Online Mortgage Lending Startup Costs for a $75M Year 1 Launch

You’re planning a regulated lending launch, so separate capital expenditures (CAPEX), setup expenses, payroll runway, and balance-sheet funding from day one In this researched first operating year case, fixed overhead starts at $34,500/month, visible Month 1 leadership payroll is $660,000/year, and warehouse lines of $60,000,000 sit outside basic startup costs These ranges are planning assumptions, not vendor quotes, legal advice, or guaranteed licensing costs

Estimate Startup Costs with Calculator

Startup CAPEX Calculator

Estimates capitalized startup assets only for the website, app, secure borrower portal, hardware, and setup work.

Excluded from CAPEX Excludes payroll runway, working capital, inventory, deposits, debt service, warehouse lines, loan funding liquidity, legal fees, and marketing. Monthly cloud hosting ($10,000), core software ($5,000), and data security ($3,000) are operating costs, not CAPEX.

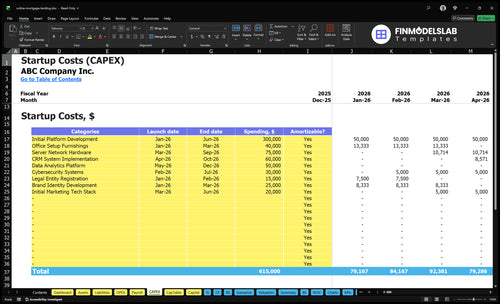

What does the CAPEX screenshot show?

CAPEX tab in Online Mortgage Lending Financial Model Template shows startup costs, timing, depreciation. Review assumptions before raising capital.

Key screenshot highlights

- Month 1 to 60

- $34.5k fixed overhead monthly

- $660k Month 1 payroll

- $75M year 1 originations

- $60M lines, $3M deposits

- Depreciation and amortization split

- Variable expense percentages shown

- Launch timing and staffing ramp

- Total funding need shown

What hidden costs come with starting an online mortgage lending business?

Online Mortgage Lending looks cheap on a startup sheet, but the hidden cost is cash tied up in working capital, regulatory net worth, surety bonds, audits, lead testing, and loan-funding liquidity. If you're sizing the model, see How Much Does The Owner Of Online Mortgage Lending Business Typically Make? for the income side; the real burn shows up in interest carry and timing gaps. Here’s the quick math: a fully drawn $60,000,000 Year 1 warehouse line at 5.75% implies $3,450,000 in annual interest, and $5,000,000 of other borrowed funds at 6.20% adds $310,000 more.

Also, $3,000,000 of warehouse line deposits, $5,000,000 of cash equivalents, $2,000,000 of short-term investments, and $1,000,000 of escrow accounts are funding items, not operating expense, so the financing plan can look much larger than the startup-cost table.

Cash costs

- Working capital bridges loan timing gaps.

- Regulatory net worth sits idle.

- Surety bonds and audits hit cash early.

- Unused implementation time and lead testing still burn money.

Funding items

- $60,000,000 warehouse lines are credit facilities.

- $5,000,000 borrowed funds can add $310,000 interest.

- $3,000,000 deposits and $1,000,000 escrow are not expense.

- $5,000,000 cash equivalents plus $2,000,000 investments sit on the balance sheet.

How much does it cost to start an online mortgage lending company?

For Online Mortgage Lending, plan startup costs by category, not one universal number: visible fixed overhead starts at $34,500/month, or $414,000/year, before funding facilities. Use What Is The Most Critical Measure Of Success For Your Online Mortgage Lending Business? to tie that spend back to loan volume, conversion, and margin.

Core budget drivers

- $660,000/year leadership payroll

- State count drives license cost

- Software choice changes setup spend

- Staff count and marketing intensity matter

Year-one scale

- $75,000,000 total originations

- $50,000,000 primary mortgages

- $10,000,000 refinance loans

- Exclude $60,000,000 warehouse lines

How much funding do I need to start an online mortgage lender?

For Online Mortgage Lending, plan on at least $89,500/month before variable costs, because $34,500 in fixed overhead plus $55,000 in Month 1 leadership payroll is the floor. If you’re targeting $75,000,000 in first-year originations, you also need separate capacity for $60,000,000 in warehouse lines and $3,000,000 in warehouse deposits, plus runway for compliance setup, tech build, lead generation, and closing delays.

Monthly burn floor

- $34,500 fixed overhead

- $55,000 Month 1 payroll

- $89,500 before variable costs

- Runway must cover delays

Capital stack needs

- $75,000,000 first-year originations

- $60,000,000 warehouse lines

- $3,000,000 warehouse deposits

- Model 100% CAC and 30% processing

Calculate Fuding Needs

Startup Cost Summary

This table compares key startup CAPEX and excluded cash needs for an online mortgage lender across low, base, and high cases.

| Cost Category | Base Estimate | Main Cost Driver | CAPEX Calculator |

|---|---|---|---|

| Initial Platform Development | $300,000 | Website and loan origination build | Yes |

| Server Network Hardware | $75,000 | Loan origination system infrastructure | Yes |

| CRM System Implementation | $60,000 | Point-of-sale workflow setup | Yes |

| Data Analytics Platform | $50,000 | Decisioning and reporting setup | Yes |

| Cybersecurity Systems | $30,000 | Security and compliance hardening | Yes |

| Operating Reserve | $113,469,000 | Negative minimum cash and balance-sheet funding needs | No |

Online Mortgage Lending Core Five Startup Costs

Licensing, Regulatory, and Compliance Setup Startup Expense

Licensing setup

You need Nationwide Multistate Licensing System and Registry filings, state mortgage lender licenses, state-specific license types, compliance policies, legal counsel, audits, surety bonds, and regulator readiness. Requirements change by state and license type, so this is not legal advice. The first questions are simple: how many states launch first, and are Federal Housing Administration (FHA) and U.S. Department of Veterans Affairs (VA) loans included?

Core cost drivers

Plan source costs at $8,000/month for compliance legal fees plus $4,000/month for professional services, or $12,000/month from Month 1 through Month 60. That is $720,000 before filing fees, bonds, and audits. Add the $190,000/year Chief Compliance Officer role if you need in-house oversight.

- Count licenses by launch state.

- Price bonds and audit work.

- Map brokered, funded, serviced.

How to size it

Use three inputs: number of states, license type per state, and product scope. Brokered lending, funded lending, and servicing can trigger different rules, forms, and exams. Here’s the quick math: more states means more filings, more policies, and more regulator touchpoints. If you start with one state, your setup load is far lighter than a multi-state launch.

- Start with the first-state license.

- Confirm examiner expectations early.

- Document every control owner.

Regulator readiness

Keep policies, training logs, complaint handling, audit trails, and bond renewals ready before launch. What this estimate hides is exam prep time: if state reviews drag, outside counsel and compliance services stay on the clock. The first hire to watch is a $190,000/year Chief Compliance Officer, because regulator readiness lives or dies on ownership.

Mortgage Loan Origination Software and Workflow Startup Expense

Core stack

A mortgage loan origination stack usually needs a loan origination system, borrower portal, CRM, pricing engine links, e-signature, document management, income and asset verification, and closing workflow. At the source assumptions, recurring software starts at $5,000/month plus $10,000/month cloud hosting, or $180,000/year before implementation work.

Build cost

Treat implementation as a separate build line, not subscription. It covers labor, data setup, user permissions, workflow testing, and reporting, and it should be sized from vendor quotes, the number of integrations, and the months of setup. Check whether the platform can support $75,000,000 in Year 1 originations across primary, refinance, jumbo, FHA/VA, and HELOC loans.

- Separate license and build costs.

- Map each workflow step first.

- Confirm every product type.

Keep it lean

Keep the first release tight: standardize workflows, limit custom code, and only pay for modules the team will use in the first 12 months. Common mistakes are mixing capex with monthly fees and overbuilding for edge cases. One clean rule: if a feature does not help fund and close loans in year one, defer it.

- Phase integrations by priority.

- Test permissions before launch.

- Save custom reports for later.

Volume check

The quick budget check is $15,000/month in recurring software and hosting, or $180,000 a year, before staff and launch work. That spend only makes sense if the workflow can handle the expected loan mix and volume without slowing approvals. If closing, pricing, or verification breaks under load, fix that first.

Website, App, Cybersecurity, and Data Protection Startup Expense

Secure intake

Borrowers will send Social Security numbers, income records, bank data, tax documents, and identity files, so the website, app, or secure portal needs encryption, identity controls, access logs, backup, incident response, and privacy-ready flows. Size the build to the application volume implied by $75,000,000 in Year 1 originations, not just a marketing site.

Monthly stack

The starting run rate is $10,000/month for cloud hosting and $3,000/month for data security infrastructure. Add implementation labor, data setup, user permissions, workflow testing, and penetration testing. Treat custom build as CAPEX only if the software is owned or capitalized; otherwise keep security subscriptions in operating expense.

- Months of hosting coverage

- Quotes for pen testing

- Users and application volume

Keep it lean

Buy only the controls tied to launch products, then add monitoring and security subscriptions as traffic grows. The common mistake is underfunding controls and paying later for rework after a review or incident. If borrower volume climbs faster than planned, the first pressure point is hosting, then monitoring, then support capacity.

Scope check

Match spend to the live borrower flow, not the demo flow. If the portal handles document upload, status tracking, and identity checks in one place, the budget needs enough room for secure storage, review tools, and audit trails from day one.

Staffing Readiness and Pre-Launch Payroll Startup Expense

Payroll First

Staffing is a pre-opening cash need, not CAPEX. For launch, the visible Month 1 salaries are $250,000 for the Chief Executive Officer, $220,000 for the Chief Technology Officer, and $190,000 for the Chief Compliance Officer, or $660,000/year and $55,000/month. Here’s the quick math: that is working capital you need before the first loan funds.

What It Covers

This payroll bucket should cover loan officers, processors, underwriters, compliance staff, operations leadership, technology leadership, recruiting, training, licensing, and system onboarding. To estimate it, use headcount × salary, plus the number of launch months covered. The Head of Data Science starts in Month 13 at $180,000/year, so it is not a launch-month cost.

- Count launch-month headcount only

- Use salary, not wishful budgets

- Separate Month 13 hires

Keep It Lean

Keep staffing lean by staging hires to volume and licensure needs. Ask whether loan officers are salaried, commissioned, contractor-based, or referral-partner driven, because that changes cash burn fast. What this estimate hides: onboarding time, training lag, and idle months before production. Hiring too early turns payroll into dead weight.

- Delay noncritical hires

- Match staff to launch states

- Use variable pay where allowed

Funding Question

Before funding, pin down launch scope: how many states go live first, how many staff need licenses, and how many months of payroll must sit on the balance sheet. Loan officers are the swing item, so their pay model drives the cash plan far more than the title list does. No model is solid until that is fixed.

Launch Marketing and Borrower Acquisition Startup Expense

Acquisition Base

Start with a defined spending base: paid search, SEO setup, referral partnerships, rate comparison channels, brand launch, landing pages, analytics, call tracking, conversion tracking, and ad-claim review. For Year 1, plan marketing against $75,000,000 originations and the product mix across purchase, refinance, jumbo, FHA VA, and HELOC. Do not budget to promised leads; use a base-first model and separate media, tools, and legal fees.

Channel Test

Control spend by splitting each channel into a test budget, then scale only what passes call and application tracking. Keep compliance review on every claim, and never imply guaranteed lead volume or funded-loan conversion rates. One message per product, one landing page per offer, one dashboard for source quality.

- Track calls and forms separately.

- Cut weak sources fast.

- Review claims before launch.

Claim Control

Keep every ad, rate page, and form in sync with compliance rules. If a claim cannot be supported, drop it. That matters most on rate comparison channels, where small wording changes can create legal risk and waste spend on low-trust clicks.

Ramp Plan

Model marketing customer acquisition at 100% in Year 1, then 80%, 60%, 50%, and 40% in later years. The math only works after you define the spending base, because dollars depend on what is included. For a $75,000,000 launch, channel intensity should match product mix and the speed needed to fill the pipeline.

Compare 3 Startup Cost Scenarios

Scenario Table

Licensing scope, team size, build depth, and funding capacity push online mortgage lending costs up fast. Lean, Base, and Full show how much the launch can change before volume starts to matter.

| Scenario | Lean LaunchProof of concept | Base LaunchRegulated growth | Full LaunchScale build |

|---|---|---|---|

| Launch model | Run a narrow footprint with a small team, broker-style flow, and a lighter website build. | Run the model plan with multi-state lending, a full core team, and standard warehouse funding. | Build a broader online lender with more automation, stronger security, and a bigger credit and ops stack. |

| Typical setup | Use limited licensing, lean paid media tests, and fewer custom systems. | Use the source plan with $34,500 monthly fixed overhead and the Year 1 leadership payroll already in place. | Add heavier cybersecurity, deeper underwriting automation, and more staff for processing and funding. |

| Cost drivers |

|

|

|

| Planning rangeCAPEX only | $500,000 - $1,500,000Lowest burn | $1,500,000 - $3,000,000Model baseline | $3,000,000 - $7,000,000Highest build |

| Best fit | Best for founders testing demand before a wider state rollout. | Best for teams ready to build a compliant operating platform and scale originations. | Best for teams planning fast scale and a wider product and state footprint. |

Planning note: These ranges are researched planning assumptions, not exact quotes.

Related Products

- Online Mortgage Lending Porter's Five Forces Analysis

- Online Mortgage Lending BCG Matrix

- Online Mortgage Lending Business Model Canvas

- 7 Essential KPIs for Tracking Online Mortgage Lending Performance

- Online Mortgage Lending Business Plan Template in Pre-Written Word

- 7 Strategies to Increase Profitability in Online Mortgage Lending

- How to Run an Online Mortgage Lending Business: Monthly Costs

- Online Mortgage Lending Financial Model Template in Excel

- How Much Online Mortgage Lending Owners Can Make At $75M Volume

- How To Start An Online Mortgage Company In 6–12 Months

- How to Write an Online Mortgage Lending Business Plan (7 Steps)

- Online Mortgage Lending Marketing Mix

- Online Mortgage Lending Marketing Plan

- Online Mortgage Lending Business Proposal

- Online Mortgage Lending PESTEL Analysis

- Online Mortgage Lending Pitch Deck Example Editable PPTX

- Online Mortgage Lending Business SWOT Analysis

- Online Mortgage Lending Value Proposition Canvas

Frequently Asked Questions

It needs launch expenses plus operating runway and separate funding capacity In this planning case, fixed overhead starts at $34,500/month, visible Month 1 leadership payroll is $660,000/year, and Year 1 originations are $75,000,000 Warehouse lines of $60,000,000 and deposits of $3,000,000 are not basic startup expenses