Owner income$6.1M

Owner income$6.1MHow Much Can an NPS Survey Tool Owner Make? $120k Plus Profit Upside

Fully Editable

Instant Download

Professional Design

Pre-Built

No Expertise Is Needed

Description

Owner income$6.1M  Net margin56%

Net margin56% Revenue for target pay$214k

Revenue for target pay$214k Business difficultyMedium

Business difficultyMedium

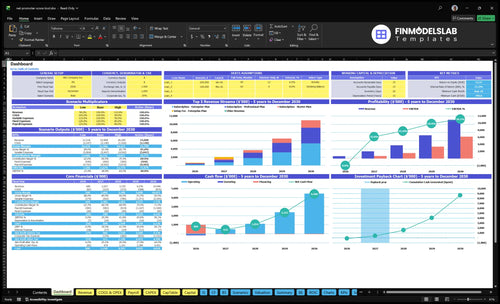

An NPS survey tool owner can model take-home as a salary plus possible distributions after reserves, taxes, and reinvestment In the researched case, owner salary is $120,000 per year, revenue is $680,000 in the first year, and EBITDA is -$49,000, so early take-home is funded by planned startup cash By Year 5, revenue reaches $10946 million and EBITDA reaches $6145 million, but that profit is not automatically owner income The business reaches breakeven in Month 8 and payback in 18 months under the modeled assumptions

Owner income$6.1MNet margin56%Revenue for target pay$214kBusiness difficultyMediumWant to test your own NPS survey tool income?

Owner income calculator

Estimate owner take-home and the target-pay gap from revenue, margin, costs, reserves, and target pay.

Planning note: This is a researched planning estimate, not guaranteed salary, tax advice, or owner distribution advice.

How do you check owner income in the Net Promoter Score Survey Tool model?

Open the Net Promoter Score Survey Tool Financial Model Template to review revenue, EBITDA, cash, breakeven, payback, and owner income; charts show Y1 revenue $680,000, Y3 revenue $3,720 million, Y5 revenue $10,946 million, and EBITDA from -$49,000 to $6,145 million—open the model.

Owner-income model highlights

- Owner take-home output included

- Revenue and EBITDA trend

- Pricing, churn, CAC inputs

- Fixed costs, capex, reserves

Can a small NPS survey tool be profitable?

Yes, a Net Promoter Score Survey Tool can be profitable if retention stays strong, support load stays light, and acquisition cost stays under control. The model reaches breakeven in Month 8, then builds to $709,000 EBITDA in Year 2, $1.554 million in Year 3, and $6.145 million in Year 5.

Profit path

- Breakeven: Month 8

- Year 2 EBITDA: $709,000

- Year 3 EBITDA: $1.554 million

- Year 5 EBITDA: $6.145 million

Main risks

- Year 1 overhead: 20% of revenue

- Cloud hosting and support tools

- Payment fees and referral commissions

- Feature requests, integrations, churn, security work, pricing pressure

How much revenue does an NPS survey tool need to pay the owner?

A Net Promoter Score Survey Tool needs about $697,000 in annual revenue to support a $120,000 owner salary under this model; for startup cost context, see How Much To Start Net Promoter Score Survey Tool Business?. At $680,000 Year 1 revenue, EBITDA is still -$49,000, so cash cushion matters until breakeven in Month 8.

Owner Pay Math

- Owner salary: $120,000

- Year 1 revenue: $680,000

- EBITDA: -$49,000

- Salary-supported revenue: ~$697,000

Cost Drivers

- Contribution margin: ~80%

- Fixed overhead: $90,000

- Non-owner payroll: $227,500

- Marketing budget: $120,000

How does the owner role affect NPS survey tool income?

If the owner runs product and stays technical, the Net Promoter Score Survey Tool can keep decisions close to customer feedback, but that role costs $120,000 a year. The model still carries a $110,000 senior full stack engineer in Year 1 and five engineers by Year 5, so income only improves if faster delivery turns into more sales and less churn. Outsourced or delayed engineering can protect early cash, but it can slow integrations, dashboards, and compliance work.

Owner-led product

- Keeps product decisions near customers

- Reduces outside development pressure

- Speeds feedback to fixes

- Helps spot churn risks sooner

Cash tradeoff

- Adds $120,000 yearly payroll

- Still includes a $110,000 engineer

- Reaches five engineers by Year 5

- Moves cash from distributions to growth

Which drivers control NPS survey tool owner income?

1

$124-$236Pricing ARPA

ARPA, or average revenue per account, rises from about $124 to $236 as plan mix moves up, so each account pays more every month.

2

$57K-$912K/moPaid MRR

More paid accounts and a richer plan mix drive MRR, or monthly recurring revenue, from about $57K a month to about $912K a month.

3

$150-$125CAC Efficiency

CAC, or customer acquisition cost, falls from $150 to $125, so each new customer takes less cash even as marketing spend scales.

4

80%-82%Gross Margin

Hosting, support, and fee loads stay near 18%-20% of revenue, so more sales can drop through to EBITDA.

5

TBDRetention Churn

Churn is not provided, so renewals are a key swing factor; if they slip, the subscription base and owner income shrink fast.

6

$781KCash Policy

Breakeven lands in Month 8, and the $781K cash trough means owner draws need a cushion before cash comes out.

Net Promoter Score Survey Tool Core Six Income Drivers

Pricing And Average Revenue Per Account

Pricing and ARPA

When the tool charges more per account, monthly subscription revenue compounds and owner income rises faster. The model’s weighted ARPA is about $124 in Year 1 from 60% Starter at $49, 30% Professional at $149, and 10% Enterprise at $499. That mix matters more than list price alone, because plan mix sets cash collected each month.

By Year 5, weighted ARPA climbs to about $236 as Enterprise reaches 25% and prices move to $59, $179, and $599. Higher ARPA helps only if buyers pay for analytics, integrations, team access, and onboarding. If price hikes push churn up, the gain in revenue can get erased fast.

Track plan mix, not just price

Watch new bookings, plan upgrades, churn, and Enterprise share every month. Here’s the quick math: ARPA rises when more accounts move into higher tiers, so an extra Enterprise account can lift revenue far more than many Starter accounts. Keep price tests small, and tie them to added value like analytics or integrations.

- Track plan mix by cohort.

- Measure churn after every price change.

- Link upsells to clear features.

- Charge onboarding only when real.

If onboarding or team access is bundled well, ARPA improves without hurting retention. But if the price jump feels like a tax, churn risk rises, and that cuts recurring cash the owner can pull out as profit.

1

Paid Customers And Monthly Recurring Revenue

Paid Customers Drive Monthly Recurring Revenue

MRR only comes from active paying businesses. Free users and trial volume do not pay salaries, so the owner’s real income depends on how many accounts stay on a subscription and how much of the revenue is recurring, not one-time setup work. In the model, annual revenue of $680,000 in Year 1 implies a monthly run-rate proxy of about $56,700; that rises to $310,000 in Year 3 and $912,000 in Year 5.

Here’s the quick math: divide annual revenue by 12, then strip out any one-time enterprise fees before calling it MRR. That matters because setup cash can help this month, but it does not build next month’s base. If recurring revenue is misread, the owner can overdraw cash, underfund support, and miss the gap between booked revenue and true monthly income.

Separate Recurring Revenue From Setup Fees

Track the paying base, not vanity signups. Measure active paying businesses, recurring subscription revenue, and enterprise setup fees as separate lines. Then forecast owner pay from MRR only, since one-time fees can make revenue look stronger without improving the next month’s run-rate.

- Count active paying accounts each month.

- Split MRR and setup revenue in reports.

- Use annual revenue divided by 12 for run-rate.

If setup work rises, cash flow may improve briefly, but recurring income still sets the ceiling on hiring, support, and owner distributions. That’s the number to protect when pricing, renewals, and expansion are being reviewed.

2

Retention, Churn, And Expansion Revenue

Retention, Churn, and Expansion Revenue

For a Net Promoter Score survey tool, churn is the leak that hits owner income first. Every lost account cuts monthly recurring revenue, so the company has to replace that cash before profit can support draws. The model should treat the churn percentage as an editable input, not a hidden assumption.

Expansion helps, but only if customers stay. The Enterprise mix rises from 10% in Year 1 to 25% in Year 5, while Enterprise price moves from $499 to $599. That lift can push weighted ARPA from about $124 to $236, and lower churn protects CAC payback, support load, and sales capacity.

Track Churn by Cohort

Use net revenue growth = starting MRR + expansion MRR - churned MRR. Track logo churn, MRR churn, and upgrade rate by customer tier, then compare them by month. If enterprise customers upgrade faster but also need more support, bake that into the forecast before you raise price or add headcount.

- Review churn by tier each month.

- Separate recurring and setup revenue.

- Flag at-risk accounts before renewal.

- Test upgrades against support time.

Keep the forecast honest: when churn moves, owner income moves with it. A lower churn rate means fewer replacement sales, better cash flow timing, and a cleaner path to distributions because more of each new dollar stays in the business.

3

Customer Acquisition Cost And CAC Payback

CAC Payback

For an NPS survey tool, customer acquisition cost matters because marketing cash goes out before subscription revenue comes in. In the model, CAC improves from $150 in Year 1 to $125 in Year 5, while annual marketing spend rises from $120,000 to $12 million. That implies capacity for about 800 and 9,600 acquired customers, before churn and conversion timing.

Here’s the quick math: Year 1 ARPA is near $124 and contribution margin is 80%, so each account must recover acquisition cost fast enough to protect cash. The model’s 15-month CAC payback means growth works only if paid signups convert, stay active, and start billing without delay. If conversion slows, owner pay gets squeezed first.

Control CAC Payback

Track CAC by channel, not as one blended number. Use paid spend, sales cost, and closed-won customers to calculate CAC, then compare it with monthly contribution per account. The key inputs are ARPA, 80% contribution margin, conversion rate, and time to first bill. If CAC rises faster than ARPA, pause spend until payback stays inside target.

One clean rule: grow only when payback still fits your cash window. Keep a weekly view of marketing spend, trial-to-paid conversion, and churn, because delayed conversion makes true payback longer than the model. If you hire ahead of collections, cash flow tightens and profit can look fine on paper while owner take-home stays flat.

- Measure CAC by channel.

- Track payback monthly.

- Watch trial-to-paid lag.

- Control churn before scaling.

4

Product Delivery And SaaS Gross Margin

Survey Delivery Gross Margin

More surveys only help if delivery stays cheap. Gross margin is what’s left after variable delivery costs. In Year 1, the model assumes 8% cloud infrastructure, 4% support tools, 3% payment fees, and 5% referral commissions, or 20% total. That leaves about 80% before fixed costs and payroll, so owner income depends on keeping usage costs below plan.

The key inputs are active accounts, survey volume, support tickets, integrations, and payment mix. If dashboards, uptime, data handling, or customer support need more engineering time, margin drops fast. By Year 5, those same categories total 18%, leaving about 82%; if support load rises faster than price, the owner pays for growth with thinner cash.

Control Usage Costs

Track delivery cost per account and per survey each month. Split cloud, support tools, payment fees, and referral commissions so you can see which line moves with usage. If tickets or data jobs climb faster than revenue, tighten onboarding, cap low-margin plans, or charge more for heavy usage before margin leaks into owner pay.

- Cloud spend per survey

- Tickets per 100 accounts

- Integration hours per client

- Payment fee rate

- Referral commission rate

Here’s the quick test: if 20% of revenue goes to delivery in Year 1 and 18% by Year 5, the business earns more only when volume rises without a matching jump in support or uptime work. That gap funds customer success, engineering maintenance, and owner draw.

5

Reinvestment, Reserves, And Owner Distributions

Owner Pay vs. Cash Reserves

An NPS SaaS owner does not take home company profit as soon as the model turns positive. This plan includes a $120,000 owner salary, but cash still has to cover a $781,000 minimum balance in Month 8, with breakeven also landing in Month 8. That means distributions should wait until operating cash is safe, not just until the income statement looks good.

Here’s the quick math: initial capex totals $95,000 across software architecture, security and compliance, workstations, office setup, and CRM implementation. With 18-month payback, early profit often needs to stay inside the company for hiring, support, product work, and compliance. One clean rule: profit is not spendable cash.

Protect Cash Before Distributions

Track three things each month: cash on hand, monthly burn, and the gap between profit and free cash flow. Free cash flow is the money left after operating costs and capex, so it’s the real source of owner distributions. If Month 8 cash is trending below $781,000, hold distributions and push cash into retention, delivery, and compliance work instead.

- Test draws only after Month 8 cash stays covered.

- Ring-fence capex and compliance spend.

- Keep a reserve before hiring ramps.

- Link owner pay to cash, not book profit.

6

Compare lean, base, and mature NPS survey tool income scenarios

Owner income scenarios

Owner income moves with trial conversion, paid conversion, and plan mix. Early years can hold pay near salary, while Year 3 to Year 5 scale can fund distributions after reserves and taxes.

| Scenario | Low CaseDownside case | Base CaseCore case | High CaseUpside case |

|---|---|---|---|

| Launch model | Lower earnings keep owner pay close to salary while the business absorbs early growth costs. | Modeled midcase supports salary plus distributions as revenue and EBITDA expand. | Stronger earnings push owner take-home higher as revenue, margins, and enterprise share scale. |

| Typical setup | Year 1 revenue is $680,000, gross margin is about 80%, owner salary is $120,000, marketing is $120,000, and payroll is $347,500. | Year 3 revenue reaches $3.72 million and EBITDA reaches $1.554 million, with better conversion and a larger support and growth team. | Year 5 revenue reaches $10.946 million, gross margin is about 82%, marketing is $1.2 million, payroll is $1.185 million, and EBITDA is $6.145 million. |

| Cost drivers |

|

|

|

| Owner income rangeBefore owner reserves | Salary onlySalary only | Salary plus distributionsDistributions start | Salary plus larger distributionsLarger distributions |

| Best fit | Founders stress-testing launch cash and an owner who plans to live on salary first. | Founders modeling a normal scale-up path with some owner distributions after reserves. | Owners testing the upside case where profit can support meaningful distributions. |

Planning note: Scenario ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions.

Related Products

- Net Promoter Score Survey Tool Porter's Five Forces Analysis

- Net Promoter Score Survey Tool BCG Matrix

- Net Promoter Score Survey Tool Business Model Canvas

- What Are The Five Core KPIs For Net Promoter Score Survey Tool Business?

- Net Promoter Score Survey Tool Business Plan Template in Pre-Written Word

- How Increase Net Promoter Score Survey Tool Profitability?

- How Increase Profitability With Net Promoter Score Survey Tool?

- Net Promoter Score Survey Tool Startup Costs: Plan For $781K

- Net Promoter Score Survey Tool Financial Model Template in Excel

- How To Launch A Net Promoter Score Survey Tool In 8 To 16 Weeks

- How Increase Net Promoter Score Survey Tool Profitability?

- Net Promoter Score Survey Tool Marketing Mix

- Net Promoter Score Survey Tool Marketing Plan

- Net Promoter Score Survey Tool Business Proposal

- Net Promoter Score Survey Tool PESTEL Analysis

- Net Promoter Score Survey Tool Pitch Deck Example Editable PPTX

- Net Promoter Score Survey Tool Business SWOT Analysis

- Net Promoter Score Survey Tool Value Proposition Canvas

Frequently Asked Questions

In this model, owner pay starts with a $120,000 annual CEO and product lead salary The company shows -$49,000 EBITDA in the first year, then $1554 million in Year 3 and $6145 million in Year 5 Extra take-home depends on reserves, taxes, reinvestment, and whether profit is distributed