How Much Does It Cost To Start A Mortgage Brokerage? $818k Base

You’re budgeting a mortgage brokerage before the first loan closes, so the real number is more than laptops and desks This outline covers researched startup-cost assumptions for a 60-month model, including $107,000 in setup outlays, $818,000 in minimum cash need by Month 2, and the working capital needed through the early ramp-up period It excludes borrower loan funding, warehouse lending facilities, and lender capital because brokers typically arrange loans rather than fund them directly

Estimate Startup Costs with Calculator

Startup CAPEX Calculator

Estimates the one-time capitalized startup assets needed before launch, not operating cash.

CAPEX only Excludes inventory, payroll runway, debt service, deposits, working capital, marketing spend, software subscriptions, licensing fees, bond premiums, and other operating expenses.

Does this Mortgage Brokerage model show startup cash needs?

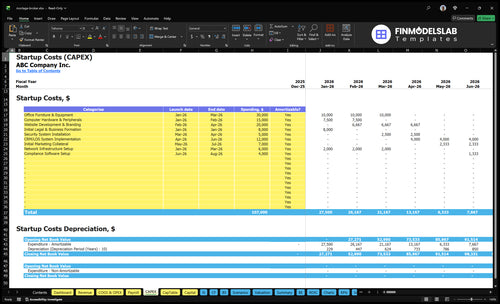

This screenshot shows the financial model tab in the Mortgage Brokerage Financial Model Template, with $107,000 CAPEX, hard asset lines, expense categories, and working capital laid out. It tracks Month 1–8 launch timing, depreciation/amortization, commission ramp-up, the 60-month cost ramp, and $818,000 minimum cash in Month 2—open it to test CAC, marketing, payroll, office, licensing, and breakeven.

Key screenshot checks

- 107k setup outlays

- Month 1-8 timing

- Month 2 cash floor

What are the biggest costs to start a mortgage brokerage?

There’s no single biggest cost for a Mortgage Brokerage; the biggest line item depends on how many people you hire, how much you spend to get a loan customer, and how wide your state footprint is. Here’s the quick math: year-1 staffing for a CEO, senior mortgage advisor, and loan processor is $275,000, while marketing is $150,000 with a $1,200 CAC (customer acquisition cost). Office rent runs $7,500 per month, tech adds $1,800 per month plus $12,000 to implement and 0.8% revenue-based transaction fees, and multi-state licensing can push up compliance, bond, and legal review costs.

Big cost drivers

- Staffing can lead at $275,000 Year 1

- Marketing can hit $150,000

- CAC is about $1,200

- Rent is $7,500 monthly

Model choices

- Tech costs $1,800 monthly

- Setup is $12,000

- Transaction fees are 0.8%

- State expansion raises legal costs

How much money do you need to start a mortgage brokerage?

You need at least $818,000 in cash by Month 2 to start a Mortgage Brokerage, because this is a working-capital business, not an equipment-heavy launch. Here’s the quick math: $107,000 setup outlays, $192,600 annual fixed costs, $275,000 Year 1 salary base, and $150,000 Year 1 marketing, with commissions lagging lead spend and payroll; compare demand context here: What Is The Current Growth Rate For Mortgage Brokerage?. Brokers usually don’t fund borrower loans directly, but they still need cash through Month 3 breakeven and a 5-month payback.

Cash Need

- $818,000 minimum by Month 2

- $107,000 setup outlays

- $192,600 annual fixed costs

- $275,000 Year 1 salaries

Why So High

- $150,000 Year 1 marketing

- Lead spend comes before closings

- Payroll runs before commissions clear

- Cash bridges Month 3 breakeven

What hidden costs of starting a mortgage brokerage should founders budget for?

If you’re budgeting for Mortgage Brokerage, the hidden costs are not just licenses; they split into one-time setup and monthly working capital. For a broader profit check, read How Much Does The Owner Of Mortgage Brokerage Make? before you price the launch.

Pre-opening costs

- $8,000 legal and formation

- $4,000 compliance software setup

- NMLS filings and state applications

- Background checks, testing, manuals

Monthly working capital

- $1,300 compliance and licensing fees

- $1,000 insurance each month

- $1,200 IT and cybersecurity support

- 0.4% of Year 1 revenue for checks

Calculate Fuding Needs

Startup cost summary

Shows setup outlays, launch costs, and excluded cash needs for a mortgage brokerage across low, base, and high scenarios.

| Cost Category | Base Estimate | Main Cost Driver | CAPEX Calculator |

|---|---|---|---|

| Office setup and equipment | $41,000 | Furniture, security, and network install | Yes |

| Technology stack implementation | $31,000 | Hardware, CRM/LOS, and compliance tools | Yes |

| Website and branding launch | $20,000 | Website build and brand assets | Yes |

| Licensing and compliance setup | $8,000 | Formation and legal filings | Yes |

| Initial marketing collateral | $7,000 | Launch collateral and promotion | Yes |

| Month 2 cash reserve | $818,000 | Month 2 runway for fixed costs and startup losses | No |

Mortgage Brokerage Core Five Startup Costs

Licensing, Regulatory, And Compliance Startup Expense

License Setup

Licensing starts with company filings, state applications, and, where required, individual mortgage loan originator licensing through the Nationwide Multistate Licensing System and Registry (NMLS). Plan about $8,000 for legal and business formation, plus $4,000 for compliance software setup. The range moves with state count, license type, background checks, testing, renewals, policies, and legal review.

First-Year Cost

Here’s the quick math: $1,300/month in compliance and state licensing fees equals $15,600/year. Add the $8,000 legal work and $4,000 software setup, and the base first-year load is about $27,600 before state-specific filings. That helps cash planning, but it still hides how many states you’ll license and whether MLO coverage is required.

- Count states before budgeting

- Separate setup from renewals

- Price MLO coverage separately

Trim Waste

Keep costs down by licensing only where you can close loans, then adding states after volume supports it. Use one policy pack, one renewal calendar, and one vendor stack. The common mistake is buying every license on day one. Smart sequencing can trim wasted setup spend, but it won’t remove filing, testing, or background-check costs.

- Map launch states first

- Reuse policy templates

- Track renewal dates monthly

Ongoing Control

Don’t cut legal review or compliance software. The $4,000 setup should cover tracking, document control, and license dates, while counsel checks company filings, MLO rules, and state notices. Set the recurring $1,300 aside as a fixed operating line; if headcount or state count rises, compliance load rises with it.

Technology Stack And Systems Startup Expense

Core Stack Build

The core stack has a $53,000 one-time build before monthly fees. That covers $12,000 for customer relationship management system and loan origination system implementation, $20,000 for website and branding, $15,000 for hardware, and $6,000 for network gear. Price it from vendor quotes, user seats, and integration count. One line: the build is front-loaded.

Monthly Software

Base software runs about $1,800 per month, plus $1,200 for IT support and cybersecurity, so budget $3,000 monthly before usage fees. This should cover the loan origination system, CRM, borrower portal or point-of-sale, document management, e-signature, pricing engine access, credit reporting, website, business email, and security tools. One line: recurring spend never sleeps.

Website And Devices

The $20,000 website and branding line is separate from the $15,000 hardware and $6,000 network setup. Use quotes for laptops, monitors, routers, and secure setup labor, then decide what stays in the office and what can run remote. Cut scope, not security.

Usage Fees

Variable tech fees can move fast. Budget 08% in Year 1 loan origination system transaction fees and 04% for credit report and verification fees. Estimate from closed-loan volume, credit pulls per file, and lender workflow. One line: volume, not headcount, drives this line.

Keep It Lean

To keep quality high, buy only the modules you need now, delay custom work, and ask for setup, per-seat, and integration charges in writing. The common mistake is paying for a full stack before loan volume can support it. Keep the first release tight.

- Delay nonessential modules

- Lock per-seat pricing

- Track volume fees monthly

Insurance And Surety Bond Startup Expense

Bond Costs

A surety bond is not the same as the annual premium. For mortgage brokerage, the required bond amount changes by state and license type, so budget for surety bonds, E&O, professional liability, cyber liability, general liability, and workers’ compensation if you hire staff. Use $1,000 per month or $12,000 per year as the insurance line.

What to Price

Here’s the quick math: gather the state list of licenses, the number of loan originators, and quotes for each policy. The Nationwide Multistate Licensing System and Registry (NMLS) filings, background checks, renewals, and legal review all affect the spend. Keep the bond amount separate from the premium, since state rules set the bond and insurers price the policy.

Keep It Lean

Keep the policy stack tight. Ask for one package quote, then compare cyber, E&O, and general liability with the same deductible and limits. Tie cyber coverage to the $1,200 monthly IT support line, because secure borrower document handling lowers loss risk. Don’t guess bond premiums without state data; that’s how budgets drift.

Budget Timing

Book this as operating spend, not hard capex. The $12,000 annual insurance line sits beside compliance and software costs, and it should be funded before the first closed loan because renewals, NMLS fees, and staffing changes can hit early. If you hire staff, add workers’ compensation from day one.

Office, Remote Work, And Physical Setup Startup Expense

Remote First

A lean remote setup keeps cash tied up in computers, phones or headsets, secure storage, and networking, not rent. For a mortgage brokerage, that means your hard-asset block can stay close to $56,000 if you buy the listed furniture, hardware, security, and network items, while rent stays off the startup budget.

Office Buildout

The core office setup includes $30,000 for office furniture and equipment, $15,000 for computer hardware and peripherals, $5,000 for security system installation, and $6,000 for network infrastructure. Treat those hard assets as CAPEX and keep monthly rent, deposits, utilities, and supplies outside it.

Control Spend

To keep the setup lean, buy only what supports file handling, client calls, and secure storage. The monthly run rate is the easier part to trim: $7,500 rent, $800 utilities and internet, and $450 office supplies. One clean rule: don’t put rent deposits into CAPEX.

Branch Model

A fuller branch setup adds fixed overhead fast. Here’s the quick math: $7,500 monthly rent plus $800 utilities and internet plus $450 supplies equals $8,750 a month before payroll. If loan volume is still thin, that fixed base can squeeze cash, so the office should scale only when production is steady.

Marketing, Lead Generation, And Staffing Readiness Startup Expense

Working capital first

Marketing and payroll are pre-opening working capital, not CAPEX. For a mortgage brokerage, that means funding website launch, local search, paid leads, referral outreach, onboarding, and base pay before commissions land. Here, the Year 1 stack is $150,000 marketing, $275,000 base payroll, and $20,000 website and branding, so cash must be in place before the first closed-loan check arrives.

Marketing budget build

The marketing budget covers $7,000 in initial collateral, $20,000 for website development and branding, and ongoing lead spend tied to a $1,200 Year 1 CAC. Here’s the quick math: $150,000 divided by $1,200 equals about 125 customer acquisitions. The real cost is higher because 70% of Year 1 spend goes to lead generation and referral fees.

- Start spend before revenue closes

- Track CAC by source

- Separate brand and lead costs

Staffing ramp

Staffing re adiness means paying for loan officers, processors, onboarding, and support before commissions stabilize. The key number is 180% mortgage advisor commissions plus $275,000 base payroll, so early payroll pressure can outrun loan closings. Keep hiring tied to pipeline volume, and do not add fixed headcount faster than funded deals.

- Hire to pipeline, not hope

- Use contractors for overflow

- Delay full team expansion

Cash timing risk

The main risk is timing, not just amount. Lead spend starts first, then staffing, then commission revenue. If your close cycle slips, the brokerage still pays the $150,000 marketing plan, the $275,000 payroll base, and the 180% commission load before cash comes back from lenders.

Compare 3 Startup Cost Scenarios

Startup cost scenarios

Mortgage brokerage costs swing with rent, payroll, licensing, and lead generation. These three launch paths show how a solo start, a small team, or a larger branch changes cash need.

| Scenario | Lean LaunchSolo broker fit | Base LaunchTeam launch fit | Full LaunchScale-up fit |

|---|---|---|---|

| Launch model | Owner-led, remote-first brokerage with reduced office and support spend. | Small-team brokerage with the model's $818,000 minimum cash and Year 1 office setup. | Multi-state, larger-footprint brokerage with more staff and heavier lead generation. |

| Typical setup | Lower rent, less furniture, and minimal non-owner payroll keep cash needs down. | Uses $107,000 setup outlays, $7,500 monthly office rent, three Year 1 roles, and $150,000 marketing. | Adds more office space, more advisors and processors, and a bigger marketing push than the base case. |

| Cost drivers |

|

|

|

| Planning rangeCAPEX only | Below $818,000Lowest cash need | About $818,000Model baseline | Above $818,000Highest cash need |

| Best fit | Fits a founder who wants to start small and keep fixed costs tight. | Fits a founder building a staffed brokerage with a normal office and marketing plan. | Fits operators planning faster growth and a broader market reach from day one. |

Planning note: These ranges are researched planning assumptions, not exact quotes or lender offers.

Related Products

- Mortgage Brokerage Porter's Five Forces Analysis

- Mortgage Brokerage BCG Matrix

- Mortgage Brokerage Business Model Canvas

- 7 Essential KPIs to Track for Mortgage Brokerage Success

- Mortgage Brokerage Business Plan Template in Pre-Written Word

- How to Increase Mortgage Brokerage Profitability in 7 Practical Strategies

- How Much Does It Cost To Run A Mortgage Brokerage Each Month?

- Mortgage Brokerage Financial Model Template in Excel

- How Much Mortgage Brokerage Owners Make: $150k Pay Plus Profit

- How To Open A Mortgage Brokerage In 8–16 Weeks With A Launch Roadmap

- How to Write a Mortgage Brokerage Business Plan in 7 Steps

- Mortgage Brokerage Marketing Mix

- Mortgage Brokerage Marketing Plan

- Mortgage Brokerage Business Proposal

- Mortgage Brokerage PESTEL Analysis

- Mortgage Brokerage Pitch Deck Example Editable PPTX

- Mortgage Brokerage Business SWOT Analysis

- Mortgage Brokerage Value Proposition Canvas

Frequently Asked Questions

The researched base case needs $818,000 in minimum cash by Month 2 That reflects more than setup costs: it has to cover $16,050 in monthly fixed costs, about $22,917 in average monthly Year 1 payroll, and $12,500 in average monthly Year 1 marketing while leads convert into closings