Owner income-$55k to $3.03M

Owner income-$55k to $3.03MHow Much Can a Nostalgic Candy Store Owner Make? $157K Year 2

Fully Editable

Instant Download

Professional Design

Pre-Built

No Expertise Is Needed

Description

Owner income-$55k to $3.03M  Net margin81%

Net margin81% Revenue for target pay$15.6k

Revenue for target pay$15.6k Business difficultyHard

Business difficultyHard

Under the researched assumptions, a nostalgic candy store owner has no clean draw capacity in the first year because EBITDA is -$55k By Year 2, the model shows $157k EBITDA, which is potential owner take-home before personal taxes, reserves, debt, and reinvestment The model improves to $684k EBITDA in Year 3 if traffic, conversion, repeat purchases, and payroll discipline hold The big swing factors are monthly sales, 840% to 864% gross margin after candy and packaging cost, $3,000 monthly rent, payroll, shrink, and how much cash the owner keeps inside the store

Owner income-$55k to $3.03MNet margin81%Revenue for target pay$15.6kBusiness difficultyHardWant to test your owner draw?

Owner income calculator

Estimate owner take-home and target-pay gap from revenue, margin, costs, reserves, and target pay.

Planning note: Research-based planning estimate only. It is not guaranteed salary, tax advice, or owner distribution advice. Taxes, debt, and one-size-fits-all salary promises are excluded.

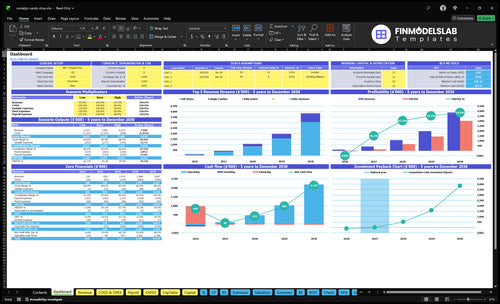

Can you check owner income in the forecast model?

The screenshot shows dashboard outputs, assumptions, revenue, costs, cash flow, and owner take-home; open the Nostalgic Candy Store Financial Model Template.

Owner-income model highlights

- Year 2 EBITDA: $157k

- Breakeven hits month 14

- Payback lands in 26 months

- Startup capex: $66k

- Minimum cash: $838k

- Test sales, margin, staffing

- Check seasonality and reserves

Can a Nostalgic Candy Store Owner Make a Living?

A Nostalgic Candy Store owner likely can’t take a clean full-time draw in Year 1 because EBITDA is -$55k, but Year 2 can support modest owner income if the store reaches $157k EBITDA before reserves, debt, reinvestment, and personal taxes; track this closely with What Is The Most Important Metric To Measure Success For Nostalgic Candy Store?.

Owner Pay Reality

- Year 1 EBITDA: -$55k

- Year 2 EBITDA: $157k

- Pay comes after cash reserves

- Debt lowers owner draw

Ramp Targets

- Weekly visitors: 540 to 790

- Conversion: 250% to 280%

- Repeat customers: 300% to 35%

- Inventory shrink weakens pay

How Do Candy Store Profit Margins Affect Owner Take-Home?

Nostalgic Candy Store owner pay moves almost one-for-one with profit margin, because rent and payroll stay mostly fixed; if you’re sizing startup cash, see How Much Does It Cost To Open, Start, And Launch Your Nostalgic Candy Store?. In Year 1, gross margin after wholesale candy and packaging is 84.0%, and contribution margin after payment fees and sales-promotion marketing is 81.0%; by Year 5, those rise to 86.4% and 84.2%. At about $407k Year 2 revenue, each 1-point margin loss cuts EBITDA and owner draw capacity by about $41k a year.

What helps take-home

- Keep bulk candy mix tight

- Push packaged retro sweets with control

- Use gift boxes for higher basket size

- Watch payment fees and promo spend

What hurts take-home

- Spoilage hits gross margin fast

- Broken packaging adds waste

- Slow-moving items tie up cash

- Over-ordering lowers owner draw

How Much Revenue Does a Candy Store Need to Pay the Owner?

For a Nostalgic Candy Store, you should work backward from the owner draw, not a revenue vanity number. Using the model’s costs, Year 1 break-even is about $156k/month and Year 2 is about $180k/month; the core formula is monthly revenue needed = (fixed costs + payroll + target owner draw + reserves) / contribution margin. If Year 2 revenue reaches about $339k/month, that leaves about $131k/month of EBITDA before reserves. Owner draw is not a guaranteed salary unless it runs through payroll.

Year 1 break-even

- Monthly fixed costs: $126k

- Break-even revenue: $156k/month

- Include payroll in the model

- Owner draw needs a clear structure

Year 2 cash view

- Monthly fixed costs: $147k

- Break-even revenue: $180k/month

- Implied revenue: $339k/month

- EBITDA before reserves: $131k/month

Want the six biggest income drivers?

1

540-1.44K/wkTraffic Conversion

Weekly visitors rise from 540 to 1,440, and conversion moves from 25% to 40%, so more walk-ins turn into paid orders and owner take-home grows fast.

2

5-8u/orderTicket Mix

Orders grow from 5 to 8 units, and gift boxes rise from 20% to 30%, so each basket carries more revenue before costs hit profit.

3

84%-86.4%Margin Shrink

Gross margin stays high because wholesale candy and packaging stay low, so every point gained drops more cash to owner income.

4

$4.68K/moFixed Overhead

The $4,680 monthly base cost, including $3,000 rent, has to be covered first, so lower overhead leaves more room for owner pay.

5

$95K-$130KLabor Model

Annual payroll climbs from about $95K to $130K as staffing fills in, so labor control protects cash after the store gets busy.

6

10%-20%Bulk Mix

Bulk orders grow from 10% to 20%, so more sales come from larger baskets and event buys instead of low-value single items.

Nostalgic Candy Store Core Six Income Drivers

Foot Traffic And Conversion

Foot Traffic And Conversion

540 weekly visitors in Year 1 rising to 1,440 by Year 5 only helps if those visitors buy. For a nostalgic candy store, traffic turns into income through more buyers, more repeat customers, and better absorption of the $4,680/month fixed cost base, including the $3,000 lease. The model also shows conversion moving from 250% to 400% as the store gets better at turning browsers into tickets.

Location matters, but rent has to earn its keep. Downtown, tourist, mall, school-adjacent, and event-heavy sites can lift volume, yet premium rent hurts fast if foot traffic is full of lookers who do not buy. The real test is whether extra visits raise gross profit enough to cover fixed costs and improve owner take-home pay. That is the whole game.

Measure Traffic That Pays

Track weekly visitors, buyer conversion, and ticket count by daypart and location type. Here’s the quick math: more traffic only matters when it lifts paid transactions, not just store visits. If a site brings more browsers but not more buyers, rent and payroll eat the gain. Build the forecast from visitors × conversion × average ticket, then check whether the added gross profit covers fixed overhead.

- Count visitors by hour.

- Separate buyers from browsers.

- Test rent against ticket volume.

- Watch repeat visits by location.

What this estimate hides is poor conversion from novelty traffic. A busy corridor can still miss the mark if the store does not turn nostalgia into a purchase. Use signage, bundle offers, and simple checkout flow to raise buyer rate, and compare that lift against rent. If extra traffic does not improve gross profit per square foot, the location is too expensive.

1

Average Ticket And Product Mix

Average Ticket Mix

Average ticket rises when the store sells more gift boxes, party favors, bulk orders, and premium imports instead of loose singles. In this model, units per order rise from 5 in Year 1 to 8 in Year 5, which lifts revenue per customer and helps spread fixed costs over bigger baskets.

The catch is margin quality. Gift boxes move from 200% to 300% of mix, while single candies fall from 700% to 500%, and gift box prices rise from $2,800 to $3,400. If packaging and fulfillment costs climb too fast, higher AOV can boost sales but not owner take-home.

Track Mix by Basket, Not Shelf

Measure orders, units per order, AOV, and gross margin by product type each week. The quick math is simple: higher AOV helps only if the added packaging, handling, and pick-pack labor stay below the extra gross profit from larger baskets.

Use a clean test plan: push gift boxes for birthdays and tourists, bulk orders for events, and premium imports for add-on sales. Watch whether the mix shift raises cash collected per order faster than it raises fulfillment cost. If it does not, owner pay gets squeezed.

2

Gross Margin And Shrink Control

Gross Margin And Shrink Control

Gross margin is the gap between sales and direct product cost, and it drives how much cash is left for owner pay. Here, wholesale candy purchases fall from 140% of sales in Year 1 to 120% in Year 5, and packaging supplies fall from 20% to 16%. That only helps if pricing and ordering stay tight; otherwise, margin leaks straight out of profit.

Shrink should be tracked as its own line because no shrink rate is given. Spoilage, broken packaging, slow-moving novelty candy, theft, and over-ordering cut gross profit dollar for dollar. Inputs needed are sales, supplier cost, packaging use, inventory counts, and write-offs. One bad ordering cycle can reduce the owner’s draw even when the register looks busy.

Measure It Before It Eats Pay

Track purchase cost as a percent of sales, packaging cost, and shrink by category each month. Split losses into spoilage, damage, theft, and dead stock so the fix is clear. If slow novelty candy sits too long, mark it down fast instead of letting it tie up cash and space. That protects gross profit and keeps more cash available for owner pay.

Use a simple reorder rule: buy to demand, not to display. Review supplier pricing often, count inventory on a set schedule, and compare expected margin to actual margin after each cycle. If the gap widens, the store is either over-ordering or losing product before sale. Here’s the quick math: lower purchase cost and lower shrink both raise take-home income without adding traffic.

- Track shrink by SKU and cause

- Count inventory on a fixed schedule

- Cut dead stock fast

- Reorder to actual sell-through

3

Rent And Fixed Overhead

Rent And Fixed Overhead

Fixed overhead is the monthly bill the store pays before owner pay: $4,680/month total, including $3,000 lease, $400 utilities, $150 insurance, $80 POS, $250 maintenance, $300 accounting, and $500 fixed marketing. That cost has to be covered by gross profit, so weak sales density can wipe out take-home income fast.

Judge rent by location productivity, not cheap rent alone. The key inputs are traffic, conversion, and average ticket; if a higher-rent site brings more buyers and larger baskets, it can still improve profit. If it doesn’t, fixed costs stay the same while owner income shrinks. Under the model assumptions, break-even hits Month 14.

Track Rent Against Sales Density

Measure sales per month against the $4,680 fixed load, then split that by traffic and conversion. One clean test: if the site can’t raise buyer counts and ticket size enough to cover rent plus overhead, it’s too expensive for the sales it generates.

- Track monthly visitors and conversion.

- Watch gross profit after fixed costs.

- Stress test rent at slow months.

- Compare sales per square foot.

4

Labor Model And Owner Workload

Owner-Covered Labor Hours

Labor is the biggest controllable cost after product and rent. Payroll is $95k in Year 1, then $120k in Years 2 and 3, and $130k in Years 4 and 5, which is about $7.9k, $10.0k, and $10.8k per month.

The owner can improve take-home income by covering manager hours, but that only helps cash flow if those hours replace paid staff. The inputs that matter are weekend and holiday traffic peaks, open hours, staffing plan, and owner time. One clean rule: pay for demand, not idle time.

Staff Peaks, Not Empty Shifts

Track labor by daypart so slow weekdays do not carry weekend rates. Measure sales per labor hour, manager coverage hours, and the share of payroll tied to peak periods. If owner hours cover the floor, sales c an hold while payroll falls, but burnout, weak service, and missed upsells can erase the gain.

- Match staff to peak traffic.

- Cut idle weekday coverage.

- Log owner hours separately.

- Watch sales per labor hour.

5

Seasonal And Supplemental Sales

Seasonal and Supplemental Sales

Holiday boxes, birthdays, corporate gifts, local events, school parties, and online retro candy orders can add sales beyond walk-ins. In this model, bulk orders rise from 100% of sales mix in Year 1 to 200% in Year 5, so owner income can improve if those orders carry strong margin. One-liner: more off-peak orders can smooth cash flow and help cover fixed costs.

The catch is extra work. Fulfillment, packaging, marketing, and inventory planning all add cost, and online orders also add shipping and error risk. Here’s the quick math: seasonal volume helps only when the gross profit on gift boxes and bulk orders stays above the added labor and supply cost. If not, revenue grows but owner take-home does not.

Track Margin Per Seasonal Order

Measure each seasonal channel by order count, average order value, packaging cost, labor minutes, and delivery cost. The key test is contribution margin per order, not just sales. If a corporate gift or online box takes extra packing time, it should still beat the store’s normal margin after all variable costs. That is what protects owner pay.

- Track holiday, birthday, and corporate order mix

- Set a minimum order size for bulk sales

- Price gift boxes to cover packing labor

- Forecast inventory before peak weeks

- Prepay large custom orders when possible

6

Owner income scenario table objective

Owner income scenario table

Owner income moves with traffic, conversion, basket size, and the shift toward gift boxes and bulk orders. Early rent and payroll keep the first year tight before volume starts to help.

| Scenario | Low CaseLow Case | Base CaseBase Case | High CaseHigh Case |

|---|---|---|---|

| Launch model | This is the cautious case, with Year 1 still ramping and no safe owner draw after fixed costs. | This is the working case, with Year 2 volume supporting a modest owner draw before reserves. | This is the upside case, with Year 3 volume driving much stronger earnings before reserves. |

| Typical setup | Year 1 is about $119k implied revenue with 81.0% contribution margin, $151k of fixed plus payroll cost, and about -$55k EBITDA. | Year 2 is about $407k implied revenue with 81.8% contribution margin, $176k of fixed plus payroll cost, and about $157k EBITDA. | Year 3 is about $1.041M implied revenue with 82.6% contribution margin, $176k of fixed plus payroll cost, and about $684k EBITDA. |

| Cost drivers |

|

|

|

| Owner income rangeBefore owner reserves | No safe drawNo Safe Draw | $13k/moDraw Capacity | $57k/moUpside Case |

| Best fit | Use this to test downside cash needs if traffic starts slow or staffing runs hot. | Use this as the main planning case if traffic, mix, and repeat buying follow the model. | Use this to test upside if conversion, basket size, and repeat buying all run hot. |

Planning note: These ranges are researched planning assumptions for cash planning, not guaranteed earnings, salary promises, tax advice, or distributions.

Related Products

- Nostalgic Candy Store Porter's Five Forces Analysis

- Nostalgic Candy Store BCG Matrix

- Nostalgic Candy Store Business Model Canvas

- 7 Essential KPIs for Your Nostalgic Candy Store

- Nostalgic Candy Store Business Plan Template in Pre-Written Word

- 7 Strategies to Boost Nostalgic Candy Store Profitability

- Operating Costs: How Much To Run A Nostalgic Candy Store Monthly?

- How Much Does It Cost To Open A Nostalgic Candy Store? $66k Setup Plan

- Nostalgic Candy Store Financial Model Template in Excel

- How to Open a Nostalgic Candy Store in 8-16 Weeks

- How to Write a Nostalgic Candy Store Business Plan

- Nostalgic Candy Store Marketing Mix

- Nostalgic Candy Store Marketing Plan

- Nostalgic Candy Store Business Proposal

- Nostalgic Candy Store PESTEL Analysis

- Nostalgic Candy Store Pitch Deck Example Editable PPTX

- Nostalgic Candy Store Business SWOT Analysis

- Nostalgic Candy Store Value Proposition Canvas

Frequently Asked Questions

The provided model shows no safe draw in the first year because EBITDA is -$55k Year 2 improves to $157k EBITDA, or about $131k/month before reserves, debt, reinvestment, and personal taxes By Year 3, EBITDA reaches $684k if the traffic, conversion, repeat customer, and cost assumptions hold