Owner income≈$883k

Owner income≈$883kHow Much Can A Peanut Butter Manufacturing Owner Make At 138,000 Units?

Fully Editable

Instant Download

Professional Design

Pre-Built

No Expertise Is Needed

Description

Owner income≈$883k  Net margin-52% to 44%

Net margin-52% to 44% Revenue for target pay≈$1.16M

Revenue for target pay≈$1.16M Business difficultyHard

Business difficultyHard

This page estimates peanut butter manufacturing owner take-home from operating assumptions, not a guaranteed salary or tax plan The researched model grows from 23,000 units and $313,000 in Year 1 revenue to 138,000 units and $2,015,000 in Year 5 revenue, then tests COGS, labor, overhead, debt service, reserves, and reinvestment

Owner income≈$883kNet margin-52% to 44%Revenue for target pay≈$1.16MBusiness difficultyHardWant to test your owner pay?

Owner income calculator

Estimate owner take-home and the target-pay gap from revenue, gross margin, labor, overhead, selling costs, debt, reserves, and target pay.

Planning note: This is a researched planning estimate only. It is not guaranteed salary, tax advice, or owner distribution advice.

Want to check owner income in the model?

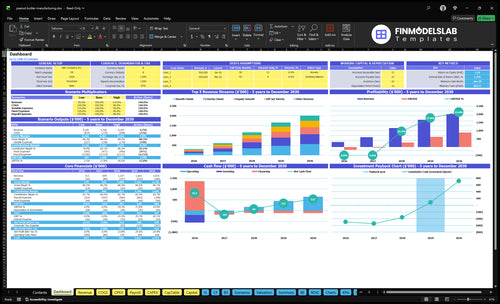

This screenshot shows revenue, margin, costs, reserves, and owner take-home assumptions; open the Peanut Butter Manufacturing Financial Model Template. Charts tie units, margins, fixed costs, and owner cash. Scenario tabs compare Year 1 at $313,000 revenue, Year 3 at $115675M revenue, and Year 5 at $2015M revenue.

Owner-income model highlights

- Owner cash after reserves

- Gross and operating profit

- Units, price, mix inputs

Is private label or branded peanut butter more profitable?

For Peanut Butter Manufacturing, neither channel is always more profitable. Private label can bring volume and repeat orders, but it can pressure price and payment terms; branded retail can support higher shelf pricing, but distributor margins, retailer deductions, broker costs, trade promotions, and slower cash collection can eat into profit. The right move is to model the mix against $1,200 to $4,000 unit pricing, gross margin, working capital, and owner cash before personal tax.

Private Label

- Brings volume fast

- Supports repeat orders

- Pressures price

- Can stretch payment terms

Branded Retail and Online

- Branded retail supports shelf price

- Distributor costs cut margin

- Direct online keeps price control

- Fulfillment and acquisition costs rise

How much does a peanut butter manufacturing owner take home?

A Peanut Butter Manufacturing owner doesn’t take home revenue; take-home starts after costs, debt service, reserves, and reinvestment. In this plan, revenue moves from $313,000 in Year 1 to $2.015M in Year 5, but actual owner pay depends on cash left after production and operating costs, which is why What Is The Current Growth Trajectory Of Peanut Butter Manufacturing? matters before setting salary or distributions.

What comes out first

- Subtract peanuts and ingredients

- Subtract jars, labels, packaging

- Subtract direct labor

- Subtract factory allocations

What owner pay uses

- $1,200 price example

- Less $145 unit production cost

- Less 15% factory allocation

- About $1,037 before overhead

How much revenue does a peanut butter business need to pay the owner?

If you want to pay the owner in Peanut Butter Manufacturing, start with target owner pay plus fixed overhead, debt service, reserves, and reinvestment, then divide by contribution margin after variable and channel costs. That’s a planning formula, not a promise. The model ranges from $313,000 in Year 1 to $2015M in Year 5, so test low, base, and high cases because wholesale pricing, distributor fees, payroll, and working capital can change the revenue need fast.

What drives owner pay

- Owner pay is a target, not a guarantee

- Fixed overhead still has to be covered

- Debt service comes before cash is free

- Reserves protect the business from shocks

What to test

- Run low, base, and high cases

- Check wholesale pricing and distributor fees

- Track jars, cases, and monthly sell-through

- Watch working capital as volume rises

Here’s the quick math: if contribution margin is thin, revenue needs climb fast; if it’s strong, the same owner pay needs less top line. So the real question is not “How much revenue pays the owner?” but “How many jars and cases do we need each month to cover the full cost stack and still pay the owner?”

Want the six biggest income drivers?

1

23K-138KProduction Volume

More units sold spreads factory overhead, and the forecast rises from 23,000 units in Year 1 to 138,000 in Year 5, so owner take-home improves fast when the line stays full.

2

$12-$40Price Mix

A shift toward higher-priced jars and gift sets lifts revenue per unit without adding the same number of units, which raises gross cash for the owner.

3

$1.00-$1.35Input Costs

Classic jars start at $1.00 for raw peanuts and other ingredients, while Organic Smooth reaches $1.35, so supplier swings hit margin right away.

4

$0.45-$1.90Plant Efficiency

Classic jars carry $0.45 for labor, packaging, and labeling, but gift sets climb to $1.90, so waste and downtime cut owner profit quickly.

5

4.5%-3.0%Delivery Costs

Payment processing plus DTC shipping take 4.5% of sales in Year 1 and 3.0% by Year 5, so channel choice directly changes cash left for the owner.

6

617KCash Runway

Minimum cash hits $617K in Month 25, breakeven arrives in Month 26, and payback takes 51 months, so reserves and owner draws decide take-home before taxes and reinvestment.

Peanut Butter Manufacturing Core Six Income Drivers

Production Volume And Capacity Utilization

Production Volume And Capacity Utilization

Capacity utilization = actual output divided by maximum output. As volume grows from 23,000 units in Year 1 to 138,000 units in Year 5, fixed costs like rent, utilities, equipment maintenance, quality control, and management get spread over more jars, so unit cost should fall and margin can improve.

Here’s the catch: income only rises if sell-through keeps pace and pricing holds. With revenue modeled from $313,000 to $2.015 million, more output helps only when sold jars turn into cash fast enough to cover peanuts, packaging, labor, and receivables. Unsold stock traps cash.

Track Sell-Through Before Adding Shifts

Measure units made, units sold, days of inventory, and cash tied up per jar. If output rises faster than sales, the plant may look busy while owner income stays flat. The quick test is whether each added batch lowers cost per sold unit, not just cost per produced unit.

Set production from demand forecasts, not machine time alone. Review sell-through, scrap, and working capital before raising volume. If inventory builds, the owner may need more cash for ingredients and labor, which can delay pay even when reported profit looks better.

1

Channel Mix And Pricing

Channel Mix Sets Take-Home

Channel mix changes owner income because each route carries a different net price after freight, retailer deductions, broker fees, and payment terms. A $1200 classic jar and a $3800 gift set can look strong on paper, but the cash left for the owner can be much lower if wholesale and distributor costs are heavy.

By Year 5, prices move to $1250 and $4000, but higher sticker price does not always raise take-home. Here’s the quick math: price, volume, and cash timing have to work together. If a channel pays late or takes big deductions, profit may show up after the business has already funded peanuts, packaging, and shipping.

Price Each Channel on Net Cash

Track net revenue per unit, not just list price. Build channel models for private label, grocery wholesale, distributor, foodservice, and direct online sales using orders, average order value, freight, deductions, broker fees, and days to cash. That shows which channel actually funds owner pay.

- Compare net price by channel

- Watch payment timing weekly

- Test margin after all fees

- Limit low-cash, high-deduction sales

What this estimate hides: a channel with the best sticker price can still hurt income if it needs deep discounts or slow collections. The owner should rank channels by gross margin, cash conversion, and repeat demand, then push more volume into the mix that pays fastest and keeps the most cash.

2

Peanut And Ingredient Costs

Raw Peanut Cost Per Jar

Peanut and ingredient cost hits gross margin first. In the model, a classic jar uses $0.90 of raw peanuts plus $0.10 of other ingredients, or $1.00 per unit before packaging, labor, and overhead. If peanut prices rise, the owner feels it on every jar, and that lowers the cash left for payroll, debt, and owner pay.

Here’s the quick math: at 23,000 units, a $0.05 peanut cost increase adds $1,150 a year. At 138,000 units, it adds $6,900. Batch yield, shrink, scrap, supplier terms, and formula changes all move cost per saleable jar, so small COGS shifts matter more as volume scales.

Track Cost Per Saleable Jar

Measure peanuts and ingredients by cost per saleable unit, not just by purchase order. Compare planned cost to actual cost each batch, and separate price moves from yield loss. If one batch uses more raw peanuts because of scrap or overfill, that loss goes straight into gross margin and cuts the owner’s draw.

Watch these inputs every month:

- Raw peanuts per jar

- Other ingredients per jar

- Batch yield and scrap

- Supplier terms and price changes

- Formulation changes that raise COGS

3

Packaging, Labor, And Factory Efficiency

Packaging, Labor, and Line Efficiency

Packaging and direct labor hit every jar. With $0.25 packaging, $0.05 labeling, and $0.15 labor per unit, the line starts at $0.45 before peanuts or overhead. Batch setup, cleaning, changeovers, rework, and waste can push that higher, which squeezes gross margin and the cash left for owner pay.

Here’s the quick math: at 100,000 jars, that pack cost is $45,000. If output grows but downtime or scrap rises, the owner makes less per jar even when sales look better. Automation can lower labor per unit, but it also brings equipment debt and maintenance, so it only helps when volume is high enough to cover both.

Cut Cost per Sellable Jar

Track packaging cost per jar, labor minutes per batch, changeover time, rework, and scrap rate. Price and staff from the true cost, not the planned one. If the pack line runs above $0.45 per unit, the owner should fix the process before chasing more volume.

Test one change at a time: tighter batch sizes, faster fill speed, better label control, or training that cuts cleaning time. If a machine lowers labor but adds debt and upkeep, compare the monthly savings to the monthly payment first. Owner income only improves when more jars leave the plant with less waste and the same or lower unit cost.

4

Distribution, Retail Fees, And Marketing Costs

Channel Selling Costs

Distribution fees, freight per case, retailer deductions, broker commissions, trade promotions, chargebacks, and online customer acquisition cost all come out after gross margin. On a $12.00 classic jar or $38.00 gift set, the owner only keeps what’s left after channel costs, not just factory margin. As volume rises from 23,000 to 138,000 units, these costs scale too.

Here’s the quick math: owner income = gross margin - selling costs. If sales grow from $313,000, the wrong channel mix can lift revenue while lowering cash to the owner. A direct online sale needs CAC control; retail needs deduction control. Price each channel on full selling cost, or margin leaks out fast.

Price Each Channel Fully Loaded

Build a channel sheet for each route: unit price, freight, broker fee, promo spend, deductions, and CAC. Keep a separate view for grocery wholesale, distributor, foodservice, and online, then compare net dollars per jar. One clean rule: if you can’t see the full selling cost, you can’t trust the profit.

Track net sales per case, deductions as % of sales, and customer acquisition cost against repeat rate. Test price moves before scaling ads or promotions. If a channel needs heavy trade spend to move product, it may grow revenue but still shrink owner draw. Fix the channel economics first, then push volume.

- Log every deduction by SKU.

- Separate freight from margin.

- Review CAC monthly.

- Price by channel, not by habit.

5

Cash Flow, Debt, Reserves, And Owner Role

Cash Flow, Debt, And Owner Pay

Profit is not the same as cash the owner can take home. In this peanut butter maker, inventory purchases, accounts receivable, equipment loan payments, compliance reserves, and growth stock can all absorb cash even when unit margin looks strong.

For the classic jar, disclosed direct inputs total $1.45 per unit: $0.90 peanuts, $0.10 other ingredients, $0.25 packaging, $0.05 labeling, and $0.15 direct labor. That equals $33,350 at 23,000 units and $200,100 at 138,000 units, before overhead and debt. Owner income depends on how fast that cash comes back from customers.

Track Cash Before Draws

Model owner salary, debt service, reserves, and reinvestment before any distribution. If the owner runs operations, salary is part of the cash model; if management is hired, that payroll cost should reduce what can be drawn. The clean rule is simple: only pay the owner from cash left after fixed obligations.

- Track inventory weeks on hand.

- Track receivable days outstanding.

- Track monthly loan payments.

- Set a cash reserve floor.

- Pay owner last, not first.

What this estimate hides is timing. Fast sales do not help if buyers pay late or stock sits too long. If receivables stretch or growth inventory builds for a new flavor launch, the business can show profit on paper but still need to hold back owner pay to keep the plant funded.

6

Scenario objective: compare lean, base, and high peanut butter manufacturing income cases before personal tax

Owner income scenarios

Income changes fast here because volume rises while fixed payroll and factory overhead stay high. Year 1 can stay cash negative, while Year 3 and Year 5 scale can support real owner draw.

| Scenario | Low CaseStartup ramp | Base CaseScaled factory | High CaseWorking-capital heavy |

|---|---|---|---|

| Launch model | This is the early-scale case where Year 1 volume and cash use keep owner income under pressure. | This is the modeled middle case where Year 3 scale starts to turn production into usable owner income. | This is the stronger scale case where Year 5 output can support the highest modeled owner income. |

| Typical setup | At 23,000 units and $313,000 revenue, Year 1 pricing and mix still sit under a full founder-led payroll, fixed overhead, and launch cash needs. | At 81,500 units and about $1,156,750 revenue, the plant has stronger gross profit, but labor, rent, and inventory still take a real bite out of cash. | At 138,000 units and $2,015,000 revenue, the plant runs at full scale with higher staffing, tighter cash control, and the owner focused on capacity and reserve discipline. |

| Cost drivers |

|

|

|

| Owner income rangeBefore owner reserves | -$162k to -$32kCash burn | $281k to $629kProfit build | $629k to $883kUpside stretch |

| Best fit | Use this to stress-test launch cash when the plant is still at Year 1 scale. | Use this for a steady-growth view where the factory is past launch but not yet fully mature. | Use this to test upside when volume stays strong and working capital does not outrun cash. |

Planning note: Scenario ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions.

Related Products

- Peanut Butter Manufacturing Porter's Five Forces Analysis

- Peanut Butter Manufacturing BCG Matrix

- Peanut Butter Manufacturing Business Model Canvas

- 7 Financial KPIs for Peanut Butter Manufacturing Success

- Peanut Butter Manufacturing Business Plan Template in Pre-Written Word

- 7 Strategies to Boost Peanut Butter Manufacturing Profitability

- Running Costs for Peanut Butter Manufacturing: Monthly Budget Breakdown

- Peanut Butter Manufacturing Startup Costs With $31k Monthly Burn

- Peanut Butter Manufacturing Financial Model Template in Excel

- How to Open a Peanut Butter Manufacturing Business: 23,000 Units

- How to Write a Peanut Butter Manufacturing Business Plan: 7 Steps

- Peanut Butter Manufacturing Marketing Mix

- Peanut Butter Manufacturing Marketing Plan

- Peanut Butter Manufacturing Business Proposal

- Peanut Butter Manufacturing PESTEL Analysis

- Peanut Butter Manufacturing Pitch Deck Example Editable PPTX

- Peanut Butter Manufacturing Business SWOT Analysis

- Peanut Butter Manufacturing Value Proposition Canvas

Frequently Asked Questions

The owner can take home only what remains after all business costs and reserves The researched model shows $313,000 revenue on 23,000 units in Year 1 and $2015M revenue on 138,000 units in Year 5 Classic jars show about $1037 gross profit before operating expenses, but payroll, rent, debt, and reinvestment decide actual pay