Owner income$180k+

Owner income$180k+How Much Can A Returns Processing Service Owner Make? Year 1 EBITDA $317k

Fully Editable

Instant Download

Professional Design

Pre-Built

No Expertise Is Needed

Description

Owner income$180k+  Net margin15% to 58%

Net margin15% to 58% Revenue for target pay$1.2M

Revenue for target pay$1.2M Business difficultyHard

Business difficultyHard

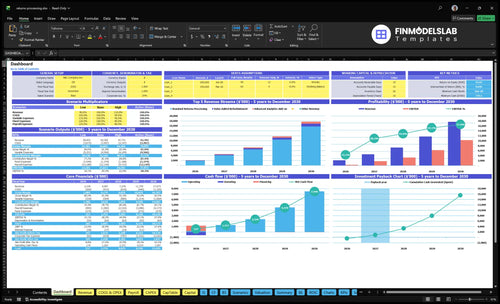

A returns processing service owner can model take-home as a $180k CEO salary plus any distributions the business can support after reserves, debt service, and reinvestment In the researched base case, revenue grows from $2104M in Year 1 to $17673M in Year 5, while EBITDA rises from $317k to $10239M EBITDA margin moves from about 151% in Year 1 to 579% in Year 5 as fixed warehouse costs and software are spread across more retailer volume The model reaches breakeven in Month 6, needs $135k of minimum cash, and pays back in 18 months

Owner income$180k+Net margin15% to 58%Revenue for target pay$1.2MBusiness difficultyHardWant to calculate owner pay from returns volume?

Owner income calculator

Estimate owner take-home and target-pay gap for a returns processing service from revenue, margin, costs, reserves, and target pay.

Planning note: Research-based planning estimate only; it is not guaranteed salary, tax advice, or owner distribution advice.

Want to check owner income in the Returns Processing Service model?

The Returns Processing Service Financial Model Template shows revenue, EBITDA, cash, payback, and owner income; charts run revenue from $2.104M to $17.673M and EBITDA from $317k to $10.239M, with breakeven in Month 6, payback in 18 months, and $135k minimum cash, so the bridge stays secondary to income planning.

Owner-income model highlights

- Owner income stays visible

- Revenue reaches $17.673M

- EBITDA spans $317k-$10.239M

- Breakeven hits Month 6

- Cash floor is $135k

How much revenue can a returns processing service make per retailer?

A Returns Processing Service can make about $2,805 a month per active retailer in Year 1, and about $3,710 by Year 5, before costs. The base is $2,500 a month for standard processing, with add-ons like $500 analytics and $1,200 refurbishment lifting the average. Gross revenue is not owner pay, because labor, packaging, cloud, rent, payroll, and reserves come out next.

Year 1 revenue per retailer

- $2,500 monthly standard processing

- $500 analytics add-on

- $1,200 refurbishment add-on

- Weighted Year 1: about $2,805/month

Year 5 weighted revenue

- $2,900 standard processing

- 650% × $600 analytics

- 300% × $1,400 refurbishment

- Weighted Year 5: about $3,710/month

Can a returns processing service owner pay themselves?

Yes — the Returns Processing Service can pay the owner, and the model already includes a $180k CEO salary from Month 1 through Month 60. Here’s the quick math: Year 1 EBITDA is $317k after that salary, so owner pay is already inside payroll if cash stays healthy. If you defer pay, early cash gets better, but the workload and risk sit on you instead.

Cash check

- $180k CEO pay is modeled in.

- $317k Year 1 EBITDA remains.

- Pay stays inside payroll, not outside it.

- Deferred pay lifts early cash only.

Staffing tradeoff

- 4 inspection specialists support volume.

- 1 warehouse operations manager adds control.

- Support staff helps service quality.

- Scale lowers take-home, but protects growth.

What profit margin does a returns processing service make?

A Returns Processing Service can post a high gross margin because it earns on processing while direct costs stay tight; the model points to about 74.0% gross margin on $2.104M revenue, and this How Increase Returns Processing Service Profits? link matters because speed only helps if quality stays high. After payroll, marketing, rent, insurance, utilities, software, maintenance, legal, and accounting, EBITDA margin drops to 15.1%, then improves to 57.9% by Year 5 at $17.673M revenue.

Year 1 margin

- Gross margin = revenue minus direct costs

- Direct costs include 95% packaging

- Cloud and data run at 80%

- Inspection payroll is $180k

Profit pressure

- 15.1% EBITDA in Year 1

- 57.9% EBITDA by Year 5

- Slow inspections cut take-home fast

- Rework and idle space hurt margins

Want to see what drives owner income?

1

$317K-$10.2MReturn Volume

More recurring retailer returns drive the model's EBITDA from Year 1 to Year 5, and they spread fixed costs across more jobs.

2

$2.5K-$2.9KPrice Floors

Higher standard fees and account minimums lift margin on every retailer and protect income when volume is uneven.

3

$229K/moWarehouse Utilization

Keeping the warehouse full turns monthly overhead into profit instead of idle cost, which is key in a fixed-heavy model.

4

4-25 FTELabor Productivity

Each return should take less inspection labor over time, or wage growth will eat the EBITDA gain from higher volume.

5

$500-$1.4KAdd-on Mix

More analytics and refurbishment work raises revenue per account without adding the same overhead as core processing.

6

23% ROESLA Quality

Accurate inspections and on-time service keep retailers renewing, which protects the modeled owner return.

Returns Processing Service Core Six Income Drivers

Recurring Retailer Return Volume

Recurring Return Volume

When monthly return volume is steady, the service can spread rent, software, utilities, insurance, and management payroll across more work. The model shows revenue rising from $2.104M in Year 1 to $17.673M in Year 5, while implied active account revenue moves from about $2,805 to $3,710 per month. That steadier base is what supports steadier owner pay.

The main risk is concentration. One large retailer can make income look strong, then churn can hit cash flow hard. Track monthly returns processed, active retailer accounts, average client revenue, client concentration, and utilization, meaning how much of warehouse and labor capacity is used. Keep volume high enough to cover fixed costs even when one account slows.

Track Volume, Not Just Revenue

Measure returns by account each month and map each client’s share of total revenue. If one account drives too much of the base, the owner’s draw becomes fragile. A broader book of recurring retailers makes the cost base easier to absorb and keeps profit less jumpy.

Use monthly forecasts with churn scenarios, not just booked revenue. If volume falls, idle labor and overhead hit margin first, then owner pay. If volume rises, each extra return helps cover the same fixed cost pool, so take-home income gets more predictable.

- Track monthly returns by client

- Watch top-customer revenue share

- Forecast churn and idle capacity

1

Pricing And Account Minimums

Account Minimums and Service Pricing

When returns volume is uneven, a monthly account minimum or per-return floor is what protects owner pay. Base pricing starts at $2,500 in Year 1 and rises to $2,900 by Year 5; analytics add-ons run $500-$600, and refurbishment runs $1,200-$1,400. If a client needs high-touch inspections or custom workflows, the fee has to cover that labor, or margin gets squeezed fast.

Here’s the quick math: revenue depends on service scope, return count, add-on mix, and the time spent on exception handling. A clean minimum keeps idle labor and admin time from eating gross margin, so more of each client dollar can flow to rent, payroll, and owner draw. Without that floor, one small or messy account can look active but still pay like a loss leader.

Price the floor, then price the extras

Track standard price, minimum fee, add-on attach rate, and labor minutes per account. If the team spends more time on inspections, grading, or retailer-specific steps than the fee assumes, raise the minimum or narrow scope before margins slip.

Watch the mix by client type: simple accounts, heavy exception accounts, and add-on heavy accounts. The goal is simple: make sure every active account covers its own work plus a share of fixed overhead, so owner take-home stays steadier even when returns volume dips.

- Minimum fee covers idle time.

- Add-ons fund extra labor.

- Scope limits protect margin.

2

Labor Productivity And Inspection Speed

Inspection Speed and Labor Cost

This driver is the time and error rate inside inspection. If each return takes more minutes, labor cost per return rises and gross margin drops before rent and admin. The model starts with 4 inspection specialists at $45k in Year 1, then scales to 25 by Year 5; direct inspection payroll is $180k in Year 1 and $1125M in Year 5.

Estimate it from labor minutes per return, units processed per hour, inspection specialist FTE, rework rate, and quality pass rate. Quick math: labor cost per return = inspection payroll ÷ returns processed. A small rise in minutes per return can force earlier hiring, which lifts cash needs and cuts the owner’s take-home income faster.

Track Minutes Before You Add Headcount

Track minutes per return by product type and by inspector. Keep a tight watch on rework hours, credits, and SLA misses; SLA means service-level agreement, the promised speed and accuracy in the contract. If speed improves but the pass rate slips, the extra labor and lost clients can wipe out the gain.

Use weekly capacity checks: units per hour, queue size, and the next FTE need. Test standard work, photo checklists, and exception routing before you hire. One slow workflow can drive the whole labor model, so fix that step first or payroll will climb ahead of revenue and squeeze owner pay.

3

Value-Added Returns Processing Services

Value-Added Add-Ons

Value-added returns processing services lift owner income only when the add-on price clears the extra labor and materials. In this model, analytics adoption moves from 250% to 650% and refurbishment from 150% to 300%, pushing weighted account revenue from about $2,805 per month in Year 1 to $3,710 by Year 5.

Here’s the catch: refurbishment can add storage time, exception handling, and rework. If those hours or materials rise faster than the add-on fee, gross margin drops and owner pay gets squeezed even when revenue per account looks better.

Price the Work Above the True Cost

Track add-on revenue, added labor time, and materials cost by service line. The owner should know the break-even point for analytics and refurbishment before offering them, because the extra revenue only helps if each task stays profitable after labor, storage, and consumables.

Use clear minimums and scope rules. A simple one-liner works: more service, more fee. Test whether analytics and refurbishment are priced high enough to cover the extra minutes, then watch margin by account so one complex client does not erase the gain.

- Track labor minutes per add-on

- Track materials per return

- Track storage days on refurb items

- Track revenue per active account

4

Warehouse Utilization And Fixed Overhead

Warehouse Utilization

This driver is about how many processed returns you push through the warehouse each month. When you spread $229k of fixed overhead, including $12k rent, $35k software, $25k legal and accounting, $22k utilities, $15k insurance, and $12k maintenance, across more work, owner income rises because each return carries less overhead.

The key inputs are processed returns, occupied capacity, rent per processed return, seasonal overflow, and idle space risk. Holiday spikes can force extra space and labor, so a warehouse that looks fine on average can still leak cash in peak months if capacity is too tight.

Track Capacity, Not Just Revenue

Measure returns per month against usable warehouse slots, then watch rent per processed return. The model says EBITDA margin expands from 151% in Year 1 to 579% in Year 5 as utilization rises, so every extra batch should lower overhead per return and lift owner pay.

- Track occupied capacity weekly.

- Price for overflow space early.

- Separate peak-month labor costs.

What this estimate hides: holiday overflow can add temporary labor and storage costs, so keep a separate peak forecast instead of averaging the year.

5

Accuracy, Rework, And SLA Performance

Accuracy, Rework, And SLA Performance

When returns get mis-sorted, reworked, or shipped late, margin leaks fast. Track mis-sort rate, rework hours, shrinkage, credits, SLA misses, and client churn. With Year 1 direct inspection payroll at $180k for 4 specialists, even small error creep adds cost to a fixed labor base and can cut owner take-home.

SLA means service-level agreement, the promised speed and accuracy level in a retailer contract. This model does not show penalty rates, so treat late fills, credits, and reserve needs as editable cost inputs. Fewer mistakes keep EBITDA available for reinvestment and possible distributions; more mistakes create disputes, lost accounts, and slower cash conversion.

Track errors before they hit profit

Measure accuracy by client, SKU, and workflow step, not just in total. Track mis-sorts per 1,000 returns, rework hours, credit dollars, and SLA miss count each week. That shows which account is burning labor and which process step is breaking.

Set a clear pass-fail check at intake and before restock. If one workflow keeps creating exceptions, fix the steps or price the account higher. The goal is simple: protect gross margin, keep retention steady, and stop avoidable rework from cutting owner pay.

6

Owner income scenario table objective

Owner income scenarios

Owner income changes fast here because EBITDA swings with client volume, add-on mix, and staffing scale. EBITDA is a planning signal, not automatic take-home pay.

| Scenario | Low CaseLow Case | Base CaseBase Case | High CaseHigh Case |

|---|---|---|---|

| Launch model | The low case keeps owner income near the first-year operating level. | The base case reflects a more mature operating run with stronger owner income capacity. | The high case shows the stronger owner income path if the business scales into Year 5. |

| Typical setup | Revenue holds near Year 1 at $2.104 million, EBITDA is about $317k, the CEO stays hands-on, and the model needs the $135k minimum cash buffer through Month 6 break-even. | Revenue reaches about $7.278 million in Year 3, EBITDA is about $3.265 million, add-on adoption improves, and the team is larger across operations, sales, and account management. | Revenue reaches about $17.673 million in Year 5, EBITDA is about $10.239 million, the client base is larger, and add-on mix is stronger while staffing and support costs keep rising. |

| Cost drivers |

|

|

|

| Owner income rangeBefore owner reserves | $317k EBITDADownside case | $3.265M EBITDACore case | $10.239M EBITDAUpside case |

| Best fit | Use this as a hard cash test when sales stay near Year 1 and owner draws must stay limited. | Use this as the middle case once the owner shifts from daily ops to oversight and the business clears early setup risk. | Use this to test upside if acquisition stays efficient, operations keep pace, and the owner can fund growth without stressing cash. |

Planning note: These scenario ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions; EBITDA is not automatic owner take-home.

Related Products

- Returns Processing Service Porter's Five Forces Analysis

- Returns Processing Service BCG Matrix

- Returns Processing Service Business Model Canvas

- What Are The 5 KPIs For Returns Processing Service Business?

- Returns Processing Service Business Plan Template in Pre-Written Word

- How Increase Returns Processing Service Profits?

- What Are Operating Costs For Returns Processing Service?

- How Much It Costs To Start A Returns Processing Service: $755k+

- Returns Processing Service Financial Model Template in Excel

- How To Open A Returns Processing Service In 8 To 16 Weeks

- How Do I Write A Business Plan For Returns Processing Service?

- Returns Processing Service Marketing Mix

- Returns Processing Service Marketing Plan

- Returns Processing Service Business Proposal

- Returns Processing Service PESTEL Analysis

- Returns Processing Service Pitch Deck Example Editable PPTX

- Returns Processing Service Business SWOT Analysis

- Returns Processing Service Value Proposition Canvas

Frequently Asked Questions

The researched model shows $2104M of Year 1 revenue and $317k of EBITDA after a $180k CEO salary By Year 5, revenue reaches $17673M and EBITDA reaches $10239M Owner take-home depends on whether profit is kept for reserves, debt service, capex, or distributions