Owner income$120k+

Owner income$120k+How Much Property Preservation Owners Make: $120K Salary, Month 29 Breakeven

Fully Editable

Instant Download

Professional Design

Pre-Built

No Expertise Is Needed

Description

Owner income$120k+  Net margin81% to 83.5%

Net margin81% to 83.5% Revenue for target pay$1.14M

Revenue for target pay$1.14M Business difficultyHard

Business difficultyHard

Under the provided assumptions, a property preservation business owner has a modeled founder salary of $120,000 per year, but that does not mean the business is profitable from day one EBITDA is negative in Year 1 at -$452,000 and Year 2 at -$218,000, then turns positive at $240,000 in Year 3 The model reaches breakeven in Month 29, with payback in 52 months Owner take-home should be planned as salary plus possible distributions only after field costs, overhead, chargebacks, reserves, debt, and reinvestment are covered

Owner income$120k+Net margin81% to 83.5%Revenue for target pay$1.14MBusiness difficultyHardWant to test your owner pay target?

Owner income calculator

Estimate owner take-home and the target-pay gap from revenue, margin, costs, reserves, and target pay.

Planning note: Research-based planning estimate only. It is not guaranteed salary, tax advice, or owner distribution advice.

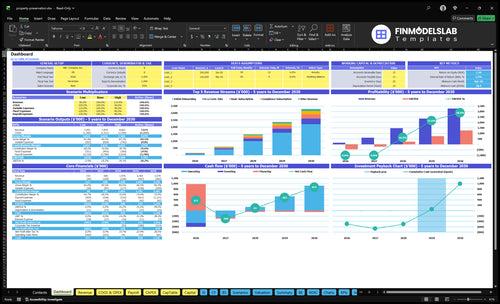

Want to check owner income in the Property Preservation model?

This view in the Property Preservation Financial Model Template shows revenue, margin, costs, reserves, and owner take-home assumptions, plus the $120,000 salary target. Open the model to see the full income math.

Owner-income model highlights

- Owner salary is $120k

- EBITDA reaches $1.274M

- Breakeven lands in Month 29

- Cash floor hits $20k

- Payback takes 52 months

- Tabs cover service mix

Is a property preservation business profitable as it scales?

Yes—Property Preservation can be profitable as it scales, but only after enough completed, approved, and collected work covers field costs, coordinators, overhead, and reserves. Here’s the quick math: the model shows negative EBITDA in Years 1 and 2, breakeven in Month 29, and about $240,000 EBITDA in Year 3. The catch is simple: growth helps, but quality control protects income as much as sales volume.

Where profit starts

- Month 29 is breakeven.

- Year 3 turns profitable.

- $240,000 EBITDA in Year 3.

- Work must be approved and collected.

Main scale risks

- Field coordinators grow from 10 FTE to 40 FTE.

- Watch vendor scorecards and compliance misses.

- Photo failures and chargebacks hit margins.

- Seasonal workload and route sprawl add cost.

How many property preservation work orders do you need to make money?

If your Property Preservation shop is still losing cash, the cutoff is not just how many work orders you get assigned. You have to watch completed orders, invoiced revenue, and collected cash, because Year 1 pricing runs from $75 Basic to $350 onboarding and breakeven is modeled at Month 29.

Revenue drivers

- $75 Basic plan starts the stack

- $120 Compliance lifts monthly value

- $200 Premium raises invoice size

- $150 a la carte jobs add cash

Cost and break-even

- Direct costs include 170% contractor payouts

- Usage technology adds 20% in Year 1

- Fixed overhead is $7,650 monthly before wages

- Volume must cover admin load, not field labor only

How much does a property preservation business owner make?

A Property Preservation owner can model $120,000 per year as CEO/founder pay, but that’s income capacity, not guaranteed cash; see What Is The Current Engagement Level For Property Preservation Services? before treating it like a fixed salary. The quick math: EBITDA is negative in Year 1 and Year 2, so early owner pay must come from capital or cash reserves.

Owner Pay

- $120,000 modeled annual founder salary

- Year 1 EBITDA: -$452,000

- Year 2 EBITDA: -$218,000

- Early pay needs reserves

Profit Path

- Year 3 EBITDA: $240,000

- Year 4 EBITDA: $747,000

- Year 5 EBITDA: $1,274,000

- Subcontractors scale faster with controls

Want the six drivers that move owner income?

1

$1.7MWork Orders

More completed work orders turn fixed staff and software cost into profit, which is the main path from the Year 1 loss to the Year 5 gain.

2

64%Service Mix

Shifting more accounts into compliance, premium, onboarding, and a la carte work lifts revenue per client because prices run from $75 to $375.

3

2ppField Margin

Cutting contractor payouts from 17% to 15% keeps more of each job after field labor.

4

29 moRoute Density

Tighter routing and scheduling cut wasted drive time and idle crews, which helps the business reach breakeven in Month 29.

5

2.0%Rework Control

Fewer chargebacks and redo visits protect the variable cost base when usage tech and storage already run at 2.0%.

6

$7.65KOverhead Control

Holding fixed overhead near $7,650 a month and keeping founder pay at $120,000 leaves more cash for reserves and owner draw.

Property Preservation Core Six Income Drivers

Completed Work Order Volume

Completed, Approved Work Orders

Completed and approved work orders are the volume that actually pays. In property preservation, assigned jobs and bid-only requests do not create cash until crews finish the work, photos pass review, invoices go out, and collections clear. Year 1 revenue comes from $75, $120, and $200 monthly plans, plus $350 onboarding and $150 a la carte jobs, so more approved volume lifts revenue capacity and speeds the path to Month 29 breakeven.

Measure the Full Closeout Chain

Track completed orders per day, approval rate, invoice lag, and collection lag to find where cash slows. If admin backlog delays billing or photos fail review, revenue slips even when field crews stay busy. Here’s the quick math: more approved jobs raise billings only if every step closes fast enough to turn work into cash.

- Count approved jobs, not assigned jobs.

- Watch photo rejections and rework.

- Bill same day when possible.

- Chase unpaid invoices fast.

1

Average Invoice And Service Mix

Service Mix Sets Owner Pay

Owner income improves when the job mix moves from low-ticket $75 Basic and $150 a la carte work toward $120 Compliance, $200 Premium, and $350 onboarding. Here’s the quick math: the same crew day can produce more collected revenue if approved work and recurring maintenance make up a bigger share of the book. That can lift EBITDA without adding the same route load.

Measure Mix by Approved Revenue

Track each service line on its own: Basic, Compliance, Premium, onboarding, and a la carte. The disclosed mix inputs start at 600% Basic, 300% Compliance, 100% Premium, and 400% a la carte attachment, so don’t blend them into one average. What matters is approval rate, attachment rate, and collected invoice per route day.

2

Field Gross Margin

Field Gross Margin

Field gross margin is what’s left after contractor labor, materials, supplies, fuel, disposal, tools, and other job-specific costs. Here’s the quick math: if direct costs climb, the owner’s cash shrinks because less is left to cover $7,650 monthly overhead, payroll, reserves, and pay. Weak job costing turns billed work into unpaid field effort.

Tighten Job Costing

Track margin by job, crew, and service type using completed work orders, labor hours, material tickets, fuel, disposal, and rework. The source model assumes contractor payouts from 170% in Year 1 to 150% in Year 5, with usage tech from 20% to 15%; gross margin is separate from EBITDA and owner distributions.

3

Route Density And Scheduling

Route Density And Scheduling

When vacant properties are grouped by service territory and maintenance day, crews spend less time driving and more time on billable work. That lifts completed jobs per day and gross profit per crew hour. Route sprawl does the opposite: even if invoice count rises, unpaid drive time, fuel waste, and crew idle time can wipe out margin on $75, $120, and $200 monthly plans, plus $150 a la carte work.

For forecasting, treat geography as a capacity limit, not just a sales map. Build the model around travel cost per job or per route because the source model does not separate fuel. The key inputs are properties per territory, average drive minutes, crew skill, and jobs completed per route day. If routing gets loose, cash flow and owner pay can lag even while revenue looks healthy.

Cluster Jobs by Territory

Track travel minutes per completed job, not just total miles. Schedule recurring maintenance by zip code and line up jobs that need the same crew skill on the same day. Then compare completed jobs, drive time, and gross profit before and after the change. If drive time climbs, margin usually falls faster than invoice volume grows.

- Price in route travel costs.

- Schedule by zip, not invoice.

- Match jobs to crew skill.

- Watch jobs per crew hour.

4

Chargebacks And Rework Control

Chargeback Control

Chargebacks, missing photos, failed compliance, and rework cut collected revenue, not just profit. In property preservation, booked work only turns into cash when the file passes vendor review, so deductions belong in the model as income risk and reserve need. One weak file can also hurt future assignments on vendor scorecards.

Track booked revenue, deducted revenue, and rework hours. Collected revenue equals booked revenue minus chargebacks and fixes that were redone before payment. If crews miss lock change proof, debris photos, or winterization records, the job can be paid late or not at all, while labor and fuel still hit cash flow.

Protect Payment

Use an editable chargeback percentage in the calculator because the source data does not give one. Pair it with the photo pass rate and compliance pass rate, then review deductions by cause: before-and-after photos, lock changes, debris, and winterization. That shows whether the fix is training, QC, or crew discipline.

- Log every deduction reason.

- Audit photos before billing.

- Score crews by acceptance rate.

When deductions fall, cash arrives sooner and fewer jobs turn into unpaid labor. That lifts gross margin and protects owner pay without adding more route miles or more assignments. A simple rule: if the file would fail a review, do not bill it yet.

5

Overhead, Reserves, And Owner Pay Discipline

Lean Overhead and Cash Reserves

Sustainable owner pay in property preservation starts with keeping fixed overhead at $7,650/month or $91,800/year before payroll. With Year 1 payroll at $397,500 and founder salary at $120,000/year, reported profit is not cash you can spend. Distributions should wait until collections, insurance, repairs, and reinvestment are funded.

The cash floor matters too: minimum cash is modeled at $20,000 in Month 28. As payroll climbs to $862,500 by Year 5, owner pay gets more exposed to slow client payments and backlog risk. One clean rule: do not treat all EBITDA as immediately distributable owner income.

Pay Yourself From Cash, Not Hope

Track collections, payroll timing, and reserve balance every month. The quick math is simple: if overhead stays lean and cash stays above the reserve floor, founder pay is safer; if not, draws should pause.

- Watch collected cash, not booked revenue.

- Hold draws until reserves are funded.

- Protect the $20,000 cash floor.

- Review overhead before adding staff.

6

Compare lean, base, and high owner income scenarios

Owner income scenarios

Owner income shifts with completed order growth, service mix, contractor cost, and overhead. The spread is widest before the business reaches the Year 3 profit turn.

| Scenario | Low CaseLow Case | Base CaseBase Case | High CaseHigh Case |

|---|---|---|---|

| Launch model | Owner pay stays at salary only while completed orders, approved bids, and service mix all run below plan. | Owner pay follows the model path as EBITDA moves from -$452k in Year 1 to $1.274m in Year 5. | Owner pay expands as route density improves, compliance mix rises, contractor payouts fall, and overhead stays controlled. |

| Typical setup | The business runs fewer completed jobs, weaker bid approval, a lower-value service mix, and more chargebacks, so cash gets tight. | The business uses the planned mix of basic, compliance, premium, onboarding, and a la carte work, with contractor payouts easing from 17.0% to 15.0%. | The business handles denser routes with a heavier compliance mix, lower contractor share, and tighter support costs. |

| Cost drivers |

|

|

|

| Owner income rangeBefore owner reserves | Salary-only owner payDownside case | Modest owner drawBase case | Meaningful owner drawUpside case |

| Best fit | Use this to stress-test a funded owner-operator setup when growth is slower than plan. | Use this as the main planning case for a sub contractor model moving into profit in Year 3. | Use this to test a multi-coordinator scale case with stronger margin and more room for owner pay. |

Planning note: Scenario ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions.

Related Products

- Property Preservation Porter's Five Forces Analysis

- Property Preservation BCG Matrix

- Property Preservation Business Model Canvas

- 7 Critical KPIs to Measure Property Preservation Success

- Property Preservation Business Plan Template in Pre-Written Word

- 7 Proven Strategies to Boost Property Preservation Margins

- How to Manage the Monthly Running Costs of Property Preservation?

- How Much It Costs To Start Property Preservation: $150k CAPEX

- Property Preservation Financial Model Template in Excel

- How To Start A Property Preservation Business In 30-90 Days

- How to Write a Property Preservation Business Plan in 7 Steps

- Property Preservation Marketing Mix

- Property Preservation Marketing Plan

- Property Preservation Business Proposal

- Property Preservation PESTEL Analysis

- Property Preservation Pitch Deck Example Editable PPTX

- Property Preservation Business SWOT Analysis

- Property Preservation Value Proposition Canvas

Frequently Asked Questions

The provided model carries a $120,000 annual founder salary, but early profit is negative EBITDA is -$452,000 in Year 1 and -$218,000 in Year 2, then turns positive at $240,000 in Year 3 Treat owner income as salary plus possible distributions after reserves, debt, reinvestment, and taxes