Owner income$667k

Owner income$667kHow Much Plush Toy Manufacturing Owners Make On $191M Year 1 Sales

Fully Editable

Instant Download

Professional Design

Pre-Built

No Expertise Is Needed

Description

Owner income$667k  Net margin35%–69%

Net margin35%–69% Revenue for target pay$950k

Revenue for target pay$950k Business difficultyHard

Business difficultyHard

You’re trying to turn stuffed toy sales into real owner pay, not just top-line revenue In this US small-business manufacturing model, Year 1 revenue is $191M on 28,000 units, with about $132M left before owner pay, taxes, debt, and reserves based on the visible cost data The scope covers a five-year operating model, not tax advice or a guaranteed salary

Owner income$667kNet margin35%–69%Revenue for target pay$950kBusiness difficultyHardWant to test your own owner pay?

Owner income calculator

Estimate owner take-home and target-pay gap from revenue, margin, costs, reserves, and target pay.

Planning note: Research-based planning estimate only. It is not guaranteed salary, tax advice, or owner distribution advice.

Want to see owner income organized in the model?

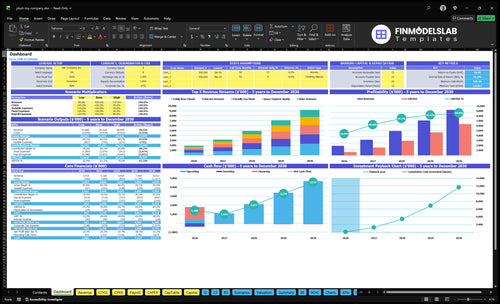

The screenshot ties owner take-home to real operating inputs in the Plush Toy Manufacturing Financial Model Template, with dashboard, sales, pricing, COGS, payroll, overhead, cash flow, and reserves all connected. Open the model.

Owner-income model highlights

- 28,000 to 120,000 units

- $191M to $921M revenue

- Scenario and take-home sensitivity

What is the plush toy manufacturing profit margin?

Plush Toy Manufacturing margin is assumption-driven, not universal; this cost guide, What Is The Estimated Cost To Open And Launch Your Plush Toy Manufacturing Business?, frames the setup spend. In Year 1, the model shows $191M revenue, $2,985k unit COGS, and $900 to $1,350 per-unit COGS across products, with factory allocations adding 25% of revenue. That puts gross profit near $156M, or 81.9%, before selling fees and fixed overhead.

Gross margin drivers

- $191M Year 1 revenue

- $2,985k unit COGS total

- $900 to $1,350 per unit COGS

- 25% factory allocations

Cash drain items

- 35% commissions and payment fees

- Defects cut cash available

- Rework cuts cash available

- Freight, tags, labels, testing matter

How many plush toys do I need to sell to make money?

You need to sell about 3,345 plush toys per year to cover visible fixed overhead before owner pay in Plush Toy Manufacturing; produced units don’t count until they’re sold. Here’s the quick math behind What Is The Most Important Metric To Measure Success For Plush Toy Manufacturing?: at a $68.21 weighted average selling price, $10.66 unit COGS, 25% factory allocation, and 35% sales fees, contribution is about $53.46 per sold unit.

Break-even math

- Sell 3,345 units/year

- Contribution: $53.46/unit

- Fixed overhead: $178.8k/year

- Formula: $178.8k ÷ $53.46

Owner-pay gap

- Add units for owner draw

- Fund inventory before sales

- Cover testing and debt

- Build cash reserves

Can a plush toy business be profitable if the owner works in production?

Yes, Plush Toy Manufacturing can be profitable if the owner works in production, but the profit can look better than it really is because unpaid labor is hiding in the numbers. If you model direct sewing labor at $325 to $450 per unit, the business’s true take-home drops once you pay staff or outsource, but the operation becomes much more scalable.

Hidden labor

- Sewing can hide real cost.

- Packing and QC eat owner time.

- $325 to $450 per unit models labor.

- Take-home can look higher than reality.

What scales

- Paid staff lowers short-term take-home.

- Outsourcing adds cost, but frees capacity.

- Repeat orders make income steadier.

- Systems beat owner dependence every time.

Want the six income drivers at a glance?

1

28K-120KUnit Sales

Going from 28K units in Year 1 to 120K in Year 5 is the biggest revenue swing, and it sets the ceiling for take-home profit.

2

$68-$77Price Mix

A weighted average price near $68 to $77 per unit, plus channel mix, lifts revenue and cushions the 3.5% to 2.5% selling fee drag.

3

$9-$13.5Unit COGS

Unit COGS of about $9.00 to $13.50 drives gross margin, so small savings on fabric, labor, or components flow straight to owner income.

4

2-4 FTELabor Capacity

Manufacturing technician capacity rising from 2.0 to 4.0 FTE decides how fast volume can scale without overtime or rework.

5

$62K/moFixed Overhead

Fixed overhead and compliance costs, including rent, payroll, and testing, can eat the margin fast if the $62K monthly burn runs ahead of sales.

6

$1.03MCash Buffer

Minimum cash of $1.029M in Month 2 shows profit is not the same as cash, so reinvestment and owner draws have to wait until the buffer stays intact.

Plush Toy Manufacturing Core Six Income Drivers

Unit Sales Volume

Unit Sales Volume

Unit sales volume is the main driver of owner income here. The model grows from 28,000 units in Year 1 to 120,000 units in Year 5, and that matters because fixed overhead like rent, utilities, insurance, and software gets spread over more sold units. At 120,000 units, the fixed-overhead load per unit is about 23% of the Year 1 level.

The catch is cash. Revenue assumes produced units are sold, so unsold stock ties up money and can erase owner distributions. Since toy demand can cluster around gift periods, weak sell-through raises inventory risk, slows cash, and leaves sewing and finishing labor underused. More sold units means better operating leverage and less idle labor risk.

Protect Sell-Through

Track sell-through by launch, month, and channel, then compare it with units produced. Here’s the quick math: when sold units rise faster than fixed costs, more gross profit reaches the bottom line and more cash is left for owner pay. When stock builds faster than sales, cash gets trapped and draw capacity falls.

Use a simple control set:

- Match production to gift periods.

- Watch unsold inventory closely.

- Cut runs when demand softens.

That keeps volume high enough to spread overhead without loading the warehouse with stock that does not turn into income.

1

Average Selling Price And Channel Mix

Average Selling Price And Channel Mix

Average selling price is the fastest income lever here because unit costs move slower than price. The model’s weighted average selling price is about $6,821 in Year 1 and $7,677 in Year 5, so mix changes can lift revenue and cash per unit sold without adding the same amount of labor or materials.

Channel mix matters because wholesale can add volume but usually cuts price control, while direct-to-consumer can lift price but adds marketing, payment fees, fulfillment, returns, and customer service. Custom or licensed work can support higher pricing, but it also adds approval, royalty, and compliance work. The owner’s take-home rises when extra price beats those added channel costs.

Track Price by Channel, Not Just Total Sales

Track units sold, average selling price, and gross margin by channel every month. Split sales into wholesale, direct-to-consumer, and custom or licensed work, then compare net contribution after channel-specific costs. That shows which mix actually funds owner pay instead of just inflating top-line revenue.

Test price changes in small steps and watch contribution per unit, not just revenue. If DTC adds price but also raises ad spend, returns, or fulfillment cost, the gain can vanish fast. A better channel mix is the one that lifts contribution per sold unit and leaves enough cash for payroll, inventory, and owner draws.

2

Production Cost Per Unit

Production Cost Per Unit

This driver is the first place profit gets squeezed. Unit COGS runs from $900 to $1,350, with a Year 1 average of about $1,066, so fabric, stuffing, sewing labor, components, packaging, safety tags, and labels set the floor for gross margin.

Factory allocations add another 25% of revenue, and waste, freight-in, or minimum order quantities can cut take-home even when sales rise. Here’s the quick math: at 28,000 units, every $10 saved per unit adds about $280,000 to gross profit, before overhead and owner pay.

Tighten Unit COGS

Protect margin before you chase more units. Track standard cost by SKU, then compare actuals for material use, freight-in, scrap, and rework every month. If a change saves $25 per unit, that is roughly $700,000 a year at 28,000 units.

Build the cost model around real inputs: labor minutes, fabric yield, packaging, safety tags, labels, and order size. Keep these in the forecast so price and cash stay honest, because a move from $1,066 toward $1,350 per unit can erase owner distributions fast.

3

Labor Efficiency And Capacity

Labor Efficiency And Capacity

This driver is the number of sellable plush toys produced per paid hour across cutting, sewing, stuffing, finishing, QC, and rework. When direct sewing labor runs at $325 to $450 per unit, small gains in speed and fewer defects lift margin fast; slower flow does the opposite and cuts the owner’s take-home pay.

Track owner labor separately, or profit will hide unpaid work. Here’s the quick math: more labor hours per unit, plus defects, means fewer good units from the same payroll and slower cash coming back from each batch.

Track Labor Hours By Step

Measure labor hours per sellable unit, defect rate, and rework hours by step. Break the line into cutting, sewing, stuffing, finishing, QC, and fix-ups, then compare actual time to plan. The goal is simple: fewer paid minutes per good unit.

Use that data to staff the line, set batch sizes, and decide when hiring is worth it. If a workflow change cuts rework, contribution improves; if it does not, labor gets absorbed by scrap and owner cash stays tight. Better flow makes growth easier without making payroll painful.

4

Overhead And Compliance Costs

Overhead And Compliance Costs

When sales look strong, owner pay can still stay thin if overhead is heavy. This model shows $149k per month in visible fixed overhead, or $1.788M per year, before any legal and accounting cost. On top of that, factory allocations take 25% of revenue, so cash has to cover a big base before profit reaches the owner.

US toy compliance also adds direct cost. CPSC documentation and testing can keep running, and safety tags run $0.25-$0.50 per unit. So even with solid unit sales, compliance and admin spend can still reduce the cash left for owner draws.

Track overhead per sold unit

Here’s the quick math: owner cash equals gross margin minus fixed overhead, compliance, and admin. Track overhead as a percent of revenue and as dollars per unit sold, then compare it with sell-through and price. If overhead per unit rises while volume stalls, distributions get squeezed fast.

- Watch monthly fixed overhead.

- Track CPSC testing spend.

- Log tags and legal costs.

- Measure overhead per unit.

Use a full launch cost sheet for every product line: production, testing, tags, freight, and admin. If a line cannot carry its share of 25% factory allocations plus fixed overhead, it may grow revenue but still cut the owner’s take-home pay.

5

Cash Reserves And Reinvestment

Cash Reserve Buffer

Accounting profit is not the same as cash you can pay yourself. In plush manufacturing, inventory buys, finished goods, samples, tooling, trade-show spend, testing, and growth stock can trap cash fast. The model shows about $132M in Year 1 before owner pay, taxes, debt, and reserves, but the reserve % is not given, so take-home could be much lower.

Growth from 28,000 to 120,000 units means about 4.3x more working capital, the cash tied up in inventory and production. Stronger reserves cut stockout and cash-crunch risk, but they delay owner pay. One clean rule: if cash is tight, reinvest before you increase your draw.

Measure Working Capital First

Track cash tied up in inventory, samples, tooling , and pre-launch spend before setting owner pay. The key test is simple: can you fund the next production run and still keep a reserve for delays, rejects, and slower sell-through? If not, profit is real on paper but not in the bank.

- Set a reserve target by month.

- Forecast inventory by unit volume.

- Separate owner pay from growth cash.

- Watch stockout and reorder timing.

6

Compare lean, base, and high owner-income planning cases

Owner income scenarios

Owner income swings with volume, pricing, and cost absorption as the model scales from Year 1 to Year 5. The spread still depends on reserves, payroll, taxes, debt, and sell-through.

| Scenario | Low CaseLow case | Base CaseBase case | High CaseHigh case |

|---|---|---|---|

| Launch model | This is the lower earnings path if sell-through slows and fixed costs stay heavy. | This is the modeled path if production, pricing, and demand track the plan. | This is the stronger earnings path if capacity, pricing, and sell-through all hold up. |

| Typical setup | Year 1-style output of 28,000 units and about $1.91M revenue, with owner take-home pressured by fixed overhead, payroll, taxes, and reserves. | Year 3-style output of 68,000 units and about $4.94M revenue, with better fixed-cost absorption and a larger earnings pool before owner pay and reserves. | Year 5-style output of 120,000 units and about $9.21M revenue, with the widest earnings pool before owner pay and reserves. |

| Cost drivers |

|

|

|

| Owner income rangeBefore owner reserves | $667kLow case band | $2.95MBase case band | $6.35MHigh case band |

| Best fit | Fits a cautious launch or slower sell-through market. | Fits the expected operating plan and normal execution. | Fits upside planning and tests strong scale with tight cost control. |

Planning note: Scenario ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions.

Related Products

- Plush Toy Manufacturing Porter's Five Forces Analysis

- Plush Toy Manufacturing BCG Matrix

- Plush Toy Manufacturing Business Model Canvas

- 7 Critical KPIs to Scale Your Plush Toy Manufacturing Business

- Plush Toy Manufacturing Business Plan Template in Pre-Written Word

- 7 Strategies to Increase Plush Toy Manufacturing Profitability

- How Much Does It Cost To Run A Plush Toy Manufacturing Business Monthly?

- Plush Toy Manufacturing Startup Costs for a 28,000-Unit Year 1

- Plush Toy Manufacturing Financial Model Template in Excel

- How To Open A Plush Toy Manufacturing Business In 16–32 Weeks

- How to Write a Business Plan for Plush Toy Manufacturing

- Plush Toy Manufacturing Marketing Mix

- Plush Toy Manufacturing Marketing Plan

- Plush Toy Manufacturing Business Proposal

- Plush Toy Manufacturing PESTEL Analysis

- Plush Toy Manufacturing Pitch Deck Example Editable PPTX

- Plush Toy Manufacturing Business SWOT Analysis

- Plush Toy Manufacturing Value Proposition Canvas

Frequently Asked Questions

The model shows about $132M in Year 1 before owner pay, taxes, debt, and reserves That is not automatic take-home The owner’s actual income depends on inventory cash, testing costs, payroll, reserve policy, and whether the 28,000 produced units are sold