Owner incomeYr1 -$324k; Yr5 $1.57M

Owner incomeYr1 -$324k; Yr5 $1.57MHow Much Does a Speakeasy Bar Owner Make? $90K Monthly Sales Math

Fully Editable

Instant Download

Professional Design

Pre-Built

No Expertise Is Needed

Description

Owner incomeYr1 -$324k; Yr5 $1.57M  Net margin-30% to 37%

Net margin-30% to 37% Revenue for target pay≈$4.3M

Revenue for target pay≈$4.3M Business difficultyHard

Business difficultyHard

You’re estimating owner income for a hidden retro bar, not a fixed salary This five-year model shows $90k average monthly revenue in Year 1, breakeven in Month 14, and EBITDA moving from -$324k in Year 1 to $1571M in Year 5, before personal taxes, debt payments, reserves, and owner distributions

Owner incomeYr1 -$324k; Yr5 $1.57MNet margin-30% to 37%Revenue for target pay≈$4.3MBusiness difficultyHardWant to test your owner income?

Owner income calculator

Estimate owner take-home and the target-pay gap from revenue, margin, costs, reserves, and your pay goal.

Planning note: This is a researched planning estimate only. It is not guaranteed salary, tax advice, or owner distribution advice.

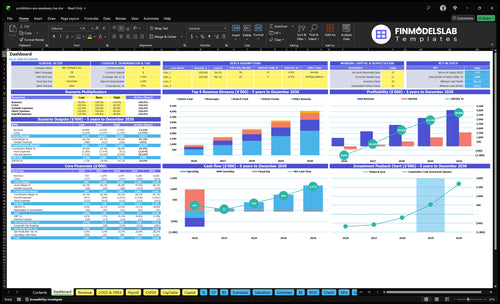

Want to see how owner income is checked in the Speakeasy Bar model?

This screenshot shows revenue, margin, costs, reserves, and owner take-home assumptions; open the Speakeasy Bar Financial Model Template.

Owner-income model highlights

- Owner income, not promise

- Revenue, EBITDA, breakeven

- Scenario tests, cash flow

Which speakeasy bar operating costs most reduce owner income?

If you’re running a Speakeasy Bar, payroll is the biggest drag on owner income, and the launch-cost math in What Is The Estimated Cost To Open And Launch Your Speakeasy Bar Business? shows why. In Year 1, wages total $759k across a $90k general manager, $80k head chef, $210k servers, and $160k line cooks. Fixed costs run $17,900 a month, led by $12,000 rent, while COGS starts at 145% of revenue and variable costs add 40% in Year 1, so every extra cost dollar cuts EBITDA before owner distributions.

Biggest cost hits

- Payroll is the main drag.

- Year 1 wages: $759k.

- Servers and line cooks total $370k.

- Rent adds $12k every month.

Cash flow pressure

- COGS: 145% of revenue in Year 1.

- Variable costs add another 40%.

- COGS falls to 117% by Year 5.

- Watch shrinkage, repairs, permits, security.

How much revenue does a speakeasy bar need to pay the owner?

For Speakeasy Bar, owner pay is not supported at Year 1 average revenue of about $90,000/month; the model first needs to cover COGS, payroll, fixed costs, variable costs, and reserves. A safer planning point starts around Year 2 revenue of about $147,000/month, where EBITDA is about $170,000/year; track the main driver in What Is The Most Important Metric To Measure The Success Of Speakeasy Bar?.

Cost Base

- $17,900 fixed costs monthly

- $63,250 payroll monthly

- $81,150 base before COGS

- Reserves come before owner draws

Owner Pay

- Year 1 EBITDA: -$324,000

- Year 2 EBITDA: $170,000

- Grow covers and average check

- Owner pay is a target

How does owner role change speakeasy bar take-home pay?

An owner-operated Speakeasy Bar can save cash, but it also consumes owner time, and the model already includes a $90k general manager. So take-home pay depends on EBITDA after reserves, not just on how many shifts you cover. Pay yourself through payroll or draws, but track them separately.

Owner pay

- $90k GM already covers core ops.

- Owner shifts can cut coverage needs.

- Unpaid labor is not free scale.

- Track payroll and draws separately.

Scale levers

- Extend strong nights.

- Raise seat utilization.

- Add private events.

- Test a second concept after cash stabilizes.

Want the six owner income drivers?

1

30-280/ntNightly Covers

More covers and better seat fill drive the biggest swing, with revenue growing from about $90K a month in Year 1 to $352K in Year 5.

2

$45-$72Guest Spend

Average spend rises from $45 midweek to $60-$72 on weekends, so upsells lift EBITDA without adding seats.

3

87%-90%Menu Margin

Food costs fall from 11% to 9% and drink costs from 3.5% to 2.7%, so tighter portioning and pour control keep more cash.

4

$759K-$1.28MLabor Load

Payroll climbs from about $759K to $1.28M a year, so staffing discipline decides how much growth turns into cash.

5

$17.9K/moFixed Overhead

Fixed costs sit near $17.9K a month, so every slow night has to clear that cash floor before profit shows up.

6

5%-9%Private Events

Events rise from 5% to 9% of sales, and booked groups add revenue without needing a full extra night of walk-ins.

Speakeasy Bar Core Six Income Drivers

Nightly Covers And Seat Utilization

Nightly Covers and Seat Use

Covers set the revenue ceiling for a hidden bar with limited seats. The model goes from 385 weekly covers in Year 1 to 1,240 weekly covers in Year 5, or about 3.2x. More filled seats lift revenue without changing rent, so each extra cover helps owner income faster than most cost cuts.

The main drag is long dwell time, reservation gaps, and hidden-entrance friction. Monday grows from 30 to 110 covers and Saturday from 90 to 280, but only if turns stay tight. Higher utilization is the path from negative Year 1 EBITDA to positive after Month 14.

Measure Turnover, Not Just Demand

Track covers, seat occupancy (the share of seats filled), dwell time, no-shows, and reservation gaps. The inputs are simple: seats available, guests seated, turn time, and cancellations. Here’s the quick math: when the room fills more often, sales rise while fixed costs stay mostly flat, so cash flow and owner pay improve.

- Watch covers by night.

- Separate Monday and Saturday.

- Measure turn time weekly.

- Cut entry delays fast.

Set separate targets for slow nights and peak nights. If guests linger too long, the bar loses one seating block and that revenue never comes back. On a limited-seat concept, small throughput gains matter more than big menu changes because they protect EBITDA and shorten the path to owner distributions.

1

Average Spend And Premium Pricing

Average Spend And Premium Pricing

Average spend, or AOV (average order value), is the check per guest. For this bar, midweek AOV rises from $45 to $57 and weekend AOV rises from $60 to $72. That lifts revenue from the same covers, so owner income can grow without adding the same payroll or rent.

Here’s the quick math: a $5 check lift across hundreds of weekly covers compounds fast. But the price has to match guest value. If craft cocktails, small plates, tasting menus, or themed presentation feel overpriced, repeat visits can fall and erase the gain.

Track AOV By Daypart And Menu Mix

Watch covers, AOV, repeat visits, and comped items by midweek versus weekend. Test higher prices on signature drinks, food pairings, and premium presentation, then compare gross profit against return visits. Revenue = covers × AOV, so small check gains matter most when labor and rent stay flat.

- Track AOV by daypart.

- Measure repeat visit rate.

- Limit discounts and comps.

- Price to guest value.

- Protect margin on signature items.

2

Beverage Cost And Gross Margin

Beverage Cost And Gross Margin

When drink and food cost run hot, owner pay gets squeezed first. Product cost comes out before labor, rent, and owner draw, so a cleaner gross margin leaves more cash to fund the rest. In the disclosed model, food cost drops from 110% to 90% of revenue and beverage cost falls from 35% to 27%, pulling combined COGS from 145% to 117%.

Here’s the quick math: on $1M of revenue, each 1 margin point = $10,000 of gross profit. The key inputs are menu mix, recipe cost, measured pours, comps, waste, and inventory counts. Shrinkage and overpouring hit cash fast, and if the bar cannot keep portions tight, EBITDA drops before any distributions reach the owner.

Track Pours, Waste, and Mix

Measure actual pour cost by drink, not just month-end COGS. Use recipe cards, measured pours, and weekly inventory counts so you can see where leakage starts. A shift toward higher-margin cocktails can move gross profit more than a price hike if guests already accept the concept.

- Track recipe cost per cocktail

- Count bottles every week

- Log comps and spill waste

- Review pour variance by bartender

If overpouring stays high, the margin story breaks even when sales rise. Control the bar well, and the owner keeps more of each dollar after product cost, which improves cash flow and lifts the chance of a real draw.

3

Labor Efficiency And Owner Involvement

Labor Efficiency

Labor is the biggest early cash burden. In this model, payroll is $759k in Year 1 and $1.278M in Year 5, so staffing has to match demand fast. The key inputs are the general manager, chefs, line cooks, servers, bartenders, dishwashers, and host staff. If headcount grows before covers do, owner take-home gets delayed.

Here’s the quick math: every added full-time worker (FTE) needs enough covers and check size to pay for itself. The owner can save cash by covering host duties, handling reservations, or controlling purchasing, but that trades money for time. Tight scheduling and cross-training help protect EBITDA during ramp-up.

Track Labor Before Adding Headcount

Watch covers per labor hour, payroll by role, and manager overtime by daypart. Add staff only when demand holds across weeks, not after one busy night. If long waits, slow turns, or entrance friction cut throughput, trim shifts before payroll drifts higher than sales can support.

- Track payroll against weekly covers.

- Split labor by daypart.

- Use owner hours as a bridge.

- Cross-train to cover peak shifts.

Use owner labor as a cash tool, not a permanent fix. Unpaid owner work lowers burn, but if it blocks sales, hiring, or purchasing, income still suffers. In the first months, a lean schedule can keep cash flow steadier and give the business more room to pay the owner later.

4

Fixed Costs, Buildout, And Compliance

Fixed Costs And Buildout

$17,900 in monthly fixed costs means the bar starts under pressure before the first cocktail sells. That includes $12,000 rent, $2,000 utilities, $750 insurance, $1,000 property taxes, $450 systems, $300 licenses and permits, $800 professional services, and $600 repairs. Fixed costs do not fall when covers miss plan, so they squeeze cash flow and delay owner pay.

The buildout also matters because startup capex totals $406k. Hidden entrance work, permit delays, and debt service can stretch the cash burn window. Downside protection, meaning how long cash lasts when sales miss plan, gets weaker fast here. With this fixed load, breakeven is pushed to Month 14, so slow traffic can turn into owner losses before pay starts.

Protect The Run Rate

Track the full monthly fixed-cost run rate before you sign the lease. The key inputs are rent, utilities, insurance, property taxes, systems, permits, professional fees, repairs, and debt service. Here’s the quick math: if the total sits near $17,900, every missed cover day matters more because those costs still hit the P&L.

- Test lease timing and free rent.

- Map permit steps and dates.

- Stress debt service before opening.

If the entrance buildout slips or permits drag, cash burn starts before revenue does. That pushes the owner’s take-home income back, because fixed overhead keeps running while sales are still ramping.

5

Private Events And Experience Revenue

Private Events And Experience Revenue

Pr ivate events add income beyond nightly covers by using the same bar, rent, and decor on slower days. In this model, event sales rise from 5% of total sales in Year 1 to 9% in Year 5, so every $100,000 of sales would imply about $5,000 to $9,000 from events. That helps owner pay only if the event mix stays profitable.

Think private parties, corporate buyouts, cocktail classes, ticketed tasting nights, and VIP experiences. The upside is real, but so is the risk: events need extra staffing, prep, marketing, and service capacity. If execution slips, regular guests can feel the impact, and the cash gain can disappear fast.

Track Event Margin Before You Scale It

Measure event revenue as a share of sales, plus labor hours, setup time, and prep cost per booking. The key test is simple: does the event still beat the profit from a normal night after paying for extra staff and materials? If not, it is volume without real income.

Use off-peak dates first, then price by headcount or buyout size so the event covers its own labor. One clean rule: protect the regular guest experience. Track repeat bookings, cancellation rate, and service issues, because poor execution can hurt the core business you depend on for cash flow.

- Book events on slower nights

- Track labor per event

- Price for extra prep

- Limit guest disruption

- Watch repeat booking rate

6

Compare low, base, and high owner income scenarios

Owner income scenarios

Owner income rises as covers, ticket size, and labor efficiency improve. The low case can keep draw near zero, while the mature case can support a much larger payout.

| Scenario | Low CaseLow | Base CaseBase | High CaseHigh |

|---|---|---|---|

| Launch model | Early ramp keeps owner draw near zero. | Stabilized operations support a meaningful owner payout path. | Mature operations can create a much larger owner-income path. |

| Typical setup | Year 1-like volume at about $90k monthly revenue and 385 weekly covers holds EBITDA at -$324k before owner pay. | Year 3-like performance at about $208k monthly revenue and 805 weekly covers produces $550k EBITDA before reserves, taxes, and debt. | Year 5-like maturity at about $352k monthly revenue and 1,240 weekly covers lifts EBITDA to $1.571M before distributions. |

| Cost drivers |

|

|

|

| Owner income rangeBefore owner reserves | Near $0Draw risk | $550kStabilized | $1.57MMature upside |

| Best fit | Use this to stress-test the opening year and cash strain before the room builds demand. | Use this as the main planning case for a room that has passed opening drag and is running steadily. | Use this to test upside in a full house with strong demand, but remember payback is still modeled at 42 months. |

Planning note: Scenario ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions.

Related Products

- Speakeasy Bar Porter's Five Forces Analysis

- Speakeasy Bar BCG Matrix

- Speakeasy Bar Business Model Canvas

- 7 Critical Financial KPIs for Speakeasy Bar Success

- Speakeasy Bar Business Plan Template in Pre-Written Word

- Increase Speakeasy Bar Profitability: 7 Strategies to Boost Margins

- How Much Does It Cost To Run A Speakeasy Bar Monthly?

- Speakeasy Bar Startup Costs: Plan For $629K Before Opening

- Speakeasy Bar Financial Model Template in Excel

- How To Open A Speakeasy Bar In 6 To 12+ Months

- How to Write a Speakeasy Bar Business Plan in 7 Steps

- Speakeasy Bar Marketing Mix

- Speakeasy Bar Marketing Plan

- Speakeasy Bar Business Proposal

- Speakeasy Bar PESTEL Analysis

- Speakeasy Bar Pitch Deck Example Editable PPTX

- Speakeasy Bar Business SWOT Analysis

- Speakeasy Bar Value Proposition Canvas

Frequently Asked Questions

In this model, first-year owner take-home is likely $0 because EBITDA is -$324k and minimum cash need peaks at $223k By Year 2, EBITDA reaches $170k, and by Year 3 it reaches $550k That is business profit before personal taxes, reserves, debt service, and owner distributions