Owner income$331k

Owner income$331kHow Much Can A Singaporean Hawker Stall Owner Make: $446k/Month

Fully Editable

Instant Download

Professional Design

Pre-Built

No Expertise Is Needed

Description

Owner income$331k  Net margin24%

Net margin24% Revenue for target pay$501k

Revenue for target pay$501k Business difficultyHard

Business difficultyHard

A Singaporean hawker stall can produce about $5358k in first-year operating cash flow under the researched base assumptions, or roughly $446k per month before reserves, debt service, and personal taxes Here’s the quick math: 70 average orders per day, a $5418 blended ticket, $1151k monthly revenue, 140% ingredient cost, 44% variable fees, $400k annual payroll, and $159k monthly fixed overhead Owner take-home depends on how much cash stays in the business for working capital, equipment, taxes, and slow weeks

Owner income$331kNet margin24%Revenue for target pay$501kBusiness difficultyHardWant to test your own stall numbers?

Owner income calculator

Estimate owner take-home and the target-pay gap from revenue, margin, costs, reserves, and target pay.

Planning note: This is a researched planning estimate, not guaranteed salary, tax advice, or owner distribution advice.

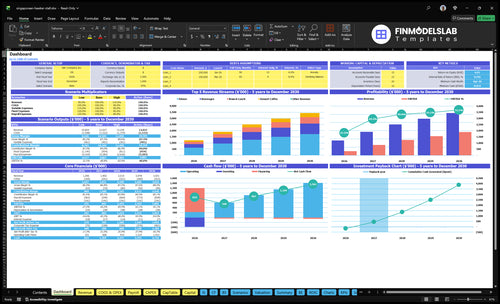

How do you check owner income in the Singaporean Hawker Stall model?

This screenshot shows revenue, margin, costs, reserves, and owner take-home assumptions. Open the Singaporean Hawker Stall Financial Model Template.

Owner-income model highlights

- Owner income sits on dashboard

- Covers, AOV, COGS, payroll drive output

- $380k capex, Month 4 cash need

- Month 3 break-even, 16-month payback

- 0.09% IRR, 601% ROE

How many orders does a Singaporean hawker stall need per day?

A Singaporean hawker stall should plan for about 70 orders a day in year one, with demand swinging from 30 on Monday to 100 on Friday, 120 on Saturday, and 80 on Sunday. Break-even is about 37 orders/day, and if the owner wants $10,000 a month in pay, the target rises to about 45 orders/day. So the real constraint is not just sales; it’s whether lunch and dinner rushes, slow weekdays, seasonality, and queue speed can hold up.

Year-one order pace

- 70 orders/day average target

- 30 orders on Monday

- 100 orders on Friday

- 120 orders on Saturday

Break-even pressure

- 37 orders/day break-even point

- 45 orders/day with $10,000 owner pay

- Lunch and dinner rush must stay fast

- Slow weekdays need tighter prep

Is a Singaporean hawker stall profitable in the US?

The Singaporean Hawker Stall can be profitable in the base case, but only if traffic, labor, and rent stay close to plan. Here’s the quick math: first-year revenue is $138M, operating cash flow is $5,358k, and break-even hits in Month 3. But the risk is still real, because startup capex is $380k and minimum cash need rises to $619k in Month 4.

Base case math

- $138M first-year revenue

- $5,358k operating cash flow

- Month 3 break-even

- Judge on cash, not just sales

Risk check

- $380k startup capex

- $619k cash need by Month 4

- Lean owner-run beats heavy staffing

- High volume only helps if costs hold

What profit margin does a Singaporean hawker stall need?

For a Singaporean Hawker Stall, the source assumptions imply a first-year ingredient COGS of 140% of sales, split into 95% food ingredients and 45% beverage ingredients, so the model needs a very high menu margin to hold. After ingredients, gross margin is 860%; after marketing and POS fees, contribution margin is 816%, and operating margin before reserves and tax is about 388%.

Margin drivers

- Rice dishes move margin fast

- Noodle soups change cost quickly

- Satay and curries matter too

- Proteins push food COGS hard

Model checks

- Track imported sauces closely

- Watch herbs and waste

- Track packaging in the model

- Packaging is not separately priced

Which drivers move owner income most?

1

70/dayDaily Orders

At about 70 first-year orders a day, every extra order adds revenue with little extra fixed cost, so volume is the biggest take-home lever.

2

$45-$70Ticket Mix

Midweek orders run $45-$55 and weekend orders run $60-$70, so a better menu mix lifts revenue per guest fast.

3

$400KLabor Model

Year 1 payroll is $400K across 10 FTE, so staffing, overtime, and role mix can swing owner profit hard.

4

12%-14%Food Costs

Food and beverage ingredients start near 14% of sales and ease toward 12%, so tighter prep and waste control drops straight to income.

5

$15.9K/moRent & Fees

Rent, utilities, insurance, permits, software, maintenance, and cleaning total $15.9K a month, so this is the floor you must cover before profit starts.

6

LowChannel Mix

Dinner is 50% of Year 1 sales and beverages are 25%, so mix shifts can help, but the model has no default delivery commission.

Singaporean Hawker Stall Core Six Income Drivers

Daily Order Volume And Foot Traffic

Daily Order Volume

Revenue starts with covers, or paid orders. The first-year model assumes 490 weekly orders, about 70 per day, but demand is uneven: 30 orders on Monday and 120 on Saturday. Staffing, prep, and cook speed have to flex by day, or labor, waste, and slow service will eat into take-home income.

Foot traffic, reviews, market days, and lunch or dinner throughput set the ceiling. Here’s the quick math: each extra $5,418 ticket adds about $4,420 contribution before payroll and fixed costs. So when volume rises, cash flow improves fast; when it falls, owner pay gets squeezed first.

Track Traffic to Raise Covers

Measure foot traffic, orders by day, weekday versus weekend mix, and line speed. That shows how many passersby turn into covers and where the bottleneck sits. A strong menu still misses income if lunch service is slow or Saturday prep runs out early.

- Track covers by hour.

- Match prep to demand.

- Test market-day traffic lift.

Use the 30-order Monday and 120-order Saturday pattern to plan labor and batch prep. Keep the goal simple: more orders at the same service speed, so more contribution reaches owner pay instead of being lost to overtime or missed sales.

1

Average Ticket And Menu Mix

Average Ticket And Menu Mix

Revenue here is covers × average ticket. With $45 midweek AOV and $60 weekend AOV, the same foot traffic can swing cash flow fast. Menu mix matters too: dinner is 50% of sales, beverages 25%, brunch/lunch 15%, and dessert/coffee 10%, so add-ons can raise take-home income without adding seats.

By Year 5, beverages rise to 27% and dinner slips to 48%, so the owner should watch whether higher drink mix improves margin or just lowers meal size. Keep pricing affordable; this concept depends on repeat traffic, so a ticket bump that hurts return visits can cut profit even if same-day revenue looks better.

Raise Ticket Without Losing Repeat Guests

Track AOV by daypart, drink attach rate, and the share of combos, proteins, sides, and specials. Here’s the quick math: if the same customer count buys one more side or drink, revenue rises before rent or base labor changes. The goal is a better mix, not a pricier menu that pushes out students and urban professionals.

Test small upsells first. Bundle a main with a beverage or dessert/coffee, then check whether the higher ticket holds on the next visit. If repeat rate softens, the extra dollars are not real profit. What this estimate hides is waste, slower line speed, and the margin hit from too many custom add-ons.

2

Food Cost, Packaging, Sourcing, And Waste

Food And Packaging COGS

When ingredients and containers run this high, the stall’s cash gets squeezed fast. The model shows first-year food ingredients at 95% of revenue and beverage ingredients at 45%, for 140% total COGS; by Year 5 that only improves to 120%. At $1.151M monthly revenue, every 1 point of COGS is about $12k/month before tax.

That means proteins, rice, noodles, coconut milk, spices, sauces, herbs, takeout containers, portion size, and batch prep all hit owner pay directly. If waste or over-portioning adds 3 points, that’s roughly $36k/month gone before rent and payroll. If COGS stays above sales, the owner is funding the gap with cash, not profit.

Cut Waste, Not Flavor

Measure food cost per dish, beverage cost per drink, and packaging per order by recipe, not by month. Track purchase price, yield, and spoilage for each protein and sauce, then compare that to actual covers and mix. The key input is real sales mix, because a noodle-heavy day and a beverage-heavy day won’t have the same margin.

- Daily covers and item mix

- Recipe cost by SKU

- Vendor price and yield

- Packaging cost per order

- Spoilage and trim loss

Cut waste with portion scoops, batch prep logs, and a simple prep sheet that ties to daily volume. If COGS drops from 140% to 130%, that’s about $115k/month of room at $1.151M revenue. One clean habit beats one big menu change.

3

Labor Model And Owner Involvement

Labor Cost and Owner Pay

First-year payroll is $400k/year across 100 FTE, or about $33.3k/month. That covers the head chef, manager, sous chef, line cooks, servers, bartender, and dishwasher, so labor is a core cash drain before rent and overhead. If the schedule runs heavy, owner pay gets squeezed fast; if staffing is too thin, speed and quality slip.

By Year 5, payroll rises to $645k with 175 FTE. An owner-operated model can improve cash flow, but unpaid labor is not free. A partly staffed model protects quality, while a manager-run model cuts owner workload but usually lowers take-home unless sales and labor efficiency rise with it.

Track Hours, Not Hope

Measure scheduled hours, overtime, and labor as a share of sales by role. Use the same lens for every shift: head chef, manager, cooks, service, bar, and dish. The right mix is the one that keeps throughput and consistency up without padding the roster.

- Track owner hours separately.

- Log overtime each week.

- Test staffing by daypart.

- Count owner time at market pay.

If the owner covers shifts, include that time in the forecast. Unpaid labor is not free; it only changes where the cost shows up and how much cash can reach owner draw.

4

Rent, Fees, Commissary, And Fixed Overhead

Fixed Overhead

Fixed overhead is the cash drain that stays in place even when Monday traffic is weak. In this model, it runs $159k/month, with named lines of $10k rent, $25k utilities, $800 insurance, $300 permits, $400 software, $700 maintenance, and $12k cleaning. Those named items total $49.2k/month, so $109.8k sits in other fixed overhead.

That’s why the stall needs about $603k/month in sales before owner pay. If sales miss that level, the owner’s take-home gets squeezed fast because these costs do not fall with slower traffic. The key check is simple: if revenue is soft but margins are holding, the issue may be traffic; if traffic is fine but cash is tight, fixed overhead may be too heavy.

Track Fixed Costs Monthly

Measure fixed overhead as a clean monthly stack, separate from variable fees. Track rent, utilities, cleaning, permits, software, insurance, and maintenance on one line, then compare that total with sales. At the break-even point of $603k/ month, fixed overhead is about 26% of sales before owner pay, so small misses in traffic can hit profit hard.

- Watch overhead versus monthly sales.

- Split fixed and variable costs.

- Flag utility spikes fast.

- Review cleaning and maintenance contracts.

- Test rent before signing longer terms.

Use this split to find the real problem. If sales are below plan but fixed costs stay flat, the owner needs more covers and better throughput. If sales are near plan but cash is still weak, the fix is usually margin, staffing, or rent pressure, not more marketing.

5

Catering, Delivery, Events, And Channel Mix

Catering, Delivery, and Events

The model leaves delivery, catering, and event revenue at 0 by default, so treat these as upside, not base case. They can raise sales, but each order also adds packaging, prep time, labor, and, on apps, commissions. The key test is net contribution after variable costs; if fees run high, owner pay can fall even when gross sales rise.

Estimate each channel with orders, average ticket, commission rate, and extra hours. Then compare that contribution to dine-in stall sales. That shows whether a corporate lunch, festival, or pop-up helps cover fixed overhead and lifts the owner’s draw, or just creates busy work.

Test Each Channel’s Margin

Track dine-in, delivery, catering, and events separately. Use the quick test: revenue - food - packaging - commissions - added labor = contribution. Keep a minimum order size for trays and lunches, and price delivery high enough to cover platform fees and the extra kitchen load.

- Measure orders by channel.

- Track ticket and fee rates.

- Log added labor hours.

- Set minimum tray orders.

- Review margin weekly.

6

Compare low, base, and high owner-income scenarios without treating them as predictions

Owner income scenarios

Owner income moves with traffic, ticket size, and labor load. In this model, the break-even case barely supports the owner, while higher volume and better mix drive much larger cash flow.

| Scenario | Low CaseDownside | Base CaseBase | High CaseUpside |

|---|---|---|---|

| Launch model | This is the lower-earnings path, where the stall only clears break-even cash and owner income stays close to zero. | This is the modeled operating case, where first-year volume supports solid cash flow before reserves. | This is the stronger-earnings path, where Year 5 scale pushes owner income sharply higher. |

| Typical setup | About $603k monthly revenue, 37 orders/day, and a $5,418 ticket leave almost no owner pool after reserves. | About $1.151m monthly revenue, 70 orders/day, 140% COGS, 44% variable fees, and $400k payroll still leave healthy cash flow before reserves. | About $2.984m monthly revenue in Year 5, 154 orders/day, a $6,375 blended ticket, 120% COGS, 29% variable fees, and $645k payroll drive stronger cash flow before reserves. |

| Cost drivers |

|

|

|

| Owner income rangeBefore owner reserves | Near $0Near break-even | $446k/moForecast cash flow | $1.842m/moStrong upside case |

| Best fit | Use this to stress-test downside cash and reserve needs. | Use this for a first-year planning case with steady demand. | Use this for an experienced operator testing peak demand and scale. |

Planning note: Scenario ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions.

Related Products

- Singaporean Hawker Stall Porter's Five Forces Analysis

- Singaporean Hawker Stall BCG Matrix

- Singaporean Hawker Stall Business Model Canvas

- 7 Core Financial KPIs for the Singaporean Hawker Stall

- Singaporean Hawker Stall Business Plan Template in Pre-Written Word

- 7 Strategies to Increase Singaporean Hawker Stall Profitability

- How Much Does It Cost To Operate A Singaporean Hawker Stall Monthly?

- How Much Does It Cost To Open A Singaporean Hawker Stall? $619K Plan

- Singaporean Hawker Stall Financial Model Template in Excel

- How To Open A Singaporean Hawker Stall In 8–16 Weeks

- How to Write a Singaporean Hawker Stall Business Plan

- Singaporean Hawker Stall Marketing Mix

- Singaporean Hawker Stall Marketing Plan

- Singaporean Hawker Stall Business Proposal

- Singaporean Hawker Stall PESTEL Analysis

- Singaporean Hawker Stall Pitch Deck Example Editable PPTX

- Singaporean Hawker Stall Business SWOT Analysis

- Singaporean Hawker Stall Value Proposition Canvas

Frequently Asked Questions

The researched setup shows $380k in capex and a $619k minimum cash need by Month 4 Capex includes $150k kitchen equipment, $80k dining room furniture and decor, $60k HVAC and plumbing upgrades, and other setup costs That cash need matters because early owner draws can weaken the business before traffic stabilizes