Owner income$21.2M

Owner income$21.2MHow Much Real Estate Crowdfunding Owners Make at $179M Deployed

Fully Editable

Instant Download

Professional Design

Pre-Built

No Expertise Is Needed

Description

Owner income$21.2M  Net margin227%

Net margin227% Revenue for target pay$9.3M

Revenue for target pay$9.3M Business difficultyHard

Business difficultyHard

Using the researched assumptions, a real estate crowdfunding owner has about $172k of first-year pre-tax pay capacity after listed variable costs and $300k of marketing, before payroll, software, reserves, debt service, and personal taxes By the mature year, that capacity reaches about $235M, driven by $125B of deployed investor capital and $283M of platform revenue These are planning outputs, not guaranteed salary, dividends, investor returns, tax advice, or securities advice

Owner income$21.2MNet margin227%Revenue for target pay$9.3MBusiness difficultyHardWant to test your owner pay?

Owner income calculator

Estimate owner take-home and the target-pay gap from revenue, margin, costs, reserves, and target pay.

Planning note: Research-based planning estimate only. Not guaranteed salary, tax advice, or owner distribution advice.

Want to check owner income in the full Real Estate Crowdfunding model?

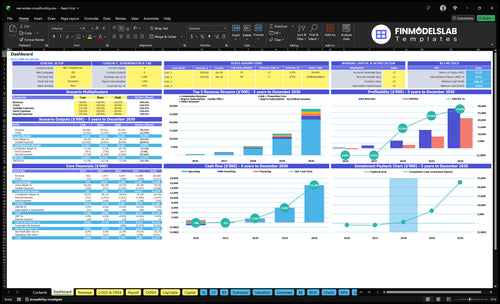

This screenshot in the Real Estate Crowdfunding Financial Model Template shows revenue, deployed capital, margin, and owner pay assumptions. Open the model.

Owner-income model highlights

- Buyer CAC: $200 to $100

- Seller CAC: $5k to $3k

- Commission: 150% to 125%

- Marketing: $300k to $3M

- Tests fee mix, costs, reserves

- Compare $530k, $45M, $283M

What costs reduce real estate crowdfunding platform profit margin?

For a Real Estate Crowdfunding platform, the biggest margin hit is getting users and deals in the door; see How Much Does It Cost To Launch Your Real Estate Crowdfunding Platform?. Year one marketing is $300k split between $100k seller acquisition and $200k buyer acquisition, and listed COGS of 6% plus legal and compliance at 3% and investor support and onboarding at 2% take another 11% of revenue. On $530k of first-year revenue, that leaves about $172k before payroll, software, reserves, and taxes.

Acquisition spend

- $100k seller acquisition

- $200k buyer acquisition

- Seller CAC starts at $5,000

- Buyer CAC starts at $200

Other margin drains

- Listed COGS are 6% of revenue

- Legal and compliance are 3% per entity

- Investor support and onboarding are 2%

- These costs cut pay capacity fast

How much AUM does a real estate crowdfunding platform need?

For a Real Estate Crowdfunding platform, the AUM needed is set by your target owner pay, fee yield, and marketing spend. With a 297% first-year blended revenue yield on deployed capital and 11% listed variable costs, $300k of marketing creates about $172k of pre-tax pay capacity before payroll and reserves; break-even before owner pay and omitted overhead is about $1.135M deployed using $300k ÷ 264%.

Scale math

- 297% blended revenue yield

- 11% listed variable costs

- $300k marketing spend

- $172k pre-tax pay capacity

What it means

- $1.135M break-even deployed capital

- Before owner pay and omitted overhead

- Target salary is a planning output

- It is not guaranteed compensation

How do real estate crowdfunding platforms make money?

Real Estate Crowdfunding platforms make money from platform fees, not investor returns or property cash flow; for KPI context, see What Is The Main Success Indicator For Your Real Estate Crowdfunding Platform?. Here’s the quick math: $178.5M deployed at a 1.50% commission creates about $2.678M in first-year commission revenue.

Main fee streams

- $2.678M commission on deployed capital

- $222k buyer subscription revenue

- $334k seller subscription revenue

- $70k listing and promotion fees

Revenue logic

- Commission scales with funded deal volume

- Subscriptions create recurring monthly revenue

- Listing fees are seller-paid and one-time

- Property cash flow belongs to deal economics

Want the six main income drivers?

1

$17.9M-$1.25BAUM Scale

More capital on the platform drives more fee dollars, and that lifts pre-tax owner take-home fastest.

2

2.97%-2.27%Fee Yield

A higher blended fee rate turns the same capital base into more revenue and more pre-tax owner take-home.

3

20-333/yrDeal Pipeline

More closed listings mean more funded deals, so revenue grows faster than the fixed team cost.

4

$200-$100Investor CAC

Lower buyer CAC and better repeat investing keep marketing spend from eating pre-tax owner take-home.

5

11%Compliance Load

An 11% first-year variable load takes a big slice off the top, so each point saved flows to owner cash.

6

-$711K→$21.2MStaffing Leverage

A fixed-heavy team means each new dollar of revenue can widen EBITDA and raise pre-tax owner take-home.

Real Estate Crowdfunding Core Six Income Drivers

Capital Deployed And Retained

Capital Deployed

Income rises when pledged capital actually closes and gets deployed. In the model, deployed capital is $1,785M in year 1, $1,723M in year 3, and $1,249B in the mature year. Higher family office and accredited investor mix can lift average order value, so more qualified dollars should expand both commission and subscription revenue.

One clean rule: funded capital pays, pledges do not. The main risk is counting commitments that never close, which flatters the pipeline but not owner income. Track deployed dollars, repeat investment, and capital still active on the platform, because retained capital is what keeps revenue coming back without restarting acquisition spend.

Track Funded Dollars

Use funded deals as the core metric, not signed interest. Here’s the quick math: if pledged capital is high but close rates slip, revenue stalls even when the funnel looks full. Better retention means more capital stays active, so the same investor base can keep producing commission and subscription income.

- Track funded deals weekly.

- Split capital by investor type.

- Measure repeat investment rate.

- Watch active capital on-platform.

To improve this driver, push larger checks from family offices and accredited investors, then follow up fast on any pledge that has not funded. The goal is simple: raise the share of capital that closes, stays invested, and comes back for the next deal.

1

Blended Platform Fee Structure

Blended platform fee mix

The owner’s income depends on how much comes from upfront commissions, recurring subscriptions, and scale-based fees. Here’s the quick math: as capital scales, variable commission falls from 150% to 125%, and blended platform revenue yield drops from 297% to 227%. That means each deployed dollar earns less as the platform gets bigger, so the fee mix has to protect margin, not just topline.

Subscriptions from buyers and sellers can smooth cash flow, while promotion and listing fees are smaller add-ons. But higher fees can hurt sponsor demand, investor trust, and deal flow, which then cuts commissions and owner pay. What this estimate hides: if funded capital slows, the recurring base looks stronger than it really is.

Measure fee yield by capital stage

Track deployed capital, fee yield per dollar, and revenue mix by offering type. Split the model into commission, subscription, promotion, and listing fees so you can see which line pays the owner and which one just adds noise. If a fee change lifts conversion or retention, it may grow profit more than a bigger rate would.

- Watch funded dollars, not pledges.

- Track sponsor close rates monthly.

- Test fees by investor segment.

- Measure subscription attach and churn.

- Check trust complaints after price changes.

Use a forecast that ties fee mix to cash flow and owner draw. If commissions fall toward 125% at scale, recurring fees have to carry more of the fixed load. If onboarding takes longer or sponsors push back on pricing, the platform may still grow but the owner’s take-home can stall.

2

Deal Flow And Underwriting Quality

Deal Flow And Underwriting Quality

More seller flow only helps if the platform can underwrite deals that actually close. Here, seller acquisition grows from 20 sellers in year 1 to about 333 in the mature year, so the funnel gets wider fast. If underwriting is weak, approved properties stall, capital velocity slows, and fee income lands later or not at all.

The seller mix also shifts toward larger sponsors, with REIT fund share rising from 10% to 30%. That usually means bigger checks and more repeatable deal sizes, but only if diligence stays tight. Track sponsor pipeline, approved properties, funded close rate, and diligence cost; better deals make income more durable and owner pay less volatile.

Track Closable Deals, Not Just Leads

Measure the gap between sourced sponsors and funded closings. A strong pipeline with low close rates is expensive, because diligence work gets paid before revenue does. The quick test is simple: if approved properties rise but funded deals do not, underwriting quality is the bottleneck.

Keep a short list of core metrics: pipeline size, approval rate, funded close rate, and diligence cost per approved deal. Use those numbers to cut weak sponsors early, focus on larger repeat sellers, and protect cash flow. One clean rule: only scale what can close.

- Track sponsor source by channel

- Review approved-to-funded conversion weekly

- Compare diligence cost to closed revenue

- Prioritize larger, repeat sponsors

3

Investor Acquisition And Retention

Investor acquisition and retention

Investor acquisition and retention drives how much capital actually gets funded, and how expensive it is to get there. If buyer CAC falls from $200 to $100, the platform keeps more of each raise. That matters more as buyer marketing rises from $200k to $2M, because weak conversion turns spend into burn, not deployed capital.

Order size also shapes payback. Retail investors start near $5,000 AOV, accredited investors at $25,000, and family offices at $100,000. Here’s the quick math: a $100 CAC equals 2% of a $5,000 order, 0.4% of a $25,000 order, and 0.1% of a $100,000 order. Retention matters because repeat investors lower the cash burned to fund new deals.

Track capital efficiency, not just sign-ups

Measure capital raised per marketing dollar, repeat investment rate, onboarding completion, and investor support load. If onboarding is slow, funded capital lags even when sign-ups look strong. The owner gets paid when investors move from interest to funded orders and then come back again, not when traffic spikes.

One clean rule: if CAC is rising while repeat buys stay flat, acquisition is masking churn. Segment by investor type, since a $5,000 retail order, $25,000 accredited order, and $100,000 family office order do not need the same support spend. Tighten onboarding and service so support cost stays below the margin from each funded investor.

- Track funded dollars, not leads.

- Watch repeat buys by cohort.

- Cut onboarding drop-offs fast.

- Cap support load per investor.

4

Compliance And Administration Load

Compliance and admin load

Compliance and admin work can take fee revenue before the owner gets paid. The stated first-year load is 3% legal and compliance per property entity, 2% investor support and onboarding, 4% due diligence and underwriting, and 2% transaction processing, or about 11% before filings, escrow, reporting, audit support, and fund administration. On $1M of fee revenue, that is roughly $110k gone before owner pay.

By the mature year, the known due diligence, transaction processing, and legal percentages are said to total at least 65%, so margin depends on tight controls and enough closed volume. If commitments do not fund, the platform still carries the work but does not get the cash. The key check is admin cost as a share of revenue, by property entity and by funded deal.

Track the work that eats margin

Price and forecast each workstream before launch: filings, escrow, reporting, audit support, and fund administration. Measure them against funded deals, not just signed commitments, and keep separate counts for onboarding and due diligence so you can see where the burn sits. If support load rises faster than funded capital, owner income will lag even when top-line fees look strong.

- Track admin cost per property entity.

- Count only funded deals.

- Review support load by workflow.

5

Staffing And Operating Leverage

Right-Sized Staffing

Owner income rises when recurring revenue grows faster than payroll, software, servicing, and admin costs. In year one, founder-led operations protect cash, but they also put underwriting, investor relations, compliance coordination, and support on the same team, so execution risk goes up fast.

The first-year pay capacity is only $172k, so every extra hire has to pay for itself. Mature-year economics look good only if headcount does not scale one-for-one with deployed capital; otherwise, revenue grows but distributable cash gets trapped in overhead.

Keep Headcount In Line

Track recurring revenue per employee, support tickets per investor, deals per underwriter, and compliance tasks per property. Those are the inputs that show whether staff is helping margin or just keeping up. If revenue is not rising faster than labor and admin spend, owner pay will stall.

- Model payroll against funded deals.

- Test outsource versus hire.

- Watch support load by investor tier.

- Cap hiring until recurring revenue covers it.

Here’s the quick math: if a new role does not lift closed deals, repeat investment, or servicing speed enough to cover its cost, it cuts cash available for the owner. Right-sized staffing turns growth into distributable cash instead of a bigger org chart.

6

Compare low, base, and high owner-pay scenarios

Owner income scenarios

Owner income moves with capital deployed, investor mix, and compliance load. The low, base, and high cases show how faster scale can lift cash left for the owner.

| Scenario | Low CaseLean case | Base CaseBase case | High CaseScale case |

|---|---|---|---|

| Launch model | Owner income stays under pressure because capital deploys slowly and compliance costs take a bigger share of cash. | Owner income follows the modeled launch path with steady deployment and normal fee load. | Owner income climbs in the mature-year scale path as capital deployment and revenue expand sharply. |

| Typical setup | This case assumes higher CAC, heavier compliance, slower deployment, and more reserves, so the platform spends more before income can clear. | This case uses $1.785M first-year deployed capital, $530k revenue, 11% listed variable costs, $300k marketing, and $172k pay capacity before omitted overhead. | This case reflects Year 3 or later scale, with $1.723M to $1.249B deployed capital and $45M to $283M revenue. |

| Cost drivers |

|

|

|

| Owner income rangeBefore owner reserves | ($711k) to ($112k)Lean band | $172kBase band | $2.4M to $21.2MScale band |

| Best fit | Use this to stress-test a slow launch with tight cash and delayed scale. | Use this as the working case for launch-year planning and hiring. | Use this to test upside when repeat investors and larger property tickets start compounding. |

Planning note: Scenario ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions.

Related Products

- Real Estate Crowdfunding Porter's Five Forces Analysis

- Real Estate Crowdfunding BCG Matrix

- Real Estate Crowdfunding Business Model Canvas

- 7 Core Financial KPIs for Real Estate Crowdfunding Platforms

- Real Estate Crowdfunding Business Plan Template in Pre-Written Word

- 7 Strategies to Increase Real Estate Crowdfunding Profitability

- How to Run a Real Estate Crowdfunding Platform Monthly Costs

- Real Estate Crowdfunding Startup Costs: $300k Year 1 Marketing

- Real Estate Crowdfunding Financial Model Template in Excel

- How to Start a Real Estate Crowdfunding Platform in 6 to 12 Months

- How to Write a Real Estate Crowdfunding Business Plan in 7 Steps

- Real Estate Crowdfunding Marketing Mix

- Real Estate Crowdfunding Marketing Plan

- Real Estate Crowdfunding Business Proposal

- Real Estate Crowdfunding PESTEL Analysis

- Real Estate Crowdfunding Pitch Deck Example Editable PPTX

- Real Estate Crowdfunding Business SWOT Analysis

- Real Estate Crowdfunding Value Proposition Canvas

Frequently Asked Questions

The researched base case shows about $172k of first-year pre-tax pay capacity after listed variable costs and $300k marketing, before payroll, software, reserves, debt, and taxes That comes from $530k revenue on $1785M deployed capital At mature-year scale, the same model shows $283M revenue and about $235M before omitted overhead