Owner income$68k

Owner income$68kHow Much Does a Pub Owner Make? $60k Salary Plus EBITDA Scenarios

Fully Editable

Instant Download

Professional Design

Pre-Built

No Expertise Is Needed

Description

Owner income$68k  Net margin16% to 412%

Net margin16% to 412% Revenue for target pay$425k

Revenue for target pay$425k Business difficultyHard

Business difficultyHard

Key Takeaways

- Sales volume drives growth, but costs decide income.

- Beverage and food margins protect owner cash flow.

- Labor and rent can outrun revenue fast.

- Events help, but extra costs must be modeled.

Owner income$68kNet margin16% to 412%Revenue for target pay$425kBusiness difficultyHardWant to test your pub owner income?

Owner income calculator

Estimate owner take-home and the target-pay gap from revenue, margin, costs, reserves, and target pay.

Planning note: Research-based planning estimate only. It is not guaranteed salary, tax advice, or owner distribution advice.

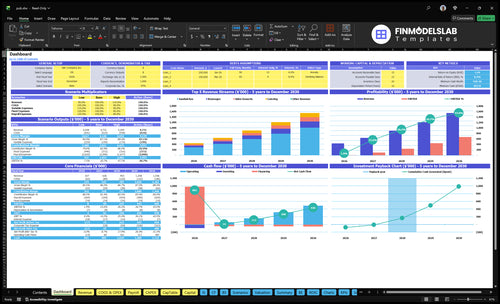

How do you check owner income in the Pub financial model?

This dashboard in the Pub Financial Model Template shows revenue, margin, costs, reserves, and owner take-home assumptions—open the model.

Owner-income model highlights

- Salary versus profit split

- $495k Year 1 revenue

- $162M Year 5 revenue

- $8k to $666k EBITDA

- $838k minimum cash

- Month 4 breakeven

- 28-month payback

How much does a pub owner make per year?

A Pub owner makes $60,000 per year in the source model if they work as the owner-manager, with EBITDA adding $8k in Year 1 to $666k in Year 5 before debt, taxes, reserves, and reinvestment; for the key operating lens, see What Is The Most Critical Metric To Measure The Success Of Pub?. Owner-operated labor protects cash flow, but it’s still a job, not passive income. A paid manager shifts payroll higher and cuts distributable profit unless sales rise.

Owner-operated

- $60k working owner-manager salary

- $8k Year 1 EBITDA add-on

- $99k Year 2 EBITDA add-on

- Cash flow improves with owner labor

Manager-run

- $237k Year 3 EBITDA add-on

- $443k Year 4 EBITDA add-on

- $666k Year 5 EBITDA add-on

- Manager payroll reduces owner profit

How much revenue does a pub need to pay the owner?

For a Pub, the model shows you can pay the owner $60k on $495k Year 1 revenue and still have about $8k EBITDA (earnings before interest, taxes, depreciation, and amortization) using only the listed Year 1 costs. But if you also need to cover $173k non-owner payroll and $744k fixed expenses, you need about $382k of revenue before any unlisted costs or reserves. So high sales do not automatically mean high take-home pay.

Owner pay math

- $60k owner salary is built in.

- $495k revenue supports Year 1.

- $8k EBITDA remains after listed costs.

- Cash buffer is still thin.

Revenue reality check

- $173k non-owner payroll is real.

- $744k fixed expenses are real.

- About $382k revenue is needed.

- Unlisted costs and reserves add pressure.

What profit margin does a pub make?

A Pub’s margin starts thin and then scales fast: the model uses EBITDA margin as the operating profit marker, at about 16% in Year 1, then 147% in Year 2, 251% in Year 3, 349% in Year 4, and 412% in Year 5. For startup cost context, see How Much Does It Cost To Open A Pub Business? because the spread depends on pour control, food waste, comps, promotions, payroll, and scheduling.

Margin path

- EBITDA starts at 16% in Year 1.

- It rises to 147% in Year 2.

- It reaches 251% in Year 3.

- It climbs to 349% and 412%.

What drives it

- Variable costs improve from 195% to 160% of sales.

- Beverage mix stays at 15% each year.

- Beverage supplies fall from 30% to 25%.

- Control pour, waste, comps, promos, payroll, scheduling.

Want the six pub income drivers?

1

535-1.5K/wkSales volume

Weekly covers rise from 535 in Year 1 to about 1.5K by Year 5, and that spread is what lets fixed costs get diluted and owner income grow.

2

3.0%-2.5%Beverage margin

Beverages stay at 15% of sales while supplies ease from 3.0% to 2.5% of revenue, so each drink keeps a bit more profit.

3

11.5%-9.5%Food margin

Food ingredients fall from 11.5% to 9.5% of revenue, so the core sandwich-led menu keeps more gross profit as sales scale.

4

$233K-$430KLabor productivity

Payroll moves from $233K to $430K, so labor productivity has to keep pace or the extra sales will leak straight out of take-home.

5

$6.2K/moFixed overhead

Rent, utilities, insurance, and admin total $6.2K a month, so low table fill can wipe out the gain from strong nights.

6

10%-15%Peak events

Catering rises from 10% to 15% of sales, so event nights add higher-check revenue without needing more seats every day.

Pub Core Six Income Drivers

Sales Volume

Sales Volume

Sales volume starts with covers per day, average check, and operating days. In Year 1, traffic runs from 50 covers Monday to 110 Saturday, or 535 weekly covers. By Year 5, volume reaches 1,485 weekly covers, while midweek AOV rises from $15 to $18 and weekend AOV from $20 to $24.

That lifts revenue from $495k to $162M, but revenue is not income. The owner only gets paid after COGS, payroll, rent, debt, reserves, and taxes are covered. So the real question is not just how many guests show up, but how much profit each open day leaves behind.

Track Covers and Check Size

Measure covers by day, AOV by weekday versus weekend, and sales per open day. Here’s the quick math: more traffic helps most when the extra covers come with steady check size and controlled labor. If sales rise but staffing, comps, or prep waste rise faster, take-home income still falls.

Use a simple weekly dashboard and watch these inputs:

- Daily covers by day of week

- Average check by daypart

- Open days and peak-night fill rate

- Revenue per labor hour

1

Beverage Margin

Beverage Margin

Beverage gross margin, the profit left after drink supply cost, is a direct owner-income lever in a licensed on-premise pub. With beverages at 15% of sales, supply cost at 30% of beverage sales in Year 1 means about 4.5% of total sales goes to beverage supplies; at 25% in Year 5, that drops to 3.75%.

This driver includes drink mix, happy hour pricing, comps, draft waste, and over-pouring. The model does not split beer, wine, and spirits, so don’t invent pour costs. If beverage margin slips, cash for payroll, rent, and owner draws tightens fast.

Control Beverage Waste

Track beverage sales, supply invoices, comps, and waste every week. Here’s the quick math: at 15% beverage mix, every 1-point swing in beverage supply cost changes total sales by about 0.15 points, so small fixes can lift profit without adding more tables.

- Watch draft waste daily.

- Limit free pours.

- Test happy hour pricing.

- Review drink mix weekly.

Tight specs, clear ring rules, and fast variance checks protect margin. If promos or over-pouring rise, gross profit falls before the owner feels it in pay.

2

Food Program Margin

Food Program Margin

The food program is where the pub turns menu sales into cash for the owner. In this model, sandwiches make up 65% of sales in Year 1 and 60% in Year 5, with sides and desserts at 10% and catering rising from 10% to 15%. That mix decides how much gross profit is left after kitchen costs.

The disclosed ingredient rate improves from 115% of sales in Year 1 to 95% in Year 5. Here’s the quick math: every $100 of food sales moves from a -$15 ingredient loss to a +$5 gross profit before prep labor and overhead, a $20 swing that can reach the owner’s draw.

Control Menu Cost and Waste

Track item-level food cost, waste, and catering share. Use recipe cards, weekly vendor quotes, and sales by item group so you can see where margin leaks start. Sandwiches still drive the mix at 65% of sales in Year 1, so small price or portion changes have a big cash effect.

- Recipe cost by item

- Waste and comps

- Vendor price changes

- Catering share

- Menu price by item

Keep the menu tight and prep simple. If a new dish adds labor but does not lift check size or margin, it reduces the cash left for rent, taxes, and owner pay. Kitchen complexity can look busy and still dilute profit fast.

3

Labor Productivity

Labor Productivity

Labor productivity means how much revenue each labor hour buys. Here, payroll rises from $233k in Year 1 to $430k in Year 5, while the owner-manager salary stays at $60k a year. Non-owner payroll grows from $173k to $370k, so the key test is covers per labor hour, not just headcount.

At 47% of revenue in Year 1, payroll already takes a big bite out of cash; at 266% in Year 5, it can swamp the model unless sales density or staffing changes. Owner shifts can save cash, but that is earned labor, not passive income. One clean rule: if labor rises faster than covers, owner pay gets squeezed first.

Track labor per cover

Measure labor cost as % of revenue, labor per cover, and sales per labor hour every week. Use covers, average check, hours worked, owner shifts, overtime, and non-owner payroll to forecast cash. If weekend checks are higher, staff for those peak blocks and keep midweek coverage tight.

- Watch overtime before it grows.

- Match hours to cover counts.

- Separate owner work from profit.

- Cut low-value prep time.

Review the schedule against actual traffic. If labor runs above plan, fix the rota, menu complexity, or opening hours before cutting owner draws. The owner’s $60k salary should be treated as a working cost, because extra shifts support cash flow only when they also lift sales or replace paid staff.

4

Occupancy And Fixed Costs

Fixed Cost Pressure

For this pub, fixed costs set the break-even floor. Rent is $4k per month, but total listed fixed expenses are $62k per month, or $744k per year. That means owner take-home gets squeezed fast if sales dip, because these costs hit before profit or draw.

Here’s the quick math: fixed expenses equal about 150% of Year 1 revenue and 46% of Year 5 revenue. That includes utilities, insurance, POS fees, internet, cleaning, maintenance, accounting, and legal. Lease terms, permits, music licensing, and liquor-license costs are local assumptions, not universal US amounts.

Track the Full Overhead Stack

Measure fixed costs monthly as a share of sales, then compare that to the sales plan by daypart. If covers miss plan, overhead does not shrink with them, so owner cash flow drops first. The key inputs are rent, contract services, license fees, and every recurring bill that stays due whether the room is full or half empty.

Keep a simple rollup of each fixed line and test every renewal. Small cuts matter when monthly overhead is $62k. If a fee does not help traffic, speed, or compliance, challenge it. That is how you protect the margin that pays debt, reserves, and the owner.

5

Events And Peak Nights

Events & Peak Nights

Events can lift pub sales without adding rent, but they only help owner income if the extra room fills with enough check volume to cover added labor, entertainment, security, marketing, cleanup, and comp risk (freebies and discounts). The model does not split trivia, live music, sports nights, or private parties, so use catering as the closest proxy; it rises from 10% to 15% of sales.

Measure event profit, not just turnout

Track event count, attendance, average check, and fully loaded event cost. A catering coordinator starts after launch, and the salary can reach $25k a year at 10 FTE later, so bake that labor into margin before you book more peak nights. If event gross profit does not beat a normal night, it will cut owner draw.

- Test one event type first.

- Price for added labor.

- Track comps and cleanup.

6

Compare low, base, and high pub owner income scenarios

Owner income scenarios

Owner income moves with weekly covers, pricing, and payroll. Debt, reserves, taxes, and reinvestment still come out before any distribution.

| Scenario | Low CaseDownside case | Base CasePlan case | High CaseUpside case |

|---|---|---|---|

| Launch model | This is the tighter earnings case, with Year 1 at 535 weekly covers, $495k revenue, and $8k EBITDA. | This is the modeled base case, with Year 3 at 945 weekly covers, $945k revenue, and $237k EBITDA. | This is the stronger earnings path, with Year 5 at 1,485 weekly covers, $162M revenue, and $666k EBITDA. |

| Typical setup | The pub opens with a $60k owner salary, a 16% EBITDA margin as given, and thin cash after payroll, rent, and other overhead. | The pub keeps a $60k owner salary, a 251% EBITDA margin as given, and a payroll base around $354k before owner distributions. | The pub carries a $60k owner salary, a 412% EBITDA margin as given, and a larger payroll base around $430k before distributions. |

| Cost drivers |

|

|

|

| Owner income rangeBefore owner reserves | Salary onlyThin cash | Salary plus drawCore plan | Salary plus larger drawUpside case |

| Best fit | Use this to stress-test a slow start, weaker trade, or higher-than-planned costs before distributions. | Use this as the main planning case for budgets, lender talks, and owner pay checks. | Use this to test strong trade, but still subtract debt, reserves, taxes, and reinvestment before taking cash out. |

Planning note: These scenario ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions.

Related Products

- Pub Porter's Five Forces Analysis

- Pub BCG Matrix

- Pub Business Model Canvas

- Track 7 Core KPIs to Scale Your Pub Business

- Pub Business Plan Template in Pre-Written Word

- How to Increase Pub Profitability Using 7 Financial Strategies

- How Much Does It Cost To Run A Pub Each Month?

- How Much Does It Cost To Open A Pub? $838k Cash Plan

- Pub Financial Model Template in Excel

- How To Open A Pub In The US: 6 To 12+ Month Launch Guide

- How to Write a Business Plan for a Pub (7 Essential Steps)

- Pub Marketing Mix

- Pub Marketing Plan

- Pub Business Proposal

- Pub PESTEL Analysis

- Pub Pitch Deck Example Editable PPTX

- Pub Business SWOT Analysis

- Pub Value Proposition Canvas

Frequently Asked Questions

In this model, the owner-manager salary is $60k per year, or $5k per month Extra take-home depends on distributable EBITDA, which is $8k in Year 1 and $666k in Year 5 before debt, taxes, reserves, and reinvestment Treat that as planning math, not a guaranteed payout