Owner income$1.58M

Owner income$1.58MHow Much Does an Organic Restaurant Owner Make? $0 to $226k+

Fully Editable

Instant Download

Professional Design

Pre-Built

No Expertise Is Needed

Description

Owner income$1.58M  Net margin-17% to 55%

Net margin-17% to 55% Revenue for target pay$968k

Revenue for target pay$968k Business difficultyHard

Business difficultyHard

Key Takeaways

- Raise average check faster than traffic, but keep value.

- More seat turns absorb fixed costs and lift revenue.

- Tighten food waste to protect gross profit per cover.

- Labor and rent can cap take-home during ramp-up.

Owner income$1.58MNet margin-17% to 55%Revenue for target pay$968kBusiness difficultyHardWant to test your owner pay?

Owner income calculator

Estimate owner take-home and target-pay gap from revenue, margin, costs, reserves, and target pay.

Planning note: This is a researched planning estimate, not guaranteed salary, tax advice, or owner distribution advice.

Can you check owner income in the model?

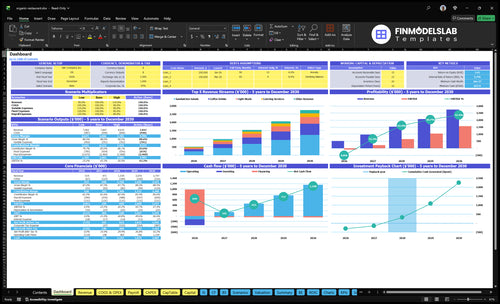

This dashboard shows revenue, margin, costs, reserves, cash flow, and owner take-home in the Organic Restaurant Financial Model Template. It also charts covers, average order value, and payback; open it to pressure-test the numbers.

Owner income model highlights

- Sandwiches and salads 450%-400%

- Coffee drinks 250%-280%

- Catering 80%-150%

- EBITDA -$101k to 1577M

- Breakeven Month 14

Does an organic restaurant owner make more by working in the business?

Yes—an Organic Restaurant owner can usually take home more by working in the business, because replacing a $65k cafe manager or $60k head chef can lift cash flow. Here’s the catch: that only works if service quality, kitchen output, and controls stay tight. Payroll starts at $338k in Year 1 and rises to $4.615M by Year 5, so labor is a major swing factor, not guaranteed owner pay.

Cash-flow gain

- Owner can replace paid labor.

- $65k manager role can disappear.

- $60k chef role can disappear.

- Take-home can rise fast.

What can break it

- Payroll starts at $338k Year 1.

- Payroll reaches $4.615M by Year 5.

- Burnout can cap growth.

- Weak delegation limits scale.

How much can an organic restaurant owner make?

An Organic Restaurant owner may safely take $0 in Year 1 if EBITDA is -$101k; the first real pre-tax profit pool appears in Year 2 at $226k EBITDA. For operating quality context, track What Is The Current Customer Satisfaction Level For Organic Restaurant? because repeat visits matter before owner distributions.

Small ramp-up case

- Year 1 EBITDA: -$101k

- Safe distributions: $0

- Year 2 EBITDA: $226k

- Pay reserves, debt, taxes first

Owner-operated upside

- Replace cafe manager: $65k

- Replace head chef: $60k

- Year 3 EBITDA: $650k

- Year 5 EBITDA: $1.577M

Do organic ingredients reduce restaurant profit margins?

Yes—Organic Restaurant margins can tighten when organic sourcing, freshness, and spoilage hit the cost base; if you’re sizing the build, see How Much Does It Cost To Open And Launch An Organic Restaurant?. In this model, Food Ingredients run at 100% of sales in Year 1 and improve to 90% by Year 5, while Beverage & Paper Goods move from 30% to 25%. That means profit gets better as purchasing, menu mix, and volume mature, but only if prices match the ingredient story.

Margin pressure

- Fresh organic inputs cost more.

- Spoilage cuts gross margin fast.

- Year 1 cost load is highest.

- Bad pricing hurts profit fast.

Margin controls

- Use premium pricing by dish.

- Control portions on high-cost items.

- Build seasonal menus around supply.

- Track waste and vendor performance.

Want the six drivers that move owner income?

1

$16-$28Menu Pricing

Midweek AOV starts at $16 and weekend AOV at $20, then reaches $22 and $28 in Year 5, so price lift flows straight to take-home profit.

2

60-400/daySeat Turns

Daily covers rise from 60-130 in Year 1 to 250-400 in Year 5, and each extra seat turn spreads the same rent and payroll over more checks.

3

$338K-$462KLabor Model

Payroll climbs from about $338K to about $461.5K, so staffing mix and schedule control have a direct effect on owner income.

4

13%-11.5%Food Cost

Food ingredients plus beverage and paper goods run from 13.0% in Year 1 to 11.5% in Year 5, so waste control protects margin on every order.

5

$10.9K/moRent Load

Rent and other fixed costs total about $10.9K a month, so occupancy pressure stays high until volume gets close to breakeven.

6

8%-15%Sales Mix

Catering grows from 8% to 15% and coffee drinks rise from 25% to 28%, which lifts revenue without needing a lot more seats.

Organic Restaurant Core Six Income Drivers

Average Check And Menu Pricing

Average Check Pricing

Average check is the spend per guest, so it drives revenue before traffic even moves. In this model, midweek AOV goes from $16 in Year 1 to $22 in Year 5, and weekend AOV from $20 to $28. If covers stay flat, higher check lifts revenue and can improve owner pay as long as portion cost and labor do not rise with it.

What this estimate hides is guest tolerance. Organic pricing must match ingredient quality, local sourcing, and service level. Push price faster than perceived value, and repeat visits can slip even if the first check is higher.

Price to Value, Not Just Cost

Track covers × average check = revenue by midweek and weekend. Split menu items by margin, then test small price moves on the highest-demand dishes first. If a dish sells well at a higher price and portion cost stays controlled, the owner keeps more gross profit without needing more traffic.

- Measure midweek and weekend checks separately.

- Watch item mix and portion sizes.

- Test price after value signals improve.

- Hold repeat demand before raising again.

1

Table Turns And Seat Utilization

Table Turns And Seat Use

Table turns mean how many times each seat sells during service. Seat utilization is how full the room stays while open. If weekly covers rise from 640 in Year 1 to 3,250 by Year 5, revenue can grow faster than rent and insurance, so more of each dollar sold can reach profit and owner pay.

Here’s the quick math: Friday grows from 130 covers to 400, and Sunday from 60 to 250. That only works if hours open, staffing, kitchen speed, and service quality all rise with demand. Overfill the room, and waits, errors, and repeat visits can fall fast.

Track Covers, Turns, And Waits

Measure covers per day, turns per seat, ticket time, and peak wait time by daypart. Use those inputs to size labor and set realistic sales plans. The goal is simple: add covers without adding rent or insurance at the same pace, so each extra guest improves fixed-cost absorption and cash for owner pay.

- Track covers by day and hour.

- Watch ticket times and table turns.

- Match staff to Friday and Sunday peaks.

- Cap waits before service quality slips.

If the room cannot serve 3,250 weekly covers cleanly, the model is too aggressive. The best gain comes from steady fill rates and fast resets, not from packing every seat and risking weaker repeat demand.

2

Organic Ingredient Cost And Waste

Organic Ingredient Cost and Waste

Organic ingredient cost hits owner pay fast because every wasted prep item lowers gross profit per cover. In the model, Food Ingredients start at 100% and Beverage & Paper Goods at 30%, then improve to 90% and 25% by Year 5. The key inputs are covers, menu mix, portion size, spoilage, and supplier pricing.

Slow turns raise waste and cash tied up in inventory. If high-cost proteins are overportioned or produce sits too long, margin falls even when sales look fine. A seasonal menu helps, but only if prep levels match daily demand.

Track Waste and Tighten Portions

Measure waste by item each day, not just total food cost. Rotate fresh produce into specials, set prep pars, and portion high-cost proteins with a scale or scoop. Ask suppliers for better pricing on the top items. One clean number matters most: food cost per cover.

Use weekly checks on spoilage, trim, and comped plates. If waste rises on slow days, cut prep before service starts. That protects margin and leaves more cash for the owner draw.

3

Labor Model And Owner Role

Owner-Led Labor Model

This driver is the split between paid leadership and owner labor. Payroll here includes a $65k cafe manager, a $60k head chef, 2 Year 1 baristas at $38k each, 25 counter staff at $35k, and 15 kitchen assistants at $33k. That is about $1.57M a year before taxes and benefits, so the owner’s income depends on how much of that leadership they personally replace.

If the owner covers the manager or chef role, the business can keep up to $125k of annual leadership pay inside the company. That can raise short-term take-home, but it is real work, not free margin. The tradeoff is simple: more owner pay now, less room to scale later, and a higher burnout risk if the owner becomes the daily fix for everything.

Track Role Swap Before You Cut Pay

Measure labor as a share of sales, owner hours, and overtime by role. Compare the saved manager and chef salary to the extra time the owner must work. If the owner is doing leadership plus service, cash flow may improve, but the real test is whether the team can still run cleanly without the owner in every shift.

- Track manager and chef coverage

- Watch owner hours weekly

- Limit overtime spikes

- Protect time for hiring

4

Rent, Location, And Occupancy Cost

Rent, Location, And Occupancy Cost

This driver is the monthly lease plus the fixed load around it. With $8,000/month rent and $10,900/month total fixed expenses, rent is about 73% of that fixed-cost block, so the site has to generate enough covers per square foot to pay the lease before owner pay. A strong organic location can lift price and traffic, but weak sales density turns a good room into a cash drag.

The risk is signing for Year 3 volume during a Year 1 ramp-up. If sales grow slower than the lease, profit and cash flow shrink fast. Rent alone is not the test; judge it against sales productivity, cover count, and how quickly the dining room fills at peak times.

Measure Sales Density Before You Sign

Track monthly sales per square foot, covers per day, and seat use during peak hours. Compare those numbers to the lease before signing, then check them every month after opening. Here’s the quick math: if sales growth does not outrun fixed costs, the owner’s draw gets squeezed even when the room looks busy.

- Rent + overhead must fit ramp sales.

- Covers per square foot drive lease safety.

- Slow months should still cover fixed costs.

- Lease terms should match Year 1 traffic.

A better lease is one you can pay in a slow month. Keep occupancy low enough that the business can clear gross profit during the ramp, or owner pay waits until traffic matures and repeat vis its build.

5

Revenue Mix And Add-On Channels

Add-On Revenue Mix

For an organic restaurant, add-on channels matter when they raise sales per labor hour without stressing the kitchen. The model mix starts with sandwiches and salads at 450%, coffee drinks at 250%, light meals at 150%, catering at 80%, and artisanal beverages at 70%. If catering reaches 150% by Year 5 and coffee drinks reach 280%, owner income improves through denser revenue, not just more covers.

Here’s the quick math: revenue grows faster than fixed costs only if channel mix stays aligned with prep time, delivery fees, and staff load. Direct takeout, private events, and beverages can add margin, but delivery charges and kitchen strain can cut the gain fast. One clean rule: if an add-on needs more labor than it pays for, it hurts take-home pay.

Track Channel Profit, Not Just Sales

Measure each add-on by order count, average check, prep minutes, labor cost, and delivery fees. That tells you whether sandwiches, salads, coffee drinks, catering, or beverages lift gross profit or just create busier shifts. If a channel adds revenue but pushes overtime or spoilage up, it is not helping owner pay.

Test small moves first: price coffee drinks to protect margin, set minimums on catering, and cap private events by kitchen capacity. Use the best-selling items as anchors, then document what each channel does to cash flow and weekly profit. If the mix starts crowding the line, cut the lowest-margin orders before they drag down the whole day.

- Track profit by channel weekly.

- Set catering minimums before booking.

- Limit low-margin delivery volume.

6

Compare lean, base, and high-performing owner income scenarios

Owner income scenarios

Owner income shifts fast here because Year 1 runs negative, Year 2 turns profitable, and later years depend on covers, average check, labor, and reserve discipline.

| Scenario | Low CaseDownside case | Base CaseModeled case | High CaseUpside case |

|---|---|---|---|

| Launch model | This is the lower-earnings path, with no safe owner draw in the ramp year. | This is the modeled path, where the restaurant turns profitable but still needs reserve control. | This is the stronger-earnings path, where scale starts to support meaningful owner distributions. |

| Typical setup | Year 1 revenue is about $5.595M, EBITDA is -$101k, and minimum cash need reaches $638k while the business is still absorbing start-up pressure. | Year 2 revenue is about $9.677M, EBITDA is $226k, and breakeven lands in Month 14, so owner pay only works after cash reserves. | Year 3 to Year 5 EBITDA rises from $650k to $1.577M as average check moves from $19 and $24 to $22 and $28, COGS eases from 13.0% to 11.5%, and payroll rises from $398k to $461.5k. |

| Cost drivers |

|

|

|

| Owner income rangeBefore owner reserves | No safe distributionNo draw | Small reserve-backed drawCareful draw | $650k - $1.577MStrong draw |

| Best fit | Use this to stress-test a slow launch and thin cash. | Use this for a cautious operating plan with a possible owner draw after reserves. | Use this to test upside with tighter reserve discipline and stronger owner pay. |

Planning note: These scenario ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions.

Related Products

- Organic Restaurant Porter's Five Forces Analysis

- Organic Restaurant BCG Matrix

- Organic Restaurant Business Model Canvas

- 7 Critical KPIs to Scale Your Organic Restaurant

- Organic Restaurant Business Plan Template in Pre-Written Word

- 7 Strategies to Increase Organic Restaurant Profitability

- How Much Does It Cost To Run An Organic Restaurant Monthly?

- Organic Restaurant Startup Costs: $220k Setup and $638k Cash Need

- Organic Restaurant Financial Model Template in Excel

- How to Open an Organic Restaurant: 6 Launch Drivers Before Service

- How to Write an Organic Restaurant Business Plan in 7 Steps

- Organic Restaurant Marketing Mix

- Organic Restaurant Marketing Plan

- Organic Restaurant Business Proposal

- Organic Restaurant PESTEL Analysis

- Organic Restaurant Pitch Deck Example Editable PPTX

- Organic Restaurant Business SWOT Analysis

- Organic Restaurant Value Proposition Canvas

Frequently Asked Questions

It may pay little or nothing in Year 1 if EBITDA is negative The researched model shows -$101k EBITDA in Year 1, then $226k in Year 2 and $650k in Year 3 Owner pay comes after debt service, taxes, reserves, and reinvestment, so EBITDA is the profit pool, not automatic take-home