Owner income$120k

Owner income$120kHow Much Nonprofit Fundraising Consulting Owners Make: $120K+

Fully Editable

Instant Download

Professional Design

Pre-Built

No Expertise Is Needed

Description

Owner income$120k  Net margin-55% to 71%

Net margin-55% to 71% Revenue for target pay$270k

Revenue for target pay$270k Business difficultyHard

Business difficultyHard

You’re planning owner pay before the client base is steady, so revenue and take-home need to be separated This five-year US model uses $120,000 planned lead consultant compensation, EBITDA from -$85,000 in Year 1 to $3213 million in Year 5, and breakeven in Month 17 It excludes employee salary surveys, tax advice, commission guarantees, and promised fundraising results

Owner income$120kNet margin-55% to 71%Revenue for target pay$270kBusiness difficultyHardWant to test your owner pay target?

Owner income calculator

Estimate owner take-home and target-pay gap from revenue, margin, costs, reserves, and target pay.

Planning note: Research-based planning estimate only, not guaranteed salary, tax advice, or owner distribution advice.

Want to see the owner-income forecast?

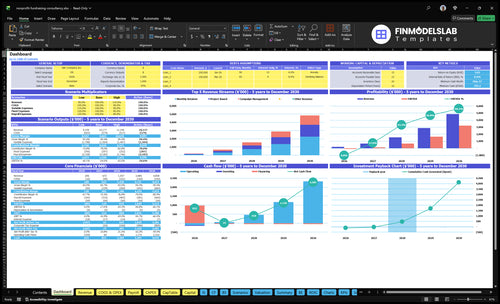

This dashboard in the Nonprofit Fundraising Consulting Financial Model Template shows revenue, EBITDA, cash, Month 17 breakeven, and $795k minimum cash need. Open the model to see pricing, hours, client mix, costs, wages, capex, and owner pay.

Owner-income model highlights

- Owner pay scenarios

- Year 1: -$85k EBITDA

- Year 2: $119k EBITDA

- Year 5: $3.213M EBITDA

- Salary, reserves, hiring

Can a nonprofit fundraising consultant scale?

Nonprofit Fundraising Consulting can scale, but the owner’s job changes fast: solo income is capped by billable hours, sales time, grant calendars, meetings, and campaign deadlines. Once the firm adds admin support, junior consultants, senior consultants, and marketing staff, the owner shifts from doing all the work to pricing, selling, reviewing, and managing delivery. That matters because payroll rises from $1,425k in Year 1 to $5,075k in Year 5, so revenue must grow faster or margin will shrink.

What helps scale

- Admin support frees owner time

- Junior consultants handle routine work

- Senior consultants review client output

- Marketing staff support new sales

What can break margin

- Quality control slips with more clients

- Client retention weakens if service lags

- Delivery management gets harder at scale

- Owner time moves off billable work

What profit margin can a nonprofit fundraising consulting business make?

If you price Nonprofit Fundraising Consulting well, gross margin can run 92% to 95% before payroll, and the startup-cost view is here: How Much Does It Cost To Open And Launch Your Nonprofit Fundraising Consulting Business? Modeled direct COGS is only 5% in Year 1, falling to 3% by Year 5, while software adds 3% to 2% and the bigger squeeze comes from marketing at 12% to 8% plus travel and project materials at 5% to 4%.

Gross margin mix

- 92% to 95% gross margin

- 5% to 3% direct COGS

- 3% to 2% project software

- 12% to 8% marketing

Profit and cash

- $4,950 monthly fixed overhead

- -$85k EBITDA in Year 1

- $119k EBITDA in Year 2

- 3213M Year 5 EBITDA; reserves cut cash

What should a nonprofit fundraising consultant charge?

Charge a nonprofit fundraising consultant by owner budget and delivery time, not by commissions. In Year 1, use $150/hour for retainers, $175/hour for projects, and $200/hour for campaign management; by Year 5, that rises to $180, $200, and $230. That puts a $2,250/month retainer, a $1,750 project, and an $8,000 campaign management fee in line with modeled hours, scope, and meeting load.

Retainer pricing

- $150/hour in Year 1

- $180/hour by Year 5

- $2,250/month example fee

- Price by budget and scope

Projects and campaigns

- $175/hour project rate

- $200/hour campaign rate

- $1,750 project example fee

- $8,000 campaign example fee

What drives nonprofit fundraising consultant income?

1

$150-$230/hrHourly Rate

Rates of $150 to $230 per hour set the ceiling on each billable hour, so even small price gains flow straight to owner take-home.

2

10Client Count

Starting with 10 retainer-equivalent clients builds the recurring base and spreads fixed time across more billable work.

3

70%-80%Service Mix

Moving more revenue into 70% to 80% retainers and up to 45% campaign work changes margin and steadies cash flow.

4

$1.4M-$5.1MLabor Leverage

Payroll rises from about $1.4M to $5.1M as the team scales, so owner income depends on keeping billable output ahead of headcount.

5

$700Retention

CAC improves from $1,500 to $800, saving about $700 per new client and making growth less expensive.

6

$4.95K/$795KCash Buffer

Fixed overhead is about $4.95K a month, and the model needs $795K of minimum cash, so liquidity has to stay ahead of owner pay.

Nonprofit Fundraising Consulting Core Six Income Drivers

Pricing Power

Pricing Power

When a consultant can raise fees without adding more clients, revenue per client goes up and owner pay gets cleaner. Here, modeled rates move from $150 retainer, $175 project, and $200 campaign management in Year 1 to $180, $200, and $230 in Year 5, so the same delivery hours can produce more contribution.

The retainer proxy rises from $2,250/month to $3,240/month, a 44% lift. The catch is scope: if pricing goes up faster than proof, nonprofits push back. Higher fees help only when hours stay controlled and the offer is easy to explain.

Measure Scope Before You Raise Rates

Track three inputs on every client: billable hours, service type, and monthly fee. That shows whether pricing power is lifting contribution or just masking overwork. A simple test is to compare revenue per client against delivery time before and after a price change.

- Quote scope in hours, not vibes

- Track fee per delivery hour

- Document proof before every increase

- Keep campaign work tightly defined

If the firm raises rates but scope stays loose, margin can slip fast. The owner wins when higher fees flow through to profit, not when extra revisions and meetings eat the gain. Price the work, then protect the hours.

1

Client Capacity

Client Capacity

Client count drives revenue, but it also caps the book. In Year 1, about 10 retainer-equivalent clients can support the $120k owner pay plan plus admin and overhead, but that workload also needs about 150 billable hours a month. If each active client adds meetings and edits, income rises only while delivery stays controlled.

Campaign work is heavier. One engagement can take 40 to 50 hours, so a few active campaigns can crowd the calendar fast. Here’s the quick math: more clients can mean more cash, but if hours spill past capacity, margin drops, deadlines slip, and churn risk rises. The cap is not demand; it’s usable time.

Keep the Load Measurable

Track active clients, billable hours, and hours per engagement every week. Separate retainers from campaign projects so you can see when the mix is pushing past the 150-hour monthly ceiling. If one client needs constant meetings, it can cost more than the fee is worth.

Price and scope to protect owner pay. Use a simple rule: if a new client adds 40 to 50 hours of campaign work or stretches response times, either raise the fee, narrow the scope, or pause intake. That keeps utilization sane and helps more revenue reach take-home pay instead of getting lost in rework.

- Watch billable hours weekly.

- Cap campaign-heavy clients.

- Protect meeting time.

- Raise scope when load climbs.

2

Service Mix

Service Mix

For fundraising consulting, the service mix drives both margin and cash flow. Retainers make up 70% to 80% of modeled customer allocation, project work 60% to 50%, and campaign management 10% to 45%. Retainers smooth owner pay, while campaign work can raise fees but also adds more delivery hours, so profit can fall if scope expands faster than pricing.

Grant strategy and advisory work are usually easier to scope than open-ended writing, which helps protect gross margin. The quick math is simple: more recurring retainer work means steadier revenue, but a heavier campaign mix means more labor and deadline risk. Never tie income to grant wins or campaign results; bill for the work, not the outcome.

Shape the Mix Around Hours

Track billable hours by service, not just revenue. If campaign management is priced higher per hour, compare that rate against the extra delivery time it takes to execute, review, and revise. That’s the gap that decides whether the owner can actually keep more cash after payroll and overhead.

Use scope notes for grant strategy, advisory, and campaign work before pricing. Keep the share of open-ended writing in check, and test whether more retainer work improves monthly draw. The goal is a mix that keeps utilization sane and avoids turning high-rate work into low-margin work.

3

Labor Leverage

Labor Leverage

Labor leverage is adding subcontractors and employees to raise delivery capacity beyond the owner’s time. In this model, modeled payroll grows from $1.425M in Year 1 to $5.075M in Year 5, with added admin, junior consultants, marketing support, and senior consultants. That can lift revenue, but only if billable work grows fast enough to cover the payroll step-up.

Here’s the quick math: more headcount can reduce the owner bottleneck, but it also adds review time, training, and rework. If revenue lags payroll, gross margin falls and cash burn rises before the team fully pays for itself. The owner’s take-home income only improves when added labor creates more billable output than it consumes in supervision and corrections.

Price the Team Before You Hire

Track billable hours, utilization, payroll by role, and nonbillable supervision time before adding staff. A simple rule: don’t add a role unless forecasted client work can cover that salary plus the extra review and admin load. If a new consultant needs heavy handholding, the real cost is higher than payroll alone.

- Measure billable hours per role.

- Watch review time and rework.

- Model payroll against booked revenue.

- Hold cash for slower collections.

For this kind of consulting firm, the goal is not just more people. It’s more delivery capacity with enough margin left for owner pay after salaries, training, and delays in client billing.

4

Retention And Referrals

Retention Stabilizes Cash

If retained advisory clients keep renewing, monthly revenue stays steadier and the owner’s pay is easier to plan. One-off projects create gaps; retainers reduce those gaps by keeping billable work active. The key inputs are active clients, renewal rate, monthly retainer value, and the hours needed per account.

Here’s the quick math: CAC improves from $1,500 in Year 1 to $800 in Year 5, while the annual marketing budget rises from $15k to $100k. That shift only helps if referrals and renewals replace cold acquisition. Renewals are not guaranteed, so churn can still create slow months.

Track Renewals and Referrals

Measure renewal rate, referral share, and recurring revenue from retainers. If referrals rise, CAC should move toward $800 over time, which frees cash for owner draw instead of extra s ales spend. Use separate tracking for retainer revenue and project revenue so you can see which one smooths cash.

Ask for renewal decisions 30 to 45 days before a contract ends, and log how many clients shift from one-off work to ongoing advisory. The main risk is counting future renewals too early. A signed project is not stable income until it turns into repeat work.

- Track active retainer clients monthly

- Track renewal rate by cohort

- Track referral-sourced leads and close rate

- Track CAC versus marketing spend

5

Overhead And Cash Discipline

Cash Discipline

If you're running fundraising consulting, overhead hits owner pay fast. Fixed overhead is $4,950/month for rent, utilities, software, insurance, legal, training, and supplies. Add variable costs at 25% of revenue in Year 1 and 17% in Year 5 for COGS, marketing, and travel, and each dollar only becomes draw after those costs are covered.

Here’s the cash trap: the business can look profitable while invoices lag. The model calls for a minimum cash need of $795k in Month 17, so reserves and taxes must stay separate from owner income. The main inputs are billed revenue, collection timing, and travel or marketing spend; if invoices slip, draw drops even when margins look fine.

Tighten Cash Buckets

Track fixed overhead, variable cost %, and cash collected each month. Keep one reserve for taxes and one for operating cash, so owner draw only comes from free cash after bills clear. If revenue rises but payment timing slows, pause draw first; that protects payroll, vendors, and your next month’s spend.

- Billings versus cash collected

- Open invoices by client

- Variable cost rate each month

- Owner draw after reserves

The cleanest control is a 13-week cash forecast. It shows when consulting fees, travel, and software renewals hit before the bank balance does, which is where a profitable-but-cash-tight firm usually gets squeezed.

6

Compare low, base, and high owner-income scenarios

Owner income scenarios

Income shifts with ramp speed, team size, and the mix of retainers, projects, and campaign work. The low case is cash-funded; the high case needs a stronger pipeline.

| Scenario | Low CaseLow Case | Base CaseBase Case | High CaseHigh Case |

|---|---|---|---|

| Launch model | This is the downside path where early ramp keeps the owner in a cash-funded position and EBITDA stays near the Year 1 loss. | This is the controlled ramp where Year 2 turns profitable and EBITDA reaches about $119k. | This is the upside path where the model scales to about $3.213M EBITDA by Year 5. |

| Typical setup | The firm leans on a small retainer and project mix, with 92% gross margin before payroll, 25% combined COGS and variable load, and $4,950 in monthly fixed overhead. | The business has a more balanced service mix, about 93% gross margin before payroll, a 22.1% combined COGS and variable load, and breakeven around Month 17. | Campaign work takes a larger share, gross margin before payroll is about 95%, the combined COGS and variable load is 17%, and the team is bigger to support delivery. |

| Cost drivers |

|

|

|

| Owner income rangeBefore owner reserves | -$85k EBITDALoss case | $119k EBITDABase case | $3.213M EBITDAUpside case |

| Best fit | Use this to test survival if client ramp is slow or hiring slips. | Use this as the main plan for budgeting, hiring, and cash control. | Use this to stress-test what happens if pipeline quality and delivery capacity both hold up. |

Planning note: These scenario ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions.

Related Products

- Nonprofit Fundraising Consulting Porter's Five Forces Analysis

- Nonprofit Fundraising Consulting BCG Matrix

- Nonprofit Fundraising Consulting Business Model Canvas

- 7 Core KPIs to Measure Nonprofit Fundraising Consulting Success

- Nonprofit Fundraising Consulting Business Plan Template in Pre-Written Word

- 7 Proven Strategies to Boost Consulting Profit Margins

- Running Costs for Nonprofit Fundraising Consulting: A 2026 Financial Roadmap

- Nonprofit Fundraising Consulting Startup Costs: $47k CAPEX Plus Runway

- Nonprofit Fundraising Consulting Financial Model Template in Excel

- How To Start A Nonprofit Fundraising Consulting Business In 4–10 Weeks

- How to Write a Nonprofit Fundraising Consulting Business Plan

- Nonprofit Fundraising Consulting Marketing Mix

- Nonprofit Fundraising Consulting Marketing Plan

- Nonprofit Fundraising Consulting Business Proposal

- Nonprofit Fundraising Consulting PESTEL Analysis

- Nonprofit Fundraising Consulting Pitch Deck Example Editable PPTX

- Nonprofit Fundraising Consulting Business SWOT Analysis

- Nonprofit Fundraising Consulting Value Proposition Canvas

Frequently Asked Questions

The model plans $120,000 in annual lead consultant compensation, but extra draws depend on cash EBITDA is -$85,000 in Year 1, then $119,000 in Year 2 and $3213 million in Year 5 Treat owner draw, profit, reserves, and taxes as separate buckets