event hours

- Orders per shift

- Payroll cash by week

If a prep helper or cashier saves time, check whether daily orders rise enough to cover the extra wage. The labor plan should flex with weekday, weekend, and event demand, because payroll that grows faster than sales cuts owner cash first.

5

Fixed Costs And Reserves

Fixed Costs and Reserves

$355k per month in fixed costs means sales have to clear a very high hurdle before the owner sees real pay. That total includes rent, utilities, property taxes, insurance, POS systems, licenses, permits, and equipment maintenance, so weak weeks hit cash flow fast even if food sales look decent.

Here’s the quick math: fixed costs come before owner draw, so slow months can wipe out profit fast. The $370k capex bucket for kitchen equipment, furniture, bar setup, POS hardware, inventory, building upgrades, signage, website, and launch marketing also matters because those uses tie up cash that could otherwise cover repairs or payroll gaps.

Track the Monthly Burn, Not Just Sales

Measure fixed cost per month, then compare it with sales by day and event. Track rent, insurance, permits, maintenance, and reserve funding as separate lines, so you can see which cost is pushing owner pay down. If slow weekdays are common, hold back draw until cash covers at least one bad month and near-term repairs.

- $355k fixed-cost hurdle

- $370k capex and setup cash need

- Separate reserves from owner draw

- Stress test slow months first

What this estimate hides: one weak location rule, a weather run, or a repair bill can cut take-home income quickly. In strong sales months, the effect is medium because extra cash can refill reserves; in slow months, it is severe because fixed costs keep coming whether the stand sells or not.

6

Compare low, base, and high owner-income scenarios without treating profit as salary

Owner income scenarios

Owner income rises fast as traffic and ticket size climb from Year 1 to Year 5. The table shows the early ramp, scaled, and mature cases.

| Scenario | Low CaseLow Case | Base CaseBase Case | High CaseHigh Case |

|---|---|---|---|

| Launch model | Year 1 is the early ramp case with about $6.334M revenue, 88.0% gross margin, and $3.351M EBITDA before taxes, debt, reserves, and owner draws. | Year 3 is the scaled case with about $11.107M revenue, 88.7% gross margin, and $7.306M EBITDA before taxes, debt, reserves, and owner draws. | Year 5 is the mature case with about $14.498M revenue, 89.2% gross margin, and $9.769M EBITDA before taxes, debt, reserves, reinvestment, and distributions. |

| Typical setup | Traffic runs 60 to 220 covers a day, with $120 midweek AOV, $150 weekend AOV, about $780k payroll, and $35.5k of fixed costs each month. | Traffic reaches 100 to 360 covers a day, AOV rises to $130 midweek and $160 on weekends, and payroll steps up to about $1.086M. | Traffic peaks at 120 to 440 covers a day, AOV reaches $140 midweek and $170 on weekends, and payroll reaches about $1.34M. |

| Cost drivers |

|

|

|

| Owner income rangeBefore owner reserves | $3.35M EBITDALow case band | $7.31M EBITDABase case band | $9.77M EBITDAHigh case band |

| Best fit | Use this to test a slow opening and see if early traffic covers payroll and fixed overhead. | Use this as the main planning case for a working stand that has found steady traffic and repeat buyers. | Use this to test a strong mature run with higher volume and pricing, plus the cash demands that come with it. |

Planning note: Scenario ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions.

Related Products

- Mobile Empanada Stand Porter's Five Forces Analysis

- Mobile Empanada Stand BCG Matrix

- Mobile Empanada Stand Business Model Canvas

- 7 Critical Financial KPIs for Your Mobile Empanada Stand

- Mobile Empanada Stand Business Plan Template in Pre-Written Word

- 7 Strategies to Increase Mobile Empanada Stand Profitability

- Analyzing the Monthly Running Costs for a Mobile Empanada Stand

- Mobile Empanada Stand Startup Costs: $719K Cash Planning Case

- Mobile Empanada Stand Financial Model Template in Excel

- How to Open a Mobile Empanada Stand in 6 to 12 Weeks

- How to Write a Business Plan for a Mobile Empanada Stand

- Mobile Empanada Stand Marketing Mix

- Mobile Empanada Stand Marketing Plan

- Mobile Empanada Stand Business Proposal

- Mobile Empanada Stand PESTEL Analysis

- Mobile Empanada Stand Pitch Deck Example Editable PPTX

- Mobile Empanada Stand Business SWOT Analysis

- Mobile Empanada Stand Value Proposition Canvas

Frequently Asked Questions

The researched case shows $3351M in Year 1 EBITDA, or about $279k per month before taxes, debt service, depreciation, reserves, and owner distributions That is not guaranteed take-home Actual owner income depends on how much cash is held back for repairs, slow months, financing, and working capital