Owner income$3.0M

Owner income$3.0MHow Much Outrigger System Owners Make on $55M Year 1 Sales

Fully Editable

Instant Download

Professional Design

Pre-Built

No Expertise Is Needed

Description

Owner income$3.0M  Net margin54.8%

Net margin54.8% Revenue for target pay$6.0M

Revenue for target pay$6.0M Business difficultyHard

Business difficultyHard

You’re selling high-ticket stabilization equipment, so revenue can look large while cash still gets tied up in freight, receivables, warranty, and inventory Under the researched first-year assumptions, the model shows $5515M in revenue, 844% gross margin after manufacturing costs, and about $377M before personal taxes, debt service, missing fixed-cost lines, reserves, and reinvestment

Owner income$3.0MNet margin54.8%Revenue for target pay$6.0MBusiness difficultyHardWant to test your owner pay target?

Owner income calculator

Estimate owner take-home and the target-pay gap from revenue, margin, costs, reserves, and target pay.

Planning note: Research-based planning estimate only. It is not guaranteed salary, tax advice, or owner distribution advice.

Want to see owner income laid out?

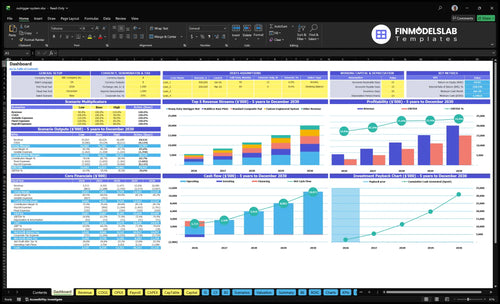

The screenshot shows revenue by product, gross profit, variable costs, fixed expenses, and owner pay. Open the Outrigger Stabilization System Sales Financial Model Template.

Owner-income model highlights

- Owner pay output included

- Revenue and gross profit

- Scenario testing built in

Which costs affect outrigger supplier owner income most?

For Outrigger Stabilization System Sales, owner income gets hit most by margin leakage, not just direct unit cost. In plain English, the money disappears fast when you stack How Much To Start Outrigger Stabilization System Sales? with 50% indirect manufacturing costs in Year 1 and 110% variable costs from commissions, outbound logistics, and warranty freight under-recovery. Gross margin is not net profit, especially when custom engineering, warranty claims, returns, slow receivables, and weak price discipline stay in the mix.

Direct cost load

- $100 Standard Composite Pad COGS

- $285 Heavy Duty Outrigger Mat COGS

- $2,550 Custom Engineered System COGS

- $52 Stabilizer Base Plate COGS

Margin leakage

- $16 Replacement Polymer Insert COGS

- 50% Year 1 indirect manufacturing costs

- 110% Year 1 variable costs

- Slow receivables cut owner take-home

How does scaling an outrigger system supplier change owner income?

Outrigger Stabilization System Sales can lift owner income from a lean, founder-led setup to a much bigger business, but only if the sales process, credit terms, freight recovery, and warranty control stay tight. The owner-operated model keeps payroll light, yet the founder becomes the bottleneck for quotes, support, and follow-up; the scaled distributor model can push revenue from about $5.5M in Year 1 toward about $20.1M by Year 5, but it also adds reps, installers, warehouse staff, and inventory risk. Here’s the quick math: commissions fall from 50% to 40%, while support and warranty still run 20% to 15%, so scale helps only when close rate stays high.

Owner-led model

- Light payroll keeps cash use low.

- Founder handles quotes and support.

- Sales speed depends on one person.

- Margins stay cleaner, but growth slows.

Scaled distributor model

- Revenue can reach about $20.1M by Year 5.

- Commissions drop from 50% to 40%.

- Support and warranty still take 15%–20%.

- Controls on payment and freight matter most.

How many outrigger systems do I need to sell to pay myself?

You need about 776 units to cover $276k in fixed overhead and pay yourself $100k pre-tax, assuming the Year 1 mix holds; for margin levers, see How Increase Outrigger Stabilization System Profitability?. Here’s the quick math: $4.046M contribution ÷ 8,340 units = about $485 contribution per unit.

Pay math

- $5.515M Year 1 revenue

- 8,340 total units sold

- 73.4% contribution margin

- 776 units for $100k owner pay

Watch cash

- Quote quality drives real pay

- Low close rates waste capacity

- Deposits can delay distributions

- Inventory and warranty timing matter

Want the six income drivers at a glance?

1

$5.5M-$20.1MQuote Volume

More qualified quotes that turn into orders drive the fastest revenue lift, and that is the biggest path to owner take-home.

2

$145-$20.5KOrder Mix

Higher average order value and the right product mix push each sale harder, from small replacement parts to custom systems.

3

84%-89%Gross Margin

Tight control of landed cost, freight, and supplier cost keeps more gross profit in the business and lifts EBITDA.

4

$1.15MCash Cycle

Better control of inventory, deposits, and receivables lowers cash tied up in the business and protects owner returns.

5

2.0%-1.5%Support Load

Lower install, support, and warranty drag keeps more of each order after the sale closes.

6

5.0%-4.0%Channel Mix

A balanced sales channel mix reduces concentration risk and helps keep selling costs from eating into profit.

Outrigger Stabilization System Sales Core Six Income Drivers

Qualified Leads and Quote Close Rate

Qualified Leads and Quote Close Rate

When quote requests come from crane, rental, utility, construction, municipal, and industrial buyers with budget, specs, and timing, owner income rises faster than traffic alone. Track qualified leads, quote close rate, average quote value, and lost-deal reason so you can see which quotes turn into orders and which ones just burn sales time.

Raw traffic is weak if buyers only want low-value replacement parts. A stronger close rate turns the known $23k per month fixed overhead into profit, but chasing unqualified custom work can tie up engineering hours without orders and drag cash out of the business.

Measure the quote funnel hard

Count only leads with budget, equipment specs, and timing. Then compare close rate by buyer type so you know whether quote volume is healthy or just busy. One clean rule: if the buyer cannot define the job, the lead is probably not worth engineering time.

- Track lost deals by reason.

- Separate parts, packages, custom work.

- Price engineering time before quoting.

1

Average Order Value and Product Mix

Average Order Value and Product Mix

Average order value is what one sale is worth, while product mix is the share of sales by item. Here that matters a lot because prices run from $145 for Replacement Polymer Inserts to $18,500 for Custom Engineered Systems. If more orders move into complete packages, revenue climbs faster, but only if the added engineering and warranty load still leaves enough gross profit for owner pay.

Here’s the quick math: more high-spec orders can lift monthly sales without adding many units, so unit count alone can mislead. A business selling mostly low-price inserts needs far more volume to cover fixed costs than one selling pads, mats, base plates, and engineered systems. The risk is simple: a richer mix can grow revenue, but a bad mix can drag cash flow through support hours and rework.

Track mix, not just units

Measure revenue by product, gross profit per product, and support hours per order. That shows which sales actually fund overhead and owner draw, and which ones create hidden service costs. If custom systems need extra design time, price that complexity into the quote instead of letting it leak into margin.

- Separate inserts, pads, and systems

- Price engineering and warranty risk

- Watch support hours per order

The clean rule is: sell the package, but price the complexity. Complete packages can be better than small parts orders, but only when the quote reflects the added labor, support, and post-sale risk. If the mix shifts toward custom work without higher gross profit, owner income falls even when revenue looks stronger.

2

Gross Margin After Landed Cost

Gross Margin After Landed Cost

For outrigger system sales, landed cost is the full cost to make the product sellable: direct materials, direct labor, indirect manufacturing, freight gaps, warranty, commissions, and overhead. The source model shows Year 1 manufacturing COGS of $8,628k on $5,515M revenue, so quote math has to be tight or owner income gets squeezed fast.

When freight is underbilled or custom specs are not priced, gross margin falls dollar for dollar and cash for owner pay falls with it. Every missed cost line is lower profit. Track gross margin by product, not just total revenue, because a high-price custom unit can still lose money if support, freight, or rework is buried in the quote.

Price the Full Delivered Cost

Build quotes from a landed-cost sheet, then check each line against actuals after shipment. Use one view for materials, labor, freight, warranty, commissions, and overhead. If a custom order needs extra engineering or special freight, price it up front so gross profit does not leak into unbilled work.

Here’s the quick math: gross profit = sales price − landed cost. So the owner’s take-home income improves when the team tracks margin by SKU, flags freight shortfalls, and reviews deal exceptions before the quote goes out. If support hours or custom requirements keep rising, margin pressure shows up before cash does.

3

Working Capital and Inventory Control

Working Capital and Inventory Control

Profit is not cash. In this business, money gets tied up in inventory, customer invoices, supplier deposits, freight bills, and slow-moving parts. With 8,340 total units in Year 1, stocking too deep can drain cash before customers pay, so owner income depends on how fast the cash turns back into cash.

Track working capital as inventory + receivables + freight prepayments - customer deposits - payables. If a large fleet order stretches payment terms while the business still pays suppliers and shipping vendors, the cash gap can delay owner distributions even when profit looks healthy on paper.

Track the cash gap, not just sales

Measure inventory reserve, customer deposits, supplier lead times, receivable days, and freight prepayments on every order. Keep a simple aging report for finished goods and slow-moving parts, then buy only what can turn into cash inside the next billing cycle. Cash reserve is separate from owner distributions.

- Set deposits before production starts.

- Match purchases to confirmed demand.

- Cut slow stock before it ages.

- Protect reserve cash from draws.

One late payment can stall owner income if materials and shipping were funded first.

4

Installation Support and Warranty Efficiency

Warranty and support drag on margin

Technical support protects repeat orders, but if it is bundled for free, it cuts owner income fast. The source model sets 20% of Year 1 revenue, or about $1,103k on $5,515M revenue, then 15% by Year 5, or about $3,013k on $20,085M revenue, for warranty and technical support.

That allowance has to cover support calls, replacement parts, returns, field visits, and install coordination. If custom systems need more hand-holding than the quote assumed, margin drops and owner pay gets squeezed. The clean rule is simple: price the support you know will happen, not the support you hope will be rare.

Separate service from product

Track support hours, replacement parts, returns, field calls, and installation coordination by order. That tells you which jobs fit inside the allowance and which ones need a paid service line. One custom order can look profitable on paper and still burn cash if service time is not billed.

- Split quotes by product and freight.

- Price commissioning help separately.

- State warranty scope in writing.

- Cap free support hours per order.

Use quotes that separate product pr ice, freight, commissioning help, and warranty scope. Then support can become paid service revenue instead of silent overhead. That protects gross margin and makes the owner’s draw more predictable.

5

Sales Channels and Customer Concentration

Sales Channel Mix and Customer Concentration

Income is steadier when sales come from several channels instead of one or two big accounts. For this business, the useful channels are crane dealers, equipment rental yards, utility contractors, municipalities, construction fleets, and industrial buyers. Track top-five customer revenue share, repeat-order rate, average payment days, and gross margin by channel so you can see which buyers support owner pay.

One delayed fleet order can push cash flow off track. That risk shows up fast when a large buyer asks for freight concessions or slower terms. More channel spread usually improves pricing power, repeat orders, and replacement-part flow, which helps convert sales into cash the owner can actually draw.

Split the book by buyer type

Tag every order by channel and customer. Then compare margin, payment days, and repeat orders by buyer type. The weak channel is the one that needs custom terms, drags payment, or buys once and stops.

Protect cash with deposits, freight charges, and minimum order sizes where needed. If one customer starts to dominate backlog or asks for concessions, tighten credit and forecast owner draw from the lower-risk channels first.

6

Compare low, base, and high owner-income scenarios

Owner income scenarios

Owner income rises fast as sales move from the opening year to the Year 5 ramp. The swing comes from higher volume, higher ticket values, and a small fixed overhead base.

| Scenario | Low CaseLow Case | Base CaseBase Case | High CaseHigh Case |

|---|---|---|---|

| Launch model | This is the lower earnings path if the launch year stays near the model's first-year pace. | This is the modeled mid-case if the business reaches the Year 3 ramp. | This is the stronger earnings path if the business reaches the Year 5 run rate. |

| Typical setup | Year 1 revenue is about $5.5M, with opening volumes across all five product lines and the modeled fixed overhead still in place. | Year 3 revenue is about $11.5M, with higher unit counts, mid-ramp pricing, and more technical and production support. | Year 5 revenue reaches about $20.1M, with the highest modeled volume, top-end pricing, and a larger support team. |

| Cost drivers |

|

|

|

| Owner income rangeBefore owner reserves | $3.0MYear 1 case | $8.2MYear 3 case | $15.0MYear 5 upside |

| Best fit | Use this to stress-test launch year cash flow and slower sales. | Use this as the planning case for a steady ramp. | Use this to test strong demand, fuller capacity, and pricing power. |

Planning note: Scenario ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions.

Related Products

- Outrigger Stabilization System Sales Porter's Five Forces Analysis

- Outrigger Stabilization System Sales BCG Matrix

- Outrigger Stabilization System Sales Business Model Canvas

- What Are The 5 KPIs For Outrigger Stabilization System Sales?

- Outrigger Stabilization System Sales Business Plan Template in Pre-Written Word

- How Increase Outrigger Stabilization System Profitability?

- What Are Operating Costs For Outrigger Stabilization System Sales?

- Outrigger Stabilization Startup Costs For A $55M Year 1 Plan

- Outrigger Stabilization System Sales Financial Model Template in Excel

- How to Launch an Outrigger Stabilization System Supplier in 90-180 Days

- How To Write An Outrigger Stabilization System Sales Business Plan?

- Outrigger Stabilization System Sales Marketing Mix

- Outrigger Stabilization System Sales Marketing Plan

- Outrigger Stabilization System Sales Business Proposal

- Outrigger Stabilization System Sales PESTEL Analysis

- Outrigger Stabilization System Sales Pitch Deck Example Editable PPTX

- Outrigger Stabilization System Sales Business SWOT Analysis

- Outrigger Stabilization System Sales Value Proposition Canvas

Frequently Asked Questions

Under the researched Year 1 assumptions, modeled pre-tax owner-income capacity is about $377M on $5515M revenue That figure is after manufacturing COGS, variable costs, and $276k of known fixed overhead It is before personal taxes, debt service, unprovided fixed-cost lines, inventory reserves, receivables, and reinvestment