Owner income$134k–$2.0M

Owner income$134k–$2.0MHow Much Does A Professional Coach Owner Make? $134k Year 1 Plan

Fully Editable

Instant Download

Professional Design

Pre-Built

No Expertise Is Needed

Description

Owner income$134k–$2.0M  Net margin5%–61%

Net margin5%–61% Revenue for target pay$3.0M

Revenue for target pay$3.0M Business difficultyHard

Business difficultyHard

You’re planning owner pay before the coaching business has stable demand, so separate revenue, profit, cash reserves, and taxes from day one This five-year US model covers solo and small-team coaching across 1:1 coaching, retainers, group work, and subscriptions, with $316k Year 1 revenue and $134k owner income before tax and reserves It is not tax advice, and it does not treat revenue as owner pay

Owner income$134k–$2.0MNet margin5%–61%Revenue for target pay$3.0MBusiness difficultyHardWant to test your coaching take-home?

Owner income calculator

Estimate owner take-home and the target-pay gap from revenue, margin, costs, reserves, and target pay.

Planning note: This output is a researched planning estimate, not guaranteed salary, tax advice, or owner distribution advice. Actual owner income depends on revenue, margins, payroll, taxes, debt, and reinvestment.

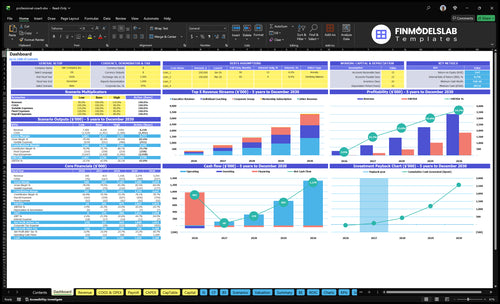

How do you check owner income in the Professional Coach model?

This dashboard shows revenue, EBITDA, owner pay, cash, breakeven, and payback; open the Professional Coach Financial Model Template.

Owner-income model highlights

- $316k to $314M revenue

- $14k to $184M EBITDA

- $134k to $196M owner income

- Tests CAC, pricing, utilization

- Also staffing, reserves, reinvestment

What expenses reduce professional coach income?

Professional Coach income gets squeezed by both fixed overhead and delivery costs, and the fastest way to see it is to map every dollar against billable time. For a full cost build, see How Much Does It Cost To Open And Launch Your Professional Coach Business?; the listed monthly fixed costs are $2,500 rent, $300 CRM, $150 website, $500 professional development, $150 insurance, and $400 accounting and legal, which totals $48,000 a year. Variable and delivery costs also cut margin: 18% coach compensation, 4% assessment tools, 3% video platform fees, and 2% onboarding materials, while marketing adds $25,000 in Year 1 and $110,000 by Year 5, with payroll the biggest scaling cost.

Fixed overhead

- $2,500 monthly office rent

- $300 CRM software

- $150 website cost

- $500 professional development

Variable and scaling costs

- 18% coach compensation

- 4% assessment tools

- 3% video platform fees

- $25,000 Year 1 marketing

How many clients does a coach need?

A Professional Coach does not need one fixed client count; it depends on price, hours, retention, and delivery capacity. With Year 1 billing at $600 per individual client, $2,400 per executive retainer, $3,000 per corporate group, and $200 per mentorship subscription, the client mix sets the math. Before variable costs, revenue has to cover the $2166k Year 1 fixed, payroll, and marketing base.

Revenue by offer

- $600 individual client

- $2,400 executive retainer

- $3,000 corporate group

- $200 mentorship subscription

What lowers client count

- Retainers reduce volume needed

- Groups raise sales complexity

- Hours cap delivery capacity

- Retention lifts total revenue

How do you scale coaching income?

Professional Coach scales past 1:1 by shifting into executive retainers, corporate groups, mentorship subscriptions, workshops, and packages. In year 1, the hourly rates are $150 individual, $300 executive, $250 corporate, and $100 mentorship, and the mix moves toward more executive and corporate work as EBITDA rises from $14k to $184M. The catch is simple: payroll grows from $140k to $580k, so hiring ahead of demand can hurt cash fast.

Where growth comes from

- Sell executive retainers at $300/hour

- Add corporate groups at $250/hour

- Use mentorship subscriptions at $100/hour

- Bundle workshops with coaching packages

Main risk to watch

- Do not hire before demand is real

- Watch payroll move from $140k to $580k

- Keep the higher-rate mix growing

- Protect cash while scaling delivery

Want the six coaching income drivers?

1

$100-$340/hrPricing

Year 1 rates run from $100 for mentorship to $300 for executive retainer, and the top rate reaches $340 by Year 5, so pricing changes owner take-home fast.

2

2-12hCapacity

Billable hours sit at 4, 8, 12, and 2 by offer, so every extra booked hour pushes revenue up before headcount fully catches up.

3

60/20/10/5Offer Mix

The mix starts with 60% individual coaching in Year 1 and shifts toward more retainer, group, and subscription work, which lifts average revenue per hour.

4

22mRetention

Repeat clients and referrals reduce how often you need to buy the same sale again, which helps when payback is 22 months.

5

$500-$350Acquisition Cost

CAC falls from $500 in Year 1 to $350 in Year 5, so each new client costs less even as the marketing budget rises from $25,000 to $110,000.

6

44%-584%Cost Control

Office rent, wages, and support costs decide how much EBITDA reaches the owner, and the model's margin expands from 44% to 584%.

Professional Coach Core Six Income Drivers

Pricing And Positioning

Pricing And Positioning

Pricing and positioning decide how much income each client brings in before you add more hours. In Year 1, the spread is wide: $100 mentorship versus $300 executive retainer work per hour. That matters because 8 executive hours create $2,400 per client period, while 4 hours of individual coaching brings about $600. Clear outcomes support higher take-home pay.

The risk is simple: if the niche is vague, proof is thin, or price moves ahead of trust, conversion slips and cash flow gets uneven. One clean line: sell the result, not the clock. Better positioning can lift revenue without adding sessions, which protects margin and leaves more room for owner pay.

Price to the outcome

Track client type, hours sold, price per hour, and revenue per client period. Those four inputs show whether the offer is priced for mentorship, individual coaching, or executive retainer work. If the executive offer earns 4x the revenue of lower-priced coaching for the same calendar block, the niche and proof are doing real work.

Test one clear promise, one buyer group, and one proof point at a time. Use testimonials, case notes, and before-and-after results to support a higher rate, then raise price only when close rates stay steady. If price rises faster than trust, sales slow and owner income drops even when demand looks strong.

1

Client Load And Utilization

Paid Utilization

Paid utilization is the share of available work time that becomes billable coaching. In this model, delivery blocks are 4 hours for individual coaching, 8 hours for executive work, 12 hours for corporate group sessions, and 2 hours for mentorship. More billable hours lift revenue, but only if sales, prep, admin, and follow-up still get done.

Here’s the quick math: if a coach has 40 available hours and fills 24 hours with paid sessions, paid utilization is 60%. That can raise owner income fast, but if every open hour turns client-facing, quality can slip and renewals can weaken. The real limit is sustainable capacity, not just schedule fill.

Track Billable Hours, Not Just Bookings

Measure utilization by service line and by week: billable hours, prep time, admin time, and follow-up time. Track the mix of 4-hour, 8-hour, 12-hour, and 2-hour blocks, because the mix changes revenue per hour and the load on the owner. One full calendar does not always mean one healthy calendar.

Set a cap before hiring. If coaching hours crowd out sales or follow-up, new demand can raise stress instead of take-home pay. Use a simple rule: protect non-billable time first, then fill the rest with paid sessions. That keeps cash flow steadier and helps the business grow without burning out the owner.

- Billable hours by offer type

- Non-billable time by task

- Weekly utilization percentage

- No-show and reschedule rate

- Owner capacity before hiring

2

Offer Mix And Revenue Model

Offer Mix

Packages, retainers, group programs, workshops, and subscriptions change what one client is worth. In Year 1, client-period revenue is $600 for individual coaching, $2,400 for executive coaching, $3,000 for corporate group work, and $200 for mentorship. Higher-end corporate and executive work can raise revenue per relationship, but they usually bring longer sales cycles and more prep, so cash can come in slower.

That mix matters for owner pay because margin is shaped by more than the sticker price. Mentorship can add recurring revenue, but at $200 it needs volume to move the needle. If the book skews too far toward low-price offers, the owner may stay busy without building enough profit for a steady draw.

Track Revenue Per Relationship

Measure revenue by offer, not just by total clients. The key inputs are client count, offer type, price per client-period, prep time, and renewal rate. Here’s the quick check: if a higher-priced offer takes much more setup and sales time, the extra revenue may not improve take-home pay.

- Track revenue by offer each month.

- Track prep hours per client.

- Track sales cycle length.

- Track renewals and subscription churn.

- Shift low-margin work into higher-value packages.

Use mentorship as a feeder, not the whole model, if you need stronger cash flow. Corporate and executive offers can lift revenue per relationship, but only if the pipeline supports the longer close. Mix drives margin as much as rates do, so forecast by offer mix before you hire or add more delivery load.

3

Retention And Referrals

Retention and Referrals

Longer engagements keep owner take-home steadier because less cash goes to replacing clients. With CAC at $500 in Year 1 and $350 by Year 5, every renewal and referral protects margin by spreading acquisition cost across more billable months.

The inputs are client count, renewal rate, average engagement length, referral share, and CAC. Retention works best when each program has measurable client outcomes, a clear next step, and ethical fit; if structure is weak, cash gets less predictable and churn risk rises.

Track renewals that earn the next sale

Measure renewal rate, referral source, and time to close. If referrals rise, paid marketing pressure drops and more gross profit stays with the owner. Here’s the quick math: a retained client avoids another $500 to $350 CAC hit later on.

- Review outcomes before each renewal

- Document the next step in writing

- Ask for referrals after clear wins

- End bad-fit work early

Use simple scorecards for goals, attendance, and progress notes. That keeps cash more predictable and protects owner pay.

4

Sales And Marketing Efficiency

Sales And Marketing Efficiency

Net income improves when marketing brings in clients at a sustainable CAC (customer acquisition cost), not just more leads. In this model, annual marketing spend rises from $25k to $110k while CAC falls from $500 to $350, so growth only helps if close rate and revenue per client stay strong.

The quick math is simple: cheaper clients mean more cash left for delivery, overhead, and owner pay. Track lead source, close rate, payback, and revenue per client, because a full pipeline with weak conversions can still drag down profit. One bad move is scaling paid ads before offer-market fit is clear.

Measure CAC Before You Scale

Build the funnel by channel: partnerships, content, referrals, speaking, and paid ads. If those lower paid acquisition pressure, you protect margin and cash flow. Keep every source tied to CAC and payback strong>, not just clicks, calls, or lead count.

- Track lead source by channel.

- Measure close rate monthly.

- Compare revenue per client.

- Cut spend when CAC rises.

- Shift budget to referrals and speaking.

If a channel cannot pay back from client gross profit, it is too expensive, even when the pipeline looks busy. That’s the filter that protects owner income.

5

Expense Control And Operating Leverage

Expense Control and Operating Leverage

In a coaching firm, owner pay is what’s left after delivery costs and overhead. With 27% COGS and variable expenses in Year 1, every $100 of revenue leaves $73 before fixed costs. Then $516k fixed overhead, $140k payroll, and $25k marketing have to be covered before the owner can draw much at all.

The mix matters too. Necessary costs like insurance, accounting, assessment tools, and software protect delivery, but extra office space, events, and overbuilt systems can eat the spread. By Year 5, if delivery costs fall to 18%, the business keeps 9 points more gross margin, which directly lifts take-home income.

Track the cost load

Build the model from revenue, delivery cost %, fixed overhead, payroll, and marketing. Then separate required spend from discretionary spend so you can cut the right line first. If fixed costs rise faster than billable hours, owner pay gets squeezed even when sales grow.

Watch the gap between client revenue and full cost to serve. A clean rule: if a cost does not improve client results, renewals, or sales, challenge it. Keep one clean metric on the dashboard: cash left after delivery and overhead. That number tells you whether growth is actually paying the owner or just funding more complexity.

6

Compare lean, base, and high coaching owner-income scenarios

Owner income scenarios

Owner income shifts with client mix, staffing, and marketing spend, so the same coaching business can look tight, steady, or highly scaled across the model years.

| Scenario | Low CaseCash risk | Base CaseHiring risk | High CaseSales complexity |

|---|---|---|---|

| Launch model | The low case uses the Year 1 model with $316k revenue and $14k EBITDA, so owner income stays modest and cash stays tight. | The base case uses the Year 3 model with $131M revenue and $475k EBITDA, showing a fuller operating setup and higher owner income. | The high case uses the Year 5 model with $314M revenue and $184M EBITDA, which points to a much stronger owner income path. |

| Typical setup | A founder-led practice leans on individual coaching, keeps staffing light, and relies on early marketing spend to reach the Month 7 breakeven point. | The business expands into retainer, group, and subscription work, with more coaching staff and a larger service load. | The business runs with a larger team, more recurring clients, and heavier sales coordination across coaching lines. |

| Cost drivers |

|

|

|

| Owner income rangeBefore owner reserves | $134kLow income | $595kSteady build | $196MUpside income |

| Best fit | Use this to stress-test early cash pressure and see how much income the owner can keep if growth is slow. | Use this as the main planning case for a growing firm that is adding people and recurring work. | Use this to test upside when the firm can sell more recurring work without breaking delivery capacity. |

Planning note: These scenario figures are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions.

Related Products

- Professional Coach Porter's Five Forces Analysis

- Professional Coach BCG Matrix

- Professional Coach Business Model Canvas

- 7 Key Financial Metrics for Professional Coach Success

- Professional Coach Business Plan Template in Pre-Written Word

- 7 Strategies to Increase Professional Coach Profitability

- How to Manage Professional Coach Monthly Running Costs and Cash Flow?

- Professional Coach Startup Costs: $66K Setup And $848K Cash Need

- Professional Coach Financial Model Template in Excel

- How To Open A Professional Coaching Business In 30 To 90 Days

- How to Write a Professional Coach Business Plan (7 Steps)

- Professional Coach Marketing Mix

- Professional Coach Marketing Plan

- Professional Coach Business Proposal

- Professional Coach PESTEL Analysis

- Professional Coach Pitch Deck Example Editable PPTX

- Professional Coach Business SWOT Analysis

- Professional Coach Value Proposition Canvas

Frequently Asked Questions

Under these assumptions, owner economic income before tax is about $134k in Year 1 That includes a $120k founder salary plus $14k EBITDA By Year 5, the model shows $314M revenue and $184M EBITDA, but taxes, reserves, debt, and reinvestment can reduce actual cash taken out