Owner income$80k

Owner income$80kPrivate Sports Coaching Owner Income: $80K Salary Plan

Fully Editable

Instant Download

Professional Design

Pre-Built

No Expertise Is Needed

Description

Owner income$80k  Net margin76%–81%

Net margin76%–81% Revenue for target pay$168k

Revenue for target pay$168k Business difficultyHard

Business difficultyHard

You’re selling one-on-one and small-group coaching, so owner income is not the same as session revenue This five-year planning view covers $80,000 planned founder salary, revenue, gross margin, operating costs, reserves, and owner take-home before personal taxes

Owner income$80kNet margin76%–81%Revenue for target pay$168kBusiness difficultyHardWant to test your owner pay?

Owner income calculator

Estimate owner take-home and the gap to target pay from revenue, margin, labor, fixed overhead, marketing, reserves, and target pay.

Planning note: Research-based planning estimate only. It is not guaranteed salary, tax advice, or owner distribution advice.

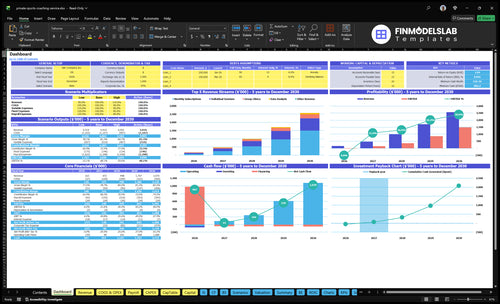

Want to see owner income in the Private Sports Coaching forecast?

This screenshot shows revenue, gross margin, costs, reserves, and owner take-home assumptions—open the Private Sports Coaching Financial Model Template.

Owner-income model highlights

- Owner salary visibility

- 71% to 77% margin

- Low, base, high cases

Can a private sports coaching business scale?

Private Sports Coaching can scale, but solo income is capped by the owner’s coaching hours, admin load, and peak training windows. Here’s the quick math: one assistant coach costs $45,000 a year, or $33,750 at 0.75 FTE in Year 2, then $67,500 at 1.5 FTE in Year 3, and $112,500 at 2.5 FTE in Year 5. Adding an operations manager at $60,000 a year costs $30,000 at 0.5 FTE in Year 2, so scale only helps owner income when coach calendars stay full.

Solo cap

- Owner hours set the ceiling.

- Admin cuts into coaching time.

- Peak windows fill fast.

- Empty slots kill growth.

Hiring tradeoff

- Year 2 assistant: $33,750.

- Year 2 manager: $30,000.

- Year 3 assistant: $67,500.

- Year 5 assistant: $112,500.

How many private coaching sessions to make a living?

For Private Sports Coaching, don’t guess a random session count; start from the owner paycheck and overhead. To pay $80,000 to the owner, cover $29,100 in fixed overhead, and spend $10,000 on marketing, Year 1 needs about $168,000 in revenue at a 71% contribution margin. At $100 per paid coaching hour, that is about 1,677 paid hours a year, or about 32 a week; at $60 it’s about 54 a week, and at $120 it’s about 27.

Year 1 target

- $80,000 owner salary

- $29,100 fixed overhead

- $10,000 marketing budget

- $168,000 revenue goal

Session math

- 71% contribution margin

- 1,677 paid hours per year

- 32 per week at $100

- 54 at $60, 27 at $120

What is the private sports coaching profit margin?

If you’re pricing Private Sports Coaching, the core margin is 71% in Year 1 and 77% by Year 5 before fixed overhead and payroll. That comes from variable costs of 29% dropping to 23%, while fixed overhead stays at $2,425 per month; for startup-cost context, How Much Does It Cost To Open Your Private Sports Coaching Business? is the right next check.

Year 1 margin math

- Contractor fees: 20%

- Analytics software: 25%

- Facility rental: 4%

- Payment processing: 25%

Profit pressure points

- Variable cost total: 29%

- Contribution before fixed costs: 71%

- Year 5 variable cost total: 23%

- Payroll includes $80,000 founder salary

Want the six income drivers?

1

$60-$140/hSession Price

At $60-$140 an hour, each price lift flows through a 71%-77% contribution band and lifts owner take-home fast.

2

2.0-8.0hBillable Hours

More paid hours per client turn the same coach time into more revenue before fixed costs.

3

40%-90%Recurring Mix

Moving work into recurring packages steadies cash and cuts the hunt for new one-off sales.

4

$120-$150CAC

CAC slides from $150 to $120 even as marketing spend grows from $10K to $65K, so growth can scale without crushing returns.

5

16%-20%Coach Leverage

The lead coach's $80K salary and 16%-20% contractor fees set the labor floor, so hiring too early can squeeze margin.

6

$2.4K/moOverhead

The $2,425 monthly overhead base is light, but it still has to be covered before owner draws start to feel real.

Private Sports Coaching Core Six Income Drivers

Paid Session Volume And Utilization

Paid Session Utilization

Owner income rises when more coaching time becomes paid sessions. Track private sessions per week, paid hours, cancellation rate, no-show rate, and calendar utilization so you know how much of the schedule actually pays. In Year 1, break-even is about 32 paid $100 coaching-hour slots per week to cover salary, overhead, and marketing.

Peak demand sits after school, in the evenings, on weekends, and during seasonal training periods. Admin work and travel cut sellable capacity, so empty gaps hurt profit fast. Tighter booking rules and prepaid packages protect take-home by locking in paid hours before the calendar fills with free holds.

Protect Sellable Hours

Use paid hours ÷ available coaching hours as the core utilization check. If utilization is weak, fix the schedule before adding staff or lowering price. What this estimate hides is setup time, travel, and resets between sessions, which can make a full calendar look busy while cash stays thin.

- Track paid sessions by coach.

- Block prime hours for prepaid clients.

- Charge for late cancellations.

- Cluster travel to cut dead time.

1

Average Price Per Coaching Session

Average Price Per Session

Average price per coaching session is the cash you actually collect per booked hour, after mix, discounts, travel gaps, and payment fees. In Year 1, the source rates are $100 for individual sessions, $85 for monthly subscriptions, $60 for group clinics, and $120 for data analysis. Higher prices help owner pay only if demand and fill rate stay strong.

Here’s the quick read: posted price is not realized revenue. If packages or free add-ons pull the hourly rate down, gross margin falls and there is less cash left for overhead and the owner’s draw. Year 5 pricing of $120, $105, $70, and $140 only helps if clients still buy at those levels.

Track Realized Rate, Not List Price

Measure realized revenue per delivered coaching hour by service type, then compare it with booking fill rate and retention. That shows whether a price lift is real or just a weaker calendar. Test each rate against demand before raising it, because a higher sticker price can still lower owner income if sessions sit empty.

- Track cash collected per hour.

- Separate private, group, and analysis fees.

- Flag discounts, refunds, and travel gaps.

2

Private Versus Small-Group Mix

Private vs Small-Group Mix

This driver is the split between one-on-one sessions and small-group clinics. Private coaching starts at $100/hour in Year 1 and reaches $120/hour in Year 5, but one client caps hourly volume. Group clinics are $60/hour in Year 1 and $70/hour in Year 5, so they lift revenue only when attendance stays high. Empty seats cut the hour’s value fast.

The key inputs are booked private hours, clinic fill rate, refunds, skill match, and setup time. A group hour can beat a private hour on revenue per coach hour, but only if the clinic runs full enough to cover prep and any no-shows. If extra admin time rises, owner pay drops even when gross revenue looks stronger.

Track Fill Rate Before Adding More Clinics

Measure each clinic’s attendance, refunds, and setup minutes against its $60 or $70 price. Compare that to private sessions at $100 or $120 per hour, then keep the format that leaves more cash after coach pay and facility rent. If attendance is uneven, fewer but fuller clinics usually protect take-home better than a busy calendar of weak groups.

- Track fill rate by age and skill.

- Stop overmixed clinics.

- Pre-sell spots before staffing.

- Charge deposits to cut refunds.

3

Client Retention And Packages

Retention And Packages

When more athletes stay on monthly subscriptions, the coach sells sessions before delivery, so cash comes in earlier and booked hours are easier to forecast. In this model, subscription mix rises from 40% in Year 1 to 90% in Year 5, while customer acquisition cost falls from $150 to $120, a 20% drop. That lowers marketing dependence and supports steadier owner pay.

Weak renewal rates do the opposite. The owner must replace churn with more paid marketing, and income gets choppy during slow seasons because future sessions are not already sold.

Protect Renewals And Prepay

Track renewal rate, subscription share, and CAC by package type. Test whether longer terms, auto-renew, or prepaid bundles lift repeat sales without hurting fill rate. The goal is simple: more revenue collected ahead of service, less reliance on ad spend, and cleaner cash flow for owner draw.

- Measure renewals every month.

- Forecast sessions sold ahead.

- Compare CAC by offer.

- Document package terms clearly.

4

Owner Coaching Versus Hired Coach Leverage

Owner Coach Leverage

Hiring coaches can raise capacity, but it does not automatically raise owner pay. In Year 1, contractor fees run 20% of revenue, then ease to 16% by Year 5. If the schedule is thin, those fees and wages still hit cash, while empty sessions do not. The quick math is simple: more staff only helps when booked hours rise faster than labor.

Assistant coach payroll starts after launch and reaches 25 FTE at $45,000 per FTE by Year 5, or $1,125,000 a year in salary alone. The hidden drag is owner time: quality control and scheduling shift onto the owner, so underused coaches can lower take-home income even when revenue looks bigger. One line says it all: unused capacity is expensive.

Hire Against Filled Hours

Track paid sessions per coach, utilization, cancellations, and no-shows before adding headcount. Compare each coach’s booked hours with labor cost and the owner’s time spent on quality control. If a new hire does not keep sessions filled, payroll becomes a fixed drain instead of profit leverage.

- Watch booked hours weekly.

- Measure no-shows and cancellations.

- Price for coach coverage.

- Delay hires until fill rate holds.

Use staffing only where demand already exists. That keeps coach payroll tied to revenue, protects gross margin, and leaves more cash for owner draw.

5

Operating Costs And Reserves

Operating Costs And Reserves

Private sports coaching pays the owner only after overhead is covered. Fixed costs are $2,425 per month for admin rent, insurance, scheduling software, hosting, utilities, and legal or accounting. Add $10,000 in Year 1 marketing, or about $833 per month, and the cash loa d starts near $3,258 per month before facility rental, payment fees, contractor fees, and usage-based analytics.

Reserve cash comes first. Weather, school breaks, injuries, and seasonality can cut sessions fast, so distributions should wait until the business can still pay fixed bills during a slow month. As marketing rises to $65,000 by Year 5, the owner needs tighter cash planning, or profit on paper can turn into weak take-home cash.

Build a reserve before you pay yourself

Track fixed overhead, marketing cash, and variable session costs each month. Then compare those costs to booked sessions, because a full calendar in August does not protect January cash. Set a reserve equal to at least one slow month of overhead plus planned marketing, so distributions only happen after that floor is funded.

- Watch monthly cash burn.

- Separate reserve from draw.

- Stress test weather cancellations.

- Track contractor and facility costs.

If usage-based analytics or contractor fees rise with volume, margin can still look fine while cash gets tight. Use prepayments, packages, or deposit timing to smooth receipts, and review reserve targets before the school year, winter, and summer break. That keeps owner pay tied to actual cash, not just booked revenue.

6

Compare low, base, and high owner-income cases

Owner income scenarios

Income moves with session mix, retention, staffing, and overhead. The same coaching business can sit below founder pay, cover salary, or produce surplus only after reinvestment.

| Scenario | Low CaseSolo model | Base CaseStaffed model | High CaseHigh-retention model |

|---|---|---|---|

| Launch model | Owner income stays below the planned salary because the business runs under the roughly $14,000 monthly break-even level. | Owner income is modeled to support the $80,000 founder salary once the core mix is running at Year 1 pricing and cost levels. | Owner income rises above salary once retention, staffing, and pricing scale enough to fund reserves and reinvestment. |

| Typical setup | A solo founder handles most sessions, keeps volume light, and does not clear the founder salary after 29% variable costs, $2,425 monthly overhead, and $10,000 marketing. | The base case assumes Year 1 revenue can cover 29% variable costs, $2,425 monthly overhead, and $10,000 marketing while the founder stays the main coach. | A staffed model adds an operations manager, assistant coach, and marketing coordinator while subscriptions and group work carry more of the mix and variable unit costs ease. |

| Cost drivers |

|

|

|

| Owner income rangeBefore owner reserves | Below $80,000Below salary | $80,000Salary funded | $80,000+Salary plus draw |

| Best fit | Use this to stress test a lean solo launch that may not cover owner pay. | Use this as the core planning case for a founder-led shop that reaches salary coverage. | Use this to test a larger, retention-led setup with distributions after reinvestment. |

Planning note: These ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions.

Related Products

- Private Sports Coaching Porter's Five Forces Analysis

- Private Sports Coaching BCG Matrix

- Private Sports Coaching Business Model Canvas

- 7 Critical Metrics to Track for Private Sports Coaching

- Private Sports Coaching Business Plan Template in Pre-Written Word

- 7 Financial Strategies to Increase Private Sports Coaching Profitability

- Running Costs for Private Sports Coaching: How to Budget Monthly

- Private Sports Coaching Startup Costs: $38K CAPEX Plan

- Private Sports Coaching Financial Model Template in Excel

- How To Open A Private Sports Coaching Business In 4 To 8 Weeks

- How to Write a Private Sports Coaching Business Plan in 7 Steps

- Private Sports Coaching Marketing Mix

- Private Sports Coaching Marketing Plan

- Private Sports Coaching Business Proposal

- Private Sports Coaching PESTEL Analysis

- Private Sports Coaching Pitch Deck Example Editable PPTX

- Private Sports Coaching Business SWOT Analysis

- Private Sports Coaching Value Proposition Canvas

Frequently Asked Questions

The model plans an $80,000 founder salary before personal taxes That is not the same as profit or distributions To support it in Year 1, the business needs about $168,000 in annual revenue, based on a 71% contribution margin, $29,100 fixed overhead, and $10,000 marketing