Owner income-$270k to $1.53M

Owner income-$270k to $1.53MHow Much Can a Paver Block Manufacturing Owner Make? $0 to $225M Before Debt

Fully Editable

Instant Download

Professional Design

Pre-Built

No Expertise Is Needed

Description

Owner income-$270k to $1.53M  Net margin-61% to 50%

Net margin-61% to 50% Revenue for target pay$3.03M

Revenue for target pay$3.03M Business difficultyHard

Business difficultyHard

You’re buying equipment, renting factory space, and trying to turn heavy blocks into owner pay Based on the provided five-year model, revenue grows from $443,000 to $3027M, while cash after operating overhead and a $120,000 general manager ranges from about $0 to $225M before taxes, debt service, reserves, and owner-specific distributions

Owner income-$270k to $1.53MNet margin-61% to 50%Revenue for target pay$3.03MBusiness difficultyHardWant to test your owner pay?

Owner income calculator

Estimate owner take-home and the target-pay gap from revenue, margin, costs, reserves, and target pay.

Planning note: This is a researched planning estimate, not guaranteed salary, tax advice, or owner distribution advice.

How does the model show owner income?

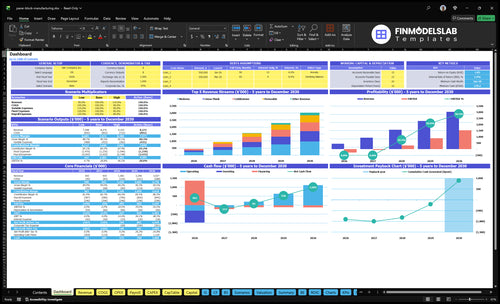

This Paver Block Manufacturing Financial Model Template screenshot shows revenue, margin, costs, reserves, and owner pay—open the model.

Owner-income model highlights

- Owner pay by scenario

- Revenue and contribution margin

- Units rise to 610,000

What revenue is needed to pay a paver block manufacturing owner?

For Paver Block Manufacturing, owner pay is not supported in year 1 under the managed staffing setup. With $366K in first-year fixed expenses plus manager payroll and an 81.9% contribution margin, break-even revenue before owner pay is about $447K a year, while modeled first-year revenue is only $443K. Every $1 of owner pay or reserve needs about $1.22 of extra revenue at that margin, and about $1.16 at the 86.5% mature-year margin.

Year 1 math

- $366K fixed cost base

- 81.9% contribution margin

- $447K break-even revenue

- $443K modeled revenue

Cash pressure

- $1.22 extra revenue per $1 pay

- $1.16 at mature-year margin

- Debt service lifts the target

- Inventory cash also lifts it

Is paver block manufacturing profitable at scale?

Yes—Paver Block Manufacturing can be profitable at scale, but only when utilization stays high. At 100,000 units, first-year volume barely covers $246K in fixed expenses plus $120K of manager payroll, while 610,000 units spread that same base much better and produce about $225M in operating cash before taxes, debt, reserves, and owner distributions.

What drives profit

- Uptime keeps output moving

- Curing capacity limits volume

- Collections protect cash

- Working capital needs tight control

Main scale risks

- Hiring managers adds $120K payroll

- Extra shifts raise maintenance risk

- More inventory ties up cash

- Delivery delays can cut sales

How much can a paver block manufacturing owner make?

A Paver Block Manufacturing owner can range from about -$34K in first-year operating cash to about $969.6K at contractor-supply scale and about $2.25M in a mature high-utilization plant, before debt, taxes, and reserves. The answer is scenario-based, not a universal salary; for demand context, see What Is The Current Growth Rate Of Paver Block Manufacturing?.

Owner income scenarios

- Year 1: 100,000 units; $443K revenue

- Contribution margin: 81.9%; cash about -$34K

- Year 3: 330,000 units; $1.581M revenue

- Operating cash: about $969.6K before deductions

What changes pay

- Mature plant: 610,000 units; $3.027M revenue

- Contribution margin: 86.5%; cash about $2.25M

- Manager role: owner-operator changes cash by $120K

- Fixed costs: first-year overhead includes $246K

Want to see what drives owner income?

1

100K-610KCapacity Use

Higher plant use spreads fixed rent, payroll, and maintenance across more blocks, so owner take-home rises fastest as output moves from 100K to 610K units.

2

$4.43-$4.96Price Mix

A better mix pushes blended price from about $4.43 to $4.96, with product prices from $3.50 to $6.30, and that lifts gross profit without much extra fixed cost.

3

$0.32-$0.54Raw Materials

Cement, aggregates, and pigments set the cost floor at about $0.32 to $0.54 per unit by product, so small input swings can move margin fast.

4

$0.06-$0.10Labor Scrap

Direct labor, rework, waste, breakage, and curing defects cut take-home when yield slips, because every bad block adds cost without adding revenue.

5

Net 30-60Channel Mix

More contractor volume and faster payment terms improve cash flow, while direct local sales can raise margin if service costs stay in check.

6

1.5%-3.0%Cash Drag

Freight, pallets, inventory, reserves, and loan payments can trap cash, so cutting logistics from 3.0% to 1.5% helps protect owner income.

Paver Block Manufacturing Core Six Income Drivers

Capacity utilization

Capacity Utilization

Income here comes from spreading $246K of fixed expenses across more sellable units. At 100,000 units, fixed cost is about $2.46 per unit; at 610,000 units, it drops to about $0.40 per unit. That’s the clean math: more loaded machine hours, molds, curing space, forklifts, and shifts means more contribution margin left for owner pay.

The risk is not just low output. Downtime, curing bottlenecks, and unsold inventory can block the plant even when demand is there. If units stack up before sale, cash gets trapped in stock instead of moving into profit and draw. Capacity only helps income when production stays close to demand and finished pavers ship fast.

Track the bottlenecks

Measure machine hours used versus available hours, plus mold turns, curing bay load, forklift uptime, and shift coverage. If one step is the constraint, that step sets the plant’s real output. A simple weekly rule helps: if finished goods pile up, stop chasing more starts and fix the slowest handoff first.

Use a unit-cost check each month: $246K ÷ annual units. When volume rises, fixed cost per unit falls and gross dollars available for owner pay rise. But to be fair, only count that gain if scrap, rework, and inventory days stay controlled. One clean line: more sold units beat more produced units.

- Track throughput by shift.

- Watch curing queue time.

- Log downtime by cause.

- Cap finished inventory buildup.

1

Selling price and product mix

Selling Price and Product Mix

Selling price and mix drive how much cash each unit brings in. Modeled prices run from $350 for interlock pavers to $630 for permeable pavers, and the blended price moves from $443 to $496. That gap matters because a better mix lifts revenue and gross dollars per unit, which leaves more room for overhead and owner pay.

The real input is mix by SKU, not just list price. Bulk contractor accounts can keep volume moving and help utilization, but they may pull the average price down. Direct local sales can support a higher price, yet they take more selling effort and delivery coordination. If premium orders slow production, the higher price can turn into lower take-home income.

Measure Mix by SKU and Channel

Track units by product type, blended price, discount rate, and gross dollars per unit each month. Revenue equals units sold times the weighted average price, so a shift toward linear plank and permeable products only wins if throughput stays steady. If premium jobs create extra changeovers or delays, the price lift can disappear in lower output and weaker cash flow.

- Price each SKU separately.

- Split contractor and direct sales.

- Watch premium share weekly.

- Track gross dollars per production hour.

- Test price against lost volume.

2

Raw material cost control

Raw Material Cost Control

This driver covers cement, aggregates, sand, pigments, additives, mix design, supplier terms, and waste. In this model, direct unit cost runs from $0.32 to $0.54 by product type, so small buy or yield changes move gross margin fast.

Here’s the quick math: at 610,000 units, a $0.01 per-unit change equals $6,100. Cement and binder costs hit several SKUs, while pigments and specialty additives matter most on colored and permeable pavers. That change shows up before owner pay as either cleaner contribution margin or cash leakage.

Lock the mix and buy terms

Track cost per unit by SKU, plus waste %, dosage rates, and supplier price changes. If one product uses more pigment or binder, price it with that in mind so margin does not quietly shrink.

Use order-size checks, tighter specs, and monthly vendor quotes to cut drift. One penny matters when volume is high, and better mix control protects the cash left for owner distributions.

3

Labor productivity and scrap

Output per crew hour and scrap

When output per crew hour rises, the plant spreads labor across more sellable pavers. Direct labor runs $0.06 to $0.10 per unit, so small gains matter. On 610,000 units, a $0.01 labor swing changes annual labor cost by $6,100. Scrap, rework, and curing losses push that cost higher fast.

The key inputs are crew hours, good units, rework units, curing losses, and damaged inventory. Quality issues hurt twice because the plant pays for labor and materials, then loses saleable volume. Watch color consistency, strength tests, curing discipline, pallet handling, and mold wear. That is what turns the same crew and equipment into more cash for owner pay.

Cut scrap and rework

Track good units per crew hour every shift, not just total output. Add a scrap log with cause codes for color, curing, pallets, molds, and breakage. Keep rework and waste near the model benchmark of 2% of sales; if it rises, gross margin and cash flow drop before the owner sees it in pay.

- Count saleable units by shift.

- Separate scrap by cause.

- Check curing time daily.

- Inspect pallets and molds often.

- Fix the biggest defect first.

Use the numbers to staff and plan. If a crew hour stops producing good units, the plant is burning labor on inventory that never becomes cash. Tight controls on setup, curing, and handling protect margin and keep more of each sales dollar available for debt service, reinvestment, and owner draws.

4

Sales channel and customer mix

Sales mix and customer concentration

This driver is about who buys your pavers, how often they reorder, and how fast they pay. Contractor and dealer accounts can keep the plant running, but they often want bulk pricing and longer terms; direct local sales can lift average price, but they take more selling time and delivery work. The real income test is not just revenue, it’s cash conversion and customer concentration.

Here’s the quick math: the model cuts sales and marketing variable costs from 50% to 25% as scale improves, so the same revenue leaves more margin for owner pay. But if a few contractor accounts drive most orders, one delayed job can hit utilization and collections at once. One clean loss of control here can shrink profit before it shows up in sales.

Track mix, terms, and collections

Measure customer share, days to collect, average selling price, and repeat order rate by channel. Split sales into contractor, dealer, and direct local work so you can see which mix gives the best margin per delivered load, not just top-line revenue. If direct sales raise price but add too much delivery effort, the extra revenue may not reach owner income.

Set limits on concentration and payment lag. If one contractor or dealer becomes too large, the plant may look busy while cash stays tied up in receivables. Watch for slow-paying accounts, because weaker collections can delay payroll, fuel, and profit draws even when the month looks good on paper. The best mix keeps orders steady and cash coming in faster.

5

Delivery, debt, and working capital burden

Delivery, debt, and cash lockup

This driver includes heavy product moves, pallet handling, forklifts, trucks, local delivery radius, maintenance, and loan payments. Logistics variable cost is modeled to fall from 30% of revenue to 15% as volume scales, but that does not fix cash trapped in inventory and receivables. The business can show profit on paper while owner pay stays tight.

Here’s the quick math: fixed maintenance is $1,000 per month, or $12,000 per year, and equipment debt service is not included, so it must be added before calling cash available for draws. If deliveries are long, pallets turn slow, or repairs spike, cash gets stuck and distributions usually shrink.

Track cash in motion, not just profit

Measure delivery cost as a share of revenue, then split it into freight, pallets, fuel, and repairs. Also track days in inventory and days to collect, because those two items decide how much cash the owner can actually take home. A business with good margin can still run short if cash is tied up for too long.

- Track delivery cost by job and route.

- Enter debt service before draw forecasts.

- Plan reserves for repairs and slow cash.

Use the model to test local radius, truck usage, and maintenance contracts before raising owner distributions. If the plant needs more forklifts, more pallets, or longer receivable terms, cash pressure rises fast. The clean rule is simple: if working capital grows faster than sales, owner pay falls unless reserves are set aside first.

6

Compare low, base, and high paver block owner-income scenarios

Owner income scenarios

Higher volume and better utilization drive owner income fast in this plant business. Low output can stay near cash break-even, while strong local demand can lift cash flow sharply.

| Scenario | Low CaseLow utilization | Base CaseBalanced scale | High CaseHigh utilization |

|---|---|---|---|

| Launch model | This is the early ramp case, where output is still thin and owner cash stays near breakeven or slightly negative. | This is the modeled midscale case, where steady contractor and dealer demand supports positive owner cash flow. | This is the upside case, where mature utilization and disciplined operations push owner cash much higher. |

| Typical setup | About 100,000 units and $443K revenue at a $4.43 blended price, with about 81.9% contribution margin and $246K fixed expenses plus $120K manager payroll. | About 330,000 units and $1.581M revenue at a $4.79 blended price, with about 84.5% contribution margin and about $969K operating cash before owner-specific items. | About 610,000 units and $3.027M revenue at a $4.96 blended price, with about 86.5% contribution margin and about $2.25M operating cash before owner-specific items. |

| Cost drivers |

|

|

|

| Owner income rangeBefore owner reserves | -$34KLow cash band | $969KBase cash band | $2.25MHigh cash band |

| Best fit | Use this to stress-test launch-stage local production demand. | Use this for an established contractor and dealer demand plan. | Use this to test upside from strong local demand and steady execution. |

Planning note: These scenario ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions.

Related Products

- Paver Block Manufacturing Porter's Five Forces Analysis

- Paver Block Manufacturing BCG Matrix

- Paver Block Manufacturing Business Model Canvas

- 7 Production KPIs for Paver Block Manufacturing Success

- Paver Block Manufacturing Business Plan Template in Pre-Written Word

- 7 Strategies to Boost Paver Block Manufacturing Profit Margins

- How Much Does It Cost To Run A Paver Block Manufacturing Business Each Month?

- Paver Block Manufacturing Startup Costs For A 100,000-Unit Year 1

- Paver Block Manufacturing Financial Model Template in Excel

- How to Open a Paver Block Manufacturing Business in 3 to 6 Months

- How to Write a Paver Block Manufacturing Business Plan

- Paver Block Manufacturing Marketing Mix

- Paver Block Manufacturing Marketing Plan

- Paver Block Manufacturing Business Proposal

- Paver Block Manufacturing PESTEL Analysis

- Paver Block Manufacturing Pitch Deck Example Editable PPTX

- Paver Block Manufacturing Business SWOT Analysis

- Paver Block Manufacturing Value Proposition Canvas

Frequently Asked Questions

Under the provided assumptions, operating cash ranges from about $0 in the first year to $225M in the mature year before taxes, debt, reserves, and owner distributions Revenue rises from $443K to $3027M, and contribution margin improves from 819% to 865% as volume scales from 100,000 to 610,000 units