Title And Escrow Services Startup Costs: $736K Funding Plan

Key Takeaways

- Compliance costs start before approval and vary by state.

- Tech implementation starts Month 2 and runs through 5.

- Insurance and bonding costs depend on risk controls.

- Payroll and marketing need pre-opening cash, not capex.

Estimate Startup Costs with Calculator

Startup CAPEX Calculator

Estimates capitalized startup assets only for a title and escrow services launch.

Scope note This calculator covers capitalized startup assets only. It excludes inventory, payroll runway, deposits, debt service, working capital, rent runway, marketing spend, SaaS subscriptions, licensing, insurance, and other operating costs. Smaller launch items like legal research software, collateral, and backup power sit outside this block.

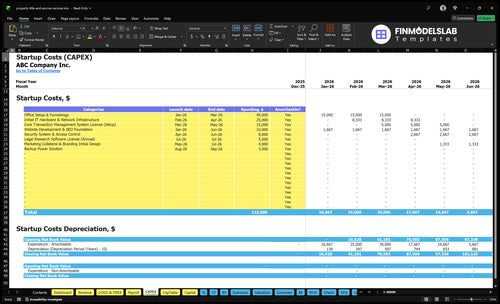

What does the CAPEX tab show?

This screenshot Title and Escrow Services Financial Model Template shows CAPEX, startup-cost categories, launch timing, depreciation/amortization; review assumptions before funding.

Screenshot highlights

- $115,000 CAPEX

- Month 1–9 launch

- $736,000 cash floor

- Month 8 breakeven

- EBITDA -$35k to $475k

What hidden costs of starting a title company should founders expect?

Founders should expect hidden costs to come from payroll, rent deposits, compliance, and slow cash collection, not just licenses and software. If you’re also asking about owner pay, see How Much Does The Owner Of Title And Escrow Services Business Typically Make?, but the bigger issue is that client escrow funds are restricted customer money, not working capital. In this model, $736,000 in minimum cash is needed by Month 7 even though breakeven is modeled for Month 8.

Upfront launch costs

- $25,000 Year 1 marketing budget

- $250 Year 1 CAC

- $3,500 monthly office lease

- $1,000 monthly accounting and legal

Cash timing traps

- Payroll starts before closings stabilize

- Rent deposits tie up cash fast

- Delayed receivables slow collections

- Compliance, audit, and cybersecurity costs hit early

How much money do you need to start a title company?

You need $736,000 of operating cash in the researched base case for a Title and Escrow Services launch, because the low point hits in Month 7 before volume fully ramps; see What Is The Current Growth Trajectory Of Your Title And Escrow Services Business? for the growth-trajectory lens behind that cash curve. Keep that separate from $115,000 of CAPEX and from protected client escrow funds, which are client money, not working capital.

Cash Need

- Survival cash: $736,000 by Month 7

- Startup CAPEX: $115,000 separately funded

- Client escrow funds: protected, not usable

- Year 1 overhead: $39,500/month before variable costs

Planning Signals

- Minimum launch budget covers opening only

- Realistic budget includes early ramp losses

- Breakeven arrives in Month 8

- Year 1 EBITDA: -$35,000

How do you fund a title and escrow company?

If you’re funding Title and Escrow Services, treat it like a cash plan, not a guess: the model calls for $736,000 minimum cash to cover $115,000 CAPEX, $387,500 Year 1 payroll, $7,250 monthly overhead, and $25,000 marketing. That implies about $41,625 in monthly burn before one-time setup costs, so the raise needs to carry the business through Month 8 breakeven with a cushion, not just launch expenses.

Funding plan

- $115,000 CAPEX starts operations

- $387,500 payroll drives fixed burn

- $7,250 overhead runs monthly

- $25,000 marketing supports demand

Investor and lender checklist

- Show use of funds clearly

- State owner contribution amount

- Set a reserve policy

- Share monthly forecast and insurance status

For lenders, the clean story is: here’s the cash need, here’s the burn, and here’s when breakeven closing volume should arrive. Use the financial model as the base, and use secondary assumptions only to test what changes if closings slip, underwriter approval slows, or insurance coverage is delayed.

Calculate Fuding Needs

Startup cost summary

Startup cost summary for opening a title and escrow services firm, separating startup CAPEX from excluded cash needs.

| Cost Category | Base Estimate | Main Cost Driver | CAPEX Calculator |

|---|---|---|---|

| Office Setup and Furnishings | $45,000 | Workspace fit-out and furnishings | Yes |

| IT Hardware and Network Infrastructure | $25,000 | Computers, network gear, and setup | Yes |

| Core Transaction Management System Setup | $15,000 | Transaction platform setup and licensing | Yes |

| Website Development, SEO, and Launch Collateral | $14,000 | Website build plus launch materials | Yes |

| Security, Backup Power, and Legal Research Software | $16,000 | Security, backup power, and software setup | Yes |

| Opening Cash Buffer | $736,000 | Payroll ramp, fixed overhead, and reserve | No |

Title and Escrow Services Core Five Startup Costs

Regulated Setup And Compliance Startup Expense

Formation Costs

Entity formation, title agency licensing where needed, escrow rules, legal review, and underwriter prep usually sit in the first compliance spend bucket. Model it with $200 a month for business licenses and fees plus $1,000 a month for accounting and legal services. Planning assumptions vary by state and underwriter, and approval is not automatic.

Compliance Inputs

This spend covers written procedures, trust accounting controls, background checks, compliance documentation, and audit readiness. Estimate it from the number of filings, review hours, and months of coverage you need before closing the first file. One clean line: the goal is to be ready for escrow handling before revenue starts.

Cost Control

Keep costs down by using one legal and accounting plan for launch, then updating only what the state or underwriter requires. Don’t skip trust controls, background checks, or written procedures to save a little cash; that creates bigger delay risk later. Use the same playbook across locations when rules allow, and recheck before each filing.

Underwriter Readiness

Underwriter approval prep should line up clean records, escrow policies, legal docs, and proof of controls before launch. That work is part of the startup budget, not a side task, because weak files slow openings and can block go-live. State rules vary, so plan for review time and keep every compliance document easy to show.

Technology And Secure Transaction Systems Startup Expense

Setup Stack

This budget covers title production software, escrow accounting controls, secure portals, e-signature tools, document storage, cybersecurity, wire fraud controls, scanners, secure printers, computers, and network gear. The core setup math is $15,000 for transaction system setup plus $25,000 for IT hardware and network infrastructure, with $40,000 before monthly SaaS starts.

Run Rate

Use two layers: one-time implementation and recurring support. Budget $750 per month for software and cybersecurity, plus 70% Year 1 external title search and transaction software COGS. Plan the cutover from Month 2 through Month 5 so training, data migration, and wire controls are live before volume builds.

- Separate setup, support, and COGS

- Test wire steps before go-live

- Phase rollout by team or office

Cost Control

Keep the stack lean by asking vendors to split setup, migration, and monthly support. That makes the $15,000 setup line and $750 monthly run rate easier to audit. The mistake is buying duplicate tools or skipping test runs on escrow and wire steps.

Wire Safety

Wire fraud controls are not optional here. Pair dual approval, callback rules, secure portals, and audit logs with trust accounting controls and document retention. If the team skips controls during the Month 2 to Month 5 build, the stack looks cheaper up front but error risk rises fast.

Insurance Bonding And Risk Control Startup Expense

Coverage stack

Title and escrow firms usually need a coverage stack: E&O for mistakes, fidelity for employee theft, cyber liability for data and wire fraud risk, and general liability for basic premises risk. Some states or underwriters also ask for surety or escrow bonds. Start with $800/month for E&O and liability, then add separate quotes for the rest.

How to price it

Estimate this line by multiplying months of coverage by the monthly premium, then adding bond fees if required. Ask each underwriter for limits, deductibles, and whether fidelity or cyber is bundled. Keep it in working capital, not CAPEX, because it recurs every month.

- Quote each coverage type

- Match limits to volume

- Check bond requirements

How to keep cost down

Lower cost by tightening controls, not by shrinking needed coverage. Use dual approval on wires, call-back checks for payee changes, background checks, trust accounting rules, and written procedures before shopping carriers. Better controls can help with underwriter expectations, but claims history and higher limits still move price. Wire fraud risk is the main reason to stay strict.

Budget impact

At $800/month, this starts at $9,600 a year before any bond costs. That sits alongside regulated setup, tech, and payroll, so founders should reserve cash early and compare quotes before launch. What this estimate hides: state rules, transaction volume, claims history, coverage limits, and risk controls can all change the bill.

Office Closing Room And Equipment Startup Expense

Office setup

Plan $45,000 for office setup and furnishings: closing table, chairs, reception area, staff desks, signage, and records storage. This is CAPEX if you buy it upfront. Add lease deposits separately, because they are cash tied up, not equipment. Do not include client escrow accounts in startup cost.

IT stack

Use $25,000 for IT hardware and network infrastructure, plus $8,000 for security system and access control and $3,000 for backup power. Add computers, scanners, secure printers, phones, and secure networking. Price it by unit count, vendor quotes, and installation labor. This is mostly CAPEX, not rent.

- Count each device and install fee

- Separate hardware from software

- Keep escrow funds off budget

Control spend

Keep the buildout modest and buy only what supports closings on day one. Ask for quotes on desks, scanners, and access control before you buy. A lean office can reduce upfront cash, but cutting security or backup power is the wrong place to save. One clean office is enough.

- Buy used furniture where allowed

- Delay extras until volume grows

- Protect records and network first

Rent and utilities

Model $3,500 monthly office lease and $600 monthly utilities and internet as operating expenses, not startup assets. If the lease needs a deposit, book that as cash on hand, not CAPEX. Here’s the quick split: buy the room, the gear, and the controls once; pay rent, power, and internet every month.

Staffing Payroll And Launch Marketing Startup Expense

Year 1 Payroll

10 CEO/principal escrow officers at $150,000, 10 senior title agents at $85,000, 10 escrow officers at $75,000, 5 title examiners at $65,000, and 10 administrative assistants at $45,000 drive the launch team. The model uses $387,500 of Year 1 payroll, so treat it as pre-opening cash and working capital, not a fixed asset.

Hiring Setup

This bucket covers recruiting, background checks, initial payroll before revenue, staff training, and notary readiness. Use hiring quotes, onboarding weeks, and first-closing timing to size the cash need. If start dates slip, payroll still runs, so keep enough working capital to cover the ramp without cutting compliance steps.

- Start background checks early

- Train before first closing

- Confirm notary readiness

Launch Marketing

The launch marketing budget is $25,000, with $250 CAC, so the spend supports about 100 customers before r epeat business. Put it into real estate agent and lender outreach, local launch marketing, referral development, and networking events. Keep the spend tied to booked meetings and signed referral relationships.

- Target agents and lenders first

- Track CAC at $250

- Use events for referrals

Cash Timing

What this estimate hides is timing. Payroll and marketing are working capital because they hit before steady revenue, and they can stretch if onboarding or referral building takes longer than planned. Keep them separate from CAPEX, since this cash funds people and demand generation, not equipment or buildout.

Compare 3 Startup Cost Scenarios

Startup Cost Scenarios

Lean, base, and full launches change cash need fast because staffing, office size, marketing, software, and insurance scale with county coverage and close volume.

| Scenario | Lean LaunchFounder-led | Base LaunchCore model | Full LaunchScaled rollout |

|---|---|---|---|

| Launch model | Run with owner-led staffing, a smaller office footprint, and lighter marketing while you prove referral flow. | Use a standard local office setup with the anchor Year 1 payroll, marketing, and breakeven profile. | Build for broader county coverage with higher staff count, deeper software, and higher insurance limits. |

| Typical setup | Keep the team tight, use basic software, and trim nonessential spend; savings come only from user-edited inputs. | Anchor the plan to $736,000 minimum cash need, $115,000 CAPEX, $387,500 Year 1 payroll, $25,000 Year 1 marketing, Month 8 breakeven, and -$35,000 Year 1 EBITDA. | Add more people, more systems, and broader coverage so the platform can handle higher close volume across counties. |

| Cost drivers |

|

|

|

| Planning rangeCAPEX only | Lower funding bandLowest cash | $736,000 minimum cash needBase case | Higher funding bandHighest cash |

| Best fit | Best for experienced founders testing one county with low monthly closings. | Best for operators with local real estate ties who want a standard launch path. | Best for seasoned founders planning multi-county coverage and higher monthly closings. |

Planning note: Scenario ranges are researched planning assumptions, not exact vendor quotes, lender terms, or legal bids.

Related Products

- Title and Escrow Services Porter's Five Forces Analysis

- Title and Escrow Services BCG Matrix

- Title and Escrow Services Business Model Canvas

- 7 Core KPIs to Drive Profitability in Title and Escrow Services

- Title and Escrow Services Business Plan Template in Pre-Written Word

- Increase Title and Escrow Services Profitability: 7 Actionable Strategies

- How to Calculate Running Costs for Title and Escrow Services Monthly?

- Title And Escrow Financial Model Template in Excel

- How Much Title And Escrow Services Owners Make At 48+ Closings

- How To Open A Title And Escrow Company In 3–6+ Months

- How to Write a Title and Escrow Services Business Plan

- Title and Escrow Services Marketing Mix

- Title and Escrow Services Marketing Plan

- Title and Escrow Services Business Proposal

- Title and Escrow Services PESTEL Analysis

- Property Title and Escrow Service Pitch Deck Example Editable PPTX

- Title and Escrow Services Business SWOT Analysis

- Title and Escrow Services Value Proposition Canvas

Frequently Asked Questions

The researched base case needs about $736,000 in minimum cash by Month 7 That figure sits above the $115,000 CAPEX budget because payroll, rent, insurance, software, legal, and marketing hit before closings fully ramp Do not include client escrow deposits in this number those funds are restricted and cannot pay operating bills