Owner income$416k–$6.9M

Owner income$416k–$6.9MPenetration Firestop Owner Income: $416K Year 1 EBITDA

Fully Editable

Instant Download

Professional Design

Pre-Built

No Expertise Is Needed

Description

Owner income$416k–$6.9M  Net margin31%–63%

Net margin31%–63% Revenue for target pay$1.3M

Revenue for target pay$1.3M Business difficultyMedium

Business difficultyMedium

You’re pricing skilled firestop work, not selling a simple labor hour This planning model shows $1335M Year 1 revenue, $416K EBITDA, and growth to $10996M revenue by Year 5 EBITDA means earnings before interest, taxes, depreciation, and amortization owner take-home still depends on reserves, debt, reinvestment, taxes, crew size, bid quality, certifications, and project mix

Owner income$416k–$6.9MNet margin31%–63%Revenue for target pay$1.3MBusiness difficultyMediumWant to test your owner pay?

Owner income calculator

Estimate owner take-home and the target-pay gap from revenue, margin, costs, reserves, and target pay.

Planning note: This is a researched planning estimate, not guaranteed salary, tax advice, or owner distribution advice. Actual owner income depends on collected revenue, margins, payroll, overhead, reserves, and timing of cash receipts.

Want to check owner income in the forecast?

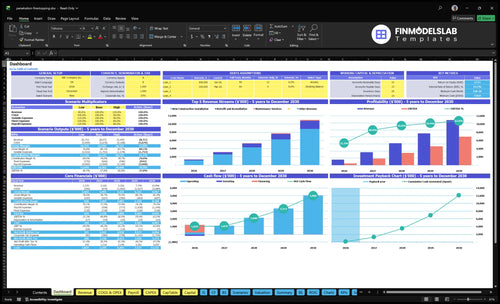

After the core tabs, the Penetration Firestop Installation Financial Model Template shows revenue, margin, costs, reserves, and owner pay. Charts run from $1,335M revenue and $416K EBITDA in Year 1 to $10,996M revenue and $6,922M EBITDA in Year 5. Open the model.

Forecast highlights

- Year 1 to Year 5

- Test pricing and crews

- Owner pay scenarios included

What is the profit margin on firestop installation jobs?

For Penetration Firestop Installation, the margin on a job is not just the sealant bill; it’s driven by labor speed, listed system requirements, access, documentation, inspections, travel, and rework. If you want the profit levers, see How Increase Profitability Of Penetration Firestop Installation? The model’s direct-cost anchors move from 180% to 160% for materials and sealants, 40% to 30% for consumables, 50% to 40% for fuel and vehicle maintenance, and 20% to 12% for disposal, while EBITDA margin rises from 312% in Year 1 to 629% in Year 5.

Margin drivers

- Speed lifts job gross margin

- Access changes labor hours

- Rework cuts profit fast

- System rules add time

Cost leaks

- Fuel and maintenance hit 40%

- Disposal sits at 12%

- Consumables fall to 30%

- Materials and sealants stay high

How much does an owner-operator firestop contractor make?

An owner-operator in Penetration Firestop Installation can earn far more than a technician wage, but only after labor, materials, overhead, insurance, tools, and admin time are paid; for the cost side, see What Are Operating Costs For Penetration Firestop Installation?. In the Year 1 model, 2 technicians support $1.335M revenue and $416K EBITDA, while a certified firestop technician salary anchors at about $62K/year.

Owner upside

- $416K EBITDA before owner-specific cash uses

- About 31% EBITDA margin on revenue

- Profit comes from collected gross profit

- Not from treating wages as profit

Take-home limits

- $62K/year technician wage as baseline

- Reserves reduce owner distributions

- Retainage delays slow cash collection

- Debt, rework, and admin time cut pay

Can a firestop installation business make more with crews?

Yes—Penetration Firestop Installation can make more with crews, but only if management scales with the labor. The crew plan grows certified technicians from 2 FTEs in Year 1 to 9 FTEs in Year 5, while revenue rises from $1.335M to $10.996M. Scale helps owner income potential, but bigger commercial jobs also raise supervision, documentation, retainage, insurance, vehicle, and cash-flow pressure.

Scale upside

- More crews can lift revenue fast

- Year 5 reaches 9 FTEs

- Estimator support speeds bid volume

- General management frees owner time

Scale risks

- Quality control gets harder

- Callbacks can erase margin

- Retainage slows cash in

- Working capital needs rise

What moves owner income most?

1

$1.3M-$11.0MProject Flow

More GC relationships and more signed projects drive the jump from Year 1 revenue to Year 5 revenue and set the ceiling for owner take-home.

2

$95-$130/hrEstimate Pricing

Tighter scope and stronger pricing protect margin on every billed hour, so small quote misses do not wipe out profit.

3

45-60 hrsCrew Output

Higher billable hours per active customer spread fixed labor across more work, which lifts EBITDA without adding the same overhead.

4

24%-29%Direct Margin

Keeping firestop materials, tools, fuel, and disposal in line cuts direct cost and leaves more gross profit for the owner.

5

5 moRework Rate

Passing inspections the first time avoids redo labor and delay costs, which helps the model reach breakeven by Month 5.

6

$719KOverhead Control

Lease, insurance, admin, and retainage pressure cash hard early on, so tight overhead and a clear owner role protect the $719K minimum cash point.

Penetration Firestop Installation Core Six Income Drivers

Project Volume And GC Relationships

GC Pipeline Mix

Project volume is the flow of firestop work from general contractors, mechanical contractors, electrical contractors, and property managers. Steady subcontractor work keeps crews billable and supports owner pay. The source mix assumption moves from 600% new construction in Year 1 toward 400% by Year 5, while retrofit rises from 300% to 400% and maintenance from 100% to 300%.

Here’s the quick math: a broader mix of new construction, retrofit, remediation, and maintenance makes revenue less lumpy and cash flow easier to plan. If one GC slows or a project type pauses, idle labor and fixed overhead hit profit fast. The risk is concentration, because a thin pipeline can delay billing and shrink the owner’s draw.

Track Source Mix

Measure booked hours, backlog weeks, and bid-to-award rate by source. Split pipeline by new construction, retrofit, remediation, and maintenance, plus channel mix across GC, mechanical, electrical, and property management. That shows whether the business is building repeat work or depending on one project type.

- Track repeat GC share monthly

- Watch maintenance share growth

- Flag any one-customer concentration

- Compare backlog to crew capacity

If the mix tilts too hard to one source, forecast gaps show up fast. A steadier share of maintenance and retrofit usually lifts utilization, and that helps collections, scheduling, and the owner’s take-home income.

1

Estimating And Pricing Accuracy

Price the Full Scope

Income here is not just billable hours × rate. A real quote has to cover penetration counts, access difficulty, rated assemblies, documentation, mobilization, inspections, travel, and rework. The model rates rise from $95/hour in new construction in Year 1 to $110/hour in Year 5, from $115/hour to $130/hour in retrofit, and from $105/hour to $120/hour in maintenance.

Underbidding can still create high revenue, but it can shrink owner take-home when labor overruns and failed inspections eat margin. Here’s the quick math: pricing misses do not just cut profit, they also slow collections and tie up crews on low-yield work.

Track Scope Before You Quote

Build each estimate from the job facts, not a flat hourly guess. Track penetration count, access difficulty, rated assembly type, documentation load, travel time, inspection steps, and likely rework. If those inputs are not in the takeoff, the quote is too thin and owner pay gets pushed down.

- Count all penetrations.

- Price hard access separately.

- Include inspection and paperwork time.

- Carry rework in every bid.

Watch jobs where the invoice looks fine but labor hours keep climbing. That is usually the sign that pricing missed scope, so gross margin slips even when top-line revenue looks strong.

2

Crew Utilization And Productivity

Crew Utilization

Utilization means the share of paid crew time spent on billable installs, not waiting, rework, or unplanned travel. The key metric here is billable hours per month per active customer, which rises from 450 in Year 1 to 600 in Year 5. More paid time on approved systems means more revenue from the same crew.

That matters for owner income because productive crews lift capacity, gross profit, and cash flow without adding headcount. A $62K/year technician costs about $5,167/month before overhead, so weak utilization turns payroll into a fixed drag. Strong utilization lets the owner delay hiring and keep more profit available for pay.

Track Billable Hours

Measure billable hours ÷ active customers every month, then split hours by new construction, retrofit, and maintenance, because service-hour assumptions differ by job type. Also track waiting time, travel, inspection delays, and rework. If billable hours move toward 600 per customer, the same payroll produces more revenue.

- Billable hours per active customer

- Paid time on approved installs

- Waiting, travel, and rework

- Hours by job type

- Idle tech days per month

Set hiring off the schedule, not hope. If crews stay under target, owner pay should stay conservative until utilization covers the full labor seat. If onboarding new work takes too long, the crew sits idle and cash flow weakens even when the backlog looks full.

3

Direct Labor And Material Gross Margin

Direct Labor And Material Gross Margin

Gross margin is what’s left after direct labor and job materials. In this model, certified technician payroll grows from 2 FTEs to 9 FTEs at $62K/year, so payroll rises from $124K to $558K a year before burden. If crews spend too much time waiting or reworking, owner pay gets squeezed fast.

The direct cost mix also moves: firestop materials and sealants decline from 180% to 160% of revenue, consumables from 40% to 30%, fuel from 50% to 40%, and disposal from 20% to 12%. Cheaper materials only help if the installed system still passes code and tested-system compliance.

Protect Direct Margin

Build each job from billable hours, penetration count, access difficulty, rated assembly, travel, and rework risk. Here’s the quick math: if labor hours rise but inspections fail, the extra payroll turns into lost gross margin, slower cash, and less money for the owner to draw.

- Track material cost per penetration.

- Log labor hours by assembly type.

- Flag failed inspections and callbacks.

- Price difficult access separately.

- Approve only code-compliant substitutes.

Watch labor hours per installed opening, fuel per trip, and disposal per load each month. If a job looks cheap on material but needs more certified labor or rework, margin drops anyway. Keep the field team on approved products, not bargain parts.

4

Inspection Pass Rate And Rework Control

Inspection Pass Rate

First-pass inspection rate is a profit lever, not just a quality stat. When penetrations fail inspection, the job picks up unpaid labor, site revisits, and paperwork fights, while retainage (the holdback paid at closeout) can sit longer. On hospitals, apartments, offices, retrofits, and multi-trade jobs, more documentation means one miss can stall billing and compress owner draw.

The key inputs are total inspections, first-pass approvals, callback hours, rework hours, and time to final sign-off. The quality stack also carries $650/month in compliance software and system subscriptions, plus a $68K/year safety and compliance officer from Year 2. Higher pass rates lift gross margin and speed cash into the business.

Cut Rework

Track pass rate by project type, not just companywide. A hospital or retrofit usually needs heavier documentation than a simple office job, so split results by building type, GC, and crew. If pass rate slips, fix prep, photo logs, and field checks before the inspection date; that is where margin leaks start.

Price and schedule for quality control work. Rework control should include photo proof, device lists, location tags, and closeout packets, because better records reduce disputes and speed collections. The goal is simple: fewer callbacks, faster billing, better GC relationships, and more durable owner pay.

5

Overhead, Reserves, Retainage, And Owner Role

Owner Pay Minus Cash Drag

Sustainable owner pay is what’s left after $107K/month of fixed overhead, payroll, debt service, and retainage delays. In this business, profit on paper can look fine while cash stays tight, so the owner draw has to wait for collections and project closeout. With $719K minimum cash needed in Month 2, the owner cannot treat bank balance as spendable income.

Marketing also rises from $12K to $35K/year, so the cash plan must cover growth spend and reserve build at the same time. One clean rule: pay the owner last, after operating cash, reserves, and reinvestment are funded.

Protect the Draw with a Cash Floor

Track a 13-week cash forecast, then cap owner pay to the amount above your reserve floor. Include retainage timing, payroll dates, debt payments, and the next round of materials and travel. If a job is billed but not collected, it is not owner income yet.

- Set a minimum cash floor.

- Track retainage by project.

- Delay draws before big pay runs.

- Keep reserves above monthly overhead.

6

Compare low, base, and high owner-income cases

Owner income scenarios

Crew size, billable hours, and mix drive owner income here. The mature case looks strong, but reserves and reinvestment still cut take-home.

| Scenario | Low CaseLow case | Base CaseBase case | High CaseHigh case |

|---|---|---|---|

| Launch model | This is the Year 1 launch case and the tightest owner-income path. | This is the modeled operating case and the main planning anchor. | This is the Year 5 upside case and the strongest owner-income path. |

| Typical setup | Year 1 modeling shows $1.335M revenue, 2 technicians, $416K EBITDA, and a 31.2% EBITDA margin, with breakeven in Month 5. | Year 3 scale reaches $5.326M revenue, 5 technicians, $2.984M EBITDA, and a 56.0% EBITDA margin. | Year 5 reaches $10.996M revenue, 9 technicians, $6.922M EBITDA, and a 63.0% EBITDA margin. |

| Cost drivers |

|

|

|

| Owner income rangeBefore owner reserves | Launch-stage drawLow draw | Scaled owner drawBase draw | Mature owner drawHigh draw |

| Best fit | Use this to stress-test a launch with high cash needs and limited owner draw room. | Use this as the most practical middle path for staffing and owner pay planning. | Use this to test upside, but not as a promised take-home level. |

Planning note: Scenario ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions. Owner take-home starts from EBITDA (earnings before interest, taxes, depreciation, and amortization) and still gets cut by reserves, debt, retainage gaps, capex, and reinvestment.

Related Products

- Penetration Firestop Installation Porter's Five Forces Analysis

- Penetration Firestop Installation BCG Matrix

- Penetration Firestop Installation Business Model Canvas

- What Are The 5 KPIs For Penetration Firestop Installation Business?

- Penetration Firestop Installation Business Plan Template in Pre-Written Word

- How Increase Profitability Of Penetration Firestop Installation?

- What Are Operating Costs For Penetration Firestop Installation?

- Penetration Firestop Installation Startup Costs: $719K Cash Need

- Penetration Firestop Installation Financial Model Template in Excel

- Start a Penetration Firestop Installation Business in 6–14 Weeks

- How Do I Write A Business Plan For Penetration Firestop Installation?

- Penetration Firestop Installation Marketing Mix

- Penetration Firestop Installation Marketing Plan

- Penetration Firestop Installation Business Proposal

- Penetration Firestop Installation PESTEL Analysis

- Penetration Firestop Installation Pitch Deck Example Editable PPTX

- Penetration Firestop Installation Business SWOT Analysis

- Penetration Firestop Installation Value Proposition Canvas

Frequently Asked Questions

The researched model shows $1335M revenue and $416K EBITDA in Year 1, growing to $10996M revenue and $6922M EBITDA by Year 5 That is business profit capacity before interest, taxes, depreciation, and amortization Owner take-home is lower after reserves, debt, retainage delays, equipment, and reinvestment