Owner income$10k

Owner income$10kHow Much Can a One-for-One Retailer Owner Make After Month 17?

Fully Editable

Instant Download

Professional Design

Pre-Built

No Expertise Is Needed

Description

Owner income$10k  Net margin87%–90%

Net margin87%–90% Revenue for target pay$150k

Revenue for target pay$150k Business difficultyHard

Business difficultyHard

You’re trying to pay yourself while funding inventory, marketing, fulfillment, and a donated product for each sale In this model, owner income is planned as a $120,000 annual founder salary before personal taxes, while EBITDA moves from -$233,000 in Year 1 to $160,000 in Year 2 and breakeven arrives in Month 17 These are planning estimates, not guaranteed earnings, salary advice, tax advice, or fixed distributions

Owner income$10kNet margin87%–90%Revenue for target pay$150kBusiness difficultyHardWant to test your owner pay?

Owner income calculator

Estimate owner take-home and the target-pay gap from revenue, margin, costs, reserves, and target pay.

Planning note: Research-based planning estimate only. Actual owner income is not guaranteed salary, tax advice, or owner distribution advice.

Want to check owner income in the One-for-One Retailer model?

Open the One-for-One Retailer Financial Model Template to see revenue, margin, costs, reserves, and owner take-home assumptions. Open the model.

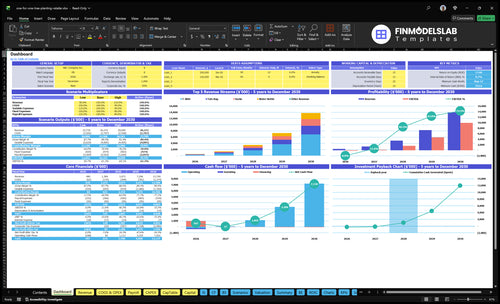

Owner-income model highlights

- Owner take-home is shown clearly

- EBITDA grows from -$233,000

- Month 17 breaks even

- $553,000 minimum cash

- 29-month payback period

When does a one-for-one retailer owner make more money?

The One-for-One Retailer owner makes more money once repeat customers start spreading fixed costs over more orders and lowering blended acquisition cost. In this model, breakeven hits Month 17, payback takes 29 months, and EBITDA turns positive at $160,000 in Year 2 as repeat customers rise from 25% to 55% of new customers, lifetime doubles from 8 to 16 months, and orders per repeat customer move from 0.4 to 0.8 per month.

Money Drivers

- Repeat orders lift gross profit fast

- Fixed costs spread over more sales

- Blended acquisition cost falls

- Year 2 EBITDA can turn positive

Main Risks

- Inventory cash can get tight

- Fulfillment gets more complex

- Marketing spend can stay high

- Donation commitments add pressure

Can a one-for-one retailer make money?

Yes, a One-for-One Retailer can make money, but only if pricing power and repeat orders beat donated item cost and paid customer acquisition; track that link between purpose and retention with What Is The Impact Of Your One-For-One Retailer On Customer Engagement And Loyalty?. The model shows -$233,000 EBITDA in Year 1, then turns positive from Year 2 with founder salary already included.

Profit path

- Year 1 EBITDA: -$233,000

- Year 2 EBITDA: $160,000

- Year 3 EBITDA: $1,615 million

- Year 5 EBITDA: $9,962 million

Watch points

- Founder salary: $120,000 in payroll

- Minimum cash: $553,000

- Control CAC and marketing spend

- Cut donated product cost

How donated product cost affects profit

Donated product cost is a real cost per sale, not a footnote, so the One-for-One Retailer has to price it into margin from day one. Year 1 product manufacturing is 8% of revenue and donated item cost is 5%, so gross margin after both is 87%; if you want the launch math, see How Much Does It Cost To Launch Your One-For-One Retailer Business?. Shipping and fulfillment add 5%, payment fees add 2%, and with $30 CAC, small cost moves hit profit fast.

Year 1 cost stack

- 8% manufacturing cost of revenue

- 5% donated item cost per sale

- 87% gross margin after both

- 2% payment fees

Year 5 cost stack

- 6% manufacturing cost of revenue

- 4% donated item cost per sale

- 90% gross margin after both

- $30 CAC starts to press profit

Want the six biggest income drivers?

1

$31-$40Order Value

Higher average order value lifts revenue on every sale, so the same traffic and repeat buying produce more take-home cash.

2

87%-90%Gross Margin

Product and donated-item costs stay low enough to leave most revenue for overhead and profit, so protecting sourcing price matters a lot.

3

$20-$30Acquisition Cost

Lower customer acquisition cost keeps the marketing budget from getting burned too fast and shortens payback.

4

25%-55%Repeat Rate

More repeat buyers raise lifetime value and cut the need to keep buying the same customer back with ads.

5

5.6%-7%Fulfillment

Shipping, fulfillment, and payment fees take a direct bite out of each order, so small fixes here flow straight to income.

6

$7.9K/moFixed Overhead

Keeping fixed spend near this level helps the model reach Month 17 breakeven instead of needing more cash to cover burn.

One-for-One Retailer Core Six Income Drivers

Average Order Value

Average Order Value

Average order value is the cash you collect per order before costs. In this model, it rises from about $3,064 in Year 1 to $3,985 in Year 5 as sales mix, prices, and units per order move from 110 to 130 bundles. That helps spread donation, fulfillment, payment, and marketing costs over more revenue, but only if discounting does not wipe out margin.

For the owner, AOV matters only when contribution profit rises, not just gross sales. Here’s the quick math: if a higher basket lifts revenue but also increases donated items, shipping, or promos, take-home income can stay flat. The real test is whether each order leaves more cash after variable costs, because that is what funds owner pay and working capital.

Raise AOV Without Cutting Margin

Track AOV by channel, product mix, and bundle type. Tie every discount to a clear margin floor, then compare revenue per order against contribution per order. If a bundle lifts AOV but lowers contribution, it hurts owner income. The goal is simple: more dollars per order, with the same or better cash left after donation and fulfillment.

Watch three inputs closely: units per order, average selling price, and promo rate. If units rise from 110 to 130, ask whether the extra items come at full margin or via heavy markdowns. A clean one-liner: higher AOV only helps when it lifts contribution margin.

- Track AOV by bundle.

- Set a margin floor.

- Test bundles without deep discounts.

- Measure contribution per order.

1

Gross Margin After Donated Product

Gross Margin After Donated Product

True gross margin has to include both the sold item cost and the donated item cost. In Year 1, 8% manufacturing cost plus 5% donated-item cost leaves 87% gross margin before shipping and payment fees. That margin is what funds owner pay after variable overhead, so a small miss on donation cost can shrink take-home fast.

By Year 5, costs improve to 6% and 4%, leaving 90% gross margin. That 3-point lift matters because it gives more room for fulfillment, chargebacks, and marketing. The main risk is underpricing the donation promise: if the donated item cost rises and the retail price does not, owner draw gets squeezed even when sales volume looks strong.

Track Donation Cost Per Order

Measure margin per order as retail revenue minus sold product cost minus donated-item cost, then test it against shipping and payment fees. Track the inputs that move this driver: order count, average order value, sold product COGS, donated item unit cost, and partner logistics costs. If donation cost rises faster than price, gross margin falls and profit turns thin.

Protect owner pay by locking supplier terms and bulk donation pricing early. Here’s the quick math: at 87% to 90% gross margin, every $100 of sales leaves $87 to $90 before shipping, fees, and overhead. Keep a floor price that covers the promise, and review it when mix, product size, or charity sourcing changes.

- Track sold COGS and donation COGS separately

- Reprice when unit costs move

- Test bundles without margin loss

- Watch shipping and payment fees monthly

2

Customer Acquisition Cost

Customer Acquisition Cost

CAC is the marketing spend needed to win one new customer. In this model, it falls from $30 in Year 1 to $20 in Year 5, even as the annual marketing budget rises from $300,000 to $1,000,000. That matters because first-order economics are tight: $3,064 AOV and about $2,450 contribution before CAC leave room, but not much if conversion is weak.

For the owner, CAC hits take-home income by changing how much cash is left after each first sale. Lower CAC lifts profit and helps fund fixed overhead, payroll, and inventory. Higher CAC can turn growth into a cash drain. The key inputs are marketing spend, new customers, AOV, and repeat orders, since repeat buying is what makes paid acquisition pay back.

Track CAC by channel

Measure CAC as marketing spend ÷ new customers, then split it by channel so you can see where the cost is coming from. A simple test is whether first-order contribution of about $2,450 stays above CAC by a wide margin. One clean rule: don’t scale spend unless the math works on the first order and the repeat order.

- Marketing spend by channel

- New customers gained

- Repeat purchase rate

- AOV and order mix

- Contribution after CAC

Repeat buyers matter because they spread acquisition cost over more revenue. In this model, repeat customers rise from 25% to 55% of new customers, and repeat lifetime grows from 8 to 16 months. If CAC creeps up, tighten targeting, raise AOV only when margin holds, and cut channels that bring one-time buyers.

3

Repeat Purchase Rate

Repeat Purchase Rate

Repeat purchase rate is the share of buyers who come back and buy again. For a one-for-one retailer, this matters because every repeat order lowers the blended acquisition cost—the original marketing spend is spread across more sales. In this model, repeat customers rise from 25% to 55% of new customers, which is a big swing for owner pay if the second order keeps the same margin.

Here’s the quick math: repeat customer lifetime grows from 8 to 16 months, and average repeat orders per month rise from 0.4 to 0.8. That can lift profit fast, but only if repeat buys do not need heavy discounts. If discounts are too deep, the revenue looks better while take-home income stays thin.

Track Repeat Orders by Cohort

Measure repeat rate by customer cohort, not just monthly sales. Track new customers, repeat customers, orders per customer, discount depth, and margin on repeat orders. If repeat orders hold the same gross margin, each extra order improves CAC payback and cash flow. If repeat buyers need constant promos, the gain to owner income drops fast.

Use one simple test: compare contribution margin on first orders vs repeat orders. If lifetime rises from 8 to 16 months and repeat orders move from 0.4 to 0.8 per month, keep stock, email, and loyalty offers focused on margin, not just volume. That’s what turns loyalty into real draw for the owner.

4

Fulfillment And Donation Logistics

Related Products

- One-for-One Retailer Porter's Five Forces Analysis

- One-for-One Retailer BCG Matrix

- One-for-One Retailer Business Model Canvas

- Tracking 7 Core KPIs for One-for-One Retailer Success

- One-for-One Retailer Business Plan Template in Pre-Written Word

- How to Boost One-for-One Retailer Profit Margins

- How to Calculate Monthly Running Costs for a One-for-One Retailer

- One-for-One Retailer Startup Costs: $138K CAPEX And $553K Runway

- One-for-One Retailer Financial Model Template in Excel

- How To Open A One-For-One Retailer In 8-16 Weeks With Verified Giving

- How to Write a One-for-One Retailer Business Plan in 7 Steps

- One-for-One Retailer Marketing Mix

- One-for-One Retailer Marketing Plan

- One-for-One Retailer Business Proposal

- One-for-One Retailer PESTEL Analysis

- Retail Pitch Deck Example Editable PPTX

- One-for-One Retailer Business SWOT Analysis

- One-for-One Retailer Value Proposition Canvas

Frequently Asked Questions

The modeled owner pay is $120,000 per year, or $10,000 per month, before personal taxes That salary sits inside payroll, not after-profit distributions The business still shows EBITDA of -$233,000 in Year 1, reaches breakeven in Month 17, and needs $553,000 of minimum cash, so early pay depends on funding