Owner income$0–$151k

Owner income$0–$151kHow Much Does a Party Supply Store Owner Make? $151k EBITDA Case

Fully Editable

Instant Download

Professional Design

Pre-Built

No Expertise Is Needed

Description

Owner income$0–$151k  Net margin83.0%–84.5%

Net margin83.0%–84.5% Revenue for target pay$345k

Revenue for target pay$345k Business difficultyHard

Business difficultyHard

A party supply store owner may take home little or nothing during the early ramp if the store carries full payroll and retail overhead In this researched case, EBITDA is -$158k in Year 1, -$127k in Year 2, and near breakeven at -$1k in Year 3 The model reaches breakeven in Month 32, then shows $151k EBITDA in Year 4 and $699k in Year 5 before taxes, debt service, reserves, and owner distributions

Owner income$0–$151kNet margin83.0%–84.5%Revenue for target pay$345kBusiness difficultyHardWant to test your owner pay?

Owner income calculator

Estimate owner take-home and target-pay gap from revenue, margin, costs, reserves, and target pay.

Planning note: This is a researched planning estimate, not guaranteed salary, tax advice, or owner distribution advice. Actual owner income depends on revenue, margin, payroll, debt, reserves, and timing.

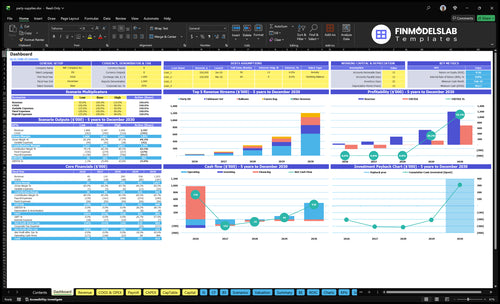

Want to test the full store forecast?

The dashboard shows revenue, gross margin, EBITDA, cash, payback, and owner-income scenarios—open the Party Supply Store Financial Model Template for scenario testing.

Model highlights

- Owner-income scenarios built in

- Year 1 to 5 cash path

- Visitor and cost assumptions tested

How much profit can a party supply store make?

A Party Supply Store can lose money for the first 2 years: EBITDA is -$158k in Year 1 and -$127k in Year 2, then the base case is nearly break-even at -$1k in Year 3. In the stronger case, EBITDA reaches $151k in Year 4 and $699k in Year 5, so track What Is The Most Important Indicator Of Success For Your Party Supply Store? before taking large owner draws.

Profit path

- Year 1 EBITDA: -$158k

- Year 2 EBITDA: -$127k

- Year 3 EBITDA: -$1k base case

- Year 5 EBITDA: $699k stronger case

Key drivers

- Fixed overhead: $558k/year

- Payroll: $120k to $185k

- Conversion: 100% to 200%

- Owner take-home: after reserves, taxes, debt

Is a party supply store profitable if owner-operated?

Yes, it can be profitable if traffic stays strong enough to cover rent, payroll, and seasonality. Here’s the quick math: this model includes a $55k store manager, retail associates, and part-time then full-time marketing support, so payroll is about $120k in Year 1 and $185k in Years 4-5; the $3,500 monthly lease adds another fixed cost. An owner-operated Party Supply Store can lower cash payroll, but that is owner labor, not free profit, so local event demand, online competition, and add-on services decide whether sales turn into income.

What supports profit

- Owner labor cuts cash payroll

- Event demand can lift traffic

- Add-ons raise basket size

- Repeat buyers improve sales mix

What can squeeze margins

- Year 1 payroll is about $120k

- Years 4-5 payroll rises to $185k

- Lease is $3,500 per month

- Seasonality can weaken cash flow

What party supply store profit margin should owners expect?

Party Supply Store owners should expect strong shelf markup, but not all of it turns into cash. The model shows 830% gross margin in Year 1 and 845% in Year 5 after payment processing and packaging, and gross margin is not owner income; if you want the setup-cost side too, see How Much Does It Cost To Open A Party Supply Store?

Shelf markup

- Balloons start at 300% of sales mix

- Tableware runs at 250%

- Favors run at 200%

- Party kits run at 250%

Cash leaks

- Contribution margin is 805% to 827%

- Year 1 gross margin is 830%

- Year 5 gross margin is 845%

- Markdowns, shrink, freight cut take-home

Which six drivers move owner income most?

1

10%-20%Traffic Lift

More walk-ins and a 10% to 20% visitor-to-buyer rate drive the most orders, and repeat buyers at 25% to 45% of new sales keep the register moving.

2

80%-83%Mix Margin

Shifting mix toward party kits lifts margin, while balloons and tableware need tight pricing to keep gross margin in the 80%-83% range.

3

$463KInventory Cash

Slow stock turns trap cash, and markdowns can push the business into the $463K cash low around Month 38 even after breakeven in Month 32.

4

$3.5KRent Load

The $3,500 lease only works when each visit covers the space, so low traffic makes rent one of the fastest drags on take-home.

5

$120K-$185KLabor Load

Labor climbs from about $120K in Year 1 to $185K by Years 4-5, so the owner-operator model matters more than almost any ad spend.

6

4-6 unitsAdd-Ons

Balloon arrangements and custom bundles raise units per ticket from 4 to 6, which adds revenue without the same jump in rent or labor.

Party Supply Store Core Six Income Drivers

Sales Volume

Sales Volume

Owner income rises only when traffic turns into profitable orders. In this model, weekly visitors grow from 310 in Year 1 to 830 in Year 5, while conversion is assumed to improve from 100% to 200%. Repeat customer share rises from 250% to 450%, and repeat life extends from 6 to 12 months. More visits help, but only if each basket carries enough gross profit.

Here’s the quick math: fixed overhead starts at $558k/year before payroll, so weak conversion leaves rent and staff uncovered. Higher basket size matters because every order must pay its share of store costs, inventory, and labor. If traffic grows without better close rates or repeat sales, the owner can look busy and still take home little or nothing.

Track Conversion and Basket Size

Measure weekly visitors, orders, average basket, and repeat share by customer type. That shows whether the store is creating enough profitable sales to support owner pay. The goal is simple: keep more of the 310 to 830 weekly visitors buying, and keep those buyers coming back for longer than 6 months.

- Track visitors versus orders weekly.

- Split first-time and repeat sales.

- Watch average basket by category.

- Forecast cash before owner draw.

- Stop pay if overhead is uncovered.

If conversion stalls while fixed costs stay at $558k/year before payroll, the model burns cash fast. The owner should only add staffing or take more draw after sales volume, basket size, and repeat buying are strong enough to cover the full cost stack.

1

Product Mix And Gross Margin

Product Mix Drives Gross Margin

Product mix is the split of what shoppers buy: balloons, tableware, favors, and party kits. In this model, balloons move from 300% to 250% of mix, tableware from 250% to 200%, favors stay at 200%, and party kits rise from 250% to 350%. That matters because party kits carry the top Year 1 price at $5,000, while favors start at $1,200.

Here’s the quick math: a richer kit mix can lift average order value and gross profit before store overhead. The model shows gross margin after inventory and inbound shipping rising from 830% to 845%. What this hides: if markdowns rise or kits sit too long, cash gets trapped and owner pay gets squeezed even when sales look strong.

Track Mix, Then Protect Margin

Watch category mix, unit sell-through, markdown rate, inbound freight, and average order value. If kits are growing, make sure their margin beats the extra packaging, handling, and discount risk. One bad theme can turn good revenue into dead stock. More kits help only when they sell at full price.

- Unit mix by category

- Markdown rate by theme

- Inbound shipping per order

- AOV by basket type

Push more kits only when AOV rises and markdowns stay flat. If kits lift basket size but force clearance later, the owner keeps less cash. That hurts the money available for payroll, overhead, and any owner draw.

2

Inventory And Seasonal Control

Inventory Cash Control

Inventory cash is what decides whether profit turns into money the owner can actually take home. In this model, inventory purchases run 150% of revenue in Year 1 and 140% by Year 5, while inbound shipping drops from 20% to 15%. Seasonal goods can miss local demand, then shrink, markdowns, and obsolete stock drain cash even when accounting profit still looks fine.

The key inputs are revenue, purchase timing, shipping cost, markdown rate, and cash reserve. The hard warning sign is the model’s minimum cash need of $463k in Month 38, so inventory planning is not just a margin issue; it directly limits owner draws and can force the business to hold back cash instead of paying it out.

Track Stock, Then Buy Slower

Measure inventory by theme and season, not just by total dollars. Watch sell-through, shrink, obsolescence, and markdowns before you reorder. If a theme is lagging local demand, cut buys early and protect cash. The goal is simple: keep stock turning fast enough that owner income comes from real sales, not from money trapped on the shelf.

- Track purchases as % of revenue.

- Review shipping at 15% to 20%.

- Flag slow themes fast.

- Hold cash for Month 38.

3

Location And Occupancy Cost

Location And Occupancy Cost

A visible storefront can bring walk-ins, but it only helps if those visits turn into profitable orders. In this model, the lease is $3,500/month and fixed occupancy overhead is $4,650/month before payroll. That annualizes to $55,800/year, so the space has to earn its keep through sales, not just traffic.

About 75% of that fixed load is rent, so location is the biggest swing cost. If local party demand is weak, the store can still look busy and still miss cash targets. Poor conversion, weak repeat orders, or a low average transaction value turns rent into a fixed-cost trap.

Make Rent Pay Back

Track daily traffic, conversion rate, repeat orders, and average transaction value. Those four inputs tell you whether the location is covering its fixed cost or just adding overhead. One clean test: if more foot traffic does not lift basket size or repeat visits, the lease is too heavy for the demand you have.

Use event weekends, school seasons, and holiday spikes to test whether the store location improves sales quality. If the space does not produce enough gross profit to cover $4,650/month before payroll, cut occupancy risk fast. Protect cash first, then pay for location only when it clearly raises owner income.

4

Staffing And Owner Role

Payroll and Owner Labor

Payroll is the biggest controllable cost after inventory, so it sets how much cash is left for the owner. This plan starts staffing at $120k in Year 1 and rises to $185k in Years 4-5, with a $55k store manager, $30k retail associates, and $40k FTE marketing support. If sales do not cover those salaries, owner pay gets squeezed fast.

If the owner works the floor or handles balloon arrangements, cash payroll can drop, but that is not free labor. Owner time should be priced before profit, because unpaid hours can hide the true break-even point. The key inputs are staff count, wage levels, owner hours, and whether the owner is replacing paid labor or adding sales capacity.

Price Owner Hours First

Track manager pay, associate pay, and owner hours separately. If the owner runs the register or builds custom balloon work, record those hours at a market rate and treat that as a real cost. That keeps cash profit from looking better than it is.

- Measure payroll as percent of sales.

- Separate owner labor from profit.

- Check if each hire boosts conversion.

Watch whether added staff lifts basket size, repeat visits, or event orders enough to cover the wage load. If it does not, the store is buying labor, not margin. Year 1 payroll at $120k only works if the floor team turns traffic into paid orders.

5

Add-On Services And Bundles

Add-On Bundles

Balloon arrangements, custom party orders, local delivery, and themed bundles raise ticket size without turning the store into an event planner. If units per order move from 4 to 6, basket size rises 50%. Party kits carry the highest listed unit price, at $5,000 in Year 1 and $5,500 by Year 5, so the real profit lever is how much of that price stays after labor and materials.

Here’s the catch: add-ons only help owner pay if pricing covers materials, labor, packaging, payment fees, and delivery time. Underpriced custom work can turn busy weekends into low-pay work. A bundle that looks strong on revenue can still hurt cash flow if it needs extra staff time, late delivery runs, or remake risk.

Price the Extra Work First

Track each add-on by ticket size, labor minutes, and gross margin. If a custom order needs delivery or setup, price those costs separately instead of hiding them in the base sale. That keeps the owner’s take-home pay tied to margin, not just sales volume.

Test bundle prices against the real inputs below:

- Materials per order

- Minutes per order

- Delivery miles and time

- Payment fees and packaging

If a bundle adds work but not margin, drop it or simplify it. One clean rule: if the add-on does not pay for itself, it is not a profit item.

6

Owner income scenario objective

Owner income scenarios

Owner income swings with foot traffic, basket size, and staffing. This store is cash-heavy early, then improves as conversion and repeat purchases rise.

| Scenario | Low CaseCash-heavy start | Base CaseBreakeven path | High CasePayroll-sensitive upside |

|---|---|---|---|

| Launch model | The low case keeps the store in ramp mode, so owner pay stays at zero. | The base case reaches breakeven by Month 32 and supports a modest owner draw by Year 4. | The high case scales traffic and repeat orders enough to produce strong owner income by Year 5. |

| Typical setup | Foot traffic stays light, conversion remains weak, and payroll plus inventory eat most gross profit. | Traffic climbs, fixed costs are covered, and the store starts to produce steady EBITDA before owner pay. | Weekend traffic, conversion, and repeat buying run stronger, while staff and inventory grow to support volume. |

| Cost drivers |

|

|

|

| Owner income rangeBefore owner reserves | $0No owner draw | $151kMeasured income | $699kStrong upside |

| Best fit | Use this to stress-test the first two years and the cash burn. | Use this as the normal ramp case for a steady store with controlled growth. | Use this to test a mature store with strong execution and heavier staffing. |

Planning note: These scenario ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions.

Related Products

- Party Supply Store Porter's Five Forces Analysis

- Party Supply Store BCG Matrix

- Party Supply Store Business Model Canvas

- 7 Essential KPIs to Track for a Party Supply Store

- Party Supply Store Business Plan Template in Pre-Written Word

- 7 Financial Strategies to Increase Party Supply Store Profitability

- Analyzing Monthly Running Costs for a Party Supply Store

- Party Supply Store Startup Costs: $84K CAPEX Plus Cash Reserve

- Party Supply Store Financial Model Template in Excel

- How To Open A Party Supply Store In 8–16 Weeks And Make First Sales

- How to Write a Party Supply Store Business Plan

- Party Supply Store Marketing Mix

- Party Supply Store Marketing Plan

- Party Supply Store Business Proposal

- Party Supply Store PESTEL Analysis

- Party Supply Store Pitch Deck Example Editable PPTX

- Party Supply Store Business SWOT Analysis

- Party Supply Store Value Proposition Canvas

Frequently Asked Questions

The owner may pay themselves only after the store covers operating losses, inventory cash, taxes, debt, and reserves In this case, EBITDA is negative in Years 1 and 2, near breakeven in Year 3, then $151k in Year 4 and $699k in Year 5 That is not the same as guaranteed salary