Owner income$25k

Owner income$25kHow Much Can a Pop-Up Bakery Owner Make? $25k to $26M EBITDA

Fully Editable

Instant Download

Professional Design

Pre-Built

No Expertise Is Needed

Description

Owner income$25k  Net margin2.2%

Net margin2.2% Revenue for target pay$1.12M

Revenue for target pay$1.12M Business difficultyHard

Business difficultyHard

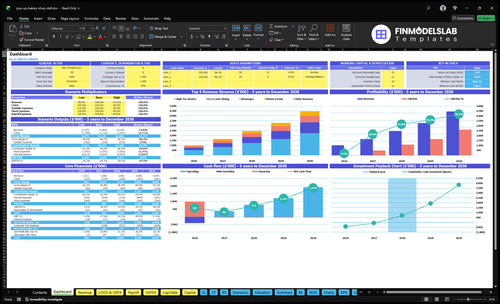

A pop-up bakery owner can make very little in the first year if fixed costs and payroll are heavy, even with strong sales In the researched assumptions, revenue starts at about $112M in Year 1, but EBITDA is only $25k, or about $21k per month before taxes, debt, reserves, and reinvestment By Year 2, EBITDA rises to $492k on $169M revenue, and by Year 5 it reaches $2607M on $455M revenue These are planning assumptions, not salary promises, and owner take-home depends on how much EBITDA is kept in the business

Owner income$25kNet margin2.2%Revenue for target pay$1.12MBusiness difficultyHardWant to test your take-home?

Owner income calculator

Estimate owner take-home and the target-pay gap from revenue, margin, costs, reserves, and target pay.

Planning note: Research-based planning estimate only. It is not guaranteed salary, tax advice, or owner distribution advice.

Want to check owner income in the Pop-Up Bakery model?

This Pop-Up Bakery Financial Model Template screenshot covers revenue, margin, EBITDA, costs, reserves, and owner take-home assumptions—open the model.

Owner-income model highlights

- Breakeven in Month 4

- Payback in 27 months

- Minimum cash $530k

- Year 1, 2, 5

- Owner scenarios, not guarantees

What profit margin can a pop-up bakery expect?

A Pop-Up Bakery can expect about 82.2% contribution before fixed costs and payroll in Year 1, with gross margin after ingredients and packaging at 85.2% and rising to 87.4% by Year 5. If you want launch cost context, see What Is The Estimated Cost To Open, Start, And Launch Your Pop-Up Bakery Business? Here’s the quick math: every 1-point cost move can swing about $112k of Year 1 revenue impact and about $455k by Year 5.

Year 1 margin stack

- Ingredients: 14.0% of sales

- Packaging: 0.8% of sales

- Card fees: 2.0% of sales

- Marketing commissions: 1.0% of sales

What squeezes owner income

- Waste cuts cash fast

- Unsold inventory hurts margins

- Premium ingredients raise COGS

- Booth fees and kitchen rental bite

How much can a pop-up bakery make per event?

A Pop-Up Bakery can make about $1,400 to $5,950 per event before owner pay, based on 20 covers at $70 AOV to 70 covers at $85 AOV; the modeled Year 1 average is about $3,100 per service day. For the main success driver, track sell-through and revenue per slot alongside What Is The Most Important Indicator For Pop-Up Bakery'S Success?.

Revenue range

- Midweek low: $1,400 revenue

- Weekend high: $5,950 revenue

- Average day: about $3,100

- Modeled across 7 service slots

Margin drivers

- Ingredients: 14.0% of sales

- Packaging: 0.8% of sales

- Gross margin: 85.2% before overhead

- Spread depends on traffic, weather, mix

How do you scale a pop-up bakery income?

Scaling a Pop-Up Bakery means pushing more high-quality events, bigger tickets, and repeatable add-ons like preorders, catering boxes, wholesale drops, and multi-location weeks. Here’s the quick math: volume climbs from 270 covers/week in Year 1 to 840 in Year 5, while revenue rises from $1,123M to $4,547M. Payroll also grows from $4,815k to $7,085k, so assistants and systems have to protect speed and quality; EBITDA moves from $25k to $2,607M, but burnout, batch errors, storage limits, service delays, and larger cash reserves can cap the upside.

Growth levers

- Use more high-quality events.

- Raise average tickets with add-ons.

- Sell preorders and catering boxes.

- Expand to multiple weekly locations.

Execution risks

- Watch burnout as volume climbs.

- Prevent batch errors and delays.

- Plan for storage limits early.

- Keep bigger cash reserves ready.

Want to see the main income drivers?

1

270-840/wkEvent Volume

More covers per week turn the same pop-up setup into more sales, so owner cash grows with each busy day.

2

$70-$110Average Ticket

Higher tickets from bundles, drinks, and add-ons lift revenue per guest without needing more foot traffic.

3

$481.5K-$708.5KStaffing Mix

Labor is the biggest cash swing here, so the right headcount mix has a direct effect on owner take-home.

4

85.2%-87.4%Gross Margin

Keeping more of each sales dollar after ingredients and packaging leaves more profit for the owner.

5

$20.9K/moFixed Costs

Rent, utilities, insurance, and admin set the break-even floor, so lower overhead flows straight to cash.

6

14%-12%Waste Control

Less unsold product and spoilage protects ingredient spend, which helps preserve margin on slower weeks.

Pop-Up Bakery Core Six Income Drivers

Event Frequency And Location Quality

Event Volume and Site Quality

Income rises when each of the 7 weekly service slots is placed in a strong site and actually clears cash. The model moves from 270 covers per week in Year 1 to 840 covers per week in Year 5, so the real driver is profitable volume, not just more dates.

High-traffic markets, festivals, corporate pop-ups, and short-term retail placements can lift revenue. Weak locations do the opposite: they add labor, waste, and setup time, but not enough sales. The owner’s take-home improves only when each event covers its direct costs, staffing, and setup burden.

Track Profit per Event

Measure each event by location, day, and covers sold, then compare that to direct cost. Here’s the quick math: event sales - food cost - packaging - event labor - transport - setup. If a site does not beat that test, it should not get repeated.

- Track covers per slot.

- Track labor hours per event.

- Track waste by location.

- Drop weak sites fast.

Use the same scorecard for every format so you can compare a festival, a corporate pop-up, and a retail placement on equal terms. If production capacity falls behind demand, sell-through slips and the extra volume stops helping EBITDA.

1

Average Ticket And Pricing

Average Ticket And Pricing

This driver is the average order value (AOV): what each guest spends on boxes, bundles, seasonal items, drinks, and premium pastries. In Year 1, AOV starts at $70 midweek and $85 on weekends, then rises to $95 and $110 by Year 5. A $1 lift across Year 1 volume adds about $140k in annual revenue before costs.

That revenue only helps owner income if conversion, sell-through, and repeat demand stay solid. Higher prices can improve cash flow and profit, but only when customers still buy enough to cover labor, waste, and setup time. One clean test: if AOV rises but units sold fall, the owner may end up with less take-home income, not more.

Track AOV By Daypart

Measure AOV by weekday, weekend, and event type, then tie it to customer count and repeat purchases. Watch the mix of add-ons, because boxes and bundles usually lift ticket size faster than base items alone. Here’s the quick math: price increases help only when the extra revenue beats any drop in conversion or sell-through.

- Track weekday and weekend AOV.

- Track attach rate on drinks.

- Track bundle and box mix.

- Track repeat demand after price tests.

Test small price moves first. If a higher ticket weakens sell-through or slows repeat orders, the extra margin can vanish fast. Keep the pricing floor tied to local demand and perceived value, then raise premiums where the menu already feels scarce or special.

2

Sell-Through And Waste Control

Sell-Through And Waste Control

Sell-through is the share of baked product sold before it turns into waste. The source does not give a rate, so the model should keep it editable. With 148% of sales tied to ingredients plus packaging in Year 1, waste hits margin and owner take-home fast. If sell-through slips, cash gets trapped in unsold product instead of profit.

The main risk is simple: overbaking in slow markets or bad weather, then scrambling to discount or toss product. On strong weekends, underbaking leaves money on the table. One bad batch can wipe out a day’s profit, especially when setup, labor, and event costs are already sunk.

Batch To Demand, Not Hope

Track sell-through by event type, weather, daypart, and preorder count. Here’s the quick math: if planned output is 100 units and 82 sell before waste, sell-through is 82%. That gives you a clean test for each pop-up slot and helps protect cash flow and profit.

Use a simple control sheet and review it after every event:

- Planned units vs. sold units

- Waste units and markdowns

- Preorders versus walk-ins

- Weather and traffic pattern

If a location or daypart keeps missing target sell-through, cut the batch before you cut owner pay.

3

Product Gross Margin

Product Gross Margin

Product gross margin tells you how much sales stay after ingredients and packaging. In Year 1, the mix is weighted toward high tea service at 500, a la carte dining at 250, beverages at 150, and private events at 100, with private events rising to 200 by Year 4. The source margin after ingredients and packaging improves from 85.2% to 87.4%.

That is before rent, payroll, and reserves, so it is not owner take-home yet. Butter, chocolate, specialty flour, fillings, and packaging can cut this margin fast. Here’s the quick math: when mix shifts toward better-priced items, gross profit rises; when premium inputs or waste rise, cash for owner pay falls.

Track Margin by Item and Event

Measure gross margin by recipe, then by event type. Use actual sell-through, ingredient cost, and packaging cost to see which items earn their place. If a high-tea box or private event uses less premium input per dollar of sales, it can protect margin better than low-ticket a la carte sales.

- Track cost per plated item.

- Review waste after every event.

- Reprice when input costs jump.

Keep a weekly sheet for sales mix, recipe cost, and waste. If butter, chocolate, or specialty flour costs rise, cut low-margin items or raise prices fast so gross margin still supports rent, payroll, and owner draw.

4

Operating Cost Control

Monthly cost hurdle

Fixed and semi-fixed costs set the cash floor before owner pay. The listed lines already total $30,550 a month, led by $15k rent, $12k cleaning, $2k utilities, $800 accounting and legal, and $750 insurance. If these stay high, strong sales can still leave little cash for the owner.

Year 1 payroll adds $40,125 a month, before booth fees, permits, storage, fuel, equipment, and kitchen rental. That puts recurring cost near $70,675 before any event-specific spend. Lower recurring costs reduce breakeven pressure fast, so every trimmed dollar helps owner take-home.

Trim recurring overhead

Track monthly overhead by line item, then test each event against its full cost load. Use a simple forecast with rent, utilities, cleaning, payroll, and site fees so you can see which locations actually clear cash. If a pop-up needs extra labor or a rented kitchen, it has to earn enough gross profit to justify it.

Review booth fees, permits, storage, fuel, equipment, and kitchen rental before you commit. One clean rule helps: if the added cost does not improve cash flow and owner draw, skip it. The goal is not just lower spend; it’s keeping recurring costs low enough that good events turn into real profit.

5

Owner Labor And Staffi ng Model

Owner Labor Mix

Take-home income changes fast based on who does the work. If the owner bakes, sells, manages, or delivers, that labor should be counted as wages or owner compensation, not both. Year 1 roles in the model include a $90k general manager, $80k head chef, $55k sous chef, $50k pastry chef, $120k servers and hosts, $64k support staff, and $225k marketing coordinator.

The key input is role mix versus owner hours. Lower payroll can lift cash flow, but it also raises burnout and service risk if the owner is covering too many shifts. One line tells the truth: if the owner is the labor, the owner is the margin. Scalable income needs trained staff, clear handoffs, and tight quality control so sales do not stall when the owner steps back.

Track Labor by Role

Measure each role separately: cooking, selling, delivery, management, and marketing. Then map those hours to revenue per event, because the business only pays the owner well when labor stays tied to profitable sales, not just busy days. The model should show who fills each job and at what cost, so owner pay is visible and not buried in payroll.

Watch three numbers every month: owner hours worked, staff cost per event, and labor as a share of sales. If the owner is doing GM work, count that cash as compensation once. If staff quality slips, train before cutting deeper. Better staffing beats cheap staffing when repeat sales depend on consistent output.

- Assign one owner role only.

- Cost each shift before booking.

- Track labor cost per event.

6

Compare lean, base, and high owner income scenarios

Owner income scenarios

Weekly covers, ticket size, and mix drive owner income here. Heavy payroll and rent mean the jump from Year 1 to Year 5 changes earnings fast.

| Scenario | Low CaseEarly ramp | Base CaseProven demand | High CaseUpside scale |

|---|---|---|---|

| Launch model | This is the lower earnings path, where the opening year still carries the load. | This is the modeled path, where weekly demand is proven and the concept starts to stabilize. | This is the stronger earnings path, where the concept becomes a fuller multi-channel operation. |

| Typical setup | Year 1 runs at about 270 covers a week, about $1.123M revenue, 85.2% gross margin, $20.85k monthly fixed costs, and about $481.5k payroll. | Year 2 reaches about 370 covers a week, about $1.688M revenue, 85.8% gross margin, annual payroll around $521.5k, and about $492k EBITDA. | Year 5 reaches about 840 covers a week, about $4.547M revenue, 87.4% gross margin, about $708.5k payroll, and about $2.607M EBITDA. |

| Cost drivers |

|

|

|

| Owner income rangeBefore owner reserves | $25k EBITDAYear 1 ramp | $492k EBITDAYear 2 proof | $2.607M EBITDAYear 5 scale |

| Best fit | Use this if you want a conservative opening case and need to test whether early demand can cover overhead. | Use this as the most likely case once the pop-up has repeat traffic and the menu mix is working. | Use this to test the upside if weekend demand holds and private events become a bigger part of sales. |

Planning note: These ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distribution targets. EBITDA is before taxes, debt, reserves, and owner distribution policy.

Related Products

- Pop-Up Bakery Porter's Five Forces Analysis

- Pop-Up Bakery BCG Matrix

- Pop-Up Bakery Business Model Canvas

- 7 Essential KPIs to Scale Your Pop-Up Bakery

- Pop-Up Bakery Business Plan Template in Pre-Written Word

- 7 Strategies to Increase Pop-Up Bakery Profitability and Margins

- Analyzing the Operational Costs of Running a Pop-Up Bakery

- Pop-Up Bakery Startup Costs: Plan For $530K Cash Need

- Pop-Up Bakery Financial Model Template in Excel

- Start A Pop-Up Bakery In 4–10 Weeks With A Compliant Launch Plan

- How to Write a Pop-Up Bakery Business Plan in 7 Steps

- Pop-Up Bakery Marketing Mix

- Pop-Up Bakery Marketing Plan

- Pop-Up Bakery Business Proposal

- Pop-Up Bakery PESTEL Analysis

- Pop-Up Bakery Pitch Deck Example Editable PPTX

- Pop-Up Bakery Business SWOT Analysis

- Pop-Up Bakery Value Proposition Canvas

Frequently Asked Questions

In these researched assumptions, pre-tax owner income capacity starts at $25k of Year 1 EBITDA and rises to $492k in Year 2 By Year 5, EBITDA reaches $2607M on $4547M revenue Actual owner draw can be lower because taxes, reserves, debt payments, and reinvestment come out before spendable cash