Owner income$115k

Owner income$115kPreventive Conservation Services Owner Income: $115k Pay, 22-Month Breakeven

Fully Editable

Instant Download

Professional Design

Pre-Built

No Expertise Is Needed

Description

Owner income$115k  Net margin-33% to 30%

Net margin-33% to 30% Revenue for target pay≈$388k

Revenue for target pay≈$388k Business difficultyHard

Business difficultyHard

Key Takeaways

- Utilization drives revenue, but quality caps capacity.

- Recurring retainers smooth cash, not profit by themselves.

- Tight scope protects margin on higher hourly rates.

- Fixed overhead and payroll make break-even pressure rise.

Owner income$115kNet margin-33% to 30%Revenue for target pay≈$388kBusiness difficultyHardWant to test your owner pay?

Owner income calculator

Estimate owner take-home and the target-pay gap from monthly revenue, margin, payroll, overhead, reserves, and owner pay.

Planning note: This is a researched planning estimate, not guaranteed salary, tax advice, or owner distribution advice. Actual owner income depends on real revenue, margins, payroll, taxes, reserves, and timing.

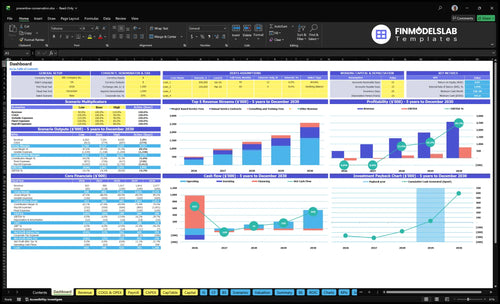

Want to check owner income in the model?

This screenshot shows dashboard logic, income outputs, revenue forecast, staffing, direct costs, overhead, reserves, and owner pay in Preventive Conservation Services Financial Model Template. It’s scenario testing, not a profit promise.

Owner-income model highlights

- Owner take-home is shown

- Revenue: $503k to $2.577M

- EBITDA: -$165k to $766k

- Breakeven Month 22, payback 51

Are preventive conservation services profitable?

Yes, Preventive Conservation Services can be profitable, but not immediately; if you want the launch steps, see How Do I Launch Preventive Conservation Services? The model shows EBITDA margin at -328% in Year 1, -45% in Year 2, then 134% in Year 3, 162% in Year 4, and 297% in Year 5. That means the early years are cash-heavy, and the real test is whether pricing covers specialist labor, travel, supplies, and admin time.

Margin path

- -328% EBITDA in Year 1

- -45% EBITDA in Year 2

- 134% EBITDA in Year 3

- 297% EBITDA in Year 5

Cost pressure

- Watch specialist payroll first

- Track travel and archival supplies

- Include lab testing and insurance

- Separate gross margin from owner take-home

How much can a preventive conservation services owner make?

A Preventive Conservation Services owner can plan for a $115k salary, but early cash should stay inside the business; see What Are The Core 5 KPI Metrics For Preventive Conservation Services Business? for the KPIs that protect that pay. The researched model shows no early distributions, with profit potential after Month 22 as EBITDA reaches $190k Year 3, $294k Year 4, and $766k Year 5 before reserves and distributions.

Owner pay

- Plan salary at $115k

- Skip early distributions

- Protect cash first

- Profit pool after Month 22

Model tradeoffs

- Solo owner limits billable capacity

- Small team raises revenue ceiling

- Payroll: $2875k Year 1

- Payroll: $770k Year 5

How much revenue does a preventive conservation business need to pay the owner?

Owner pay is a planning target, not a payout right. For Preventive Conservation Services, $121k/month of fixed overhead and $2,875k of Year 1 payroll mean revenue has to cover specialist labor before any owner distribution. Even at $503k in Year 1 revenue, EBITDA is still -$165k; Year 2 revenue of $980k is near break-even at -$44k, and full business breakeven arrives in Month 22.

Revenue checkpoints

- $503k still loses $165k EBITDA

- $980k is near break-even

- Month 22 reaches full breakeven

- Specialist labor comes first

Owner pay test

- Test against gross margin

- Test against overhead

- Test against reserves

- Test against $542k minimum cash need

Want the six income drivers?

1

12.5-16hBillable Hours

More billable hours per active customer lifts revenue without adding fixed cost at the same pace.

2

45%-65%Retainer Mix

A bigger share of annual service contracts steadies cash flow and raises repeat work.

3

$185-$310/hrPricing

Higher hourly rates push top-line growth fast because labor is the main sellable input.

4

1-4 FTELabor Model

Smart staffing keeps capacity ahead of demand so the owner can grow income without bottlenecks.

5

29%-22.5%Cost Control

Lower direct costs protect margin, which matters more as project mix and travel load shift.

6

$45K-$85KClient Growth

Higher marketing spend with CAC falling from $2,500 to $2,000 improves the return on each new client.

Preventive Conservation Services Core Six Income Drivers

Billable utilization

Billable Utilization

Billable utilization is the share of owner and staff time that turns into paid assessments, surveys, monitoring reviews, training, and preservation plans. It drives income because admin, proposals, travel, documentation, and report writing drain usable hours. Higher utilization lifts revenue and owner pay without the same jump in fixed overhead, but overbooking can hurt report quality and client trust.

The plan says average billable hours per active customer move from 125/month in Year 1 to 16/month in Year 5, which should be checked because that direction looks inconsistent. Still, the point is clear: more paid hours through the same labor base improve cash flow and profit, until capacity is full and growth needs more staff, not just more sales.

Track Capacity by Person

Measure utilization as billable hours ÷ available hours for each person and each service line. Split out field work, report writing, and travel so you can see where time leaks. If you know which tasks are nonbillable, you can price and schedule around them instead of assuming every booked day turns into revenue.

- Billable hours by staff member

- Travel and documentation hours

- Report rework hours

- Active customer load

- Turnaround time per deliverable

Use a weekly cap on open engagements so quality stays high. With $121k/month of fixed overhead before payroll and marketing, idle hours hurt fast, but pushing too many jobs through can delay cash collection, raise rework, and weaken renewals.

1

Contract size and retainer mix

Retainer Mix

When more work comes from annual retainers, owner pay gets easier to plan. Revenue shifts from 45% annual service contracts in Year 1 to 65% in Year 5, while project fees fall from 35% to 25% and consulting/training rise from 20% to 30%. That mix helps cash flow, but it only lifts profit if labor and travel are priced into the fee.

Price the Repeat Work

Track each contract type separately: annual monitoring reviews, integrated pest management reviews, and annual collection condition assessments should each carry their own labor and travel load. The quick test is simple: if a retainer needs extra site visits or long reports, build that time into the renewal price before you sign.

- Watch margin by contract type

- Track site visits and travel hours

- Invoice renewals before work starts

Use the mix to forecast cash, not just revenue. A steadier book of annual service contracts makes owner draws less choppy, but underpriced field time can still turn a busy month into weak profit.

2

Pricing discipline

Pricing Discipline

Pricing has to cover more than field time. For preventive conservation, the rate needs to pay for site visits, research, risk assessment, documentation, report writing, training materials, travel time, and professional liability exposure. If those inputs are not built in, the owner’s draw gets squeezed even when sales look strong.

Current source prices move from $185-$225/hour for annual contracts, $215-$260/hour for project work, and $250-$310/hour for consulting and training. That spread only helps if scope stays tight; fixed-fee jobs can turn unprofitable fast when field days or reporting hours run long.

Tight Scope, Better Margin

Price from the work plan, not the first phone call. Use three inputs: expected field days, report hours, and travel hours. Then add the risk load for liability and revisions. If the estimate leaves no room for admin time, the project is underpriced.

- Track hours by work type.

- Separate travel from billable labor.

- Cap report revisions in writing.

- Quote fixed fees only with clear scope.

Annual contracts should reward repeat work, but not at the cost of margin. A lower hourly rate can still work if utilization is high and scope is stable; otherwise, owner income drops because every extra unpaid hour comes straight out of gross profit.

3

Labor model

Labor model

The labor model decides whether preventive conservation revenue turns into owner pay. With payroll modeled at $2.875M in Year 1 and $770k in Year 5, the key question is how much work is done by the principal conservation scientist, senior technicians, collections care specialists, business development, and admin support versus the owner. Owner-performed work protects cash, but it also caps capacity.

Protect margin with staffing rules

Track billable hours, review time, and subcontractor margin by role. That shows whether employees are adding leverage or just adding payroll. Subcontractors add flexibility, but if review and rework grow, gross margin drops and owner draw gets squeezed.

- Price for non-billable review.

- Cap admin hours per project.

- Use subcontractors for overflow only.

- Measure utilization by role monthly.

4

Operating cost control

Operating cost control

Operating cost control is a direct income driver because this business carries $121k/month in fixed overhead before payroll and marketing. That means rent, insurance, software, utilities, admin/legal, and other fixed bills must be covered before the owner sees real profit. One clean line: if fixed costs stay high, owner pay gets squeezed fast.

Here’s the quick math: add lab and office rent, vehicle costs, travel, lodging, shipping, archival materials, and testing fees, and cash burn can outrun billings in slow months. The provided cost path also shows direct costs shifting from 29% of revenue in Year 1 to 225% in Year 5, so confirm that assumption before using it. Every fixed commitment raises breakeven pressure.

Track fixed spend before it locks in

Measure overhead by bucket each month: rent, insurance, software, climate control, admin/legal, vehicle, travel, lodging, shipping, archival materials, and testing fees. Then tie each cost to booked work so you can see which bills support revenue and which just add drag on owner income.

- Track fixed burn monthly.

- Test travel against billings.

- Cap unused software seats.

- Review vehicle and lab use.

- Delay nonessential equipment buys.

The launch gear matters too: a $45k vehicle, $25k handheld analyzer, and $12k dataloggers all raise cash needs up front. Keep a simple overhead forecast, and only add fixed costs when recurring contracts cover them. That protects margin and leaves more room for owner draw.

5

Reputation-driven client acquisition

Reputation-driven client acquisition

Reputation-driven client acquisition turns credentials, referrals, museum network relationships, and grant-aligned proposals into lower CAC (customer acquisition cost) and better pricing power. Here, CAC improves from $2,500 in Year 1 t o $2,000 in Year 5, a 20% drop, while marketing spend rises from $45k to $85k. That helps revenue quality, but only if sales keep closing fast enough to cover outreach and staff time.

The cash risk is timing. Institutional sales can move slowly, and grant-funded work can land unevenly, so booked revenue may not turn into cash right away. Better reputation can lift close rates and support premium pricing, but weak follow-up still leaves the owner with more proposal cost and less take-home pay.

Track trust, not just leads

Measure this driver by source, not just total inquiries. Track referrals, museum network intros, grant-aligned proposals, close rate, CAC, and days from proposal to signed contract. If one channel brings cheap leads but slow closes, it can still hurt owner income by delaying cash. The goal is simple: spend more where trust converts faster.

- Track close rate by source.

- Compare CAC to gross margin.

- Forecast grant payment timing.

- Keep reserve cash for gaps.

Use credentials and niche proof to justify higher rates on institutional work, then keep scope tight so the sale stays profitable. If the team spends more on proposal writing and relationship building, the pricing floor has to rise too, or revenue grows while owner pay stays flat.

6

Preventive conservation owner income scenario objective

Owner income scenarios

Owner income here moves with utilization, contract mix, travel, and staffing. Breakeven lands in Month 22, payback takes Month 51, and the cash trough reaches about $542k.

| Scenario | Lean CaseLean case | Base CaseBase case | High CaseHigh case |

|---|---|---|---|

| Launch model | Owner income stays limited because utilization is lighter, project work is heavier, and distributions stay off the table. | Owner income follows the model path, with early losses, Year 3 profit, and cautious draws after reserves. | Owner income lifts faster when retainers rise, billable hours improve, and CAC and travel costs come down. |

| Typical setup | Gross margin stays near 71.0% to 77.5%, but fixed rent, insurance, software, and wages keep cash tight, so owner pay stays salary only. | Gross margin improves as direct costs fall from 29.0% to 22.5%, EBITDA moves from -$165k and -$44k to $190k, $294k, and $766k, and cash still has to carry the $542k trough. | Higher retainer mix, stronger billable hours, and tighter travel control improve cash conversion, so the owner can take more after reserves and overhead are covered. |

| Cost drivers |

|

|

|

| Owner income rangeBefore owner reserves | Salary onlyLean income | Salary plus modest drawBase income | Salary plus larger drawHigh income |

| Best fit | Use this to stress-test a thin pipeline, uneven utilization, and no owner distributions. | Use this as the main plan for a normal pipeline and cautious owner draws after breakeven. | Use this when the contract mix improves and the business keeps the $542k cash cushion intact. |

Planning note: These scenario ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions.

Related Products

- Preventive Conservation Services Porter's Five Forces Analysis

- Preventive Conservation Services BCG Matrix

- Preventive Conservation Services Business Model Canvas

- What Are The Core 5 KPI Metrics For Preventive Conservation Services Business?

- Preventive Conservation Services Business Plan Template in Pre-Written Word

- How Increase Profitability Of Preventive Conservation Services?

- What Are Preventive Conservation Services Operating Costs?

- How Much It Costs To Start Preventive Conservation Services: $542K Cash Need

- Preventive Conservation Services Financial Model Template in Excel

- How To Open Preventive Conservation Services In 3 To 6 Months

- How To Write A Business Plan For Preventive Conservation Services?

- Preventive Conservation Services Marketing Mix

- Preventive Conservation Services Marketing Plan

- Preventive Conservation Services Business Proposal

- Preventive Conservation Services PESTEL Analysis

- Preventive Conservation Services Pitch Deck Example Editable PPTX

- Preventive Conservation Services Business SWOT Analysis

- Preventive Conservation Services Value Proposition Canvas

Frequently Asked Questions

Plan around a large reserve, not just a few slow months The model shows a $542k minimum cash need in Month 26, even though breakeven arrives in Month 22 That gap comes from payroll, fixed overhead, equipment, marketing, and delayed payback Owner distributions should wait until cash coverage is stable