Owner income$150k

Owner income$150kHow Much Can a Precision Machining Owner Make on $397M Sales?

Fully Editable

Instant Download

Professional Design

Pre-Built

No Expertise Is Needed

Description

Owner income$150k  Net margin59%

Net margin59% Revenue for target pay$331k

Revenue for target pay$331k Business difficultyHard

Business difficultyHard

You’re weighing owner pay against machine capacity, payroll, and reinvestment needs In the first-year model, the shop shows $397M revenue, 878% gross margin, and a $150,000 CEO / operations manager salary This is an operating estimate, not tax advice or a guaranteed owner distribution

Owner income$150kNet margin59%Revenue for target pay$331kBusiness difficultyHardWant to test your own shop pay?

Owner income calculator

Estimate owner take-home and target-pay gap from revenue, margin, costs, reserves, and target pay.

Planning note: Research-based planning estimate only. It is not guaranteed salary, tax advice, or owner distribution advice.

Want to check owner income in the Precision Machining model?

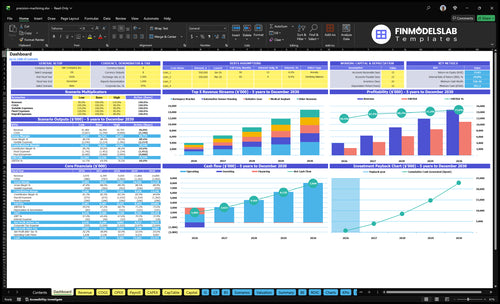

The dashboard in the Precision Machining Financial Model Template shows revenue by part family, owner-income output, unit volume and price assumptions, COGS by job type, fixed expenses, wage line, EBITDA, and scenario charts; open it to test the first-year $397M, Year 3 $906M, and Year 5 $1,480M cases.

Owner-income model highlights

- Owner take-home output

- Revenue by part family

- COGS by job type

- Fixed expenses and wages

- Scenario charts and assumptions

Can an owner-operated machine shop make good money?

Yes—Precision Machining can make good money if the owner’s labor drives profitable throughput, not hidden unpaid work. If the model includes a $150,000 CEO/operations manager salary from month one, that’s about $12,500 per month before payroll taxes, so the shop has to keep machines busy, control scrap, and sell enough high-margin work to cover it.

Works when

- Utilization stays high

- Customer mix supports margin

- Quality control stays tight

- Cash reserves cover slow weeks

Breaks when

- Payroll grows faster than sales

- Systems lag behind capacity

- Debt scale outruns cash

- Owner time hides real costs

How much revenue does a machine shop need to pay the owner?

For Precision Machining, the shop needs about $542,000 per year, or $45,200 per month, to cover first-year fixed overhead and pay the owner $150,000 before taxes, debt, and reserves; this ties directly to What Is The Most Critical Measure Of Success For Precision Machining?. Here’s the quick math: ($290,400 fixed overhead + $150,000 owner salary) / 81.3% contribution margin = ~$542,000.

Target Revenue

- $290,400 first-year fixed overhead

- $150,000 target owner salary

- 81.3% contribution margin

- $45,200 monthly revenue needed

Cash Reality

- Pay comes after product COGS

- Commissions reduce available margin

- Shipping lowers contribution dollars

- Loans and reserves cut take-home

How does machine utilization affect owner income?

Owner income in Precision Machining rises when machine utilization stays high, because fixed costs still hit the P&L when machines sit idle. Here’s the quick math: the model turns 7,300 first-year units into $397M revenue, but if booked spindle hours fall, the shop still carries $290,400 in fixed overhead and a $150,000 owner salary target. For a launch-cost view, see What Is The Estimated Cost To Open And Launch Your Precision Machining Business?

Why utilization pays

- Fixed overhead stays at $290,400

- Owner pay target is $150,000

- Idle machines still cost money

- More spindle hours support pay

What cuts margin fast

- Pricing errors hurt contribution

- Setup time lowers output

- Scrap and rework add waste

- Inspection delays slow cash

Want the six income drivers at a glance?

1

$3.97MBillable Utilization

At 7,300 forecast units, year 1 revenue is about $3.97M, so more billable machine time spreads the $290,400 fixed overhead across more parts.

2

10xPricing and Quoting

The unit price spread runs from $250 to $2,800, so tighter quotes protect take-home by keeping the 87.8% gross margin and the 6.5% selling and shipping load intact.

3

87.8%Job Gross Margin

After direct material, labor, tooling, QC, software, and utilities, gross margin is about 87.8%, so small cost slips still move owner income fast.

4

$498KLabor Productivity

Year 1 wages run about $497.5K, so rework, idle time, and low output hours hit take-home quickly even with the $150K owner salary in the model.

5

$951KEquipment and Debt

The model shows about $1.01M of capex and a $951K cash trough in month 2, but debt and reserve assumptions are not provided, so financing can swing owner income.

6

10xCustomer Mix

Mixing more medical implants and aerospace brackets into the book lifts revenue fast, because those parts sell at $2,500 and $850 versus $250 for a fluid connector.

Precision Machining Core Six Income Drivers

Billable machine utilization

Billable machine utilization

Machines only create owner income when they are booked, running, inspected, and shipped. With fixed overhead at $24,200 per month, idle time hurts cash fast because rent, software, insurance, and maintenance still need to be covered. Track billable spindle hours, setup time, maintenance downtime, and inspection queue time.

Cut idle hours first

Here’s the quick math: $24,200 in monthly fixed overhead is about $807 per day. Every hour that sits in setup, repair, or inspection backlog has to be recovered by the remaining billable hours, so owner pay gets squeezed even if sales stay steady. Less waiting time means more income per machine day.

- Track booked hours by machine.

- Separate run time from setup time.

- Log downtime by cause.

- Watch inspection queue time daily.

1

Pricing and quoting

Pricing and Quoting

Pricing decides owner income before the first part is cut. In precision machining, first-year unit prices run from $250 for fluid connectors to $2,500 for medical implants, so quoting has to capture programming, setup, tolerance risk, material, tooling, inspection, shipping, and commissions.

Here’s the quick math: if a quote misses any of those inputs, revenue can still look fine, but take-home drops because the job margin was thin from day one. The key risk is underquoting high-tolerance work, where rework and extra inspection eat profit fast.

Quote Every Cost

Track quoted price versus actual job cost on every order. Separate material, labor, setup, tooling, inspection, shipping, and sales commission so you can see which part of the quote is leaking margin. A simple rule: if the quote does not cover the full job path, it is not a profitable job.

- Log setup hours by job

- Price tolerance risk separately

- Review win rate by price band

- Compare quoted vs actual margin

The best control is a quote template with required inputs and a final margin check. That keeps revenue quality high and protects cash for owner pay instead of letting sales volume hide weak pricing.

2

Job gross margin

Job gross margin

Job gross margin is revenue minus direct job costs before overhead. In precision machining, that includes raw material, direct machining labor, post-processing, specialized tooling, quality inspection, supplies, tooling wear, software allocation, and job-level utilities. If those costs rise faster than price, the owner’s take-home income drops even when sales look busy.

Here’s the quick math: $486,140 of first-year product COGS against $397M of revenue is about 0.12% of sales. That leaves almost no room for overhead, EBITDA, or owner distributions, so quote accuracy and job mix matter more than top-line volume.

Track cost by job

Measure margin on each order, not just at month-end. Split out material, direct labor, inspection, and tooling wear so you can see which jobs are weak. If a part needs extra setup, rework, or post-processing, the quote should carry that cost before the job starts.

- Compare quote to actual job cost.

- Track scrap and rework fast.

- Price tolerance risk into bids.

- Keep overhead out of gross margin.

When gross margin holds, the shop can cover fixed costs and still leave room for owner pay. When it slips, sales can rise and cash can still tighten because direct job losses hit before overhead and profit draws.

3

Labor productivity

Labor productivity

Employee wages and owner labor need separate tracking. In this model, the $150,000 CEO / operations manager salary is not the same as direct machining labor inside COGS, so labor productivity shows up in how many billable parts each paid hour produces. If setup, programming, rework, or inspection queues rise, direct labor eats margin and cuts the owner’s take-home pay.

Here’s the quick math: more output per paid hour spreads labor cost across more shipped units, so gross profit rises. But overtime and bottlenecked inspection can reverse that fast, because they add cost before overhead gets covered. What this estimate hides is job mix: a simple connector and a tight-tolerance implant do not use the same hours or supervision.

Track paid hours, not just parts

Measure billable spindle hours, setup minutes, rework loops, and inspection queue time by job. Compare direct labor dollars per shipped part against the quote, then check where time slipped: programming, changeovers, or quality holds. If one step keeps running hot, fix that step first, because it protects margin and the owner’s distribution.

Keep a clean split between CEO salary and shop wages in the P&L. If overtime becomes the default to hit schedule, labor productivity is too low or shift coverage is wrong. Right-size staffing so labor supports throughput, not just payroll, and use job standards to forecast whether sales growth will actually raise owner pay.

4

Equipment and financing burden

Equipment cash burden

Equipment adds capacity, but it also pulls cash through $2,000 per month in maintenance contracts, plus repairs, software, tooling, fixtures, and replacement reserves. If loan payments are not modeled, profit can look fine while owner cash falls. Every $1,000 a month of debt service or reserve funding removes $12,000 a year from take-home.

Here’s the quick math: cash improves only when machine revenue covers the full equipment stack, not just the purchase price. Track purchase cost, loan term, maintenance, tooling wear, and downtime together. A machine that boosts capacity but sits idle or needs constant rework can raise revenue and still lower owner pay.

Track cash, not just profit

Use a monthly schedule for each machine: hours run, revenue billed, maintenance, tooling, software, fixture spend, and debt service. For computer numerical control (CNC) machines, compare cash outflow to billable spindle hours so you can see whether the asset pays for itself. If it does not, it is a cash drag, not a growth tool.

Test lease versus buy, stretch replacement timing, and push preventive maintenance before failures. Document which jobs consume the most tooling and fixtures, then quote those costs back into the job. That keeps gross margin real and protects the cash that should reach the owner after reinvestment.

5

Customer mix

Customer Mix

Customer mix decides whether the shop gets steady cash or lumpy cash. A mix with recurring production work in aerospace brackets, medical implants, automotive sensor housings, robotics gears, and fluid connectors can smooth revenue and scheduling. Prototype-heavy work can raise setup and quoting risk, so owner pay gets less predictable.

The key inputs are

Track Mix by Cash and Risk

Track revenue by customer type, then split it into recurring production versus prototype work. Add days to collect cash, rework hours, and quote-to-win rate. Here’s the quick check: if a customer buys often, pays fast, and needs fewer revisions, that mix supports owner draw better than a one-off job with long approvals.

Use a simple dashboard with share of revenue, gross margin by customer, and top-customer concentration. If one account becomes too large or too technical, margins can swing fast. To protect pay, raise prices on high-risk work, push more repeat orders, and avoid mixing slow-paying prototypes with jobs that fund payroll.

6

Compare low, base, and high owner-income cases

Owner income scenarios

Owner income changes fast here because volume, part mix, and machine time drive revenue, while labor, tooling wear, and quality work stay tied to each part.

| Scenario | Low CaseDownside | Base CaseBase | High CaseUpside |

|---|---|---|---|

| Launch model | Year 1 is the low path, with the smallest volume ramp and about $3.97M revenue. | Year 3 is the base path, with higher volume and about $9.059M revenue. | Year 5 is the high path, with the strongest volume ramp and about $14.8M revenue. |

| Typical setup | The shop runs lean in the first year, with 7,300 units, a $150k owner salary, and about $2.361M EBITDA before taxes, debt service, reserves, and distributions. | The model reaches 16,300 units, keeps the owner salary at $150k, and produces about $6.221M EBITDA before taxes, debt service, reserves, and distributions. | The shop reaches 25,400 units, keeps the owner salary at $150k, and produces about $10.893M EBITDA before taxes, debt service, reserves, and distributions. |

| Cost drivers |

|

|

|

| Owner income rangeBefore owner reserves | $2.361M EBITDAFirst-year plan | $6.221M EBITDAYear 3 plan | $10.893M EBITDAYear 5 plan |

| Best fit | Use this to stress-test the launch year if demand ramps slower than planned. | Use this as the most likely operating case once the mix and throughput are steadier. | Use this to test upside if capacity, pricing, and delivery stay on track. |

Planning note: These scenario ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions. They exclude taxes, debt service, reserves, and distributions.

Related Products

- Precision Machining Porter's Five Forces Analysis

- Precision Machining BCG Matrix

- Precision Machining Business Model Canvas

- 7 Critical Financial Metrics for Precision Machining Success

- Precision Machining Business Plan Template in Pre-Written Word

- 7 Strategies to Increase Precision Machining Profitability

- How Much Does It Cost To Run A Precision Machining Business Monthly?

- Precision Machining Startup Costs: $242K/Month Plus Equipment

- Precision Machining Financial Model Template in Excel

- How To Open A Precision Machining Business In 3 To 9 Months

- How to Write a Precision Machining Business Plan in 7 Steps

- Precision Machining Marketing Mix

- Precision Machining Marketing Plan

- Precision Machining Business Proposal

- Precision Machining PESTEL Analysis

- Precision Machining Pitch Deck Example Editable PPTX

- Precision Machining Business SWOT Analysis

- Precision Machining Value Proposition Canvas

Frequently Asked Questions

It can be profitable if utilization and quoting cover fixed overhead early In this model, first-year revenue is $397M, gross margin is 878%, and fixed overhead is $290,400 per year That leaves about $279M EBITDA after the $150,000 owner salary, before taxes, debt, and reserves