Owner income$75k

Owner income$75kHow Much Mobile Home Cleaning Owners Make: $75k Pay Plus Profit

Fully Editable

Instant Download

Professional Design

Pre-Built

No Expertise Is Needed

Description

Owner income$75k  Net margin48%

Net margin48% Revenue for target pay$823k

Revenue for target pay$823k Business difficultyHard

Business difficultyHard

Key Takeaways

- Ticket mix drives revenue, but overlap must be confirmed.

- Completed jobs matter more than leads for weekly revenue.

- Route density cuts fuel and raises billable hours.

- Cash needs stay high despite $7,500 monthly overhead.

Owner income$75kNet margin48%Revenue for target pay$823kBusiness difficultyHardWant to test your owner pay?

Owner income calculator

Estimate owner take-home and the target-pay gap from revenue, margin, labor, overhead, reserves, and owner pay.

Planning note: This is a researched planning estimate, not guaranteed salary, tax advice, or owner distribution advice.

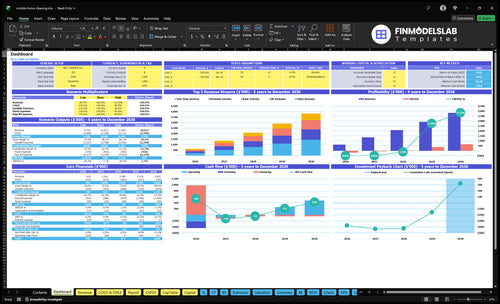

Want to check owner income in the Mobile Home Cleaning financial model?

The screenshot in the Mobile Home Cleaning Financial Model Template shows revenue, EBITDA, breakeven, cash need, and payback. Open the model to see how $75,000 owner pay comes from the assumptions, not hope.

Owner-income model highlights

- EBITDA from -$194k to $380k

- Month 22 breakeven

- $339k minimum cash need

- 57-month payback

- Tabs cover pricing and labor

- Charts show margin and runway

How many mobile home cleanings per week to make money?

If you’re asking how many jobs it takes for Mobile Home Cleaning to make money, a solo operator needs about $28,646 in monthly revenue to cover $13,750 owner pay and $7,500 fixed overhead at a 48% contribution rate. That works out to roughly 24 weekly $275 jobs or 74 weekly $89 jobs, before cancellations; route density matters more than raw lead count.

Price points

- $89 Basic Exterior

- $129 Premium Interior

- $189 All-Inclusive

- $275 One-Time Services

What changes the weekly count

- Average ticket sets the target

- Home size changes job time

- Service depth changes margin

- Staff in Year 1 changes capacity

How much can a solo mobile home cleaning owner make?

A solo Mobile Home Cleaning owner can use $75,000 a year as the planning anchor, but that requires about $141,509 in annual sales before fixed overhead because core costs take 47% of revenue. For the operating metric behind that math, see What Is The Most Important Measure Of Success For Mobile Home Cleaning?: wages saved help, but they don’t create scalable profit if travel, quoting, callbacks, scheduling, and collections eat billable hours.

Solo income math

- $75,000 target owner pay

- 47% variable cost load

- 53% contribution margin

- $11,792 monthly sales needed

Costs still hit

- 12% supplies

- 6% equipment

- 8% fuel

- 18% marketing, plus 3% fees

Can a mobile home cleaning business make more by hiring cleaners?

Yes—Mobile Home Cleaning can grow revenue by hiring cleaners, but the margin can shrink fast if pricing, utilization, and quality control slip. A Year 1 team with 2 lead technicians at $42,000 each, 3 technicians at $36,000 each, and 1 customer service representative at $38,000 totals $230,000 in payroll, and payroll can reach $1.1 million by Year 5. The best setup is clustered parks, landlords, investors, and property managers with repeat move-out and recurring cleans, because higher revenue only helps when crew hours stay billable.

When hiring helps

- Clustered parks cut drive time.

- Repeat cleans improve crew utilization.

- Move-out jobs support steady demand.

- Billable hours protect owner income.

Where it breaks

- Labor quality drives rework risk.

- Seasonal demand can leave crews idle.

- Cancellations create lost payroll leverage.

- Travel gaps and underbooked crews hurt margin.

Want the six income drivers?

1

$89-$275Package Mix

Pushing more jobs into Premium Interior and All-Inclusive work raises each stop's ticket, since starting prices run from $89 to $275.

2

$380KJob Volume

More completed cleanings spread the fixed cost base, and that is what takes cash-like profit from -$194K in Year 1 to $380K in Year 4.

3

8%-6%Route Density

Shorter drive gaps trim vehicle fuel and time on the road, and the transport cost line eases from 8% to 6% of revenue.

4

7-27 FTECrew Model

Moving from owner-led work to a small crew adds full-time equivalent capacity, but wages can squeeze take-home if staffing grows faster than demand and the $75K owner pay stays in place.

5

3.5-4.5hRecurring Accounts

Park, landlord, investor, and property-manager accounts smooth demand, lift monthly billable hours per active customer, and help you reach Month 22 break-even.

6

$339KOverhead Control

Your fixed overhead runs about $7.5K a month, so tight reserves protect the $339K minimum cash need and the 57-month payback path.

Mobile Home Cleaning Core Six Income Drivers

Average ticket and package mix

Average Ticket and Package Mix

Average ticket moves income fast because revenue is jobs × ticket, and a shift from $89 exterior work to $129, $189, or $275 service lifts cash without adding the same number of stops. If you normalize the listed mix, the weighted ticket is about $152 because the shares total 120%, so confirm overlap before treating it as a clean portfolio.

Price should reflect home size, condition, access, pet mess, move-out scope, and local competition risk. Underpricing dirty homes is a margin leak because labor time rises faster than revenue. One line: cheap jobs only work if the clock stays short.

Protect Margin on Every Quote

Track ticket by package and by actual labor minutes. If a job needs extra scrubbing, stairs, clutter moves, or move-out detail, reprice before the crew starts. That keeps gross margin from being eaten by unpaid labor and helps owner pay and cash flow stay tied to real profit, not just booked sales.

- Log price, minutes, and rework.

- Compare planned vs actual time.

- Separate overlap from true mix.

- Charge more for dirty homes.

Before forecasting income, confirm whether the 45%, 35%, 15%, and 25% allocations overlap. If they do, the real mix may be richer than it looks; if they don’t, the model needs a correction. Either way, steer the calendar toward higher-ticket interior and all-inclusive work, not low-price exterior only.

1

Weekly job volume

Weekly job volume

For mobile home cleaning, completed cleanings drive weekly revenue more than leads do. The quick math is jobs per week × average ticket, then subtract direct and variable costs. In Year 1, contribution after supplies, equipment, fuel, marketing, commissions, and payment fees is about 48% before fixed overhead and payroll.

Cancellations hurt twice: you lose the job, and the crew still has idle time while the route still burns fuel and admin time. That makes weekly volume a high revenue driver with high scheduling difficulty, especially when one owner is also handling quotes, reminders, reviews, and payment collection.

Protect completed jobs each week

Track booked jobs, completed jobs, cancellations, average ticket, and variable cost % every week. Use those numbers to forecast take-home pay, because more completed jobs lift cash only if the route stays full and the crew stays busy. One clean calendar is worth more than a stack of leads.

- Measure booked-to-completed rate

- Price by job size and scope

- Cut no-shows with reminders

- Keep routes tightly clustered

What this estimate hides is the owner’s time cost. If quotes, follow-ups, and payment collection start crowding the day, weekly capacity drops fast, so the real control lever is not just more leads, but more finished cleanings.

2

Route density and travel time

Clustered Routes

Route density is how many jobs sit close together. In this model, fuel and direct transportation are 8% of revenue in Year 1 and improve to 6% by Year 5. That spread drops pure cost and lifts margin because cleaners spend more time cleaning and less time driving. On $100,000 of revenue, that is about $2,000 less transport cost by Year 5.

The risk is taking far-apart jobs that look profitable on price but fail after travel. Booking three homes in one community or pairing interior cleans with nearby exterior jobs raises billable hours, lowers fuel, and cuts vehicle wear. That’s why this driver has a high margin impact and can directly improve owner pay.

Keep Jobs Close

Track drive minutes per job, miles per stop, and revenue per route day. If travel starts eating crew time, add a minimum ticket, a trip fee, or a zone limit before you accept the work. One clean rule helps: if the route breaks the day, it probably breaks the margin too.

- Group homes by park or street

- Pair interior and exterior visits

- Reject thin, far routes

- Watch transport cost at 8% then 6%

The key inputs are job count, average ticket, distance between stops, and technician time on site versus on road. When cleaning time rises and drive time falls, weekly capacity improves without adding labor, which helps cash flow cover fixed costs and owner pay faster.

3

Labor model

Crew Payroll and Utilization

Owner-led work keeps wage spend down, but it also caps weekly jobs because one person can only clean so many homes. In Year 1, the model carries $75,000 owner pay, two lead technicians at $42,000 each, three technicians at $36,000 each, and one customer service representative at $38,000, or $305,000 in annual payroll.

This driver hits owner income through utilization, or booked time actually used. If booked hours do not fill the crew, payroll turns into idle time and rework, and margin gets squeezed. By Year 5, payroll scales to $11 million, so pricing, route density, and handoffs have to support the team or the owner’s draw gets crowded out.

Track Hours Before You Hire

Measure billable hours per tech, jobs per route, and callback rate. The key test is simple: hired hours must be backed by booked work, not hope. A full crew only helps income when cleaner time, drive time, and admin time stay aligned with revenue.

- Price by home size and condition.

- Watch labor as % of revenue weekly.

- Cut rework with clear handoffs.

- Add staff only after route fill-up.

One underbooked crew day can erase the wage savings you thought you earned.

4

Recurring accounts

Recurring Accounts

Recurring accounts mean repeat cleaning from mobile home parks, property managers, landlords, investors, and homeowners who book on a schedule. This driver smooths revenue, lifts route density, and cuts the cost to win each new job: model customer acquisition cost falls from $85 in Year 1 to $65 in Year 5, while marketing drops from 18% to 10% of revenue.

That steadier schedule helps crews stay booked, which supports take-home pay because less time is lost to gaps and more jobs fit into each route. The catch is concentration risk: one property manager can’t become too large a share of sales, or one account loss can hit cash flow fast. One big account is not the same as a stable base.

Track repeat revenue by source

Measure recurring revenue by account type, renewal rate, and share of total sales. Track how many jobs come from parks, managers, landlords, and repeat owners, then watch whether the same account type starts to dominate. Use that mix to forecast labor, fuel, and owner draw without overcounting any one relationship.

To improve this driver, lock in service dates, document scope, and test simple packages that fit route planning. Predictable timing helps fill a route with fewer dead miles and better crew use. Keep one account under control, though: if a single property manager gets too big, revenue can look stable right up until it isn’t.

- Track CAC by account source.

- Watch marketing as % of sales.

- Limit concentration by client.

- Book same-day nearby homes.

5

Overhead, reserves, and cash discipline

Overhead, reserves, and cash discipline

Cash on hand is not the same as owner pay. With $7,500 in fixed overhead each month, the business has to cover office, vehicle insurance, software, business insurance, professional services, communications, training, and storage before any draw. The model also carries $220,000 in startup capex, needs $339,000 minimum cash in Month 31, and reaches payback in 57 months.

Reserves are what keep income steady. They need to cover equipment replacement, slow months, callbacks, and payroll timing. If reserves are thin, the owner can look profitable on paper and still miss bills in cash. One clean rule: don’t treat leftover cash as income until overhead is covered and reserve targets are funded.

Track cash, not just profit

Build a rolling 13-week cash forecast and watch minimum cash, not just month-end profit. Separate reserve buckets for equipment replacement, slow weeks, callbacks, and payroll timing. If the reserve can’t absorb one bad month, the owner draw is too high.

Use a simple gate: cover $7,500 monthly overhead first, then fund reserves, then pay the owner. Track how much cash is needed to keep payroll and vendors current, especially if jobs slip or callbacks rise.

- Forecast cash weekly.

- Ring-fence reserve money.

- Delay owner draws early.

6

Compare low, base, and high owner-income scenarios

Owner income scenarios

Owner income shifts with marketing spend, mix, and reserves. The low case protects the plan, the base case waits for breakeven, and the high case shows profit after cash catches up.

| Scenario | Low CaseDownside case | Base CasePlanning case | High CaseUpside case |

|---|---|---|---|

| Launch model | This case keeps owner pay fixed while Year 1 stays under heavy EBITDA pressure. | This case assumes the model reaches breakeven in Month 22 and starts supporting cautious distributions after reserves. | This case assumes the business reaches Year 4 scale with much stronger EBITDA, but cash still lags profit. |

| Typical setup | Year 1 runs on $75,000 owner pay, $85 CAC, 18% marketing, and negative EBITDA of $194,000 before reserves. | By Year 3, EBITDA turns positive at $32,000, with marketing down to 14%, CAC at $72, and billable hours per active customer rising from 3.5 to 4.0. | Year 4 EBITDA reaches $380,000 as marketing falls to 12%, CAC drops to $68, and higher-margin premium and all-inclusive work takes more share, but payback is still 57 months and the cash trough hits $339,000 in Month 31. |

| Cost drivers |

|

|

|

| Owner income rangeBefore owner reserves | $75,000Planned pay | Salary plus small drawReserve-aware draw | Strong draw after reservesUpside with discipline |

| Best fit | Use this to test how long the business can absorb losses before owner pay must slow. | Use this for a conservative operating plan with little room for owner distributions. | Use this if you can fund growth, keep reserves high, and wait for cash to catch up. |

Planning note: Scenario ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions.

Related Products

- Mobile Home Cleaning Porter's Five Forces Analysis

- Mobile Home Cleaning BCG Matrix

- Mobile Home Cleaning Business Model Canvas

- 7 Essential KPIs to Track for Mobile Home Cleaning Profit

- Mobile Home Cleaning Business Plan Template in Pre-Written Word

- 7 Proven Strategies to Boost Mobile Home Cleaning Profit Margins

- How to Run Mobile Home Cleaning: 2026 Monthly Operating Costs

- Mobile Home Cleaning Startup Costs: $173K+ CAPEX Planning Guide

- Mobile Home Cleaning Financial Model Template in Excel

- How to Start a Mobile Home Cleaning Service in 1–3 Months

- How to Write a Mobile Home Cleaning Business Plan: 7 Actionable Steps

- Mobile Home Cleaning Marketing Mix

- Mobile Home Cleaning Marketing Plan

- Mobile Home Cleaning Business Proposal

- Mobile Home Cleaning PESTEL Analysis

- Mobile Home Cleaning Pitch Deck Example Editable PPTX

- Mobile Home Cleaning Business SWOT Analysis

- Mobile Home Cleaning Value Proposition Canvas

Frequently Asked Questions

The model includes $75,000 in annual owner/general manager pay, but extra take-home depends on cash after expenses, reserves, and reinvestment EBITDA is negative in Year 1 and Year 2, then reaches $32,000 in Year 3 and $380,000 in Year 4 Treat profit distributions as conditional, not salary