Owner income$165k

Owner income$165kHow Much Payables Management Service Owners Make By Year 5

Fully Editable

Instant Download

Professional Design

Pre-Built

No Expertise Is Needed

Description

Owner income$165k  Net margin-116% to 33%

Net margin-116% to 33% Revenue for target pay$180k+

Revenue for target pay$180k+ Business difficultyHard

Business difficultyHard

You’re estimating owner income from a US payables management service, not employee accounts payable wages or generic bookkeeping fees In the model, revenue grows from $474,000 in Year 1 to $5535 million in Year 5, while EBITDA moves from -$550,000 to $1815 million Owner take-home depends on whether the modeled $165,000 CEO salary is funded by cash flow, not treated as an automatic distribution

Owner income$165kNet margin-116% to 33%Revenue for target pay$180k+Business difficultyHardWant to test your payables management owner income?

Owner income calculator

Estimate owner take-home and the target-pay gap from revenue, margin, costs, reserves, and target pay.

Planning note: Research-based planning estimate only. Actual owner income depends on revenue, margin, payroll, taxes, reserves, and reinvestment. It is not guaranteed salary, tax advice, or owner distribution advice.

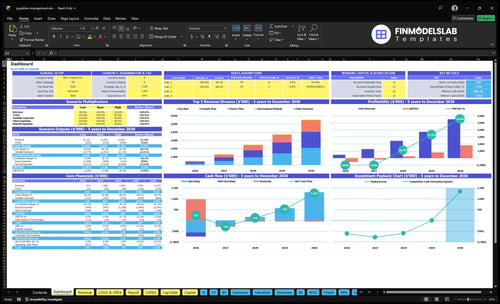

Want to see the full Payables Management Service forecast?

The dashboard shows revenue ramp, EBITDA, cash low point, breakeven, payback, and owner pay; open the Payables Management Service Financial Model Template.

Model highlights

- Revenue: $474K to $5.535M

- EBITDA: -$550K to $1.815M

- Assumptions: tiers, CAC, fees

How many clients does a payables management service need to pay the owner?

A Payables Management Service needs about 46 Year 1 average clients just to cover the modeled $165,000 CEO salary, before payroll, marketing, software, transaction fees, overhead, or reserves. Here’s the quick math for How To Launch Payables Management Service?: $165,000 / 12 / $297 weighted monthly revenue per client = 46.3 clients. The full model reaches breakeven at Month 22, so client revenue isn’t owner cash while EBITDA is negative.

Owner Pay Math

- $165,000 annual CEO salary

- $13,750 monthly owner pay target

- $297 Year 1 revenue per client

- 46 clients before other costs

Breakeven Reality

- $447 Year 5 revenue per client

- 31 clients cover salary only in Year 5

- Month 22 modeled breakeven point

- Negative EBITDA blocks owner cash

What affects payables management service profit margin?

Profit margin in a Payables Management Service gets squeezed by AP labor, invoice exceptions, payment method costs, and support, so if you’re mapping How To Launch Payables Management Service?, the real test is whether revenue grows faster than cost. In Year 1, direct cloud/API cost is 45% of revenue and payment network fees are 35%; by Year 5 those drop to 35% and 27%, but fixed overhead still sits at $14,000 per month. Payroll rises from $605,000 in Year 1 to $1.93 million in Year 5, so owner take-home improves only if revenue outpaces those costs.

Margin drains

- AP labor adds manual handling.

- Invoice exceptions slow payment work.

- Cybersecurity and compliance add spend.

- Payment fees hit 35% in Year 1.

Margin levers

- Cloud/API cost falls to 35% by Year 5.

- Network fees fall to 27% by Year 5.

- Fixed overhead stays at $14,000 monthly.

- Revenue must outrun payroll growth.

How does a payables management service make money?

Payables Management Service makes money from monthly retainers on tiered plans, plus fees for onboarding, reporting, controls support, an international module, and scoped volume-based processing. In Year 1, pricing is $149 Starter, $349 Growth, $749 Pro, and $99 for the international module, then rises by Year 5 to $169, $399, $849, and $119. The model’s revenue grows from $474,000 to $5.535 million, but owner income only works if added scope does not turn into manual AP labor.

How it earns

- Starter at $149 monthly

- Growth at $349 monthly

- Pro at $749 monthly

- $99 international module

Margin drivers

- Onboarding work adds setup fees

- Reporting add-ons lift ARPU

- Controls support can be billed

- Keep scope from becoming labor

Want the six drivers behind owner income?

1

$474K-$5.5MActive Clients

More active clients lift revenue from the first year to year 5, and that is the biggest swing in owner take-home.

2

$149-$849Price Mix

A better mix of Starter, Growth, Pro, and International fees raises revenue per client without adding the same amount of work.

3

$605K-$1.93MPayroll Load

Payroll rises fast as sales, tech, and service staff scale, so lean hiring protects cash and owner profit.

4

80%-62%Margin Mix

Lower direct variable cost as the business scales leaves more of each dollar billed to flow through to the owner.

5

3.5%-2.7%Fee Control

Lower payment network fees keep transaction costs down, so more of the billed amount stays in the business.

6

$14K/moOverhead Floor

Cybersecurity, legal, software, rent, and utilities set the fixed cash floor, so tight control here protects take-home.

Payables Management Service Core Six Income Drivers

Active Client Count

Active Client Count

Active client count drives recurring revenue because each retained client adds monthly subscription income. With a weighted average monthly revenue per client of $297 in Year 1 and $447 in Year 5, modeled revenue rises from $474,000 to $5.535 million. That implies about 133 active clients in Year 1 and 1,032 in Year 5.

Owner income improves only if delivery capacity holds. Add low-fit clients and support tickets, approval exceptions, and payment errors go up, so margin gets thinner even as revenue grows. CAC improves from $450 to $350, but annual marketing also rises from $120,000 to $700,000, so growth has to stay efficient.

Track Retained Clients and Fit

Measure active clients by cohort, tier, and churn. The core formula is active clients × monthly revenue per client, but that only helps if support hours do not rise faster than revenue. A clean client base should lift owner pay through steadier recurring cash and fewer manual fixes.

Watch retention, CAC, payment error rate, and support tickets per client together. If marketing spend climbs from $120,000 to $700,000, each new client needs to stay long enough to cover acquisition cost and service load. Tight onboarding and strict fit checks protect cash flow.

1

Revenue Per Payables Management Client

Plan Mix Per Client

When more clients move into Pro and add the international module, revenue per payables management client rises without needing the same client count. Year 1 pricing is $149 Starter, $349 Growth, $749 Pro, and $99 for international. By Year 5, that moves to $169, $399, $849, and $119.

The mix shift is the real driver: Pro allocation rises from 15% to 25%, and international rises from 5% to 20%. That can lift top-line revenue and owner pay, but only if scope stays tight. If manual vendor follow-up and approval chasing grow with premium clients, the extra fee gets eaten by labor and rework.

Track Mix, Not Just Client Count

Measure monthly revenue per client, plan mix, module attach rate, and support time per account. The key inputs are client count, plan tier, and how often premium clients trigger exceptions. One clean check: if Pro and international shares rise but support tickets and manual touches rise faster, margin is leaking.

Set rules for approvals, vendor follow-up, and payment changes before pricing up-sells. Higher fees should show up in cash flow and profit, not just in more work for the team. If each premium client adds too many exceptions, the owner will see less take-home income even with stronger billing.

2

AP Processing Efficiency

AP Processing Efficiency

Owner income rises when invoice intake, approvals, coding, payment scheduling, and vendor messages need less manual labor. That matters because payroll is the biggest modeled cost, moving from $605,000 in Year 1 to $193 million in Year 5. More automation can lift margin and free cash for owner pay, but only if it cuts real work, not just re-labels it.

Here’s the quick math: if revenue grows faster than staff can process invoices, overtime and rework eat the gain. Track invoices per staff member, approval cycle time, payment error rate, and support tickets per client. Automation should reduce exceptions, not hide them. Weak workflow design turns growth into delay, vendor friction, and higher labor cost.

Reduce manual AP labor

Set a target for each step: capture, coding, approval, payment, and vendor follow-up. Use the same process for every client segment so staff do not rebuild the workflow each time. If one team member handles too many exceptions, owner pay gets squeezed by payroll before revenue shows up in profit.

Measure what breaks, then fix that step first. A clean dashboard should show exceptions per 100 invoices, cycle time by approval level, and tickets per client. If those numbers worsen as volume rises, add rules, not people. That keeps AP scaling tied to margin, cash flow, and the owner’s draw.

3

Payment And Software Cost Control

Payment and Software Cost Control

If you absorb cloud, API, and payment network fees, they hit gross margin before owner pay. Here, cloud/API costs fall from 45% to 35% of revenue and payment fees from 35% to 27%, while professional software adds $1,400 per month. At $1 million of revenue, a 10-point cloud/API drop saves $100,000; an 8-point fee drop saves $80,000.

The key split is absorbed cost vs pass-through cost. If client-specific payment or platform charges are not billed back, they come out of the owner’s draw. Track revenue mix, fee recovery, and exception volume, because manual rework can wipe out the margin gain from automation.

Measure and recover costs

Build a monthly cost file with revenue, cloud/API spend, network fees, software subscriptions, and pass-through billings. Reconcile absorbed costs to client contracts so you know what hits gross margin and what is recoverable. One clean rule: if the cost is tied to one client, bill it back or cap it.

- Track cost rate by revenue.

- Separate pass-throughs from margin costs.

- Test pricing when fees rise.

- Review subscriptions every month.

If software and network costs drift up even 2 to 3 points, the hit is real at scale, so the owner should watch them as closely as payroll.

4

Exception And Fraud Control Workload

Exception and Fraud Control

This is the cost of stopping bad payments before they hit cash. The modeled control stack is $6,100 per month: $2,200 for cybersecurity and compliance monitoring, $3,000 for legal and regulatory counsel, and $900 for insurance. If duplicate invoices, missing approvals, vendor changes, or payment errors slip through, owner income drops through rework, loss, higher reserves, and weaker vendor trust.

Track exceptions before they hit cash

Measure the volume and cost of each exception type: duplicate invoices, approval gaps, vendor edits, fraud reviews, audit-trail breaks, and payment errors. One clean audit trail ca n save emergency labor later. Compare recovery dollars and hours saved against the $6,100 monthly control spend, then tighten the worst step first so profit and owner draw are not eaten by manual cleanup.

- Invoice count by exception type

- Hours spent per review

- Dollars lost or recovered

- Vendor-change verification time

5

Owner Role And Staffing Structure

Owner Role And Staffing Mix

Owner income depends on what the founder actually does. If the founder sells, manages delivery, and reviews controls, more cash stays in the business but the owner’s pay is tied to operating work. The modeled CEO pay is $165,000 per year, but that is only a benchmark, not a guaranteed distribution.

Adding leaders shifts work off the founder and can raise capacity, yet payroll rises fast. In the model, sales/account managers grow from 10 FTE to 80 FTE, and customer success from 10 FTE to 40 FTE. Scale improves stability, but it also reduces early cash flexibility.

Track founder time before adding headcount

Track three inputs: founder hours on selling, delivery, and control review; revenue per FTE; and payroll as a share of revenue. If the founder still handles daily approvals or vendor issues, owner pay will stay capped because cash goes to labor before it reaches profit.

Set a hiring trigger before adding leaders. Use one test: does the next manager cut enough founder time to protect sales and controls? If not, the extra payroll delays owner income. Hire when the new FTE lifts capacity more than it raises fixed cost.

6

Compare lean, base, and mature owner-income scenarios

Owner income scenarios

Owner income swings hard here because payroll, payment fees, and fixed compliance costs are heavy early on. Mix shift, volume growth, and lower fee rates drive the move from loss to profit.

| Scenario | Low CaseDownside | Base CaseCore | High CaseUpside |

|---|---|---|---|

| Launch model | This low case keeps Year 1 close to the opening model, with $474k revenue and a -116% EBITDA margin. | This base case follows the modeled path to Year 3, where revenue reaches $2.464m and EBITDA margin is about 10.7%. | This high case tracks the mature model, with Year 5 revenue at $5.535m and EBITDA margin near 32.8%. |

| Typical setup | Heavy payroll at $605k, direct variable cost around 80%, and only the modeled $165k owner salary fit while cash stays tight. | Breakeven lands after Month 22, and the mix broadens across Starter, Growth, Pro, and International modules as volume builds. | By then the model is scaled, payback reaches Month 52, and margin improves as transaction fees ease to 2.7% and volume rises. |

| Cost drivers |

|

|

|

| Owner income rangeBefore owner reserves | Modeled salary onlyCash stress | Positive owner drawCore case | Scaled profit poolUpside case |

| Best fit | Use this to stress-test launch month cash needs and the first-year draw limit. | Use this as the main planning case for hiring, pricing, and cash timing. | Use this to test upside staffing, payout capacity, and expansion timing. |

Planning note: Scenario ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distribution results.

Related Products

- Payables Management Service Porter's Five Forces Analysis

- Payables Management Service BCG Matrix

- Payables Management Service Business Model Canvas

- What Are The 5 Core KPIs For Payables Management Service?

- Payables Management Service Business Plan Template in Pre-Written Word

- How Increase Payables Management Service Profits?

- How Increase Payables Management Service Profitability?

- Payables Management Service Startup Costs: $190K CAPEX To Month 22

- Payables Management Service Financial Model Template in Excel

- Launch A Payables Management Service In 6 To 12 Weeks

- How To Write A Business Plan For Payables Management Service?

- Payables Management Service Marketing Mix

- Payables Management Service Marketing Plan

- Payables Management Service Business Proposal

- Payables Management Service PESTEL Analysis

- Payables Management Pitch Deck Example Editable PPTX

- Payables Management Service Business SWOT Analysis

- Payables Management Service Value Proposition Canvas

Frequently Asked Questions

The model uses $165,000 per year as CEO pay, but that is not guaranteed owner cash EBITDA is negative in Year 1 at -$550,000 and Year 2 at -$206,000, then turns positive at $263,000 in Year 3 Distributions should wait until reserves, payroll, and operating needs are funded