Owner income$282K

Owner income$282KHow Much Radio Advertising Owners Can Make on $891K Revenue

Fully Editable

Instant Download

Professional Design

Pre-Built

No Expertise Is Needed

Description

Owner income$282K  Net margin31.6%

Net margin31.6% Revenue for target pay$891K

Revenue for target pay$891K Business difficultyHard

Business difficultyHard

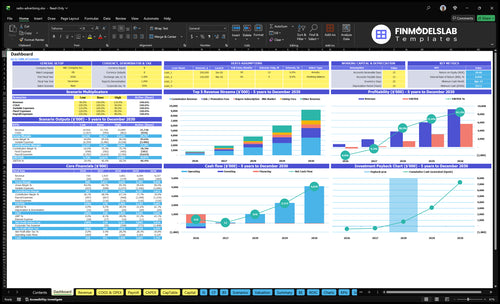

A radio advertising business owner can make meaningful income if the business keeps enough margin after station pass-through costs, sales commissions, support, marketing, and fixed overhead In the first-year planning case, $118 million in advertiser billings produces about $891,000 in revenue before extra seller fees After 6% COGS, 10% variable expenses, $116,400 fixed overhead, and $350,000 acquisition marketing, about $282,000 remains before wages, owner pay, taxes, debt, and reserves These are researched planning assumptions, not guaranteed earnings or tax-adjusted distributions

Owner income$282KNet margin31.6%Revenue for target pay$891KBusiness difficultyHardWant to test your owner pay?

Owner income calculator

Estimate owner take-home and target-pay gap from revenue, margin, costs, reserves, and target pay.

Planning note: This is a researched planning estimate only. It is not guaranteed salary, tax advice, or owner distribution advice.

How do you check owner income in the Radio Advertising model?

Dashboard shows advertiser count, seller count, mix, AOV, costs, reserves, and owner income; open the Radio Advertising Financial Model Template.

Owner-income model highlights

- Charts billings to cash

- Tests ramp, base, mature

- Shows costs and reserves

What is a realistic radio advertising profit margin?

If you're sizing Radio Advertising, don’t chase one universal margin; the first-year model shows 84% contribution before fixed overhead and marketing, after 6% COGS and 10% variable expenses. For startup cost context, see What Is The Startup Cost To Launch Your Radio Advertising Business?, because retained margin still depends on fixed commission per order, variable commission rate, and subscription fees.

Margin drivers

- 84% contribution before fixed costs

- 6% COGS already in model

- 10% variable expenses already in model

- Fixed commission changes take-home fast

Revenue scale

- $1,314K commission revenue

- On $118M gross billings

- $7,596K subscription revenue added

- Renewals and support costs move margin

What changes when scaling a radio advertising business?

Scaling Radio Advertising raises revenue, but it also raises payroll risk, support load, and cash timing pressure. The model shifts from 200 sellers and 1,000 buyers in year one to 900 sellers and 5,357 buyers in a mature year, so the team has to close profitable billings faster than commissions and overhead grow. Buyer mix also moves from 70% small business and 5% enterprise to 50% small business and 12% enterprise, while seller mix shifts from 60% local stations to 40% and national broadcasters rise from 10% to 18%.

What grows

- 200 sellers becomes 900.

- 1,000 buyers becomes 5,357.

- Enterprise buyers rise from 5% to 12%.

- National broadcasters rise from 10% to 18%.

What gets harder

- Payroll grows before cash lands.

- Support load rises with more users.

- Commissions must stay below billings.

- Overhead can outrun profit fast.

How much revenue does a radio advertising business need to pay the owner?

If the owner wants $100K in pay, Radio Advertising needs about $674K in retained revenue under the provided model. Here’s the quick math: first-year contribution margin is 84% after 6% COGS and 10% variable expenses, and owner salary should stay separate from distributions.

Revenue math

- 84% contribution margin

- $100K owner pay target

- $1.164M fixed overhead

- $350K acquisition marketing

Pay structure

- Keep salary separate

- Use distributions after salary

- Cover reserves before payouts

- Track fixed costs monthly

Want the six biggest income drivers?

1

1.0KActive Advertisers

At 1.0K first-year buyers, more live advertisers lift commission and fee revenue, so cash before owner pay scales fast.

2

$500-$5KMonthly Ad Spend

A mix from $500 small business to $5K enterprise orders pushes revenue up faster than headcount, so take-home rises with spend per account.

3

84%Retained Margin

After 6% COGS and 10% variable expenses, the 10% variable commission and $10 fixed fee decide what cash before owner pay keeps.

4

$1.16MOverhead Control

Holding fixed overhead near $1.16M matters because these costs hit EBITDA directly and set how much cash reaches owner pay.

5

0.8-1.8xClient Retention

Repeat orders of 1.5x for small business, 1.2x for mid-market, and 0.8x for enterprise spread sales cost over more billings, so cash before owner pay improves.

6

$140-$750Sales Efficiency

With $350K marketing, buyer CAC falling from $200 to $140 and seller CAC from $750 to $500 keeps more of that spend as cash before owner pay.

Radio Advertising Core Six Income Drivers

Active advertisers

Active advertisers

Active advertisers are the buyers placing live orders and renewing campaigns. In the first-year model, 1,000 buyers are funded with $200K of buyer marketing at $200 CAC, so every extra active account matters. More active advertisers lift recurring billings and make owner pay less dependent on a few accounts.

The mix is 70% small business, 25% mid-market, and 5% enterprise. Enterprise buyers can reach $5,000 AOV, but the repeat-order assumption is only 0.80. That means quality matters: weak fit raises churn, which forces more acquisition spend and cuts cash left for profit and draws.

Measure repeat, not just signups

Track active advertisers by segment, repeat order rate, and CAC payback. Here’s the quick math: $200 CAC only works if retained billings keep coming back, so the real metric is revenue per active account, not raw buyer count. One-liner: more repeat buyers beat more one-off buyers.

- Active advertisers by segment

- Repeat order rate by cohort

- CAC versus retained billings

- Churn from weak account fit

If enterprise buyers renew poorly, shift effort to the segments with steadier repeat. That keeps acquisition spend from outrunning revenue and helps protect monthly cash flow, especially before the base is large enough to absorb churn.

1

Monthly ad spend

Monthly Ad Spend

Monthly ad spend is the money each advertiser commits per month, and it sets how fast retained revenue grows. In the first year, assumed AOV is $500 for small business, $1,500 for mid-market, and $5,000 for enterprise. Higher spend usually beats stacking lots of tiny buys, because one larger campaign can produce more billings with less account churn.

Spend depends on campaign frequency, station mix, market size, and advertiser goals. Mature-year AOV rises to $580, $1,900, and $7,000, so the owner’s income improves when buyers move from one-off tests to repeat monthly plans. Better campaign budgets beat tiny one-off buys.

Raise Spend per Advertiser

Track how many accounts stay above each AOV tier and how often they renew. If small businesses sit near $500 and never move up, retained revenue stays thin. The quick math is simple: more monthly spend means more gross billings per active buyer, so the same sales effort can support higher owner pay.

- Track spend by customer type.

- Test station mix and frequency.

- Match budgets to market size.

- Document goals before quoting.

- Watch repeat spend, not one-offs.

What this estimate hides is fit: a weak campaign budget can look busy but still produce low retained revenue. Push for clear monthly plans, then price around the value of reach and repetition. If an account can support $1,500 or $5,000 a month, it usually improves cash flow faster than three small buyers at the same sales cost.

2

Retained commission margin

Retained Commission Margin

Owner pay depends on what the platform keeps, not the full $118M in gross billings. With a $10 fixed commission per order plus 10% of order value, the model shows $1.314M in commission revenue, and buyer and seller subscriptions add $7.596M before extra seller fees.

This is the cash that pays support, sales, and overhead, so the take rate (the share the platform keeps) matters more than raw spend. Gross billings are not profit. If order value or subscription mix drops, the owner’s draw can shrink even when volume looks strong.

Track Margin by Order, Not Just Volume

Measure orders, average order value, fixed fee per order, variable commission %, and subscription revenue separately. Here’s the quick math: retained revenue = fixed commissions + variable commissions + subscriptions, then subtract sales, support, and fixed overhead.

- Watch order count by account type.

- Track AOV by campaign.

- Separate subscriptions from transaction fees.

- Test pricing before adding headcount.

If gross billings grow but fee yield slips, the owner keeps less. Tight fee terms and better subscription mix usually improve take-home income faster than chasing more ad spend.

3

Advertiser retention

Renewal Rate

Advertiser retention is the share of buyers who place another order. It matters because renewals stabilize cash flow and cut pressure on paid acquisition. In year one, repeat order assumptions are 150 for small business, 120 for mid-market, and 80 for enterprise; by the mature year, they rise to 180, 140, and 100. More repeats mean more revenue with less new-customer spend, so owner take-home improves faster.

Here’s the quick math: retention depends on active advertisers, order frequency, campaign size, and seasonality. It improves when reporting links airtime to calls, visits, leads, or sales, because buyers can see proof. Seasonal advertisers need planned follow-up, not last-minute selling, or repeat orders slip and the business must keep paying to replace lost revenue.

Track Repeat Orders by Segment

Measure repeat orders separately for small business, mid-market, and enterprise. A buyer that renews from 80 to 100 orders is worth more than a one-time account, even before pricing changes. Watch renewal rate, time between orders, and which reports get opened. If the reporting does not show business results, retention weakens and acquisition costs eat profit.

Build follow-up into the campaign calendar. Send proof of performance before the buyer’s next budget decision, then book the next flight early. Seasonal accounts should get a planned reactivation date, because late outreach usually means missed revenue. The goal is simple: keep more advertisers buying again, so fixed costs and owner pay are covered by recurring billings, not constant prospecting.

4

Sales labor efficiency

Sales Labor Efficiency

Sales labor efficiency is how much revenue a rep and support team can sell before commissions and service work eat the margin. In this model, first-year sales commissions are 7% of revenue and customer support scaling is 3%, so team-sold revenue gives up about 10% before other overhead. Owner-sold revenue keeps more cash for owner pay.

Here’s the quick math: on $100,000 of billings, first-year team labor uses $10,000; in mature year, it drops to 7% total because commissions fall to 5% and support to 2%. The key inputs are revenue per rep, commission rate , support load, and how much billings repeat. If demand is not proven, payroll can push profit down fast.

Track Billings Before You Hire

Measure billings per rep, repeat orders, and support hours per $1,000 sold. If a new rep does not cover the 7% commission plus the 3% support load, the hire cuts take-home income before it helps it. The owner should compare team-sold margin with owner-sold margin every month, not just top-line growth.

Use a simple hiring rule: add payroll only after current reps show steady profitable billings. If mature performance gets to 5% commission and 2% support, margin improves, but only after the team proves demand. Keep the forecast tied to actual closed revenue, not pipeline hope.

- Track revenue per rep monthly

- Separate owner-sold from team-sold

- Watch support cost by billings

- Hire after proven demand

5

Fixed overhead control

Fixed overhead control

Fixed overhead is the cost base that stays on every month: office rent, legal and accounting, software, cybersecurity, fixed digital advertising, insurance, and travel. At $9,700 per month, that is about $116.4K per year, so owner take-home improves only when recurring billings cover that base early. One line: fixed costs do not wait for renewals.

That load is much easier to carry after scale than in year one, when revenue is only $891K. If renewals are shaky, every extra fixed dollar cuts cash flow and delays profit draws; if repeat orders hold, the same overhead becomes much easier to absorb and the owner can pay themselves sooner.

Keep overhead boring

Track monthly fixed cost run rate, then compare it with recurring gross profit. Here’s the quick math: $9,700 × 12 = $116.4K before owner pay. If repeat revenue is not stable, don’t lock in new rent, long software contracts, or fixed ad spend that cannot flex with bookings.

Use a monthly gate: add no new fixed cost until renewals are steady and current overhead is covered by repeat orders. Review each line item for whether it helps close deals, retain advertisers, or invoice faster. If it does not, cut it or move it variable.

6

Compare low, base, and high radio advertising owner income scenarios

Owner income scenarios

Owner income changes fast as seller count, buyer count, and commission mix scale. Early ramp-up, year-three growth, and mature volume create very different cash profiles.

| Scenario | Low CaseRamp-up | Base CaseScaling | High CaseMature |

|---|---|---|---|

| Launch model | This is the early income path with lower volume and thinner owner take-home. | This is the modeled growth path with steadier volume and stronger owner income. | This is the stronger income path with mature volume and the highest owner take-home. |

| Typical setup | First-year assumptions use 200 sellers, 1,000 buyers, $118M billings, and $891K revenue before extra seller fees, with about $282K before wages and reserves. | Year-three assumptions use 500 sellers, 2,813 buyers, $466M billings, and $316M revenue, with about $187M before wages and reserves. | Year-five assumptions use 900 sellers, 5,357 buyers, $1,271M billings, and $761M revenue, with about $545M before wages and reserves. |

| Cost drivers |

|

|

|

| Owner income rangeBefore owner reserves | $282KRamp-up | $187MScaling | $545MMature |

| Best fit | Use this to stress-test the business if ramp-up is slow or close rates stay light. | Use this as the main planning case for budgeting, hiring, and cash timing. | Use this to test upside if acquisition stays efficient and larger accounts keep scaling. |

Planning note: Scenario ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions.

Related Products

- Radio Advertising Porter's Five Forces Analysis

- Radio Advertising BCG Matrix

- Radio Advertising Business Model Canvas

- 7 Critical KPIs for Radio Advertising Platforms

- Radio Advertising Business Plan Template in Pre-Written Word

- 7 Strategies to Boost Radio Advertising Platform Profitability

- How to Manage Monthly Running Costs for Radio Advertising Services

- How Much It Costs To Start A Radio Advertising Business: $916K+ Year 1

- Radio Advertising Financial Model Template in Excel

- How To Start A Radio Advertising Business In 6 To 12 Weeks

- How to Write a Radio Advertising Business Plan (7-Step Financial Guide)

- Radio Advertising Marketing Mix

- Radio Advertising Marketing Plan

- Radio Advertising Business Proposal

- Radio Advertising PESTEL Analysis

- Radio Advertising Pitch Deck Example Editable PPTX

- Radio Advertising Business SWOT Analysis

- Radio Advertising Value Proposition Canvas

Frequently Asked Questions

In the first-year planning case, about $282,000 remains before wages, owner pay, taxes, debt, and reserves That comes from $118 million in advertiser billings and $891,000 in retained revenue before extra seller fees Actual take-home depends on payroll, reserve policy, and how much cash the owner leaves in the business