Owner income$1.35M

Owner income$1.35MHow Much Can a Royalty Management Service Owner Make? Year 1 Math

Fully Editable

Instant Download

Professional Design

Pre-Built

No Expertise Is Needed

Description

Owner income$1.35M  Net margin31.6%

Net margin31.6% Revenue for target pay$4.26M

Revenue for target pay$4.26M Business difficultyMedium

Business difficultyMedium

You’re pricing a royalty management service before you know the real workload, so owner income has to start with accounts, fees, transaction volume, and reserves In the Year 1 planning case, the revenue-side assumptions support 10,000 sellers, 2,400 buyers, about $595M in annual revenue, and $105M in marketing spend Owner take-home is what remains after labor, software, payment costs, compliance, taxes, reserves, and reinvestment

Owner income$1.35MNet margin31.6%Revenue for target pay$4.26MBusiness difficultyMediumWant to test your owner take-home?

Owner income calculator

Estimate owner take-home and target-pay gap from revenue, margin, costs, reserves, and target pay.

Planning note: Research-based planning estimate only. Actual owner income depends on revenue, margins, staffing, taxes, reserves, and distribution policy. It is not guaranteed salary, tax advice, or owner distribution advice.

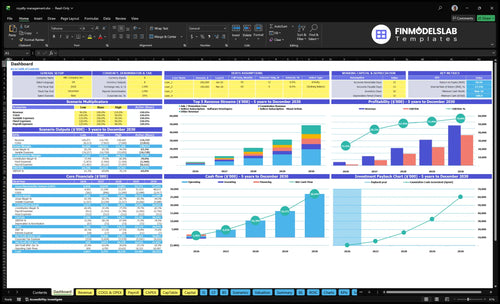

How does owner income look in the Royalty Management Service financial model?

This screenshot shows revenue, margin, costs, reserves, and owner take-home assumptions; open the Royalty Management Service Financial Model Template.

Owner-income model highlights

- Dashboard to owner pay

- 12,400 accounts Year 1 test

- $595M revenue scenario case

- $105M marketing stress test

- ~$376k commissions output

- Charts and tables for income

What are the biggest costs in a royalty management service?

The biggest cost in a Royalty Management Service is customer acquisition, not the software itself. In Year 1, marketing is $450k for sellers and $600k for buyers, with CAC at $45 per seller and $250 per buyer; see How Increase Royalty Management Service Profits? for the margin side of that math. The other big costs are analyst labor, statement reconciliation, payment processing, royalty software, data security, professional services, insurance, client support, and dispute reserves, and the reserve logic matters because payment errors and rights-holder disputes can eat cash before owner distributions.

Visible cost drivers

- $450k seller marketing

- $600k buyer marketing

- $45 seller CAC

- $250 buyer CAC

Cash drains to plan for

- Analyst labor and reconciliation

- Payment processing and software

- Security, legal, and insurance

- Client support and dispute reserves

Can a royalty management service scale profitably?

Yes—Royalty Management Service can scale profitably if recurring fees grow faster than reconciliation labor, support time, and compliance controls. In Year 5, the model assumes 40,000 sellers and 10,000 buyers from $35M in total marketing, with revenue at about $3,810M before operating costs scale up. As the founder stops doing reconciliations personally and hires analysts, account managers, and compliance support, workload falls but payroll and quality control costs rise. Faster distributions help, but only if accuracy and dispute controls stay tight.

Scale drivers

- 40,000 sellers in Year 5

- 10,000 buyers in Year 5

- $35M total marketing spend

- Recurring fees must outgrow labor

Profitability risks

- Founder hands off reconciliations

- Analysts and support add payroll

- Quality control costs rise

- Dispute accuracy must stay high

How many clients does a royalty management service need to be profitable?

A Royalty Management Service needs about 2,200 blended active accounts just to cover $875k/month in marketing, but true profitability needs more once labor, software, payment costs, taxes, and reserves are included; track the operating gap with What Are The 5 KPIs For Royalty Management Service Business?. Year 1 assumes 12,400 acquired accounts from $105M total marketing, split into 10,000 sellers and 2,400 buyers, producing about $496k/month in blended revenue.

Profit drivers

- Price per seller and buyer

- Commission per royalty transaction

- Analyst workload per account

- Reserve policy for disputes

Key caveats

- 2,200 accounts cover marketing only

- Labor can delay break-even

- Bad metadata raises support cost

- Clean usage data protects margin

Want the six main income drivers?

1

$4.3MClient Volume

More active accounts drive the top line fastest; Year 1 already models 12,400 accounts.

2

$15.49/$129Pricing Mix

A richer seller-buyer mix lifts subscription revenue because buyer fees are much higher than seller fees.

3

$5+12%Royalty Complexity

Higher order value and more complex splits raise commission revenue without adding many new clients.

4

3.5xReconcile Speed

Cleaner workflows let one team handle more repeat orders, which protects margin as volume grows.

5

15%Infra Cost

Gateway, DRM, cloud, and support costs take a direct bite out of every dollar collected.

6

$1.1MStaffing Load

Keeping the owner out of low-value admin and matching hires to volume keeps fixed payroll from swallowing cash.

Royalty Management Service Core Six Income Drivers

Managed client volume

Managed Client Volume

More managed royalty clients and catalogs can lift recurring revenue, but only if onboarding, reporting, and support keep pace. Year 1 source volume is 10,000 sellers and 2,400 buyers, with sellers split 60% independent musicians, 30% visual artists, and 10% software developers. The buyer mix is 50% ad agencies, 40% content producers, and 10% app developers.

One clean rule: volume helps only when service work grows slower than revenue. If more accounts cause statement errors, support tickets, or payment delays, margin and cash flow drop fast, and owner pay gets squeezed. The key test is whether recurring income rises without a matching jump in labor.

Track Load Before You Add Accounts

Measure the inputs that drive this line: active sellers, active buyers, catalog count, onboarding time, reporting cadence, ticket volume, and days to distribution. If statements per analyst or support hours per account climb faster than revenue, the business is growing the hard way. Source data gives the mix, but not labor cost, so model staffing with editable hourly and headcount fields.

- Track accounts per ops staff.

- Watch error rate weekly.

- Flag payout delays fast.

- Pause growth when tickets spike.

Keep onboarding standardized and reporting automated so each added client adds more revenue than cost. That is where owner take-home improves: volume rises, but payroll and correction work do not rise at the same pace.

1

Pricing model and revenue per account

Revenue per account

Royalty management income rises when the fee matches the work in each account. Here, seller pricing runs from $999 to $4,999 a month, with a $1,549 weighted average, while buyer pricing runs from $49 to $199 a month, with a $129 weighted average. Commission adds $5 per order plus 12% of order value, so revenue per account improves when reporting is frequent and splits are hard.

What this estimate hides is retention risk. If higher fees do not come with cleaner reports or faster payments, clients can push back or leave. The key inputs are reporting frequency, stakeholder count, data cleanup, and reconciliation difficulty. One clean rule: price the pain, not the login.

Track pricing against service load

Measure net revenue per account by tier, then compare it with support time, correction work, and payment delays. Raise fees only after the client sees a real gain, like cleaner statements or faster distributions. If you do not segment by account complexity, the weighted averages of $1,549 seller and $129 buyer fees can look fine while margin quietly slips.

- Track revenue by seller and buyer tier.

- Watch churn after price changes.

- Test fees by reporting frequency.

- Flag messy accounts before renewal.

2

Royalty transaction complexity

Royalty transaction complexity

More transactions can lift revenue, but only if the added review work stays priced in. With 4,032 orders from 2,400 buyers, the Year 1 commission math is about $376k using a $5 fixed fee plus 12% of order value. Inputs that matter here are order count, average order value, split count, rights holders, and how often statements and payments run.

This driver raises take-home income only when the extra margin beats the extra labor. Complex splits, messy statements, and frequent payment cycles push more manual review, which raises labor hours and error risk. If the team spends more time fixing statements than the platform earns from the transaction, owner pay gets squeezed even when top-line revenue looks stronger.

Price for the review load

Track orders per month, review hours per order, error rate, and rework time. Those four numbers tell you whether complexity is profitable or just busywork. A clean rule: if a client’s split structure or payment cycle adds more support time, the fee should rise with it. Otherwise, the business is subsidizing complexity with founder time.

Use a simple test on each account: commission revenue minus extra labor cost. If that spread turns thin, cap the number of rights holders, tighten reporting formats, or charge for higher-touch reconciliation. The goal is not fewer complex deals; it is making sure the extra work is paid for before it reaches payroll and owner draw.

3

Automation and labor efficiency

Automation that cuts analyst time

Automation raises owner income when statement imports, split math, and approvals need fewer manual touches. With 4,032 orders in Year 1, rework and bottlenecks can eat margin fast, so the real gain is more statements processed per labor hour and fewer payment delays.

Track analyst hours per account, statements processed per labor hour, correction rate, and days to distribution. No direct labor cost is given, so the model should use editable hourly cost and staffing fields. Better workflow lifts gross margin before overhead, which is what funds owner pay.

Measure the work, not just the software

Use standardized onboarding, automated statement imports, exception queues, reusable reports, and approval workflows. One clean target: cut manual corrections first, then reduce analyst hours. If the team can process more statements per labor hour, owner income rises even before revenue grows, because the same labor base supports more accounts.

Build the forecast around accounts, statement volume, hourly pay, and headcount. Also test whether complex splits or messy statements push up review time. If days to distribution slip, cash gets trapped and client trust drops, so automation should protect both margin and retention.

- Hours per account

- Corrections per statement

- Statements per labor hour

- Days to distribution

4

Software, payment, security, and compliance costs

Software and payment overhead

This cost bucket covers software licenses, payment rails, secure storage, insurance, legal or accounting support, audit controls, and dispute handling. It protects accuracy and trust, but every unpaid dollar cuts owner take-home. At 4,032 orders, a $0.30 processing fee alone is $1,209.60, before the rest of the stack.

The key test is simple: if infrastructure spend rises faster than order volume, net profit falls even when revenue grows. That matters most when complex splits or payment delays trigger more support and exception work. Underpriced compliance does not show up in gross sales, but it does show up in lower distributions and a smaller owner draw.

Price the stack into every deal

Track cost per transaction and cost per managed account. Start with software, secure storage, insurance, legal/accounting support, and dispute handling, then divide by orders and clients. If a deal does not cover the $0.30 payment fee plus your fixed stack, raise the retainer or add a transaction-fee floor.

- Orders per month

- Average order value

- Support and dispute hours

- Monthly software and storage spend

- Insurance and legal fees

- Payment fee per transaction

The model’s annual marketing costs also run from $105M in Year 1 to $35M in Year 5, so this stack has to be protected before other fixed spend eats cash. Keep exception work billed and visible, or it quietly shrinks owner pay.

5

Owner role and staffing

Owner role and staffing

If you do every reconciliation check, meaning you match usage, splits, and payouts, plus all client service yourself, owner income can look highest on paper. But that only works until your owner hours hit the wall, so revenue stops growing with demand and burnout risk climbs.

Hiring analysts and account managers lowers your workload, but it adds payroll before any distributions. The clean model is: pay a fair owner salary first, cover staffed service costs next, then treat the rest as economic profit and year-end distribution after the reserve percentage is set aside.

Track payroll before owner pay

Build the forecast with four inputs: owner hours, analyst headcount, account manager load, and reserve percentage. That shows whether staffing supports quality or just eats contribution. One clean rule: if service quality rises but payroll swallows margin, take-home is weaker, not stronger.

- Track hours per client each month

- Set salary before distributions

- Watch reserve cash after payroll

- Cap load before errors rise

Here’s the quick math: owner-led service can maximize cash in the short run, but it also caps capacity. Add staff only when the extra payroll is smaller than the margin created by more accounts, fewer errors, and faster payouts. That’s what makes take-home durable.

6

Compare lean, base, and high-scale owner-income cases

Owner income cases

Income swings with seller volume, buyer demand, and commission mix, while fixed legal, software, and support costs stay heavy. These three cases show how much the owner can keep after operating costs.

| Scenario | Low CaseLean case | Base CaseModeled case | High CaseUpside case |

|---|---|---|---|

| Launch model | This is the lower earnings path if volume lands at about half of Year 1 active demand. | This is the modeled middle path using Year 1 acquisition assumptions and the full operating cost stack. | This is the stronger earnings path if the model reaches Year 5 volume, repeat orders, and the highest commission mix. |

| Typical setup | Lean launch with about 5,000 sellers and 1,200 buyers, plus the fixed legal, software, and support stack still running. | Year 1 setup with 10,000 sellers and 2,400 buyers, a balanced mix across musicians, artists, and developers, and the core team in place. | Mature Year 5 setup with 40,000 sellers and 10,000 buyers, higher software-developer mix, more repeat orders, and the largest support and compliance load. |

| Cost drivers |

|

|

|

| Owner income rangeBefore owner reserves | $0.7M - $1.3MDownside range | $1.3M - $6.6MCore range | $22.2M - $36.9MUpside range |

| Best fit | Use this to stress-test cash and owner draw if growth starts slow or churn stays high. | Use this as the main planning case for budgeting, hiring, and owner payout decisions. | Use this to test upside if acquisition stays efficient and the platform keeps compounding. |

Planning note: Scenario ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions.

Related Products

- Royalty Management Service Porter's Five Forces Analysis

- Royalty Management Service BCG Matrix

- Royalty Management Service Business Model Canvas

- What Are The 5 KPIs For Royalty Management Service Business?

- Royalty Management Service Business Plan Template in Pre-Written Word

- How Increase Royalty Management Service Profits?

- What Are Operating Costs For Royalty Management Service?

- How Much Does It Cost To Start A Royalty Management Service? $26K/Month Base

- Royalty Management Service Financial Model Template in Excel

- How to Start a Royalty Management Service in 8-16 Weeks

- How Do I Write A Business Plan For Royalty Management Service?

- Royalty Management Service Marketing Mix

- Royalty Management Service Marketing Plan

- Royalty Management Service Business Proposal

- Royalty Management Service PESTEL Analysis

- Royalty Management Service Pitch Deck Example Editable PPTX

- Royalty Management Service Business SWOT Analysis

- Royalty Management Service Value Proposition Canvas

Frequently Asked Questions

Owner take-home depends on costs, not just revenue The Year 1 assumptions support about $595M in revenue from 10,000 sellers, 2,400 buyers, and about $376k in commissions That cash must still cover labor, software, payment processing, compliance, insurance, taxes, reserves, and reinvestment before the owner takes distributions