Owner income$763k → $428M

Owner income$763k → $428MHow Much Can A Printing Marketplace Owner Make On $12M GMV?

Fully Editable

Instant Download

Professional Design

Pre-Built

No Expertise Is Needed

Description

Owner income$763k → $428M  Net margin6.4% → 65.8%

Net margin6.4% → 65.8% Revenue target$12M → $650M GMV

Revenue target$12M → $650M GMV Business difficultyHard

Business difficultyHard

You’re estimating owner take-home from an online printing marketplace, not a local print shop These researched planning assumptions cover $12M Year 1 GMV, commission revenue, subscriptions, acquisition spend, COGS, reserves, and owner pay logic over a five-year model They are not guaranteed earnings, tax advice, or salary benchmarks

Owner income$763k → $428MNet margin6.4% → 65.8%Revenue target$12M → $650M GMVBusiness difficultyHardWant to test your owner-income case?

Owner income calculator

Estimate owner take-home and the target-pay gap from revenue, margin, costs, reserves, and target pay.

Planning note: This is a researched planning estimate only, not guaranteed salary, tax advice, or owner distribution advice.

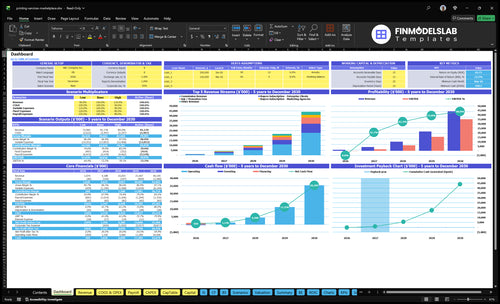

How do you check owner income in the Printing Marketplace model?

This screenshot shows dashboard, GMV build, costs, reserves, and owner take-home in the Printing Marketplace Financial Model Template—open the model.

Owner-income model highlights

- Owner income output shown

- GMV from $12M to $650M

- Acquisition budgets $300k to $35M

What costs change printing marketplace margins the most?

Acquisition spend changes Printing Marketplace margins the most, because buyer and seller marketing reaches $300k in Year 1 and $35M in Year 5. The next biggest drag is payment fees and hosting, modeled at 18% and 25% in Year 1, then 14% and 15% by Year 5; see How Much Does It Cost To Launch Your Printing Marketplace Business? for launch-cost context. Provider production cost only hits the marketplace if the platform guarantees fulfillment or absorbs refunds.

Largest margin drivers

- Acquisition spend scales fastest.

- $300k in Year 1 marketing.

- $35M by Year 5.

- Payment fees and hosting stay material.

Costs to watch closely

- Support and software add fixed load.

- Seller onboarding raises setup cost.

- Dispute handling drives labor and refunds.

- Provider production is not your COGS by default.

How does scaling a printing marketplace change owner income risk?

Printing Marketplace can scale fast, but owner income gets riskier as the business gets bigger. The base case grows from $12M GMV in Year 1 to $650M in Year 5, and that does not mean take-home rises the same way if support, sales, provider management, onboarding, payroll, refunds, or paid ads climb faster.

GMV growth

- $12M Year 1 GMV

- $650M Year 5 GMV

- Buyer mix shifts to agencies

- Seller mix shifts to larger providers

Owner income risk

- Support load rises with scale

- Sales and provider management grow

- Refunds can eat margin fast

- Paid ads can outgrow take-home

Can a printing marketplace make money?

Yes, a Printing Marketplace can make money if repeat orders, take rate, provider reliability, and acquisition cost stay in balance; see What Is The Current Customer Acquisition Rate For Your Printing Marketplace? before scaling spend. In the Year 1 researched case, $1.195M GMV creates $1.111M platform revenue, but only $143k comes from commissions, so subscriptions and seller promotion fees carry the model.

Money Drivers

- $1.195M Year 1 GMV

- $143k commission revenue

- $1.111M total platform revenue

- Subscriptions fill the gap

Profit Risks

- $100 buyer CAC

- $500 seller CAC

- Refunds can erase margin

- Payroll decides owner profit

Want the six income drivers?

1

$12M-$650MGMV Volume

More booked print volume spreads fixed costs and lifts commission, seller fees, and subscription income.

2

12%-10%Take Rate

A 2-point commission slide changes revenue on every order, so take rate matters even when volume is flat.

3

1.5x-3.8xRepeat Orders

Repeat buying raises revenue per customer and cuts how much CAC you need to earn back.

4

$60-$500Acquisition Cost

Buyer CAC falls from $100 to $60, and seller CAC from $500 to $300, so paid growth keeps more margin.

5

$673KPlatform Overhead

About $673K of annual overhead sets the cash burn floor until the model clears month 9.

6

43%-29%Provider Reliability

Cleaner provider performance lowers rework and support cost, which protects margin and repeat demand.

Printing Marketplace Core Six Income Drivers

GMV And Print Order Volume

GMV Drives Commissionable Revenue

The owner’s income starts with GMV (gross merchandise value, the dollar value of print orders sold through the marketplace). It comes from print order count and average order value; in Year 1, the disclosed figure is about $1,195M from 3,460 annual orders, or 288 monthly orders. More orders raise the revenue pool, but GMV is not profit.

By Year 5, volume reaches about 110,417 annual orders, or 9,201 monthly orders, with GMV around $650M. Here’s the quick math: higher volume only helps owner pay if take rate stays solid and acquisition spend, fulfillment quality, and overhead hold. If refunds or support load climb, the bigger top line can still leave less cash.

Track Volume Before It Hides Margin

Measure monthly orders, GMV per order, and net margin after fees. The owner should also track refund rate, chargebacks, and rework, because those costs hit the same GMV pool. One clean rule: if order growth rises but net cash does not, the marketplace is buying volume at the wrong price.

- Orders by buyer type.

- Average order value by category.

- Refunds and support tickets.

- Acquisition cost per order.

- Overhead as a share of revenue.

Use those inputs to forecast owner take-home, not just sales. If 9,201 monthly orders come with weak provider quality, cash flow can tighten fast. Keep vetting, pricing, and escalation rules tight so GMV turns into distributable profit.

1

Take Rate And Monetization

Take Rate And Monetization

Take rate is the commission or service fee kept from each print order. The model assumes a commission/service fee rate of 120% in Year 1 and 100% in Year 5, while commission revenue rises from about $143k to $65M as GMV scales. That cash pays overhead and owner draw only if refund losses and payment fees stay under control.

Inputs are GMV, order count, average order value, and the fee mix. Don’t mix take rate with markup, featured listings, or subscriptions: seller plans, buyer plans, and seller promotion fees are separate revenue lines. If fee yield falls faster than order volume grows, take-home income gets squeezed even when sales look strong.

Track blended monetization

Measure blended take rate as commission, subscriptions, and promo fees divided by GMV. Split it by buyer type, seller type, and order size so you can see where margin is thin. Keep a weekly view of GMV, fee revenue, and refund losses; that shows whether growth is turning into real profit or just more traffic.

- Watch commission per order.

- Separate subscriptions from take rate.

- Track promo fee attach rate.

- Stress test lower-fee scenarios.

If volume rises but blended take rate drops, owner income will lag unless fixed costs stay flat. That matters most once support, software, and acquisition spend start climbing, because the platform needs enough fee density to pay those bills and still leave cash for the owner.

2

Repeat Orders And Retention

Repeat Orders

Repeat orders are the same customer coming back for another print job. For a printing marketplace, that means more flyers, labels, packaging, signage, and promotional materials without restarting acquisition each time. If small-business repeat orders move from 150 to 190, agency orders from 300 to 380, and enterprise from 80 to 120, owner income steadies because each buyer produces more paid jobs and more commissionable volume.

Here’s the quick math: higher retention lifts gross profit per customer and cuts reliance on paid ads. If repeat orders stall, a buyer CAC of $100 or even $60 matters less, because each buyer generates fewer orders and payback slows. The real risk is choppy cash flow and less room to pay the owner from operating profit.

Track Repeat Jobs

Measure repeat order rate, orders per customer, and time between jobs by segment. The key inputs are customer type, average order value, order frequency, and gross margin after support and payment fees. If a buyer keeps ordering but basket size falls, income can still rise; if repeat volume slips, acquisition spend has to do more work just to hold revenue steady.

- Watch orders per account monthly.

- Segment by SMB, agency, enterprise.

- Trigger follow-up after each job.

- Quote the next print need early.

3

Customer Acquisition Cost

Customer Acquisition Cost

For a printing marketplace, customer acquisition cost (CAC) is the cash spent to win each buyer and seller. Here, buyer CAC drops from $100 in Year 1 to $60 in Year 5, while seller CAC falls from $500 to $300. That matters because the business only keeps more owner income when new orders come from cheaper channels and each customer pays back fast enough.

Here’s the quick math: if growth relies only on paid campaigns, rising budgets from $200k to $25M for buyers and $100k to $10M for sellers can crush cash flow. Repeat buyers, organic search, partnerships, and referrals lower CAC and protect profit, while weak retention makes every new order more expensive to earn.

Track CAC by channel

Measure buyer and seller CAC separately, then split it by paid, organic, partner, and referral source. Track inputs like new buyers, new sellers, orders per buyer, repeat order rate, and spend by channel. If repeat orders stall, the drop from $100 to $60 buyer CAC helps less because each buyer generates fewer paid jobs.

- Watch CAC payback by channel.

- Push repeat orders and referrals.

- Cut spend that misses conversion.

- Test seller leads by source.

Owner take-home improves when CAC falls faster than order growth costs. Keep the paid mix tight, because a lower CAC with rising volume still frees cash only if support, sales, and platform costs stay under control.

4

Provider Quality And Fulfillment Reliability

Provider Quality Leak

Provider quality is a direct income driver because bad print jobs cut commission revenue and add refunds, chargebacks, rework, support tickets, and churn. If the marketplace only matches buyer and seller, the printer carries most production risk. If it guarantees delivery, handles disputes, or refunds customers directly, that risk moves onto the owner’s P&L and cash flow.

Track refund rate, chargeback rate, rework cost, and tickets per order by provider type. As the seller mix shifts from 600% small print shops in Year 1 to 550% mid-size commercial providers in Year 5, quality should improve; specialty printers stay at 100% to 150%. One bad order can wipe out the fee on several clean ones.

Control Fulfillment Risk

Set a provider scorecard before scaling volume. Measure on-time delivery, defect rate, refund rate, and response time, then cut off weak vendors fast. If you mediate quality or refund buyers, reserve cash for disputes so owner pay is not funded by borrowed time.

- Review provider scores weekly.

- Flag repeat late shipments.

- Match risky jobs to proven shops.

- Track cost per support ticket.

5

Platform Overhead And Reserves

Platform Overhead and Reserves

Platform overhead is the cash left after payment processing, hosting, core licenses, support, payroll, insurance, admin, and taxes. In this model, payment processing falls from 18% to 14% of revenue and hosting plus core licenses from 25% to 15%, so every $1M of revenue keeps about $40k more and $100k more, before other costs.

That is not all owner take-home. When acquisition budgets rise from $300k to $35M, reserve needs grow too, because support, software, payroll, insurance, admin, reinvestment, financing, and taxes are not fully covered by operating profit. The key number is reserve-adjusted owner income: cash still safe to pay out after those claims.

Track reserve-adjusted pay

Build the model from revenue, payment fees, hosting and licenses, acquisition spend, and fixed overhead. Then hold a reserve for support, payroll, insurance, admin, reinvestment, financing, and taxes before any owner draw.

- Track fee % by month

- Separate profit from cash

- Set a reserve floor first

- Stress test spend at $35M

If fee rates slip back toward 18% or 25%, owner pay gets squeezed fast. A lower-cost stack only helps if reserve rules stop growth spend from eating the payout.

6

Compare lean, base, and high-growth owner-income scenarios

Owner income scenarios

Owner income changes fast here because take rate, repeat orders, CAC, and overhead all scale differently by customer mix. The table shows a cautious path, the modeled path, and a stronger path.

| Scenario | Low CaseDownside | Base CasePlan case | High CaseUpside |

|---|---|---|---|

| Launch model | This is the lower earnings path, with slower conversion and lighter repeat volume. | This is the modeled path built from the researched buyer, seller, and fee assumptions. | This is the stronger earnings path, with better CAC, repeat orders, and mix. |

| Typical setup | Small print shops still dominate, buyer growth is uneven, and higher CAC plus softer repeat orders keep owner income tight. | Year 1 shows about $12M GMV, $11M revenue, and about $763k before payroll, support, admin, reserves, and taxes, then Year 5 reaches about $650M GMV, $476M revenue, and about $428M before those unprovided costs. | Mid-size commercial and enterprise clients rise faster, repeat orders improve, and lean overhead lets owner income run above the base path. |

| Cost drivers |

|

|

|

| Owner income rangeBefore owner reserves | Below Y1 base caseLow income | Y1 $763k; Y5 $428MBase income | Above Y5 base caseHigh income |

| Best fit | Use this to test what happens if CAC stays high and repeat orders lag. | Use this as the planning case for budgeting, staffing, and cash reserves. | Use this to test what happens if the platform wins more repeat, higher-value accounts. |

Planning note: Scenario ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions.

Related Products

- Printing Marketplace Porter's Five Forces Analysis

- Printing Marketplace BCG Matrix

- Printing Marketplace Business Model Canvas

- 7 Critical KPIs for Scaling a Printing Marketplace

- Printing Marketplace Business Plan Template in Pre-Written Word

- 7 Data-Driven Strategies to Increase Printing Marketplace Profitability

- How Much Does It Cost To Run A Printing Marketplace Monthly?

- Printing Marketplace Startup Costs: $8478K Before Platform Build

- Printing Marketplace Financial Model Template in Excel

- How To Open A Printing Marketplace In 10 To 20 Weeks

- How to Write a Printing Marketplace Business Plan in 7 Steps

- Printing Marketplace Marketing Mix

- Printing Marketplace Marketing Plan

- Printing Marketplace Business Proposal

- Printing Marketplace PESTEL Analysis

- Printing Marketplace Pitch Deck Example Editable PPTX

- Printing Marketplace Business SWOT Analysis

- Printing Marketplace Value Proposition Canvas

Frequently Asked Questions

The researched Year 1 case shows $11M platform revenue on $12M GMV After 43% payment and hosting COGS and $300k acquisition budgets, about $763k remains before payroll, support, admin, reserves, taxes, and owner pay Actual owner take-home is the safe amount left after those costs