Owner income($40k)

Owner income($40k)How Much Mobile Wallet Owners Can Make: $115M Year 1 Surplus

Fully Editable

Instant Download

Professional Design

Pre-Built

No Expertise Is Needed

Description

Owner income($40k)  Net margin93%

Net margin93% Revenue for target pay$1.44M

Revenue for target pay$1.44M Business difficultyHard

Business difficultyHard

Key Takeaways

- Funded users, not downloads, drive revenue.

- Transaction volume scales fast with regular users.

- Take rate matters less than volume and subscriptions.

- CAC, compliance, and processing costs decide payback.

Owner income($40k)Net margin93%Revenue for target pay$1.44MBusiness difficultyHardWhat would your wallet pay you?

Owner income calculator

Estimate owner take-home and the target-pay gap from revenue, margin, costs, reserves, and target pay.

Planning note: This is a researched planning estimate only. It is not guaranteed salary, tax advice, or owner distribution advice.

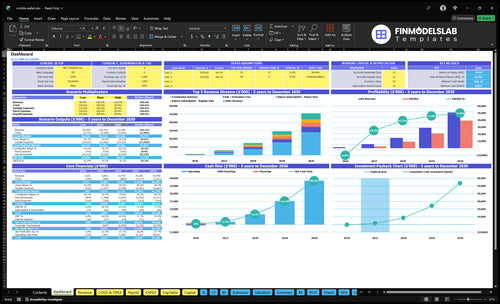

Can you check owner income in the Mobile Wallet model?

The dashboard shows revenue, gross margin, costs, reserves, and owner take-home assumptions in the Mobile Wallet Financial Model Template. Open it.

Owner-income model highlights

- Owner pay capacity tab

- Buyer, seller, volume tabs

- Revenue, COGS, payroll, reserves

- Charts test $166M-$4.256B

How do mobile wallets make money?

Mobile Wallet makes money from fee capture, not from the full amount processed. The model uses a $0.10 fixed order fee, a 1.50% to 1.30% variable commission, buyer subscriptions from $0 to $600 per month, seller subscriptions from $19 to $120 per month, seller ads from $50 to $90, and premium tools from $0 to $55.

Core payment income

- $0.10 fixed fee per order

- 1.50% to 1.30% commission on value

- Revenue rises with order count

- Take rate drives owner income

Extra revenue streams

- Buyer subscriptions: $0 to $600

- Seller subscriptions: $19 to $120

- Seller ads: $50 to $90

- Premium tools: $0 to $55

Can a mobile wallet pay its owner?

Yes, Mobile Wallet can pay its owner, but only after funded active usage covers marketing, payment costs, compliance, fraud, payroll, and reinvestment. In the first-year assumptions, 50,000 buyers and 600 sellers produce $166M revenue, a 93% gross margin, and $115M before unprovided fixed costs; What Is The Main Metric That Reflects The Success Of Mobile Wallet? shows the usage metric that drives that pay capacity.

Owner Pay Rule

- Pay salary through payroll

- Take distributions after profit

- Fund reserves before payouts

- Reinvest before excess cash

Quick Math

- Formula: costs plus salary ÷ margin

- $120k salary needs coverage first

- 93% margin lowers the hurdle

- Weak activation raises it fast

What costs reduce mobile wallet owner income?

If you’re pricing owner take-home for a Mobile Wallet, the main drains are COGS, marketing, payroll, payment gateway fees, cloud hosting, data security, and compliance. See How Much Does It Cost To Open And Launch Your Mobile Wallet Business? In year 1, COGS is 7% of revenue, then 5% by Year 5, while marketing rises from $400k total in Year 1 to $41M in Year 5; fraud, legal, audits, insurance, support, engineering, and reserves are not quantified, so they must be subtracted separately.

Quantified cost drains

- COGS: 7% in Year 1

- COGS: 5% by Year 5

- Marketing: $400k in Year 1

- Marketing: $41M in Year 5

Other income cuts

- Payment gateway fees

- Cloud hosting and data security

- KYC/AML checks and fraud losses

- Legal, audits, insurance, support

Which drivers decide wallet owner income?

1

50K/600Active Users

A first-year base of 50,000 buyers and 600 sellers sets the revenue ceiling, so more funded users means more owner income.

2

2-14xRepeat Spend

More orders per user and higher ticket sizes multiply payment volume without adding much fixed cost.

3

$0.10+1.5%Monetization

The fixed fee, variable fee, and subscriptions decide how much of each transaction becomes revenue.

4

7%Cost Control

Payment gateway and cloud security costs start near 7% of revenue and fall over time, which protects margin.

5

$824KCompliance Burn

Year 1 payroll and overhead are about $824K before variable costs, so breakeven depends on tight compliance and lean staffing.

6

$5/$250CAC Retention

Low buyer CAC and seller CAC only work if repeat use stays strong enough to pay back marketing spend.

Mobile Wallet Core Six Income Drivers

Active Funded Users

Active Funded Users

Active funded users are the buyers and sellers who are verified, funded, and actually transacting. Here, $250k of buyer marketing at $5 CAC can create 50,000 buyers, and $150k of seller marketing at $250 CAC can create 600 sellers. Downloads alone do not pay the owner. If activation is weak, revenue per user falls, and payback on acquisition spend gets slower, which presses cash flow and owner draw.

The mix matters too: the model shifts from 60% casual users in Year 1 to 40% in Year 5, with regular and power users driving more revenue. More funded users raise repeat transactions, while casual-only users inflate user counts without lifting profit. What this hides: onboarding delays, KYC friction, and failed funding can block revenue even after downloads land.

Track Activation, Not Downloads

Track verified users, funded users, and first transaction rate by cohort. Use inputs for buyer CAC, seller CAC, funded-user conversion, repeat purchase rate, and user mix across casual, regular, and power tiers. If a cohort does not fund and transact fast, trim spend or fix onboarding. The goal is simple: more active funded users per marketing dollar.

- Verified-user conversion

- Funded-user rate

- First transaction rate

- Repeat purchase rate

- Buyer and seller CAC

When active funded users rise, transaction volume, subscription take, and seller tool sales rise with them. When they stall, fixed support and compliance spend stay in place, so profit and owner pay shrink fast. In this model, a better mix toward regular and power users matters more than raw downloads.

1

Transaction Volume

Transaction Volume

Transaction volume is the order count and ticket size that turn active funded users into gross transaction volume. In this model, Year 1 produces about $1,125M GTV from 185,000 modeled orders, and Year 5 reaches about $4,384M from 553M orders. GTV is not revenue; the wallet only keeps the fixed fee, commission, subscriptions, and other monetized fees.

The key inputs are active funded users, transactions per user, average order value, and the mix of casual, regular, and power users. Small changes in regular and power user frequency matter more because those users place more orders and spend more per order. Volume is the top line engine, but only monetized volume pays the owner.

Track Orders and AOV by User Type

Measure orders per active user, average order value, and the share of volume from regular and power users. Forecast GTV as active users × transactions per user × AOV, then layer in the take rate to see cash available for payroll, support, and owner draws. If the mix shifts toward low-frequency users, revenue quality drops fast.

Push repeat use first. Improve discovery, checkout speed, and trust so regular and power users buy more often and buy larger baskets. What this estimate hides is that a big GTV number can still miss owner income if monetized fees stay thin or if repeat orders stall after sign-up. Keep segment-level reporting on by week, not just by month.

2

Monetization Rate

Monetization Rate

Monetization rate is the share of wallet activity the business keeps as revenue. Here it comes from a $0.10 fixed fee per order, a variable commission that declines from 1.50% in Year 1 to 1.30% in Year 5, plus buyer plans at $2.99 to $6 a month and seller plans at $19 to $120. More paid users and more orders lift owner income; downloads alone do not.

Here’s the quick math: 10,000 orders add $1,000 from the fixed fee alone. At $100,000 in wallet spend, the variable commission adds $1,300 to $1,500 before subscriptions, ads, and premium tools. If paid user mix stays thin, revenue per user falls and cash for owner pay gets tight even when transaction volume looks strong.

Raise revenue per order

Track orders, average order value, paid buyer count, paid seller count, and ad or tool attach rate every month. Split revenue by casual, regular, and power users so you can see which segment actually pays. If the variable commission drops, you need either more volume or more subscriptions to keep profit and owner draw moving up.

Test fee changes against checkout conversion and subscription uptake, not just gross transaction value. The model can still work with a lower take rate if volume, subscriptions, and seller services grow faster than costs. If seller tools and buyer plans don’t convert, the business leans too hard on volume and the owner’s cash flow gets more fragile.

3

Processing, Network, and Fraud Costs

Processing, Network, and Fraud Costs

Processing, network, and fraud costs are the cut taken before the owner sees cash. In the model, gateway fees fall from 40% of revenue in Year 1 to 30% in Year 5, while cloud and security fall from 30% to 20%; modeled gross margin still only moves from 93% to 95%.

Fraud losses, chargebacks, failed payments, dispute handling, and screening are not included, so they need separate inputs. On the provided $4,256M revenue base, the model says each extra 1% cost is about $426k less before owner pay, so small slippage can hit take-home fast.

Track the true cost per payment

Measure costs by gateway fees, cloud and security, fraud losses, chargebacks, and failed payments. Tie each one to revenue so you can see margin by user type and order flow, not just by total spend.

- Track cost as a revenue percent.

- Separate fraud from processing.

- Watch dispute and screening costs.

- Test margin before owner draw.

Here’s the quick check: if a control cuts cost by 1%, it can protect about $426k before owner pay on the model’s revenue base. If fraud or failed payments rise, the gross margin gain from cheaper hosting gets eaten before it reaches profit.

4

Compliance and Operating Burn

Compliance Burn

KYC/AML (know-your-customer/anti-money laundering) checks, legal review, audits, security work, support, engineering, insurance, and cloud spend decide the real break-even point. The model already assumes cloud and security at 30% of revenue in Year 1, easing to 20% by Year 5, but it leaves payroll, legal, audits, and compliance staffing out. Owner pay only starts after those costs are covered.

That means top-line growth can still leave thin cash if transaction volume rises faster than compliance headcount. If revenue grows but support tickets, fraud review, or audit work scale one-for-one, operating burn can eat the pre-fixed surplus. Plan income after fully loaded overhead, not after gateway or cloud spend alone.

Measure Burn Before Draw

Track compliance cost as a percent of revenue, plus fixed overhead per month. Break it into verified users, transactions, support tickets, audit hours, and cloud bills so you can see which line moves with activity and which does not.

Use a simple rule: if added revenue does not cover cloud, security, payroll, legal, audits, and insurance, don’t lift owner draw. Test staffing and vendor spend against live order volume, because break-even changes fast when verification, disputes, or reviews spike.

- Track fully loaded compliance burn.

- Separate fixed and variable overhead.

- Reprice when review volume rises.

- Delay owner pay until coverage holds.

5

Customer Acquisition and Retention

Customer Acquisition and Retention

CAC payback decides whether growth funds the owner or drains cash. Buyer CAC improves from $500 to $350, and seller CAC from $250 to $190, but those gains only help if users verify, fund, and keep transacting. Marketing spend rises from $400k in Year 1 to $41M in Year 5, so weak activation can turn spend into a cash drag fast.

Retention is the second half of the math. Paid buyer subscriptions and repeat orders create recurring revenue, so the owner gets paid more when customers come back. If users churn before the second use, CAC becomes a cash leak and reserve needs rise. The key inputs are CAC, funded-user conversion, repeat order rate, and subscription renewal rate.

Track payback, not just signups

Measure CAC payback period by channel and user type, then compare it with repeat purchase timing and subscription renewal timing. A signup is not income until it becomes a funded, transacting user. The owner should watch verified users, repeat orders, and paid retention together, because one weak step lowers revenue quality and raises cash needs.

- Track CAC by buyer and seller

- Measure first repeat order rate

- Watch subscription renewal by cohort

- Cut spend on slow-payback channels

Here’s the quick test: if CAC falls but repeat use does not rise, owner income still stays under pressure. The platform should only scale channels that bring back users fast enough to cover acquisition spend before the next cash cycle.

6

Compare lean, base, and high-growth mobile wallet income scenarios

Owner income scenarios

Owner income moves with buyer and seller scale, repeat orders, and margin. Payroll, compliance, fraud reserves, taxes, debt, and reinvestment still cut into what the owner keeps.

| Scenario | Low CaseLow Case | Base CaseBase Case | High CaseHigh Case |

|---|---|---|---|

| Launch model | This is the lower earnings path built from first-year assumptions. | This is the modeled earnings path using year 3 assumptions. | This is the stronger earnings path if scale and margin both hold. |

| Typical setup | First-year setup with 50,000 buyers, 600 sellers, 185,000 orders, $1,125M GTV, $166M revenue, 93% gross margin, and $400k marketing. | Year 3 setup with 300,000 buyers, 2,619 sellers, 146M orders, $958M GTV, $1,239M revenue, 94% gross margin, $743k COGS, and $175M marketing. | Year 5 setup with 857,143 buyers, 5,789 sellers, 553M orders, $4,384M GTV, $4,256M revenue, 95% gross margin, $213M COGS, and $41M marketing. |

| Cost drivers |

|

|

|

| Owner income rangeBefore owner reserves | About $115M pre-deductionLow Case | About $99M pre-deductionBase Case | About $3.6B pre-deductionHigh Case |

| Best fit | Use this to stress-test launch-month cash and slower adoption. | Use this as the main planning case for a scaled operating run. | Use this to test upside if scale stays strong and reinvestment still works. |

Planning note: These scenario ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions.

Related Products

- Mobile Wallet Porter's Five Forces Analysis

- Mobile Wallet BCG Matrix

- Mobile Wallet Business Model Canvas

- 7 Core Financial KPIs for Mobile Wallet Growth

- Mobile Wallet Business Plan Template in Pre-Written Word

- Increase Mobile Wallet Profitability with 7 Focused Financial Strategies

- Analyzing Mobile Wallet Running Costs and Path to Profitability

- Mobile Wallet Startup Costs: Plan Around $400k In Year 1 Marketing

- Mobile Wallet Financial Model Template in Excel

- How To Launch A Mobile Wallet App In The US In 6–12+ Months

- How to Write a Mobile Wallet Business Plan: 7 Steps to Funding

- Mobile Wallet Marketing Mix

- Mobile Wallet Marketing Plan

- Mobile Wallet Business Proposal

- Mobile Wallet PESTEL Analysis

- Mobile Wallet Pitch Deck Example Editable PPTX

- Mobile Wallet Business SWOT Analysis

- Mobile Wallet Value Proposition Canvas

Frequently Asked Questions

The provided first-year model shows about $115M before payroll, compliance, fraud reserves, taxes, debt, and reinvestment That comes from $166M revenue, 93% gross margin after gateway and cloud costs, and $400k total marketing Actual owner take-home can be much lower if staffing and compliance costs are heavy