Owner income$250k

Owner income$250kHow Much Does a Retail Development Owner Make? $250k Salary Case

Fully Editable

Instant Download

Professional Design

Pre-Built

No Expertise Is Needed

Description

Owner income$250k  Net margin-14%

Net margin-14% Revenue for target pay$12.4M

Revenue for target pay$12.4M Business difficultyHard

Business difficultyHard

Key Takeaways

- Larger projects raise upside, but cash gaps widen.

- Occupancy and rent decide recurring cash flow.

- Cost overruns cut owner distributions fast.

- Financing and exit timing shape take-home cash.

Owner income$250kNet margin-14%Revenue for target pay$12.4MBusiness difficultyHardWant to test your owner pay case?

Owner income calculator

Estimate owner take-home and the target-pay gap from revenue, margin, costs, reserves, and target pay.

Planning note: This is a researched planning estimate, not guaranteed salary, tax advice, or owner distribution advice.

Want to check owner income in the Retail Development financial model?

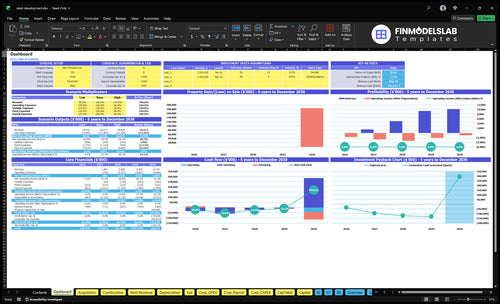

This screenshot shows revenue, margin, costs, reserves, and owner take-home assumptions; open the Retail Development Financial Model Template.

Owner-income model highlights

- Month 29 breakeven

- Month 60 payback

- Cash gap, IRR, ROE

What retail development costs reduce owner income most?

If you’re asking what cuts owner income the most in Retail Development, it’s the big front-end costs: $650 million for owned-site purchase and $525 million for construction, plus tenant improvements and delay risk. See What Is The Estimated Cost To Open And Launch Your Retail Development Business? for the setup math, but the short answer is simple: land, construction, and debt service drain cash fastest. Small overruns matter here, because even a few points of extra cost can hit a very large base.

Main cost drains

- Land: $650 million owned-site purchase

- Construction: $525 million budget

- Delays: tie up cash and push income out

- Debt service: reduces cash left for the owner

Ongoing income hits

- $155,000/month rented-site obligations at full use

- $18,500/month fixed overhead

- Payroll rises from $720,000 to $1.185 million

- Variable expenses fall from 50% to 20% of revenue

How much revenue can a retail development business generate?

Retail Development revenue comes from tenant leases, occupancy, gross leasable area, CAM recoveries, and lease terms, so the top line can swing a lot by asset. Asset rental fees run about $110,000 to $200,000 per month, and the full portfolio gross rental fee totals $1,035 million/month or $1,242 million/year before costs. That’s gross revenue, not owner income, because payroll, fixed overhead, variable expenses, rented-site costs, construction funding, reserves, debt service, and investor obligations come first.

Revenue drivers

- Tenant leases set rent flow.

- Occupancy lifts monthly receipts.

- Gross leasable area expands rent base.

- CAM recoveries add fee revenue.

What cuts cash

- Payroll hits cash first.

- Debt service comes before owner payouts.

- Construction funding uses working capital.

- Reserves reduce distributable income.

How many retail development projects are needed to pay the owner?

Seven projects do not automatically pay the owner in Retail Development. In the source case, a $250,000 CEO/Managing Partner salary starts in Month 1, but EBITDA stays negative every year; breakeven lands in Month 29 and payback in Month 60, so owner pay only works after stabilized rent, debt service, reserves, and investor splits are covered.

Owner pay test

- 7 projects still miss cash cover

- $250,000 salary starts in Month 1

- EBITDA stays negative every year

- Month 29 is breakeven

Cash reality

- Month 60 is payback

- Cover debt service first

- Build reserves before distributions

- Each property must fund overhead

What changes retail development owner income most?

1

-$107.5MDebt Stack

The cash trough hits -$107.547M, so the debt mix decides how much equity you must fund before owner cash turns positive.

2

$117.5MCost Control

Purchase plus construction totals about $117.5M, so any overrun hits take-home before the Month 29 breakeven point.

3

60 moExit Timing

Payback lands at Month 60, so a faster exit or refinance pulls capital back to the owner sooner.

4

$1.035MRent Roll

The seven assets can reach about $1.035M a month in rent, so vacancy moves owner cash fast.

5

5%-2%Lease Terms

Deal pursuit and leasing commissions run 5.0% in Year 1 and drop to 2.0% by Year 5, so stronger lease terms keep more rent after costs.

6

7 assetsProject Size

More sites mean more leasable area, and the 7-asset rollout sets the ceiling for monthly rent and long-term owner income.

Retail Development Core Six Income Drivers

Project Size and Leasable Area

Project Size and Leasable Area

Project size and gross leasable area (GLA) set the ceiling on rent revenue and sale value, but they also raise land, construction, financing, and lease-up risk. In the sample pipeline, construction budgets run from $55 million to $100 million, while owned-site purchase costs range from $120 million to $200 million. Bigger isn’t better unless the space can be leased fast enough.

More leasable square feet can lift top-line rent and terminal value, but it can also widen the cash gap if leases lag spending. The key inputs are GLA, rental fee, occupancy, and tenant mix. Upside rises with scale, but take-home doesn’t follow automatically if the space sits empty.

Size to Signed Demand

Track whether planned GLA matches signed leases, not just site control. Build the pro forma around rent per square foot, occupancy, and tenant mix so you can see how much space the market can actually carry before you spend on concrete.

- Match GLA to preleased space.

- Stress-test lease-up delays.

- Limit size to real tenant demand.

If construction spending rises faster than signed rent, owner distributions slip. The fix is simple: size the project to the lease pipeline, then keep trimming the plan until the rent can support the build.

1

Rent, Occupancy, and Lease-Up

Rent, Occupancy, and Lease-Up

Rent and occupancy are the cash engine here. When an asset leases at $110,000 to $200,000/month, every extra point of occupancy raises recurring rent, improves NOI (net operating income), and can support a better refinance or sale. Track rent per square foot, occupancy, lease-up month, and downtime to see when owner distributions can start.

Lease-up timing matters as much as rent. A slow lease-up keeps carrying costs running and can delay owner pay even if the project is open. If the anchor tenant slips, smaller-shop leasing often slows too, so cash flow can stay below plan longer than the rent roll suggests.

Measure Lease-Up by Month

Build a monthly lease-up model that shows square feet leased, occupied square feet, rent per square foot, and the month each tenant starts paying. Here’s the quick math: more occupied space means more rent, and less downtime means less cash burn. Compare actual leasing speed to plan every month, not just at quarter-end.

Watch the anchor first, then the inline shops. A delayed anchor can push back the whole tenant mix, which delays rent and owner distributions. The disclosed portfolio gross rental fee is $1035 million/month, so even a short vacancy gap can hit cash flow, NOI, and take-home income fast.

- Track monthly occupancy by asset.

- Model downtime for each vacancy.

- Reforecast distributions after delays.

- Test rent sensitivity by square foot.

2

Development Cost Control

Development Cost Control

Cost control decides how much of each deal turns into owner cash. The program has 7 projects, $525 million of construction budget, and $650 million of purchase costs on owned assets. A 5% variance on construction alone is $26.25 million before financing, so land basis, hard costs, soft costs, permitting, tenant improvement allowance, contingency, and change orders all matter.

Delays hurt twice: they add interest, rent carry, and payroll burn. Here’s the quick math: if spending runs late or over budget, cash stays tied up longer and the owner’s distribution gets pushed down, even if the project still looks viable on paper.

Track the budget by cost bucket

Use one live forecast for each bucket: land basis, hard costs, soft costs, permits, TIA, contingency, and change orders. Compare committed cost to budget every week, and approve any change order before it eats contingency. That keeps overruns visible while they’re still small.

Stress-test schedule risk too. If a delay pushes up interest or rent carry, owner cash falls fast. Tight budgets protect distributions, so track variance in dollars and as a percent of the $525 million program, not just at the project level.

3

Tenant Mix and Lease Structure

Tenant Mix and Lease Terms

This driver is the mix of anchor tenant leases and local tenant leases, plus how costs are shared. Strong leases improve rent durability, lender confidence, expense recovery, and exit value. A triple net lease means the tenant pays certain property costs, and common area maintenance reimbursement can reduce the owner’s operating burden and lift net income.

Here’s the quick math: the model tracks rental fees, but not tenant-level terms, so the real inputs are weighted average lease term, credit quality, reimbursement ratio, and renewal risk. Longer terms and better credits usually make NOI more stable, which can support higher refinance proceeds or sale price. If an anchor leaves early, smaller shops can weaken fast.

Track Lease Quality, Not Just Rent

Measure each lease by term, credit, and recovery terms, not just monthly rent. A lease with strong reimbursements and lower renewal risk can be worth more than a higher headline rent with weak support. That matters because owner pay comes from durable NOI, not from one-time top-line spikes.

Use a simple watchlist: weighted average lease term, reimbursement ratio, and any lease expiring in the next 12 months. Also flag the anchor tenant lease first, since one weak renewal can hit traffic, occupancy, and cash flow across the center.

- Check anchor credit before signing.

- Push reimbursement on common costs.

- Stagger expirations to cut renewal risk.

- Document percentage rent upside clearly.

4

Debt, Equity, and Capital Stack

Debt and Equity Waterfall

The capital stack is the order of who gets paid first: lenders, then preferred equity, then the sponsor. In this model, the cash gap is severe, with minimum cash at -$107,547 million in Month 53, so owner pay can stay low even when the project shows profit. That’s why loan-to-cost, interest reserve, and amortization matter as much as project value.

Higher permanent financing rate or a larger investor preferred return can push cash out of the owner’s pocket. The sponsor only sees real take-home after debt service, reserves, and pref are covered, so the same asset can look profitable on paper but still delay distributions. One line says it all: profit is not pay.

Track the Waterfall First

Build the model around the cash waterfall, not just NOI. Track loan-to-cost, interest reserve months, amortization schedule, refinance rate, pref return, and sponsor promote so you can see when cash reaches equity. If debt service or reserves rise, owner draw falls fast.

- Test debt at different rates.

- Watch preferred return accrual.

- Model Month 53 cash lows.

- Check promote timing before draws.

Use the waterfall to answer one question: after lenders and investors are paid, what cash is left for the owner? If the answer stays thin, improve terms, slow leverage, or reset the equity split before distributions start.

5

Exit, Refinance, and Hold Period

Exit Timing

Exit timing drives whether owner pay comes from a sale, a refinance, or just salary. In this model, the sale date is Month 60 for all seven projects, and payback also lands in Month 60. That means income is lumpy, not steady. A strong exit can create a big cash spike, but weak timing can leave the owner waiting on distributions.

The key inputs are stabilized NOI, cap rate (NOI ÷ property value), debt balance, equity ownership, closing costs, and reserves. If NOI is stable and debt is lower by Month 60, the owner keeps more of the sale or refinance proceeds; if not, the take-home check shrinks fast.

Track the Month 60 Cash Event

Measure exit value against the debt paydown path, not just the headline sale price. One clean rule: if the cap rate is weak or NOI is still moving, delay the capital event unless carry costs are hurting more than the upside helps.

- Track stabilized NOI each month.

- Watch debt balance and reserves.

- Model closing costs before payback.

- Test sale and refinance timing.

- Check equity split before exit.

Here’s the quick math: owner proceeds = value at exit - debt balance - closing costs - reserves, then split by equity. If Month 60 is too early, the owner may still get salary only and see delayed distributions instead of a real payout.

6

Compare low, base, and high owner-income outcomes

Owner income scenarios

Retail development is cash-intensive and timing-sensitive, so owner income moves with lease-up, build costs, and capital events. Early years may support salary before any distributions.

| Scenario | LowCash tight | BaseModeled case | HighUpside case |

|---|---|---|---|

| Launch model | Income stays near the owner salary line because lease-up is slow and distributions are deferred. | Income follows the modeled operating case, with owner pay supported but distributions still limited. | Income improves only if occupancy ramps faster and a refinance or sale creates distributable cash. |

| Typical setup | Higher construction costs, slower occupancy, and rent roll-up delays keep cash tied up longer. | Seven assets reach the modeled $1.035 million monthly gross rental fee, but EBITDA stays negative each year and payback lands at Month 60. | Faster lease-up, tighter construction control, and better exit timing create room for owner distributions after debt, reserves, and partner terms. |

| Cost drivers |

|

|

|

| Owner income rangeBefore owner reserves | $250,000 salary onlySalary only | $250,000 salaryNo draw yet | $250,000 salary plus distributionsCapital upside |

| Best fit | Use this to stress-test a delayed start and a no-distribution year. | Use this as the core planning case for lender, partner, and reserve work. | Use this to test the best realistic outcome after capital events, not as guaranteed pay. |

Planning note: These scenario ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions.

Related Products

- Retail Development Porter's Five Forces Analysis

- Retail Development BCG Matrix

- Retail Development Business Model Canvas

- 7 Essential KPIs for Retail Development Success

- Retail Development Business Plan Template in Pre-Written Word

- 7 Strategies to Increase Retail Development Profitability

- How to Manage the Monthly Running Costs of Retail Development

- Retail Development Startup Costs: $23M First Project Plus $150K Setup

- Retail Development Financial Model Template in Excel

- How To Open A Retail Development Company: 60-Month Launch Path

- How to Write a Retail Development Business Plan in 7 Steps

- Retail Development Marketing Mix

- Retail Development Marketing Plan

- Retail Development Business Proposal

- Retail Development PESTEL Analysis

- Retail Development Pitch Deck Example Editable PPTX

- Retail Development Business SWOT Analysis

- Retail Development Value Proposition Canvas

Frequently Asked Questions

In this case, the modeled owner role pays $250,000 per year as CEO / Managing Partner That is salary, not proof of distributable profit EBITDA is negative from Year 1 through Year 5, minimum cash reaches -$107547 million, and payback occurs in Month 60, so extra owner income depends on funding, refinancing, sale proceeds, and investor terms