Owner income$149k–$3.8M

Owner income$149k–$3.8MHow Much Secretarial Services Owners Make: $95k Pay Plus Profit

Fully Editable

Instant Download

Professional Design

Pre-Built

No Expertise Is Needed

Description

Owner income$149k–$3.8M  Net margin9%–56%

Net margin9%–56% Revenue for target pay$1.6M

Revenue for target pay$1.6M Business difficultyMedium

Business difficultyMedium

A secretarial services business owner can plan around a $95k general manager salary in this model, plus possible profit distributions if cash allows The researched assumptions show revenue rising from $591k in Year 1 to $6591M in Year 5, with EBITDA moving from $54k to $3658M That means EBITDA margin improves from about 91% to 555%, but EBITDA is not the same as owner pay Owner income depends on retainers, billable capacity, payroll, marketing, software, contractor use, and reserves

Owner income$149k–$3.8MNet margin9%–56%Revenue for target pay$1.6MBusiness difficultyMediumWant to test your owner pay?

Owner income calculator

Estimate owner take-home and the gap to your target pay from revenue, margin, costs, reserves, and target pay.

Planning note: This is a researched planning estimate, not guaranteed salary, tax advice, or owner distribution advice. It does not include personal living expenses.

Want to check owner income in Secretarial Services?

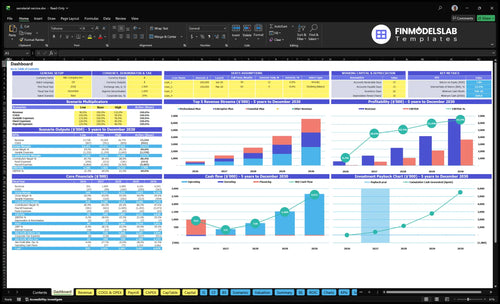

Yes—open the Secretarial Services Financial Model Template dashboard to see revenue, EBITDA, margin, minimum cash, breakeven, payback, $591k revenue, $54k EBITDA.

Owner-income model highlights

- GM pay: $95k

- Revenue: $591k Year 1

- Minimum cash: $830k

- Breakeven: Month 7

- Payback: 16 months

- Flex retainers and staffing

How much revenue is needed to pay myself?

For Secretarial Services, the revenue needed to pay yourself depends on whether you take a salary or a profit distribution, plus overhead and reserve rules. In the source model, $591k of Year 1 revenue supports a $95k general manager salary and $54k EBITDA before taxes and reserves. For profit-only pay, use target EBITDA ÷ EBITDA margin; at 91%, a $100k profit pool needs about $110k revenue, and don’t drain the $830k minimum cash need.

Salary route

- $591k revenue supports $95k pay

- $54k EBITDA stays before reserves

- 91% EBITDA margin in Year 1

- Salary depends on payroll load

Profit route

- Use EBITDA ÷ margin for pay

- $100k profit needs about $110k revenue

- 386% Year 2 margin lifts room

- 435% Year 3 margin lifts room

Can a secretarial services business scale beyond the owner?

Yes—but Secretarial Services only scales if the owner shifts from doing admin work to managing clients, staff, quality, and capacity. In the model, virtual assistant leads grow from 2 in Year 1 to 18 in Year 5, and account managers rise from 1 to 6, so growth depends on systems, not the founder’s personal typing speed. The quick rule is simple: retainer prices, utilization, and quality control must cover payroll, or the model gets crushed by rework, churn, and unpaid support.

What makes it scale

- 2 leads in Year 1 become 18 by Year 5.

- Owner moves into client and staff management.

- Retainers must fund payroll growth.

- Utilization has to stay high.

What breaks it

- Contractor rework eats margin.

- Client churn slows recurring revenue.

- Unlimited support turns into unpaid labor.

- Quality slips as headcount rises.

What profit margin can secretarial services earn?

Secretarial Services can earn a very high EBITDA margin, rising from 91% in Year 1 to 555% by Year 5 as revenue scales faster than costs. The early drag is payroll, since admin work needs people, and the main cost load also includes 80% cloud infrastructure in Year 1, 35% payment fees, $355k fixed monthly overhead, and $45k marketing. For the margin levers, see How Increase Secretarial Services Profits?

Main cost drivers

- Payroll is the biggest early drag.

- 80% cloud cost in Year 1.

- 35% payment fees hit each sale.

- $355k fixed overhead stays high.

Margin moves

- CAC falls from $450 to $350.

- Retention has to hold.

- Rework cuts margin fast.

- Poor scope control hurts take-home.

What drives owner income most?

1

$600-$2KPricing Mix

Year 1 starts with 50% Essential at $600, 35% Professional at $1,100, and 15% Enterprise at $2,000, so lifting mix toward higher plans is the fastest way to raise owner take-home.

2

9.1%Billable Utilization

Year 1 EBITDA is $54K on $591K revenue, so idle admin time quickly squeezes the 9.1% margin; keep calendars full and work standardized.

3

$3.6KOverhead Discipline

Fixed expenses run $3.6K a month and Year 1 payroll is $330K, so lean tools and tight back office costs protect cash.

4

$450Client Retention

Year 1 CAC is $450, so churn forces you to buy the same revenue again; faster response times and clean handoffs keep income sticky.

5

$1.4MRecurring Retainers

Revenue rises from $591K in Year 1 to $1.4M in Year 2, and repeat contracts are the cleanest way to smooth that jump for the owner.

6

2-18xSubcontractor Leverage

The Virtual Assistant Lead scales from 2.0 FTE in Year 1 to 18.0 FTE in Year 5, so subcontractors can add capacity without matching payroll one for one.

Secretarial Services Core Six Income Drivers

Pricing and Service Mix

Pricing and Service Mix

This driver is about charging more for fast-response scheduling, executive admin, document prep, and recurring support, then moving clients into higher tiers. Year 1 plan prices are $600 Essential, $1,100 Professional, and $2,000 Enterprise, so the mix matters as much as the list price.

Here’s the quick math: the weighted average monthly price rises from $985 to $1,334, a $349 increase or about 35%. The mix also shifts from 50% Essential in Year 1 to 30% by Year 5, while Professional rises from 35% to 50%. That lifts revenue without the same jump in admin hours, but underpricing urgent or complex work can cap owner pay.

Price for speed and scope

Track tier mix, average monthly price, and time spent per client by service type. The main inputs are active clients, plan mix, response-time promises, and how much work is standard versus complex. If a client needs same-day support or heavier document work, price it above the base tier so margin follows effort.

- Review renewal prices every contract cycle.

- Separate urgent work from routine work.

- Watch hours per client, not just revenue.

1

Billable Utilization

Billable Utilization

Billable utilization is the share of paid client work out of total available hours. For secretarial services, unpaid time includes sales calls, onboarding, invoicing, inbox triage, scheduling fixes, staff training, and quality checks. The owner’s income rises when more of the same labor base turns into paid work, because EBITDA before interest, taxes, depreciation, and amortization improves without adding payroll.

The key inputs are available hours, billable hours, and the utilization rate you let users edit. Since no source utilization rate is provided, keep it flexible in the model. Push it too high and response time slips; leave room for client emergencies or renewals can suffer. That tradeoff is what protects take-home pay.

Track paid hours, not just busy hours

Measure billable hours by client, month, and service line. Compare them to total scheduled hours so you can see where time leaks into non-billable work. Then set a target range that protects service quality, because an hour booked with no slack can turn into rework, delays, and churn. The goal is better revenue from the same payroll base.

Use the math on each plan: $600, $1,100, and $2,000 monthly fees divided by hours used tells you real revenue per hour. If onboarding, scheduling corrections, or quality checks keep rising, tighten scope, price the work higher, or shift low-value tasks away from senior staff so more paid hours flow to owner profit.

2

Recurring Retainers

Recurring Retainers

Recurring retainers make owner income easier to forecast than one-off typing or scheduling jobs. The source model uses monthly plans at $600, $1,100, and $2,000 in Year 1, rising to $680, $1,300, and $2,400 by Year 5. More repeat clients smooth cash flow, cut sales pressure, and help staffing stay steady.

The risk is scope creep. A retainer can turn into unpaid unlimited work if request limits are loose, which pushes down gross margin and owner pay. Here’s the quick math: more retained clients help revenue grow from $591k to $6591M, but only if the work stays inside the package.

Lock the Scope

Track monthly recurring revenue, active clients, plan mix, renewal dates, and hours used per client. Those inputs tell you whether each retainer still covers labor and overhead. If a client on a $600 plan starts using senior support or constant rush work, the margin can disappear fast.

Set written limits on turn times, revisions, and out-of-scope tasks. Review every client that exceeds plan hours or needs frequent extras, then raise price or repackage before the work becomes free. That keeps recurring revenue predictable and protects the owner’s monthly draw.

3

Subcontractor Leverage

Subcontractor Leverage

Delegating admin work can raise capacity fast, but the owner only wins if markup, utilization (paid hours as a share of available hours), and quality control stay tight. In the source model, virtual assistant staffing rises from 2 FTE in Year 1 to 18 FTE in Year 5, while payroll climbs from $330k to $1595M. That means more revenue can be sold, but margin is easier to lose.

This is not solo margin. In an agency setup, the owner pays subcontractors before taking distributions, so take-home income depends on what is left after payroll, fixes, and churn. The main leak is rework: if client work has to be corrected, the team absorbs more hours without new revenue, and client churn follows. One line says it all: more hands only help if each hand stays busy and accurate.

Track FTE output and rework

Measure revenue per FTE, billable hours per FTE, and rework rate each month. If the team is busy but corrections are rising, the added headcount is not lifting owner income. Also watch response time and churn by client tier, because delegated admin work fails fast when service slips on speed or accuracy.

Use a simple gate before adding staff: new payroll should be backed by enough recurring work to keep the team productive. Keep scopes tight, document standard steps, and price fast-response or complex tasks above basic admin. If markup is thin or utilization drops, the owner’s distribution gets squeezed even when revenue grows.

4

Client Retention

Stable Clients and Referrals

Client retention is about keeping active subscribers long enough to recover sales time and cut replacement spend. In this model, CAC (customer acquisition cost) improves from $450 in Year 1 to $350 in Year 5, but the annual marketing budget still rises from $45k to $250k. If churn stays high, that spend eats owner profit fast.

Repeat clients also lift margin because the team already knows each client’s tools, tone, and deadlines. One clean win: fewer re-sales, fewer handoffs, and smoother scheduling. The main risk is post-onboarding churn if scope, responsiveness, or confidentiality slips, which forces the owner back into costly replacement mode.

Track Retention That Pays

Measure repeat client rate, referral share, and time to first repeat booking. Those inputs tell you whether retained clients are lowering unpaid sales work and protecting cash flow. Here’s the quick math: more repeat revenue means each marketing dollar supports more months of billings, so the owner keeps more take-home after payroll and sales effort.

Protect retention with tight onboarding, clear scope, fast response times, and written confidentiality rules. If onboarding takes 14+ days or scope keeps expanding without a price reset, churn risk rises. The goal is simple: hold clients longer so you replace fewer accounts and spend less to keep revenue steady.

- Track churn after onboarding.

- Review referral sources monthly.

- Price scope changes fast.

- Document response-time standards.

5

Overhead and Reserves

Overhead and Reserves

Lean overhead protects owner pay, but profit is not all spendable cash. This model has $355k per month of fixed expenses for insurance, systems, virtual office, accounting, internal tools, and professional development. If those costs rise faster than recurring subscriptions, EBITDA can look fine while cash for distributions stays tight.

The cash buffer matters just as much. Required capital spending includes $12k workstations, $85k security setup, $15k website and SEO setup, $25k client portal, and $10k training modules. The disclosed minimum cash need is $830k in Month 2, so taking draws before slow months, software renewals, refunds, or payroll timing can create a shortfall.

Track cash, not just profit

Measure monthly fixed cost, capex timing, and cash on hand against the $830k floor. Here’s the quick check: if the reserve balance drops below that line, owner distributions should pause until the next cash inflow clears. That keeps pay safer in slow months and avoids funding operating gaps with personal draws.

Build the reserve around real timing risks: software renewals, refund spikes, and payroll dates. A simple rule helps: pay the owner only after fixed costs, near-term capex, and the next payroll cycle are covered. That turns profit into usable cash instead of paper income.

6

Scenario objective: compare low, base, and high owner income cases

Owner income scenarios

Income rises as revenue scales, but payroll and marketing take most of the gain. The owner's take depends on salary plus any draw left after reserves.

| Scenario | Low CaseLaunch | Base CaseScale | High CaseMature |

|---|---|---|---|

| Launch model | Owner income is mostly the $95k general manager salary in a thin launch year. | Owner income can add distributions on top of salary in a $2.499M Year 3 scale case. | Owner income can be strongest in Year 5, when revenue reaches $6.591M and EBITDA reaches $3.658M. |

| Typical setup | Year 1 uses $591k revenue, $54k EBITDA, 9.1% EBITDA margin, $45k marketing, and $330k payroll. | Year 3 uses $2.499M revenue, $1.087M EBITDA, 43.5% EBITDA margin, $120k marketing, and $820k payroll. | Year 5 uses $6.591M revenue, $3.658M EBITDA, 55.5% EBITDA margin, $250k marketing, and $1.595M payroll. |

| Cost drivers |

|

|

|

| Owner income rangeBefore owner reserves | $95k-$149kLaunch pay | $95k-$1.182MScale pay | $95k-$3.753MMature pay |

| Best fit | Use this to test launch pay if growth is slow and reserves stay tight. | Use this for planning a normal scale-up with room for salary and draws. | Use this to test upside if the team fills capacity and keeps margins strong. |

Planning note: These are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distribution outcomes; reserve holdbacks are still user-set because no fixed reserve rate is provided.

Related Products

- Secretarial Services Porter's Five Forces Analysis

- Secretarial Services BCG Matrix

- Secretarial Services Business Model Canvas

- What Are The 5 Core KPIs For Secretarial Services Business?

- Secretarial Services Business Plan Template in Pre-Written Word

- How Increase Secretarial Services Profits?

- What Does Running Secretarial Services Cost?

- Secretarial Services Startup Costs: $830K Launch Cash Plan

- Secretarial Services Financial Model Template in Excel

- How To Open A Secretarial Services Business In 2 To 6 Weeks

- How Increase Secretarial Services Profitability?

- Secretarial Services Marketing Mix

- Secretarial Services Marketing Plan

- Secretarial Services Business Proposal

- Secretarial Services PESTEL Analysis

- Secretarial Services Pitch Deck Example Editable PPTX

- Secretarial Services Business SWOT Analysis

- Secretarial Services Value Proposition Canvas

Frequently Asked Questions

The model shows $95k in general manager pay plus possible profit distributions Revenue is $591k in Year 1, with $54k EBITDA, then reaches $6591M revenue and $3658M EBITDA by Year 5 Treat this as planning math, not a guaranteed salary or tax result