Owner income$70k

Owner income$70kHow Much Can a Raw Juice and Smoothie Bar Owner Make? $70k Salary

Fully Editable

Instant Download

Professional Design

Pre-Built

No Expertise Is Needed

Description

Owner income$70k  Net margin15% to 48%

Net margin15% to 48% Revenue for target pay$347k

Revenue for target pay$347k Business difficultyHard

Business difficultyHard

A raw juice and smoothie bar owner can make a planned $70,000 salary in this model, but extra owner distributions depend on cash left after payroll, rent, ingredients, packaging, reserves, debt, and taxes The researched Year 1 case produces about $645,840 in revenue and $105,000 in EBITDA, which is profit before interest, taxes, depreciation, and amortization By Year 5, revenue rises to about $171 million and EBITDA to $863,000 under the traffic and pricing assumptions That’s a planning range, not a guaranteed salary

Owner income$70kNet margin15% to 48%Revenue for target pay$347kBusiness difficultyHardWant to test your owner pay target?

Owner income calculator

Estimate owner take-home and the target-pay gap from revenue, margin, costs, reserves, and target pay.

Planning note: Research-based planning estimate only. It is not guaranteed salary, tax advice, or owner distribution advice, and it does not include financing terms unless entered.

Want to check owner income in the full financial model?

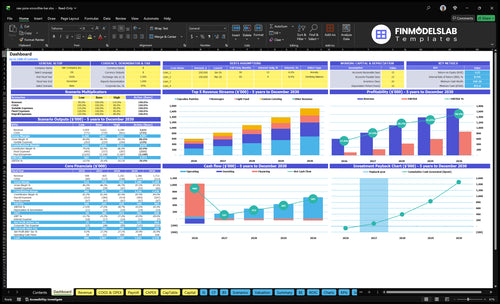

The screenshot in the Raw Juice and Smoothie Bar Financial Model Template ties assumptions to revenue, COGS (cost of goods sold), labor, overhead, cash flow, and owner pay. It shows Year 1 revenue of $6458k, Year 1 EBITDA of $105k, Year 5 EBITDA of $863k, $70k owner salary, month 4 break-even, 20-month payback, and $831k minimum cash need in Month 2; use it as planning support, not a promise. Open the model.

Owner-income model highlights

- $70k owner salary

- Revenue and EBITDA shown

- Month 4 break-even

- Month 2 cash need

How much revenue does a juice bar need to pay the owner?

For a Raw Juice and Smoothie Bar, paying the owner a $70k annual salary means about $58k per month in owner pay math. With 81% contribution after ingredients, packaging, and marketing, plus $167k in non-owner payroll and $56k in fixed overhead, the model needs about $347k in monthly sales before taxes, debt, and reserves. Year 1 monthly revenue averages about $538k, so the pay target is covered if volume stays on plan.

Owner pay math

- $70k yearly owner salary

- About $58k per month

- 81% contribution margin

- $347k monthly sales needed

Cost stack

- $167k non-owner payroll

- $56k fixed overhead

- Before taxes and debt

- Year 1 average: $538k monthly revenue

Does a juice bar make more money if owner operated?

Raw Juice and Smoothie Bar only makes more cash if the owner replaces paid labor or lifts sales enough to cover that time. Here’s the quick math: Year 1 payroll is $270k with a $70k owner-operator salary plus $200k in non-owner payroll, and by Year 5 it rises to $390k; if you buy back owner time with managers or extra staff, cash drops unless volume rises too. Separate wages from profit distributions so you can see what the business truly earns.

When owner-op helps

- Replaces one paid shift

- Can improve short-term cash

- Helps if sales stay flat

- Works when owner drives traffic

When it hurts cash

- Adds managers or extra staff

- Pushes payroll toward $390k

- Needs higher volume to offset

- Keep wages out of profit math

Can a juice bar owner make a living?

Yes, a Raw Juice and Smoothie Bar owner can make a living in this case: the launch model includes a $70k owner-operator salary, about $645.8k Year 1 revenue, $105k EBITDA, and Month 4 breakeven. The catch is execution: the shop must hold about 121 daily transactions at a blended ticket near $14.70, and track repeat demand through What Is The Most Important Indicator Of Customer Satisfaction For Raw Juice And Smoothie Bar?.

Living wage math

- Includes $70k owner salary

- Targets $645.8k Year 1 sales

- Shows $105k EBITDA

- Breaks even in Month 4

Owner draw risk

- Hold 121 daily transactions

- Keep ticket near $14.70

- Delay draws if labor runs high

- Delay draws if waste or rent spikes

What drives juice bar owner income most?

1

121-263/dayCustomer volume

More daily orders spread rent and labor across more sales, so owner income rises fastest as traffic builds.

2

$14.7-$17.9Average ticket

A higher blended ticket lifts revenue without adding the same number of orders, and weekends carry the strongest basket size.

3

84%-86%Gross margin

Keeping ingredient and packaging spend tight protects the share left after direct costs, which drives cash more than top-line growth alone.

4

$270K-$390KLabor mix

Payroll is the biggest controllable cost block, so staffing to demand matters if you want EBITDA to turn into real owner cash.

5

$5.6K/moRent overhead

Fixed overhead stays on even in slow weeks, so lean rent and utility control help more once sales dip or seasonality hits.

6

15%-20%Added channels

Growing custom catering from 15% to 20% adds higher-ticket sales and smooths weekday demand without relying only on walk-ins.

Raw Juice and Smoothie Bar Core Six Income Drivers

Customer Traffic And Transaction Volume

Daily Orders and Covers

Customer traffic, or covers meaning paid orders, sets the revenue base for owner pay. Here’s the quick math: 845 weekly covers ÷ 7 = 121 orders per day in Year 1, and 1,840 weekly covers ÷ 7 = 263 orders per day in Year 5. More orders lift sales and help spread fixed labor and rent across a bigger base.

Friday through Sunday matter most: 380 weekend covers in Year 1 and 750 in Year 5, or about 45% and 41% of weekly volume. If seasonality, weak repeat traffic, slow mornings, or location mismatch cut traffic, cash flow drops fast and the owner’s draw gets squeezed even before profit looks weak.

Track Covers by Daypart

Measure daily covers, weekend share, and repeat visits each week. If Friday-Sunday are carrying the business, staff and prep should match that pattern. If mornings are slow, test breakfast bundles, earlier hours, or local partnerships only when the added covers cover the extra labor.

Use a simple weekly scorecard: covers by hour, weekday versus weekend split, and the gap to forecast. That tells you if traffic can support owner pay. If traffic misses plan for several weeks, fix hours, offers, or site fit before adding payroll or assuming the draw will hold.

- Count covers by hour.

- Separate weekday and weekend.

- Watch repeat visits monthly.

- Test morning offers carefully.

1

Average Ticket And Menu Mix

Average Ticket And Menu Mix

Average ticket is the dollars per order, and it matters because each extra dollar runs through high gross margin before labor and rent. In this model, midweek ticket rises from $12 in Year 1 to $15 in Year 5, while weekend ticket rises from $18 to $22. Higher ticket size can lift owner pay fast if volume holds.

Menu mix drives that ticket: larger smoothies, protein add-ons, wellness shots, bottled juices, bundles, and catering orders. The upside is real, but premium ingredients and price sensitivity can eat into the gain, so a higher check only helps if gross margin stays strong. Here’s the quick math: more add-ons means more revenue per guest, not just more guests.

Track Mix, Then Price the Upside

Measure ticket by daypart and by item type, not just by store average. If weekend orders run at $22 and midweek at $15, you want to know which add-ons and bundles create that lift. The goal is simple: raise revenue per order without pushing away repeat buyers.

- Track attach rate for add-ons.

- Test bundle pricing weekly.

- Watch gross margin by item.

- Flag price-sensitive menu items.

- Separate catering from walk-in sales.

What this estimate hides: if premium produce, protein, or bottled packs rise too fast in cost, the ticket gain may not reach profit. A one-dollar lift in average check helps only when the extra gross margin is larger than the extra waste, labor time, and discounting needed to sell it.

2

Ingredients, Packaging, And Waste

Ingredients, Packaging, and Waste

Ingredients and packaging sit right above payroll and rent in the cash waterfall. In Year 1, 14% of sales goes to ingredients and 2% to packaging, leaving 84% gross margin. That margin funds labor, rent, reserves, and owner pay, so even small waste can squeeze take-home income fast.

Here’s the quick math: if produce spoils, portions run heavy, or add-ins cost more than planned, gross margin drops even when sales stay flat. The model’s Year 5 target shows 12.5% ingredients and 1.5% packaging, for 86% gross margin. What this hides: gross margin is not owner income; overhead still comes out next.

Track Recipe Cost and Waste

Track cost per recipe, not just total food spend. Use purchase price, yield, and portion size to build true recipe cost, then compare it with menu price and actual shrink. If the cup, lid, or add-in changes, the margin changed too.

- Spoilage by produce type

- Yield by recipe

- Portion counts by shift

- Add-in margin by item

- Cup and lid cost per order

- Prep waste by day

Test smaller default portions, tighter prep batches, and priced add-ins. If waste rises on weekends or slow mornings, cut batch size or raise price on the weakest items. That keeps gross margin closer to plan and protects cash for payroll and owner pay.

3

Labor Model And Owner Involvement

Labor Mix And Owner Time

Payroll is the biggest cost the owner can still control after sales volume. In Year 1, payroll is $270k, including a $70k owner salary and $200k for staff. By Year 5, payroll rises to $390k while owner pay stays flat, so the extra burden is on cash flow, not the owner’s draw.

This model needs orders per day, prep time, peak rush coverage, closing shifts, and weekend demand. The labor shift is large: non-owner staff payroll climbs to $320k, up 60% from Year 1. If manager-led coverage protects owner time, sales must rise enough to pay for it, or profit gets squeezed.

Staff To The Rush, Not The Hope

Track labor by daypart, not just by month. Compare weekday prep and closing hours against weekend covers, then staff to the actual traffic pattern. Here’s the quick test: if added manager coverage does not lift sales or reduce owner hours enough to justify the cost, it cuts owner income.

- Separate owner and staff hours

- Track labor per order weekly

- Match staffing to rush windows

- Test manager coverage against sales

Use the owner salary as a hard floor in forecasting. With $70k fixed for the owner, any labor creep above plan comes straight out of profit unless covers, ticket, or weekend volume improve first. That is the part to watch closely when the business starts adding more shifts and more supervision.

4

Rent, Location, And Fixed Overhead

Rent Sets the Sales Floor

Fixed overhead is the monthly cost you pay before owner income is safe. Here, modeled overhead is $5,620 per month, led by $3,500 rent, plus $800 utilities, $300 insurance, $150 POS, $100 website hosting, $400 accounting and legal, $250 cleaning, and $120 internet and phone. That is $67,440 a year before any owner draw.

Better locations can lift traffic, but higher rent pushes the breakeven point up fast. One clean line: higher rent only works if extra sales come with it. Watch repairs, permits, and local cost creep, because small monthly add-ons can quietly eat the cash that should pay the owner.

Track the Full Fixed Cost

Measure each fixed line monthly and compare it with sales. If rent, utilities, or fees drift up, owner pay drops first because the store has less cash left after overhead. The key inputs are monthly sales, lease cost, and every recurring bill tied to the site.

Before signing a lease, test whether the location adds enough daily traffic to justify the higher base cost. Cheap rent with weak traffic is still a bad deal, but so is a busy corner that wipes out margin. Keep a simple rent-to-sales check and update it whenever the landlord, utility bill, or permit fee changes.

5

Added Revenue Channels

Added Revenue Channels

These channels add scheduled sales, not just more sales. If custom catering and other preorders move from 15% of sales in Year 1 to 20% by Year 5, daily volume gets steadier and owner pay is easier to support. The best case is when these orders fill slow production windows instead of crowding out counter sales.

The risk is extra labor and spoilage. Bottled juice packs, wellness shot bundles, cleanse packages, gym partnerships, and corporate wellness orders can lift revenue but still miss the mark if packaging, delivery planning, or short shelf life push costs up faster than the check size. More channels only help income if each one stays margin-positive after labor and waste.

Track Profit Per Channel

Measure each channel by order count, average ticket, labor minutes, packaging cost, and spoilage rate. Compare preorders, gym partnerships, and corporate orders against walk-in sales so you can see which ones raise take-home pay. A channel that adds 20% of sales but needs too much labor can still cut owner income.

- Track margin per order.

- Cap spoilage each week.

- Price delivery separately.

- Schedule prep by demand.

- Forecast peak labor hours.

6

Compare low, base, and high owner-income scenarios

Owner income scenarios

Traffic, basket size, and staffing swing owner income the most. EBITDA (earnings before interest, taxes, depreciation, and amortization) rises as orders and average order value improve.

| Scenario | Low CaseLow Case | Base CaseBase Case | High CaseHigh Case |

|---|---|---|---|

| Launch model | This is the lower earnings path with a softer first-year launch. | This is the modeled core path for steady operating results. | This is the stronger earnings path if volume and pricing hold up. |

| Typical setup | Year 1 runs about 121 daily orders at a blended $14.70 average order value, with 84% gross margin after ingredients and packaging and about $270k payroll. | Year 3 reaches about 186 daily orders at a blended $16.06 average order value, with 84.9% gross margin and about $337.5k payroll. | Year 5 reaches about 263 daily orders at a blended $17.85 average order value, with 86% gross margin and about $390k payroll. |

| Cost drivers |

|

|

|

| Owner income rangeBefore owner reserves | $105,000 EBITDAYear 1 EBITDA | $426,000 EBITDAYear 3 EBITDA | $863,000 EBITDAYear 5 EBITDA |

| Best fit | Use this to stress-test a slower start and tighter cash room. | Use this as the main plan if traffic and staffing track the model. | Use this to test upside if demand stays strong and labor stays controlled. |

Planning note: These ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions.

Related Products

- Raw Juice and Smoothie Bar Porter's Five Forces Analysis

- Raw Juice and Smoothie Bar BCG Matrix

- Raw Juice and Smoothie Bar Business Model Canvas

- 7 Financial KPIs to Scale Your Raw Juice and Smoothie Bar

- Raw Juice And Smoothie Bar Business Plan Template in Pre-Written Word

- Increase Raw Juice and Smoothie Bar Profitability: 7 Strategies

- Operating Costs: How to Run a Raw Juice and Smoothie Bar Monthly

- How Much To Open A Raw Juice And Smoothie Bar: $831k Plan

- Raw Juice and Smoothie Bar Financial Model Template in Excel

- How To Open A Raw Juice And Smoothie Bar In 3 To 6 Months

- How to Write a Raw Juice and Smoothie Bar Business Plan

- Raw Juice and Smoothie Bar Marketing Mix

- Raw Juice and Smoothie Bar Marketing Plan

- Raw Juice and Smoothie Bar Business Proposal

- Raw Juice and Smoothie Bar PESTEL Analysis

- Raw Juice and Smoothie Bar Pitch Deck Example Editable PPTX

- Raw Juice and Smoothie Bar Business SWOT Analysis

- Raw Juice and Smoothie Bar Value Proposition Canvas

Frequently Asked Questions

The model includes a $70,000 annual owner-operator salary It also shows EBITDA of $105,000 in Year 1 and $863,000 in Year 5, but EBITDA is not the same as take-home cash Extra draws depend on reserves, debt, taxes, reinvestment, and whether the shop keeps hitting its traffic targets