Owner income$22.4M

Owner income$22.4MHow Much Paper Recycling Owners Can Make: $230M First-Year Cash Flow

Fully Editable

Instant Download

Professional Design

Pre-Built

No Expertise Is Needed

Description

Owner income$22.4M  Net margin77.3%

Net margin77.3% Revenue for target pay$28.9M

Revenue for target pay$28.9M Business difficultyHard

Business difficultyHard

Key Takeaways

- Throughput drives volume, and underused capacity hurts cash.

- Cleaner inbound paper lifts sellable yield and margin.

- Freight and contamination can erase sale price gains.

- Fixed overhead needs steady output before owner draws.

Owner income$22.4MNet margin77.3%Revenue for target pay$28.9MBusiness difficultyHardWant to test your owner pay?

Owner income calculator

Estimate owner take-home and the target-pay gap from revenue, margin, costs, reserves, and target pay.

Planning note: Research-based planning estimate only. Actual owner income depends on revenue, margins, payroll, debt, reserves, and taxes. This is not tax advice, salary guidance, or a promise of earnings.

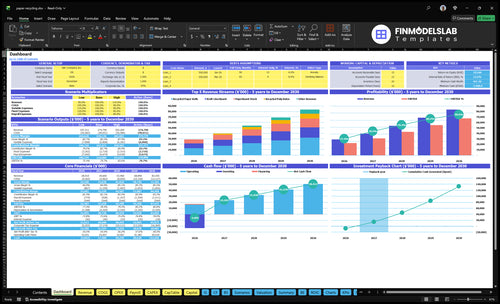

Want to check owner income in the financial model?

It shows revenue, margin, costs, reserves, and owner take-home assumptions in the Paper Recycling Financial Model Template—open it for the full cash flow view.

Owner-income model highlights

- Revenue: $2,891M to $8,343M

- Units: 33,000 to 100,000

- Cash flow: ~$230M to $688M

- Debt, reserves, distributions

How many tons does a paper recycling business need to process?

For Paper Recycling, the data points to sellable units, not inbound tons, so you first size the plant by output: 33,000 units imply about $718 per unit from $2.368M in contribution. Break-even is about 925 units a year, or 77 a month, to cover $5.436M in fixed overhead plus a $120K Plant Manager salary; to turn tons into a real plan, you still need sellable yield after contamination.

Unit math

- 33,000 sellable units in year one

- $2.368M total contribution

- About $718 per sellable unit

- Each extra $100K needs 139 more units

Break-even

- Break-even is about 925 units a year

- That equals about 77 units a month

- Fixed cost base is $5.436M

- Add $120K Plant Manager salary

How much does a paper recycling facility owner make?

A Paper Recycling facility owner does not “make” one fixed salary; take-home depends on salary, draws, and distributions. In the first-year model, $2.891M revenue supports about $230K pre-tax operating cash flow before debt service, reserves, taxes, and payouts, so track cash conversion closely with What Is The Most Important Indicator Of Success For Paper Recycling Business?.

Owner pay scenarios

- $120K if owner acts as Plant Manager

- $230K cash flow before required obligations

- Draws depend on lender and tax limits

- Distributions come after reserves and debt

What changes take-home

- Keep paper volume steady and clean

- Control labor, hauling, and utilities

- Scale regionally only with margin discipline

- Expect higher workload if self-managing

What paper recycling profit margin should owners expect?

Owners should treat Paper Recycling margin as market-dependent, not fixed; with the provided figures, first-year operating margin is about 796% ($230M operating cash flow divided by $2,891M revenue). For startup cost context, see What Is The Estimated Cost To Open The Paper Recycling Facility? The biggest swing comes from pricing, contamination, hauling distance, and labor, because a $10 price move across 33,000 units changes revenue by $330K and contribution by about $3,135K after 50% revenue-based costs.

Big margin drivers

- 796% first-year operating margin

- $10 price move = $330K revenue shift

- Contribution moves about $3,135K

- 1-point cost swing = $2,891K cash-flow change

Margin risks

- Contamination raises rework fast

- Labor use can swing take-home

- Hauling distance cuts margin

- Buyer pricing resets the floor

Want the six income levers?

1

33K-100KInbound volume

More feedstock and runs move sellable output from 33K units in year 1 to 100K in year 5, so income scales fastest here.

2

$420-$1,000Product mix

Mixing more paperboard and linerboard into the sales mix lifts revenue per unit, and that boosts gross margin without adding much plant cost.

3

0-9KSellable yield

Cleaner sorting turns more waste into saleable output; the Tissue Base Stock line rises from 0 to 9K units, so scrap hurts less.

4

15K-35KEquipment uptime

Higher uptime on the paper lines spreads labor and lease costs over more units, so every lost hour cuts take-home.

5

2.2%-3.0%Freight cost

Logistics and sales commissions run at 3.0% in year 1 and 2.2% by year 5, and each point saved stays in margin.

6

$1.21MOverhead discipline

Fixed overhead and payroll are about $1.21M a year, including the $120K Plant Manager, so cost control matters before scale.

Paper Recycling Core Six Income Drivers

Inbound supply and processed volume

Inbound Supply and Throughput

Income rises when clean paper arrives steadily enough to keep the line near planned throughput. The model grows from 33,000 sellable units in year one to 100,000 in a mature year, or about 2,750 units per month at the start. With $453K in monthly fixed costs, every missed load lowers cash flow and makes owner pay harder to support.

This driver includes inbound volume, contamination, sorting, and processing uptime. A dirty or mixed load cuts sellable yield, so the business earns less from the same freight and labor. Here’s the quick math: $453K ÷ 2,750 is about $165 per sellable unit before variable costs. At 100,000 units, that fixed-cost load drops to about $54 per unit.

Track Supply Quality, Not Just Tons

Measure supply by source, route, and grade so you can see which inputs turn into sellable output. The strongest flow comes from haulers, offices, warehouses, printers, and municipal partners. If one source keeps sending mixed loads, margin falls even when inbound volume looks fine. Better yield protects revenue, cuts disposal, and keeps owner draws safer.

- Track sellable units per load.

- Log rejected loads by source.

- Separate clean and mixed paper.

- Forecast cash from processed volume.

1

Sale price and product mix

Recovered Paper Sale Price and Product Mix

Owner income moves with the realized sale price per ton or unit and the mix of finished grades. The spread is wide: recycled pulp bales at $420-$450 sit far below paperboard stock at $920-$1,000, so the product mix can change gross margin fast.

This driver depends on contract price, buyer access, and grade consistency. Use realized price, not quoted price, and stress-test at least a 10%-20% drop before setting owner draws. If the mix tilts toward lower-value pulp, cash for pay-out shrinks even when tons sold stay flat.

Price and Mix Controls to Protect Owner Pay

Track realized price by grade, not just total revenue. A tighter mix toward recycled paper rolls at $850-$910, kraft linerboard at $880-$960, and tissue base stock at $780-$820 supports better income than a weak mix heavy in low-grade output.

- Realized price by product

- Mix by ton or unit

- Contract term and floor

- Rejected grade share

Push premium grades first, lock in buyers before ramping volume, and price new deals off the lowest acceptable margin. If quality slips, lower-grade output can hit cash flow twice: lower sale price and slower owner draws.

2

Contamination rate and sellable yield

Sellable Yield Beats Raw Tons

Higher contamination turns more inbound paper into waste, not revenue. The model should use sellable yield, not raw tons, because rejected material still creates disposal, labor, and rework costs. At a $920–$1,000 paperboard price, one lost sellable unit can wipe out nearly a thousand dollars of revenue.

Cleaner office paper, sorted cardboard, and controlled commercial streams protect gross margin. Track rejected loads by supplier, route, and grade, because mixed loads can make volume look strong while owner take-home falls.

Measure Yield by Stream

Use inbound tons, contamination rate, accepted tons, and sellable units to forecast income. A simple check is: sellable output = inbound material × (1 − contamination rate). That keeps the forecast tied to what actually sells, not what arrives at the gate.

- Log rejects by supplier

- Split routes by paper grade

- Flag dirty loads fast

What this hides: lower contamination also trims sorting labor and disposal, so the same inbound flow can lift cash flow twice. If rejected loads rise, profit drops even when inbound volume holds steady.

3

Equipment utilization and uptime

Equipment Uptime

Balers, conveyors, forklifts, pulpers, sorting lines, and shifts only pay off when they stay running. In this model, monthly output averages 2,750 sellable units in year one and 8,333 in the mature year, so every idle hour delays cash. Downtime is painful because $453K per month of fixed overhead keeps burning while revenue stops.

Model maintenance is 0.5% of revenue, but that does not cover every repair. Owners still need cash for parts, breakdowns, and reserve builds. Here’s the quick math: higher uptime lifts sellable units, spreads fixed cost over more output, and protects owner draw. Underused equipment can make a forecast look strong while real cash stays weak.

Track Runtime, Not Just Assets

Measure scheduled hours, run hours, downtime hours, and sellable units per shift. Also track yield by machine so you can see which step is choking output. If one line or forklift causes stoppages, fix that first. A small uptime gain matters more than a nice-looking capacity chart.

Use a simple operating log with:

- Planned shifts vs. actual shifts

- Downtime by machine

- Repair reserve cash

If uptime slips, cut owner draws before cash gets tight. That keeps the facility funded until output recovers.

4

Hauling and freight cost

Hauling and Freight Cost

If hauling is too expensive, a paper supply deal can look good on revenue and still miss on profit. Modeled logistics and distribution cost runs at 15% of first-year revenue and 11% in the mature year, which is about $4.3M on $28.9M and $9.2M on $83.4M. That cost sits right before owner pay, so freight discipline matters.

This driver includes inbound pickup, bale shipping, and buyer-paid freight. Here’s the quick math: every 1 point of freight on $28.9M revenue is about $289K; on $83.4M, it’s about $834K. Poor route density, long mill distance, and partial truckloads cut net margin per unit, even when the contract price looks fine.

Track route economics, not just sales

Price each load from the route up. Use tons per stop, miles to mill, trailer fill rate, and who pays for freight. Separate pickup cost, bale shipping, and buyer-paid freight in every contract so you can see the real margin by supplier and customer. If a route runs light or far, it should earn a higher fee or get rejected.

- Measure cost per ton by route

- Track partial-load share monthly

- Flag long-distance suppliers fast

This is the line that protects cash. A route that adds freight cost faster than revenue growth can eat the cash needed for payroll, repairs, and owner draws. If contract terms don’t cover the miles, the business is financing the customer. Price the route first, then decide whether the paper itself is worth buying.

5

Operating cost and reserve discipline

Operating Cost and Reserve Discipline

Owner pay comes last, not first. Fixed overhead is $453K per month, or $5.436M per year, plus a $120K Plant Manager salary. In year one, revenue-based COGS add 20% and logistics plus commissions add 30%, so 50% of revenue is already spoken for before owner draw.

Raw paper waste, de-inking agents, pulping enzymes, direct production wages, and packaging all hit cash early. If sales do not cover overhead plus reserves for repairs, working capital, debt service, and reinvestment, the business can look profitable on paper and still run short on cash. No reserve, no draw.

Protect the Draw With Cash Rules

Set the pay order in writing: operating bills first, then reserves, then owner distributions. Track monthly revenue, the 20% COGS load, the 30% logistics and commission load, and the fixed $453K overhead so you can see real free cash, not just gross sales.

- Ring-fence repair reserves each month.

- Cover 30 days of payroll and freight.

- Fund debt service before distributions.

- Hold reinvestment cash back first.

If the reserve bucket is thin, skip the draw and rebuild cash. That protects uptime, avoids missed payments, and keeps the owner from taking money out before the plant can afford it.

6

Owner income scenario table objective

Owner income scenarios

Owner income swings with recovered volume, product mix, and unit costs. The first-year case is three products, the mid case adds pulp and tissue, and the mature case runs all five lines.

| Scenario | Low CaseLow case | Base CaseBase case | High CaseHigh case |

|---|---|---|---|

| Launch model | This is the first-year run rate, built on 33,000 sellable units and the core three paper products. | This is the mid-period run rate, with a fuller mix and steadier throughput. | This is the mature-year upside case, where all five product lines are running at scale. |

| Typical setup | Year 1 only, with about $28.9M revenue from recycled paper rolls, paperboard stock, and kraft linerboard, while pulp bales and tissue base stock are still at zero. | Mid-period volume reaches 65,000 sellable units and about $54.0M revenue as recycled pulp bales and tissue base stock turn on, with more supervisors and QC staff in place. | Mature-year volume reaches 100,000 sellable units and about $83.4M revenue, with higher staffing, logistics, and commission spend but stronger operating spread. |

| Cost drivers |

|

|

|

| Owner income rangeBefore owner reserves | $22.4MFirst-year floor | $42.8MMid-period core | $67.4MMature-year upside |

| Best fit | Use this to stress-test a slow ramp, narrow mix, or tighter working-capital control. | Use this as the main budgeting case for staffing, lender talks, and owner draw planning. | Use this to test strong throughput, fuller capacity use, and the upside if all lines run well. |

Planning note: Scenario ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions.

Related Products

- Paper Recycling Porter's Five Forces Analysis

- Paper Recycling BCG Matrix

- Paper Recycling Business Model Canvas

- 7 Critical KPIs for Paper Recycling Operations

- Paper Recycling Business Plan Template in Pre-Written Word

- 7 Strategies to Boost Paper Recycling Plant Profitability

- Running Costs: How to Operate a Paper Recycling Facility Monthly

- Paper Recycling Startup Costs: Plan Beyond $98K Monthly Overhead

- Paper Recycling Financial Model Template in Excel

- How to Open a Paper Recycling Business With a 33,000-Unit Year 1 Ramp

- How to Write a Paper Recycling Business Plan: 7 Steps

- Paper Recycling Marketing Mix

- Paper Recycling Marketing Plan

- Paper Recycling Business Proposal

- Paper Recycling PESTEL Analysis

- Paper Recycling Pitch Deck Example Editable PPTX

- Paper Recycling Business SWOT Analysis

- Paper Recycling Value Proposition Canvas

Frequently Asked Questions

Under the provided assumptions, first-year pre-tax operating cash flow is about $230M before debt service, taxes, reserves, reinvestment, and owner distributions That comes from $2891M revenue, 33,000 sellable units, and known fixed overhead of $453K per month Actual owner take-home depends on financing, reserves, and how much cash the business keeps