Owner income$150k-$1.45M

Owner income$150k-$1.45MHow Much Does a New York-Style Bagel Shop Owner Make at $150k EBITDA?

Fully Editable

Instant Download

Professional Design

Pre-Built

No Expertise Is Needed

Description

Owner income$150k-$1.45M  Net margin14%-49%

Net margin14%-49% Revenue for target pay$1.11M

Revenue for target pay$1.11M Business difficultyHard

Business difficultyHard

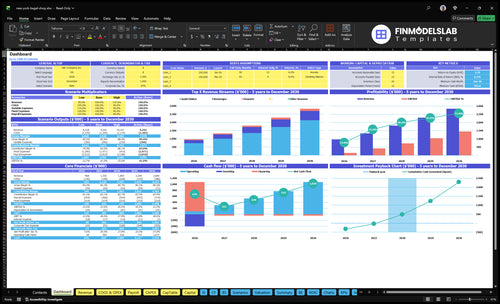

A New York-style bagel shop owner can only take home what remains after food cost, payroll, rent, fixed costs, debt service, taxes, and reserves In this model, annual revenue is about $105M in Year 1, with EBITDA of $150k before owner taxes, reserves, and debt service By Year 5, modeled revenue reaches about $283M and EBITDA reaches $1449M These are planning assumptions, not guaranteed owner income

Owner income$150k-$1.45MNet margin14%-49%Revenue for target pay$1.11MBusiness difficultyHardWant to test your owner pay target?

Owner income calculator

Estimate owner take-home and the target-pay gap from revenue, margin, costs, reserves, and your pay target.

Planning note: Research-based planning estimate only, not guaranteed salary, tax advice, or owner distribution advice.

Want to check owner income in the New York Bagel Shop model?

This New York Bagel Shop Financial Model Template shows the dashboard, income outputs, assumptions, and owner take-home math—open the model.

Owner-income model highlights

- Year 1 EBITDA: $150k

- Year 2 EBITDA: $421k

- Minimum cash need: $592k

- Breakeven: Month 4

- Cash low point: Month 6

- Payback: 26 months

How much revenue does a bagel shop need to pay the owner?

For New York Bagel Shop, the owner salary has to come from what’s left after operating costs, reserves, and debt payments. Here’s the quick math: Year 1 modeled revenue is about $105M, payroll is $367k, fixed costs are $2,142k a year, and COGS plus variable costs equal 185% of sales, so each extra $10k of owner pay needs more contribution from food, packaging, marketing, card fees, labor coverage, and rent.

Owner pay needs room

- Owner pay comes last.

- Operating costs come first.

- Debt service cuts cash next.

- Reserves still need funding.

Timing and cash strain

- Break-even hits in Month 4.

- Cash low point lands in Month 6.

- Owner salary must wait for surplus.

- Every $10k needs added contribution.

How much does a single bagel shop owner make?

A single New York Bagel Shop owner makes about $150k in Year 1 EBITDA on about $1.05M revenue, before owner taxes, reserves, debt service, and distributions; track it as operating profit, not a generic salary, alongside What Is The Most Important Metric To Measure The Success Of Your New York Bagel Shop?.

Owner Profit

- $1.05M Year 1 revenue

- $150k Year 1 EBITDA

- About 14.3% EBITDA margin

- Before taxes and debt service

Work vs. Profit

- $70k manager salary is modeled

- Owner-operated can keep that labor cost

- That pay is wages, not passive profit

- Light management must cover payroll load

Can a bagel shop owner make money without working there?

Yes, a New York Bagel Shop owner can make money without working there, but only if profit still survives the labor replacement cost. This model already includes a full-time manager at $70,000 a year, and Year 1 EBITDA is $150,000 before owner pay, debt service, reserves, and taxes. So the owner’s income starts only after those claims are covered.

Core math

- $70,000 manager pay is built in

- $150,000 EBITDA comes first

- Owner pay is not included yet

- Debt, reserves, and taxes still reduce cash

Growth tradeoffs

- Catering can lift revenue

- Wholesale can add volume

- Multiple locations can raise income

- Each adds labor, packaging, and discount risk

Want the six main income drivers?

1

295/wkCustomer Flow

Year 1 averages 295 covers a week, so even small traffic swings change profit fast.

2

$60-$80Ticket Size

Midweek checks run about $60 and weekend checks about $80, so add-ons and sandwiches lift take-home.

3

85%Menu Mix

A tight mix of bagels, cream cheese, sandwiches, and drinks protects gross margin and cuts waste.

4

$367KPayroll

Year 1 payroll is about $367K, so staffing and shift coverage decide how much revenue sticks.

5

$12K/moRent Load

Rent runs $12K a month, so the site has to earn its keep before owner income grows.

6

$150KStore Profit

Year 1 EBITDA is about $150K, which shows the income ceiling after direct costs and overhead.

New York Bagel Shop Core Six Income Drivers

Daily Customer Volume

Daily Customer Volume

Covers means paying guests served. Year 1 uses 295 weekly covers, or about 42 a day, with 20 on Monday and 70 on Saturday. Year 5 reaches 660 weekly covers, about 94 a day. More traffic lifts revenue first, but only profitable traffic helps owner take-home.

The mix matters as much as the count. Breakfast traffic, commuter flow, neighborhood repeat visits, and weekend dozen orders can change the day fast. If volume rises without enough staffing or oven capacity, service slows and waste risk rises, so cash flow can improve while profit slips.

Track covers by daypart

Measure covers by day of week, breakfast, and weekend. Match labor and bake batches to the peak, not the average. One clean rule: if Monday sits near 20 covers and Saturday near 70, build the schedule around that spread, then test whether added volume still clears labor and spoilage.

- Track covers by day and hour.

- Watch oven output per rush.

- Flag overtime and waste fast.

If traffic grows but prep or staffing lags, the extra sales can turn into slower lines and more unsold product. The goal is simple: add guests only when each extra cover still leaves room for profit after labor, product, and waste.

1

Average Ticket and Menu Mix

Average Ticket and Menu Mix

Average ticket turns foot traffic into cash. In Year 1, the model assumes $60 midweek AOV and $80 weekend AOV, rising to $75 and $95 by Year 5. The lift can come from sandwiches, coffee, cream cheese, specialty spreads, beverages, and dozen orders, but not every add-on lifts profit because eggs, meats, dairy, packaging, and prep labor take a cut.

What matters is gross profit per check, not just sales per check. If a $10 add-on needs extra labor or high-cost inputs, the owner may see bigger tickets with little extra take-home. Track the mix by daypart and keep the highest-margin items easy to sell first.

Track check lift by daypart

Measure midweek AOV, weekend AOV, and the share of tickets with coffee, sandwiches, and dozen orders. Then compare those items’ food cost, packaging, and prep time. If a bundle raises ticket size but hurts margin, reprice it or swap in lower-cost add-ons. The goal is simple: higher check, better margin, same or lower labor per order.

Use item-level sales data to see which add-ons actually improve owner income. One clean rule: if the extra dollar does not add enough gross profit to cover its labor and ingredient cost, it is not helping cash flow.

2

Gross Margin and Waste

Gross Margin and Waste

Gross margin is the money left after direct product costs. In this model, Year 1 gross margin is 85.0% and Year 5 reaches 86.4% as direct costs ease from 15.0% to 13.6%. For a bagel shop, flour, toppings, eggs, meats, dairy, paper goods, spoilage, and unsold bagels all cut owner income.

Here’s the quick math: at $1M revenue, each 1% of waste or food cost is about $10,000 a year. So a small swing in dough yield, portioning, or unsold bagels can be the difference between funding owner pay and just covering payroll and rent.

Track Waste by Batch

Measure bagels baked, bagels sold, and bagels discarded every day. Also track ingredient use per batch, packaging cost per order, and waste as a percent of sales. That shows whether margin is moving because of better pricing and mix, or because the kitchen is simply throwing away less product.

- Log unsold bagels each shift.

- Count spoilage by ingredient.

- Track packaging cost per ticket.

- Review gross margin weekly.

If waste rises on slow days, cut batch size or bake timing before it hits cash. The goal is simple: keep more of each sales dollar after direct costs, because that’s the pool that pays the owner.

3

Labor Model and Owner Role

Labor Mix and Owner Pay

Labor decides whether sales turn into owner income or just payroll. Year 1 payroll is $367k, including a $70k manager, $95k head production role, $60k second production role, plus counter, host, and dish labor. By Year 5, payroll reaches $553k. If the owner covers some manager work, that can lift cash flow, but unpaid owner labor is not true profit.

Estimate labor from covers, open hours, station needs, wage rates, overtime, and owner hours. The risk is simple: if early-morning staffing slips, service quality drops fast, lines slow, and repeat traffic can fall. One bad breakfast rush can erase the savings from a lean schedule.

Protect the Morning Shift

Track labor by shift, not just by month. Compare weekday breakfast covers, Saturday volume, and prep load against staffed roles, then test whether the manager, production, counter, and dish coverage are enough to keep speed steady. If the owner works free shifts, record that time anyway, or the model will overstate take-home income and hide the true cost of running the shop.

Use the schedule to protect service first, then cut waste. If labor is too thin at opening, the shop may save dollars but lose orders, and that hurts owner pay more than a few saved hours help. The goal is enough labor to protect speed without letting payroll swallow the margin.

4

Rent and Location Economics

Rent vs. Traffic

Rent is a fixed bet on traffic. At $12k per month, or $144k per year, the lease has to clear before owner pay. If morning volume, delivery access, seating, or production capacity lag, premium visibility just becomes overhead. The model also lists total fixed operating costs at $1,785k per month, so rent has to fit the full fixed-cost load.

Track Rent-to-Sales Weekly

Measure rent-to-sales before signing or renewing. Track weekday breakfast volume, weekend dozen orders, average ticket, and how many orders the shop can serve without slowing the line. If traffic rises but lease cost rises faster, cash flow tightens and the owner’s draw gets squeezed.

- Stress test slow mornings.

- Check seating and pickup flow.

- Compare rent to monthly sales.

5

Catering, Wholesale, and Capacity Utilization

Catering and Wholesale

Catering and wholesale can raise revenue by filling off-peak oven time with office breakfast trays, dozen-bagel orders, and wholesale accounts. The real question is not sales volume; it is whether each order adds EBITDA after delivery labor, packaging, discounts, and extra prep. If the order uses idle capacity, it can lift owner pay. If it steals from walk-in production, it can crush margin.

Track each channel separately: order count, average ticket, discount rate, packaging cost, delivery labor, prep hours, and waste. The quick math is contribution = sales - direct labor - packaging - delivery costs - discounts. If that number stays weak, the shop is just keeping staff busy, not improving take-home income.

Measure Channel Profit

Price each catering or wholesale order for the extra work it creates, not just for bag count. Office trays, wholesale drops, and dozen-bagel orders should sit on separate revenue lines so you can see which one covers its own cost and which one only fills the schedule. One clean rule: if it needs special packing or timing, it needs its own margin check.

Watch capacity first. Use slow hours, but do not let catering pull ovens or prep labor away from morning walk-ins. Track on-time delivery, spoilage, and overtime every week; if volume rises while gross margin falls, the shop is buying revenue with profit.

6

Compare low, base, and high bagel shop owner income cases

Owner income cases

Owner income moves with daily covers, ticket size, payroll, and rent. The base case uses Year 1 EBITDA and Month 4 breakeven; the high case reflects Year 5 scale.

| Scenario | Low CaseDownside case | Base CasePlan case | High CaseUpside case |

|---|---|---|---|

| Launch model | This is the downside case where traffic stays soft and owner cash stays tight through the launch period. | This is the modeled case where the shop reaches plan and clears breakeven by Month 4. | This is the upside case where traffic, ticket size, and staffing scale into the Year 5 run rate. |

| Typical setup | Weekday covers sit near the low end of the model, tickets stay near $60 midweek and $80 on weekends, and the shop runs on Year 1 margins with $367k payroll and about $214k fixed overhead. | Average covers follow the Year 1 forecast, gross margin stays around 85% before labor, and the business carries $367k payroll, about $214k fixed overhead, and a $592k minimum cash need. | Covers rise to the Year 5 forecast, weekend tickets reach $95, ingredient and packaging ratios trend down, and EBITDA scales to about $1.449M. |

| Cost drivers |

|

|

|

| Owner income rangeBefore owner reserves | $0 - $75kCash-tight range | $150kModeled income | $1.0M - $1.45MScale income |

| Best fit | Use this to stress-test the plan if traffic comes in below the model and reserves matter. | Use this as the most likely owner draw path if the opening plan holds. | Use this to test owner income if the shop reaches full scale and keeps margin. |

Planning note: These scenario ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions.

Related Products

- New York Bagel Shop Porter's Five Forces Analysis

- New York Bagel Shop BCG Matrix

- New York Bagel Shop Business Model Canvas

- 7 Essential KPIs to Track for a New York Bagel Shop

- New York Bagel Shop Business Plan Template in Pre-Written Word

- 7 Strategies to Increase New York Bagel Shop Profitability

- Calculating the Monthly Running Costs for a New York Bagel Shop

- How Much It Costs To Open A Bagel Shop: $592K Cash Plan

- New York Bagel Shop Financial Model Template in Excel

- Launch a New York-Style Bagel Shop in 4 to 9 Months

- How to Write a Business Plan for a New York Bagel Shop

- New York Bagel Shop Marketing Mix

- New York Bagel Shop Marketing Plan

- New York Bagel Shop Business Proposal

- New York Bagel Shop PESTEL Analysis

- New York Bagel Shop Pitch Deck Example Editable PPTX

- New York Bagel Shop Business SWOT Analysis

- New York Bagel Shop Value Proposition Canvas

Frequently Asked Questions

In this model, the owner-income pool starts with $150k Year 1 EBITDA, not guaranteed take-home pay Revenue is about $105M in Year 1, and EBITDA reaches $1449M by Year 5 Owner cash still depends on taxes, reserves, debt service, reinvestment, and whether the owner works in the shop