Owner income-$70k to $425k

Owner income-$70k to $425kHow Much Does A Small Inn Owner Make? 14-Month Breakeven View

Fully Editable

Instant Download

Professional Design

Pre-Built

No Expertise Is Needed

Description

Owner income-$70k to $425k  Net margin-10% to 32%

Net margin-10% to 32% Revenue for target pay$682k to $1.335M

Revenue for target pay$682k to $1.335M Business difficultyHard

Business difficultyHard

Key Takeaways

- Profitable occupancy matters more than full rooms.

- ADR drives income fast when room count is small.

- Labor and fixed costs cap owner take-home.

- Direct bookings lift margin better than paid channels.

Owner income-$70k to $425kNet margin-10% to 32%Revenue for target pay$682k to $1.335MBusiness difficultyHardWant to test your inn owner income?

Owner income calculator

Estimate owner take-home and the target-pay gap from revenue, gross margin, labor, overhead, reserves, and target owner pay.

Planning note: Model backdrop shows Year 1 EBITDA of -70,000, Year 5 EBITDA of 425,000, minimum cash of 727,000, and breakeven in Month 14. Research-based planning estimate only; not guaranteed salary, tax advice, owner distribution advice, financing approval, valuation guarantees, or legal advice.

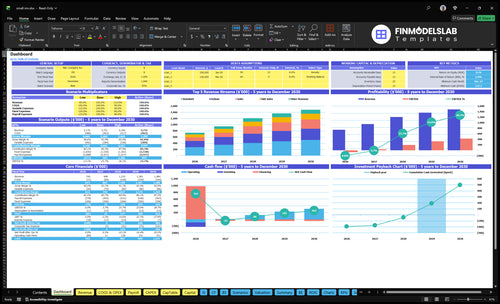

How do you check owner income in the Small Inn financial model?

The screenshot shows revenue, margin, costs, reserves, and owner take-home assumptions in the Small Inn Financial Model Template; open the model.

Owner-income model highlights

- Owner pay from cash flow

- Revenue ties to occupancy

- Scenarios test EBITDA and breakeven

How does owner-operated inn income differ from hiring an innkeeper?

For Small Inn, owner-operated income can look higher because you keep the $80k general manager salary in the business if you handle reservations, guest service, breakfast oversight, vendor coordination, and housekeeping checks yourself. But that is not free profit, because your unpaid labor still has real value. If you hire an innkeeper, the owner’s workload drops, but take-home also drops because payroll stays in the model.

Owner-run cash effect

- $80k stays in the business

- Owner covers daily guest work

- Reservations and service stay in-house

- Income looks higher, not passive

Hire-an-innkeeper tradeoff

- Payroll stays in the model

- Owner workload drops fast

- Front desk coverage needs budget

- Quality control still needs oversight

What small inn operating costs reduce owner income most?

For a Small Inn, the biggest hit to owner income is payroll, then fixed property costs. If you want the launch cost side too, see What Is The Estimated Cost To Open And Launch Your Small Inn Business? — the model shows $306k/year in fixed expenses and payroll of about $327k in Year 1, rising to $433k from Year 3 onward. Variable costs also stay heavy, so labor, booking commissions, repairs, and reserve discipline drive most of the income squeeze.

Fixed costs hit first

- $15k/month lease, or $180k/year

- $35k utilities each year

- $25k taxes each year

- $18k maintenance and $12k insurance

Control these levers

- Payroll starts near $327k in Year 1

- Payroll rises to $433k from Year 3

- Variable costs fall from 175% to 128%

- Launch capex totals $128k

How much can a small inn owner make?

A Small Inn owner may make little or nothing in Year 1 because EBITDA is -$70k, then the business improves to $35k in Year 2, $190k in Year 3, $323k in Year 4, and $425k in Year 5; see What Is The Main Goal You Hope To Achieve With Small Inn? before treating profit as personal cash. EBITDA is not owner salary, since take-home depends on debt service, taxes, reserves, and cash kept inside the business.

Owner Income Path

- Year 1 EBITDA: -$70k

- Year 2 EBITDA: $35k

- Year 3 EBITDA: $190k

- Year 5 EBITDA: $425k

Cash Reality

- Minimum cash need: $727k

- Payback period: 42 months

- GM role equals $80k payroll

- Unpaid owner labor is not profit

Want to see what changes inn income most?

1

55%-82%Occupancy

Higher occupancy and steadier weekend fill push EBITDA from -$70K in Year 1 to $425K by Year 5.

2

$120-$300ADR and RevPAR

ADR (average daily rate) and RevPAR (revenue per available room) raise income from each occupied night.

3

17-18 roomsRoom Capacity

Adding rooms lifts sellable nights, and the suite count rises from 17 to 18 total rooms in Year 3.

4

$327K-$433KLabor Model

Payroll rises from $327K to $433K, so staffing control decides how much revenue becomes profit.

5

$306K/yrFixed Costs

A $306K fixed-cost base means the property needs volume before profit shows up.

6

7%-5%Channel Mix

Online travel agencies (OTAs) take 7.0% to 5.0%, so direct bookings keep more room revenue.

Small Inn Core Six Income Drivers

Occupancy And Room Nights Sold

Occupancy and Room Nights Sold

Occupancy is the share of available room nights you sell, and it only helps when each stay stays profitable. With 17 rooms, you have 6,205 available room nights a year; with 18 rooms, 6,570. At 55% occupancy, that is about 3,413 sold nights; at 82%, about 5,387. More filled nights can lift EBITDA, but only after variable stay costs stay in line.

Weekend nights can carry higher ADR than midweek, so a full calendar is not the same as good margin. If you discount midweek too hard, you may sell more rooms and still lose cash on housekeeping, breakfast, supplies, and commissions. The real test is contribution per occupied night, not occupancy alone.

Track Occupancy by Night Type

Track occupancy, room nights sold, and ADR by day type. Split demand into midweek and weekend, then set a floor rate that covers the variable cost of each stay. One clean rule: if a discount does not improve contribution, do not take it.

- Watch sold nights by weekday.

- Separate weekend and midweek rates.

- Compare rate to stay-level costs.

- Protect break-even on discounted nights.

Build the forecast from available room nights × occupancy, then stress-test it against labor and other stay costs. If higher occupancy forces extra cleaning, breakfast, or commission expense faster than room revenue rises, owner pay gets squeezed. The safest growth comes from filling higher-rate nights first, then using low-demand nights to backfill at a controlled floor price.

1

ADR And RevPAR

ADR and RevPAR

ADR, or average daily rate, is the average price you collect per room night. In a small inn, it hits owner income fast because there are only a few rooms to sell. Year 5 assumptions run from $120 midweek for a standard room to $300 for a suite, and from $180 on weekends to $420 for a suite. Underpricing premium rooms caps upside while fixed costs still sit at $306k/year.

RevPAR means revenue per available room, and it combines rate with occupancy. Here’s the quick math: RevPAR = ADR × occupancy. Pricing should move with location, guest experience, reviews, amenities, events, and seasonal demand. If rate rises but demand softens, RevPAR and owner take-home can still stall.

Track rate by room and night

Measure ADR by weekday, weekend, and room type, then compare it with occupancy and RevPAR each month. The inputs that matter are room count, guest mix, seasonal demand, and how often suites actually sell at a premium. One clean rule: raise rates where demand is already strong.

- Compare suite ADR to standard ADR

- Test event weekends separately

- Watch discounts against margin

- Protect premium room pricing

If suites are discounted just to fill midweek gaps, you may lift occupancy but cut the cash that pays payroll, repairs, and the owner draw.

2

Room Count And Revenue Capacity

Room Count Sets Revenue Ceiling

Room count is the hard cap on room revenue. This inn starts with 17 rooms — 10 standard, 5 deluxe, and 2 suites — then adds a third suite in Year 3, lifting supply to 18 rooms. That means 6,205 sellable room nights at 17 rooms and 6,570 at 18 rooms, before occupancy. More rooms can raise owner income, but only if demand fills them and service stays tight.

Each added room also adds cleaning, linen use, maintenance, and guest service load. One clean line: more keys can mean more cash, or more cost. Suites can lift ADR, but only if guests will pay the higher rate; if the suite sits empty or gets discounted, the added room may raise payroll and supplies faster than profit.

Track Room Mix And Fill Rate

Measure revenue by room type, not just total occupancy. Track suite occupancy, ADR by room class, housekeeping cost per occupied room, and how often each room is out of service. If the third suite in Year 3 does not hold a premium rate, it may be better to protect margin than chase volume.

Here’s the quick math: a new room only helps if its extra room nights cover the added labor and supply cost. Watch whether the suite’s rate lifts enough to offset the extra cleaning and service time. If staffing slips, reviews and repeat bookings can fall, and owner take-home drops even when gross revenue looks higher.

3

Owner Role And Labor Model

Owner Labor Mix

With $327k payroll in Year 1 and $433k from Year 3 onward, labor is one of the biggest cash costs. The owner’s income rises only when staff hours cover front desk, housekeeping, kitchen, and spa demand without idle time. The best gain comes from matching staff hours to occupancy patterns.

A owner-operator can replace paid management tasks and cut cash payroll, but that is still real work. What this estimate hides: cutting labor too far can hurt room turns, breakfast service, reviews, and repeat bookings, which can erase the savings.

Match Staff to Demand

Track labor hours per occupied room, not just total payroll. Split hours by general manager, front desk, housekeeping, chef, kitchen staff, spa therapist, and marketing coordinator, then compare them with occupancy and event days.

- Occupied rooms and turn time

- Breakfast covers and kitchen hours

- Spa bookings and therapist hours

- Owner hours versus manager pay

Test a leaner shift plan on slow midweek dates first. Keep enough cover for room turns, breakfast service, and guest response time. If guest scores or repeat bookings slip after a cut, the payroll savings are fake because room revenue falls faster than labor cost.

4

Fixed Property Costs And Cash Pressure

Fixed Property Cash Load

This driver is the property overhead that drains cash before owner pay: $255k/month in fixed expense, excluding debt service and reserves. The big lines are $15k lease, $25k property taxes, $12k insurance, $35k utilities, and $18k maintenance. Even if rooms sell better, these costs stay put, so margin must clear them first.

The cash test matters more than the profit line early on. The model shows a $727k minimum cash need at Month 24, so early losses and working capital must be funded. Owner take-home should come only after lease coverage, repairs, reserves, and any debt service. If not, draws just turn a paper gain into a cash crunch.

Protect Cash Coverage First

Build a monthly cash forecast that tracks lease, taxes, insurance, utilities, and maintenance separately. Here’s the quick test: if operating cash cannot cover those lines, do not pay owner draws yet.

- Track ending cash vs. $727k

- Stress-test utilities and maintenance

- Delay draws until reserves fund

- Include debt service in coverage

What this hides: deferred maintenance often comes back as bigger repair bills and weaker guest reviews. Keep the property safe and open first, then pay yourself from cash that is truly free.

5

Booking Channel Mix

Booking Channel Mix

When 70% of revenue goes to OTA commissions and marketing at launch, a lot of room revenue never reaches owner profit. By Year 5, that share falls to 50%, so the same occupied room can throw off more cash without adding rooms. This driver is the split between online travel agencies (OTA) and direct bookings, and it changes net revenue, not just occupancy.

The inputs are room nights sold, booking source mix, commission rate, and repeat guest share. Here’s the quick math: if one booking shifts from OTA to direct, contribution rises because less revenue gets paid away. But if paid channels are doing the heavy lifting, rooms may fill faster while owner take-home stays tight.

Push Direct Share Up

Track bookings by source each month: OTA, direct website, repeat guests, and walk-ins. Direct bookings need three things already in the model: a working website, guest reviews, and local demand. The launch spend of $8k for website development and $5k for signage and branding helps build that channel mix.

- Watch commission rate by channel.

- Measure repeat guest booking share.

- Track direct conversion from the website.

- Forecast owner cash after fees.

If OTA share stays high, commissions keep eating cash and can delay owner pay even when occupancy looks good. If repeat guests rise, the same room night produces more net income with no new rooms, so the business keeps more of each booking.

6

Compare low, base, and high small inn income cases

Owner income scenarios

Owner income here swings with occupancy, room mix, ADR, staffing, and booking fees. The first year is cash-heavy, then tighter labor and better direct bookings can lift take-home as EBITDA rises.

| Scenario | Low CaseCash-heavy ramp | Base CaseBreakeven case | High CaseMature-year upside |

|---|---|---|---|

| Launch model | Owner income stays near zero during the ramp as occupancy builds slowly and commissions stay high. | Owner income turns on after breakeven as the inn scales from 17 rooms to 18 rooms in Year 3 and EBITDA improves from -$70k to $425k by Year 5. | Owner income lifts faster when ADR stays strong, direct bookings replace some OTA fees, and staffing runs tighter than plan. |

| Typical setup | The inn runs with 17 rooms at launch, 55% occupancy, lower pricing power, heavier OTA commissions, and fixed payroll and lease costs that keep cash tied up. | This case assumes occupancy moves from 55% to 82%, ADR rises across room types, and the labor model stays close to plan while extra income from food, events, parking, and spa services fills out revenue. | The inn reaches the upper end of its room base with 18 rooms in later years, 82% occupancy, stronger room rates, and better labor scheduling, which supports more cash for the owner. |

| Cost drivers |

|

|

|

| Owner income rangeBefore owner reserves | No owner distributionsLow Case | Breakeven to $190kBase Case | $323k - $425kHigh Case |

| Best fit | Use this to stress-test a slow opening where cash stays tight and the owner takes no draws during ramp. | Use this as the main planning case for a normal ramp with breakeven in Month 14 and payback around 42 months. | Use this to test upside if demand stays strong and the owner keeps a close grip on labor and booking costs. |

Planning note: These scenario ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions.

Related Products

- Small Inn Porter's Five Forces Analysis

- Small Inn BCG Matrix

- Small Inn Business Model Canvas

- Tracking Key Performance Indicators for Your Small Inn

- Small Inn Business Plan Template in Pre-Written Word

- 7 Strategies to Increase Small Inn Profitability and Boost ADR

- How Much Does It Cost To Run A Small Inn Each Month?

- Small Inn Startup Costs: $132K CAPEX for a 17-Room Opening

- Small Inn Financial Model Template in Excel

- How To Open A 17-Room Small Inn: 4 To 9 Month Launch Plan

- How to Write a Small Inn Business Plan: 7 Steps to Financial Clarity

- Small Inn Marketing Mix

- Small Inn Marketing Plan

- Small Inn Business Proposal

- Small Inn PESTEL Analysis

- Small Inn Pitch Deck Example Editable PPTX

- Small Inn Business SWOT Analysis

- Small Inn Value Proposition Canvas

Frequently Asked Questions

In this model, owner take-home is limited at first because EBITDA is -$70k in Year 1 EBITDA turns positive at $35k in Year 2 and reaches $425k by Year 5 Actual owner pay comes after debt service, reserves, taxes, and cash kept for repairs