Owner income≈$185k

Owner income≈$185kShared Services Consulting Owner Income: $0 Distribution on $245M Revenue

Fully Editable

Instant Download

Professional Design

Pre-Built

No Expertise Is Needed

Description

Owner income≈$185k  Net margin26.2%–56.7%

Net margin26.2%–56.7% Revenue for target pay≈$326k

Revenue for target pay≈$326k Business difficultyMedium

Business difficultyMedium

You’re modeling owner take-home, not employee pay In this five-year shared services center consulting income model, revenue grows from about $455k in Year 1 to $245M in Year 5, but the researched cost plan leaves $0 in owner distribution capacity after payroll, overhead, marketing, and delivery costs This is not tax advice or a guaranteed draw

Owner income≈$185kNet margin26.2%–56.7%Revenue for target pay≈$326kBusiness difficultyMediumWant to test your owner income?

Owner income calculator

Estimate owner take-home and target-pay gap from revenue, gross margin, labor, fixed costs, reserves, and target pay.

Planning note: This is a researched planning estimate only. It is not guaranteed salary, tax advice, or owner distribution advice.

Can you check owner income in the model?

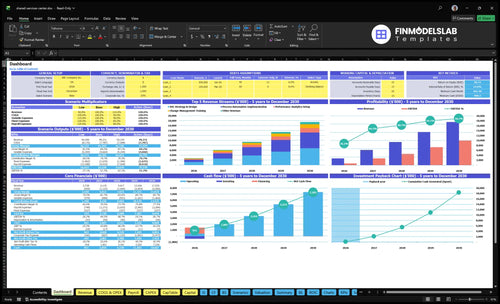

Open the Shared Services Center Consulting Financial Model Template to see dashboard, revenue, staffing, margin, overhead, cash reserves, and owner scenarios.

Owner-income model highlights

- Distribution capacity: $0

- Revenue chart: $455k-$245M

- Margin chart: 795%-857%

- Fixed overhead: $327k

- Payroll: $600k-$2365M

- Product bridge stays secondary

- Pricing, hiring, cash scenarios

How much revenue does a shared services consulting firm need to pay the owner?

Shared Services Center Consulting does not pay the owner from revenue alone. In Year 5, the model shows about $245M in revenue and about $210M in gross profit, but $218M of non-owner payroll, plus travel, commissions, marketing, fixed overhead, reserves, and taxes still sit ahead of owner distributions. The owner salary is only $185k, so the real test is whether there is cash left after delivery costs and overhead.

Cost load first

- $218M non-owner payroll

- Delivery costs come first

- Travel and commissions add up

- Marketing and overhead still hit

Owner pay math

- $185k owner salary

- Revenue is not owner pay

- Need higher revenue or leaner payroll

- Lean delivery model lifts draw capacity

What margins matter most in shared services consulting?

In Shared Services Center Consulting, gross margin can look fine, but owner pay gets squeezed by hiring and sales costs. If you’re sizing How Much To Start Shared Services Center Consulting Business?, the real test is whether margin survives $327k of fixed overhead, travel and commissions at 93% to 65%, and payroll that scales fast. Here’s the quick read: delivery costs fall from 205% of revenue in Year 1 to 143% in Year 5, but subcontractors, senior consultant utilization, proposal time, client travel, analytics tools, and implementation complexity decide what the owner keeps.

Gross margin

- 205% of revenue in Year 1

- 143% of revenue in Year 5

- Delivery cost falls over time

- Gross margin still needs control

Owner income

- $327k fixed overhead yearly

- Travel and commissions run 93% to 65%

- Payroll scales fast with growth

- Margin only counts after sales costs

Is shared services center consulting profitable?

No, Shared Services Center Consulting is not profitable under the current staffing and overhead plan: Year 5 revenue reaches about $2.45M, but known payroll alone reaches $2.365M before $327k fixed overhead, $325k marketing, variable costs, and delivery costs. For launch context, see How To Launch Shared Services Center Consulting Business?, but the core fix is bigger engagements, slower hiring, higher utilization, more advisory retainers, and better sales efficiency.

Profit math

- Year 5 revenue: $2.45M

- Known payroll: $2.365M

- Fixed overhead: $327k

- Marketing spend: $325k

Main levers

- Gross margin: 79.5% to 85.7%

- Sell larger client engagements

- Hire slower against booked revenue

- Add recurring advisory retainers

Want the six income drivers?

1

$114K-$539KEngagement Value

Year 1 service fees run about $114K-$539K per engagement, so each bigger deal moves owner income fast.

2

35-220 hrsBillable Capacity

Tighter use of billable hours lifts revenue per consultant, and the model's service lines span 35 to 220 hours.

3

1-6 FTEStaffing Mix

Adding project, change, analytics, and admin support lets the firm take more work without breaking margin.

4

15%-38%Retainer Mix

Advisory work rises from 15% to 38% of service mix, which steadies revenue and improves cash quality.

5

$15K-$9.5KSales Cycle

CAC falls from $15K to $9.5K, so each client costs less to win and more of the fee drops to profit.

6

$327KOverhead

Fixed overhead totals $327K a year, and marketing rises from $125K to $325K, so reserve discipline protects take-home.

Shared Services Center Consulting Core Six Income Drivers

Average engagement value

Average engagement value

Average engagement value is the fee per project, and it drives owner income because bigger shared services jobs bring in more revenue with the same sales effort. Year 1 examples from the model are $527k for strategy, $539k for automation, $281k for analytics, $185k for training, and $114k for advisory.

The risk is underpricing complex implementation or giving away transition support. If scope grows but the fee does not, gross margin falls and owner pay gets squeezed. One oversized, underbilled project can tie up the team and delay cash faster than three smaller, cleanly priced jobs.

Price scope, not effort

Measure average fee by work type: diagnostic, design, automation, analytics, training, and advisory. Then separate paid delivery from unpaid transition support so the real engagement value stays visible. If the team is doing extra handoff work, add a line item or change order instead of letting it sit inside the base fee.

- Track fee by engagement type.

- Bill transition support separately.

- Use change orders for scope creep.

What matters for take-home pay is fee quality, not just close count. A higher $539k automation project can fund owner income better than several low-fee jobs, but only if delivery stays tight and paid scope stays clean. If implementation gets messy, the margin gets eaten fast.

1

Utilization and billable capacity

Billable Capacity and Utilization

When owner and team time stays billable, revenue grows; when it gets eaten by selling, cash work, and client risk, take-home slips. In this model, Year 1 engagements run from 35 advisory hours to 220 automation hours, then move to 55 and 195 hours by Year 5, so capacity planning matters as much as pricing.

Owner utilization is not the same as employee utilization. The owner also handles proposals, collections, and escalation, so a proposal-heavy month can cut paid hours and delay the owner draw even if the team stays busy. More nonbillable time means less invoiced work, weaker cash flow, and slower profit conversion.

Track billable hours by role

Measure billable hours by owner versus staff, and split work into strategy, implementation, governance, and analytics. Track proposal time, billed hours per engagement, and unbilled client support so you can see where revenue leaks. If the owner is spending too much time on sales and risk, use staff or subcontractors to protect billable capacity.

- Track owner billable hours weekly.

- Set hours per engagement by service.

- Flag proposal-heavy months early.

- Watch unbilled transition support.

Use the Year 1 range of 35 to 220 hours as your planning band, then compare each active client against it. If billed hours fall faster than the team can add capacity, revenue lands late and owner pay moves out.

2

Delivery staffing mix

Delivery staffing mix

This driver is the mix of senior specialists, subcontractors, payroll, and technology partner licensing used to deliver the work. It hits owner income before taxes and reserves: delivery costs are 205% of revenue in Year 1 and 143% in Year 5, so the model starts underwater and stays tight even as payroll rises from $600k to $2.365M.

Senior specialists can lift quality and capacity, but every hire needs enough billable work. If demand is uneven, subcontractors protect cash better than adding payroll; otherwise idle time and fixed salary burn eat gross profit. The key input is the ratio of paid hours to total delivery labor.

Measure billable load first

Track billable hours, utilization, subcontractor spend, and licensing fees by project. Here’s the quick test: if a senior specialist cannot stay loaded with paid work, the staffing mix is too fixed for the revenue base. Reforecast each month, because a small gap in demand turns into slower owner pay fast.

- Billable hours by role

- Payroll per consultant

- Subcontractor rate and mix

- License cost per project

Use subcontractors for uneven demand and reserve payroll for steady work. That keeps cash from getting trapped in bench time. If staffing is right-sized, more of each fee can flow to gross profit, then to taxes, reserves, and the owner’s draw.

3

Recurring advisory revenue

Recurring advisory retainers

Advisory retainers help smooth cash flow between larger transformation projects, but they do not replace the core project engine. Here’s the quick math: at 35 hours × $325 in Year 1, one engagement is about $11,375; at 55 hours × $405 in Year 5, it’s about $22,275. As the advisory share rises from 15% to 38%, owner pay gets steadier, but the firm still depends on project wins.

Track retainer mix and hours

Measure retained clients, billable hours, renewal rate, and realized hourly rate. Keep advisory work tied to governance, KPI design, process improvement, and optimization. The win is smoother cash flow and a steadier owner draw; the risk is senior time getting trapped in low-scope support.

- Track renewal rate each quarter

- Compare sold hours to used hours

- Protect project capacity first

Because the model stays heavily project-based through strategy, automation, training, and analytics, use retainers to bridge gaps, not to carry the whole P&L. If advisory hours rise without price discipline, margin slips and owner income becomes less predictable.

4

Sales cycle and close rate

Sales cycle and close rate

In shared services consulting, the sales cycle decides when fee revenue lands and whether fixed overhead gets covered on time. With marketing spend rising from $125k in Year 1 to $325k in Year 5, the source case implies about 83 clients at first and 342 later, so slow closes can leave payroll and overhead hanging before cash arrives.

CAC (customer acquisition cost, or total sales and marketing spend per new client) moves from $15k in Year 1 to $95k in Year 5 in the model. Long enterprise buying cycles also cut owner billable time, and every missed deal means one more month of proposal work without revenue to support owner pay.

Tighten the close-rate math

Track leads, proposals, win rate, days to sign, and days to cash. Use the clean formula: close rate = wins ÷ proposals. If proposals keep rising but wins do not, the firm is spending owner time and cash on work that never turns into fee revenue.

Before each proposal, check fit, bu dget, decision maker, and timing. That keeps unpaid drafting down and protects payroll. The goal is not more activity; it is more signed work that starts fast enough to cover fixed costs and let the owner draw profit without waiting on slow approvals.

5

Overhead and reserve discipline

Overhead and reserve discipline

Overhead here means fixed costs that hit even in a slow quarter: $27,250 per month, or $327,000 per year, before payroll and marketing. Add $125,000 of marketing in Year 1 and the firm is already near $452,000 before payroll. That is why owner pay gets squeezed fast when deal flow slows.

Reserves are not profit. Hold cash only after the firm can cover delivery, payroll, sales, tools, insurance, travel, and admin. In Year 5, marketing rises to $325,000, so faster reinvestment can keep cash tied up; tighter overhead and slower spend usually improve owner distributions sooner than revenue growth alone.

Track burn before you add spend

Measure monthly fixed burn, marketing spend, payroll timing, and reserve months on hand. Then test whether new spend brings in paid work fast enough to cover the extra burn. One clean rule: don’t fund new overhead with hoped-for pipeline.

Track fixed burn monthly.

Set a cash reserve floor.

Delay spend until cash covers it.

The key question is simple: does each added dollar of overhead improve billable capacity, or just raise break-even? If it does not, it cuts owner draw even when revenue is growing.

6

Compare owner income scenarios

Owner income scenarios

Owner income scales with revenue, margin, and headcount load. In this model, cash stays inside the business through the forecast, so distributions are not yet a planning source.

| Scenario | Low CaseRevenue growth | Base CasePayroll pressure | High CaseNot yet fundable |

|---|---|---|---|

| Launch model | This is the early ramp case, where Year 1 scale is still funding the buildout. | This is the modeled mid-scale case, where the business is bigger but still reinvesting cash. | This is the stronger Year 5 run-rate case, but owner distributions still do not clear the model. |

| Typical setup | Year 1 revenue is about $2.7M, gross margin is 79.5%, payroll is about $648k, fixed overhead is $327k, and marketing is $125k. | Year 3 revenue is about $9.4M, gross margin is 83.6%, payroll is about $1.65M, and marketing is $225k. | Year 5 revenue is about $17.5M, gross margin is 85.7%, payroll is about $2.53M, and marketing is $325k. |

| Cost drivers |

|

|

|

| Owner income rangeBefore owner reserves | $0No payout yet | $0Still no payout | $0No distributions |

| Best fit | Use this to stress-test the first operating year when growth still absorbs cash. | Use this as the core plan for staffing, cash use, and owner take-home timing. | Use this to test the mature run-rate and when owner payouts could start. |

Planning note: Scenario figures are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions.

Related Products

- Shared Services Center Consulting Porter's Five Forces Analysis

- Shared Services Center Consulting BCG Matrix

- Shared Services Center Consulting Business Model Canvas

- What Five KPIs Define Shared Services Center Consulting Business?

- Shared Services Center Consulting Business Plan Template in Pre-Written Word

- How Increase Profitability Of Shared Services Center Consulting?

- What Are Operating Costs For Shared Services Center Consulting?

- Shared Services Center Consulting Startup Costs: $280K+ CAPEX

- Shared Services Center Consulting Financial Model Template in Excel

- How To Start A Shared Services Consulting Firm In 8-16 Weeks

- How To Write A Business Plan For Shared Services Center Consulting?

- Shared Services Center Consulting Marketing Mix

- Shared Services Center Consulting Marketing Plan

- Shared Services Center Consulting Business Proposal

- Shared Services Center Consulting PESTEL Analysis

- Shared Services Center Consulting Pitch Deck Example Editable PPTX

- Shared Services Center Consulting Business SWOT Analysis

- Shared Services Center Consulting Value Proposition Canvas

Frequently Asked Questions

Under these researched assumptions, sustainable owner distributions are $0 because EBITDA stays negative The model includes a $185k managing partner salary line, but that pay would need funding if operating cash is short Revenue grows from about $455k to $245M, yet payroll, marketing, delivery costs, and $327k fixed overhead absorb the margin