Owner income$185k

Owner income$185kHow Much Precedent Transaction Analysis Owners Make: $888k Year 1 Revenue

Fully Editable

Instant Download

Professional Design

Pre-Built

No Expertise Is Needed

Description

Owner income$185k  Net margin-21% to 54%

Net margin-21% to 54% Revenue for target pay$343k

Revenue for target pay$343k Business difficultyHard

Business difficultyHard

Key Takeaways

- Price complex work by scope, not just senior time.

- Signed engagements matter more than raw inquiry volume.

- Analyst leverage grows margins if quality control holds.

- Data and marketing costs must match real pipeline.

Owner income$185kNet margin-21% to 54%Revenue for target pay$343kBusiness difficultyHardWant to test your owner-income case?

Owner income calculator

Estimate owner take-home and the target-pay gap from revenue, margin, costs, reserves, and target pay.

Planning note: Research-based planning estimate only. It is not guaranteed salary, tax advice, or owner distribution advice.

Want to see owner income in the model?

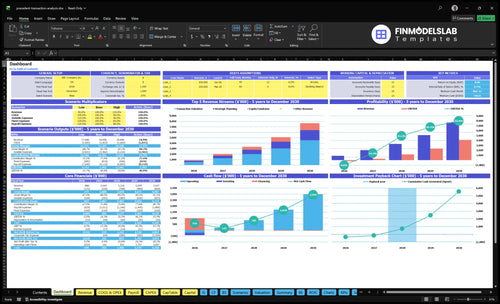

This screenshot shows dashboard, revenue assumptions, pipeline, service mix, costs, reserves, and owner take-home in the Precedent Transaction Analysis Service Financial Model Template; open it next.

Charts should show revenue from $888k to $7.647M, EBITDA from -$190k to $4.125M, breakeven in Month 9, payback in 29 months, and minimum cash of $542k.

Owner-income model highlights

- Dashboard to take-home

- Revenue and EBITDA range

- Runway and payback

How much can a precedent transaction analysis service owner make?

A Precedent Transaction Analysis Service owner can plan around $185k Managing Director pay in the base boutique case, not guaranteed owner profit; see How To Write Business Plan For Precedent Transaction Analysis Service? for the business plan logic. Year 1 shows $888k revenue and -$190k EBITDA, while the scaled case reaches $7.647M revenue and $4.125M EBITDA by Year 5 if staffing and project flow hold.

Owner Pay Range

- Use planning ranges, not guarantees

- Solo case capped by owner hours

- Base boutique pay: $185k

- Year 1 EBITDA: -$190k

Scale Economics

- Year 1 revenue: $888k

- Year 5 revenue: $7.647M

- Year 5 EBITDA: $4.125M

- EBITDA margin: 54%

What are the profit margins for a precedent transaction analysis service?

The Precedent Transaction Analysis Service can post a strong 87% gross margin in Year 1 after delivery costs, but net profit is still tight because referral fees and travel cut contribution margin to 73%. For the operating math behind that, see What Are The 5 Core KPIs For Precedent Transaction Analysis Service? High fees do not mean high take-home if utilization stays low.

Year 1 margin snapshot

- 87% gross margin after delivery costs

- 8% data terminal subscriptions

- 5% research analyst support

- -$190k EBITDA on $888k revenue

What changes the take-home

- 73% contribution margin after fees and travel

- 10% referral fees reduce margin

- 4% travel also cuts margin

- Year 2 reaches about 143%

Margin drivers to watch

- Data tools can swing results fast

- Analyst hours shape delivery cost

- Review time lifts or cuts margin

- Report depth raises client time

Scale effect

- Year 5 margin improves to 539%

- Utilization drives cash more than fees

- Client acquisition cost still matters

- Low volume can erase pricing power

Can a precedent transaction analysis service scale beyond the owner?

Yes — the Precedent Transaction Analysis Service can scale beyond the owner, but only if the owner stops doing analyst delivery and shifts into senior review, sales, and relationship management. Staffing grows from 1 Senior Valuation Analyst and 2 Junior Analysts in Year 1 to 4 Senior Valuation Analysts and 6 Junior Analysts in Year 5, and EBITDA moves from -$190k to $4.125M. The catch is that quality control gets harder as utilization, turnaround time, client trust, and founder bottlenecks all start to matter more.

How it scales

- Owner shifts to senior review.

- Sales starts after Year 1.

- Business development reaches 2 FTEs.

- Year 5 adds 10 total analysts.

Main tradeoffs

- Utilization pressure can rise fast.

- Turnaround time can slip.

- Client trust depends on consistency.

- Founder bottlenecks can block growth.

Want the six income drivers?

1

$15.75KAverage Fee

Raising the Year 1 transaction valuation fee lifts take-home fast because each deal adds to revenue before the 87% gross margin is diluted.

2

$888KProjects Month

More closed projects push Year 1 revenue to $888K and help cover the $13,650 monthly fixed overhead sooner, so pipeline depth drives cash.

3

45hAnalyst Leverage

At 45 valuation hours per engagement, stronger analyst leverage turns the same team into more billable output without matching headcount.

4

32hOwner Utilization

Each active customer averages 32 billable hours in Year 1, so keeping owner time on billable work instead of admin raises take-home.

5

13%Data Costs

Database and research spend sits inside the 13% Year 1 delivery cost block, so lean data buying helps protect the 87% gross margin.

6

$3.5KCAC

A $3,500 Year 1 CAC has to pay back quickly, or it eats the $542K minimum cash buffer before the business is comfortably past month 9 breakeven.

Precedent Transaction Analysis Service Core Six Income Drivers

Average Engagement Fee

Average Engagement Fee

When this service prices by scope, the average engagement fee is the main lever on owner income. In Year 1, transaction valuation work is 45 hours × $350 = $15,750; by Year 5 it rises to 50 hours × $450 = $22,500. That only helps if the fee matches report depth, data cleaning, comp screening, client calls, and turnaround time.

Underpricing custom work cuts profit fast because senior judgment is the expensive part. Strategic planning runs $9,000 to $14,000, and equity fundraise work runs $6,875 to $11,250. If scope creeps but price stays flat, the owner pays for the extra time personally, and take-home income falls even when revenue looks busy.

Price the work, not just the hours

Track fee by deliverable, not just by project. Split each engagement into report depth, data cleaning, comparable screening, client calls, and turnaround time. Here’s the quick math: higher fees lift revenue only if senior hours do not rise faster than the bill. One clean rule: complex deals should never be sold at basic-report pricing.

Use a simple pricing floor before you quote. Compare estimated hours to the expected fee, then test whether the work needs more partner review or custom analysis. If the project needs judgment-heavy modeling or faster delivery, raise the fee or narrow scope. That keeps gross margin intact and protects owner pay instead of turning custom work into unpaid overtime.

1

Projects Per Month

Projects Per Month

Owner income rises when booked engagements turn into completed reports, not when raw inquiries grow. In Year 1, $888k revenue is supported by a $45k marketing budget and $3,500 CAC, which implies about 13 acquired customers. By Year 5, $135k marketing and $2,500 CAC imply about 54 customers.

Here’s the quick math: average billable hours per active customer rise from 32 to 38 per month, so each signed project can carry more revenue. What this hides is timing. A lumpy funnel can leave analysts underused if leads, qualified opportunities, signed engagements, and completed reports do not move together.

Track the funnel, not just inquiries

Measure each stage separately: leads, qualified opportunities, signed engagements, and completed reports. That shows where revenue stalls and where cash gets delayed. If leads rise but signed work does not, the issue is close rate or pricing, not marketing volume.

- Track signed engagements monthly.

- Watch billable hours per client.

- Flag idle analyst weeks early.

Use booked work to forecast staffing and owner pay. More completed reports lift revenue quality; more raw inquiries do not. If pipeline timing slips, cash flow stretches and the founder ends up doing delivery work instead of selling.

2

Analyst Leverage In Valuation Advisory

Analyst Leverage

This driver is how much valuation work junior analysts can absorb before the owner steps in. When juniors gather data and screen comps (comparable transactions), the owner can focus on judgment, review, and client calls, which lifts take-home pay. Year 1 payroll is $295k for 1 Senior Valuation Analyst and 2 Junior Analysts; by Year 5 it reaches $1.01M with 4 seniors and 6 juniors.

The key test is whether added staff reduces owner hours per report, not just whether headcount grows. Research analyst support is 5% of revenue in Year 1 and 3% by Year 5, so leverage only helps if first-pass work is clean and review time stays tight. Otherwise, the extra $715k in payroll turns into more checking, not more profit.

Control Review Quality

Track junior screening pass rate, owner review hours, rework per report, and turnaround time. Here’s the quick math: if juniors handle the data pull and comp screen before the owner reviews, the firm protects margin and frees the owner to sell and price. If rework rises, labor cost is not the main problem; weak quality control is.

Use simple sign-off rules so the owner reviews judgment calls, not spreadsheets. Keep source notes, templates, and checklist steps on every engagement. That helps cash flow because faster delivery means fewer idle hours, less unpaid senior time, and more room for owner pay.

- Junior pass rate

- Owner review hours

- Rework per report

- Turnaround time

3

M&A Transaction Database Costs

Data Access Costs

M&A transaction database costs are a margin lever, not a fixed bill. They cover paid access to comparable-deal data, search tools, and screening support, and they only make sense when project volume, fee level, and quality standards can absorb them.

Here’s the quick math: at $888k Year 1 revenue, data terminal subscriptions at 8% cost about $71k. By Year 5, at $7.647M revenue, 5.5% is about $421k. If the pipeline is not full, enterprise data spend cuts gross margin and pushes out owner pay.

Match Data Spend to Signed Work

Track subscription cost per engagement, not just total spend. The key inputs are active projects, report depth, turnaround time, and the level of comp screening needed for each client. If the firm is doing fewer deals, cap the data stack fast so the cost does not outrun billings.

Use a simple control: compare monthly database spend to booked revenue and completed reports. If cost stays near 8% early on, the business needs enough hours and pricing to support it. One clean rule: do not buy premium access before the pipeline can turn that access into paid work.

- Track cost per completed report.

- Match tier to project volume.

- Review spend before renewals.

- Price for deep custom comps.

4

Client Acquisition Cost For Valuation Advisory

CAC and Referral Mix

This dri ver is the cost to win each signed valuation engagement. With a $45k Year 1 marketing budget and $3,500 CAC, the model supports about 13 customers ($45,000 ÷ $3,500). By Year 5, $135k of marketing at $2,500 CAC supports about 54 customers. That helps owner income only if close rates hold and the work is actually signed.

Referral-heavy growth helps margin because referral fees fall from 10% of revenue in Year 1 to 7% by Year 5. But paid acquisition and long sales cycles tie up cash before billing starts, so distributable profit lags bookings. Don’t count marketing spend as revenue; count only signed engagements and collected fees.

Track Signed Engagements First

Measure the funnel in four steps: leads, qualified opportunities, signed engagements, and completed reports. That shows whether a lower CAC is real or just a busier pipeline. Keep referral source, close rate, and time-to-sign by channel, because a cheap lead that never closes does not lift owner pay.

Test the mix between referrals and paid channels each month. If referral fees stay near 7% to 10% of revenue, more cash stays in the business. If marketing spend rises before contracts are signed, cash flow gets tighter fast. One clean rule: no revenue until the engagement letter is signed.

5

Owner Utilization In Valuation Consulting

Owner Utilization

Owner time is a profit lever, not just a cost. In this model, the Managing Director is paid $185k a year, but the real issue is where those hours go. If the founder stays deep in billable work, sales, hiring, and quality review get squeezed, and that limits how fast average billable hours per active customer can move from 32 to 38 per month as the team grows.

The inputs that matter are owner billable hours, active customers, review load, and pipeline time. Here’s the quick math: more owner delivery can lift current revenue, but it can also slow deal flow and client trust work, which is what protects take-home pay later. The risk is simple: the founder becomes the delivery bottleneck.

Shift the Founder to Higher-Value Work

Track the split between billable and non-billable hours. The goal is to move founder time toward pricing, senior judgment, client calls, and pipeline management, while juniors and analysts handle data gathering and first-pass review. If the owner is still doing too much production, the firm may look busy but pay less after overhead.

Measure these items every month: active customers, owner billable hours, review hours, and signed engagements. If active customers rise but owner review time also rises, that is a warning sign. The clean target is more leverage per client, not more founder labor per report.

- Owner billable hours by week

- Active customers per month

- Review time per engagement

- Pipeline stage by lead source

6

Scenario objective: Compare lean solo, base boutique, and high-leverage owner-income cases

Owner income scenarios

Deal flow, pricing, and staffing change owner income fast in this advisory model. The table shows a lean solo case, the researched middle case, and a scaled team case.

| Scenario | Low CaseLean solo | Base CaseModeled case | High CaseScale-up upside |

|---|---|---|---|

| Launch model | This is the lean solo path, where the owner stays hands-on and project count stays light. | This is the modeled path, with Year 1 revenue of $888k and the current staffing plan. | This is the scaled path, with Year 5 revenue of $7.647M and a larger analyst bench. |

| Typical setup | The firm runs with fewer projects, lower leverage, and mostly owner-led delivery with tight support spending. | The model starts at $888k Year 1 revenue, 87% gross margin after delivery costs, 73% contribution margin after referral fees and travel, -$190k Year 1 EBITDA, Month 9 breakeven, and $542k minimum cash. | The business reaches $7.647M revenue and $4.125M EBITDA in Year 5 with 5.5% data terminal costs, 3% research support, 7% referral fees, and a larger analyst team. |

| Cost drivers |

|

|

|

| Owner income rangeBefore owner reserves | Loss-makingLow income path | -$190k EBITDACore plan | $4.125M EBITDAUpside path |

| Best fit | Use this to stress-test a small book of work and a mostly self-delivered practice. | Use this as the researched middle case for founder, lender, or board planning. | Use this to test a stronger pipeline, better leverage, and higher owner take-home potential. |

Planning note: Scenario ranges are researched planning assumptions only, not guaranteed earnings, salary promises, tax advice, or distributions.

Related Products

- Precedent Transaction Analysis Service Porter's Five Forces Analysis

- Precedent Transaction Analysis Service BCG Matrix

- Precedent Transaction Analysis Service Business Model Canvas

- How Increase Precedent Transaction Analysis Service Profitability?

- Precedent Transaction Analysis Business Plan Template in Pre-Written Word

- How Increase Precedent Transaction Analysis Service Profitability?

- How Increase Precedent Transaction Analysis Service Profitability?

- Cost To Start A Precedent Transaction Analysis Service: $542K Cash Need

- Precedent Transaction Analysis Financial Model Template in Excel

- How To Start A Precedent Transaction Analysis Service In 6 To 12 Weeks

- How To Write Business Plan For Precedent Transaction Analysis Service?

- Precedent Transaction Analysis Service Marketing Mix

- Precedent Transaction Analysis Service Marketing Plan

- Precedent Transaction Analysis Service Business Proposal

- Precedent Transaction Analysis Service PESTEL Analysis

- Precedent Transaction Analysis Service Pitch Deck Example Editable PPTX

- Precedent Transaction Analysis Service Business SWOT Analysis

- Precedent Transaction Analysis Service Value Proposition Canvas

Frequently Asked Questions

The clean planning number is $185k before tax if the owner fills the Managing Director role Extra draw depends on cash after payroll, overhead, reserves, and taxes In the base case, EBITDA is -$190k in Year 1, then $292k in Year 2, so early distributions should stay conservative