Owner income$185K base + upside

Owner income$185K base + upsideHow Much Does A SOC 2 Compliance Consulting Owner Make? $185K+

Fully Editable

Instant Download

Professional Design

Pre-Built

No Expertise Is Needed

Description

Owner income$185K base + upside  Net margin-12% to 27%

Net margin-12% to 27% Revenue for target pay$1.38M

Revenue for target pay$1.38M Business difficultyHard

Business difficultyHard

A SOC 2 compliance consulting owner can model $185K in annual salary from the Managing Principal role, with distributions only if the firm has profit after costs, reserves, and taxes In the researched base case, revenue grows from $138M in Year 1 to $791M in Year 5, while EBITDA moves from -$159K to $2136M That means Year 1 owner take-home is mainly salary, not profit By the mature year, owner earnings can include salary plus a share of EBITDA, but only after protecting the $519K minimum cash need and funding growth

Owner income$185K base + upsideNet margin-12% to 27%Revenue for target pay$1.38MBusiness difficultyHardWant to test your SOC 2 owner pay?

Owner income calculator

Estimate owner take-home and target-pay gap from revenue, margin, costs, reserves, and target pay.

Planning note: Research-based planning estimate only, not guaranteed salary, tax advice, or owner distribution advice.

How do you check owner income in the SOC 2 Compliance Consulting financial model?

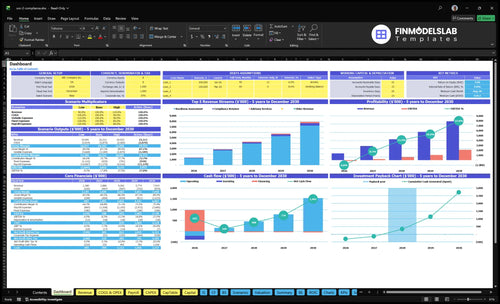

This dashboard shows revenue, pricing, client volume, capacity, retainers, payroll, software costs, fixed overhead, marketing budget, CAC, cash reserves, EBITDA, and owner income in SOC 2 Compliance Consulting Financial Model Template. Open the model to test scenarios from $138M to $791M revenue and EBITDA from -$159K to $2,136M.

Owner-income model highlights

- Owner take-home scenarios

- Revenue and EBITDA charts

- Pricing and client volume

- Capacity, payroll, overhead

How much revenue does a SOC 2 consulting firm need to pay the owner?

For SOC 2 Compliance Consulting, owner pay comes from what’s left after delivery margin, percentage costs, $186K in fixed overhead, marketing, and retained cash. In the base model, $138M Year 1 revenue can support a $185K Managing Principal salary but still lands at -$159K EBITDA, while Year 2 revenue of $2886M gets to $240K EBITDA; so there’s no universal client count, only math tied to pricing and margin.

What pay must cover

- Owner salary first

- Delivery payroll next

- Percentage costs after that

- Fixed overhead and marketing

Quick model read

- $186K fixed overhead

- -$159K EBITDA in Year 1

- $240K EBITDA in Year 2

- No set client count

Can a solo SOC 2 consultant make more than a small firm owner?

A solo SOC 2 consultant can sometimes keep more cash per dollar of revenue because payroll is lighter, but a staffed SOC 2 Compliance Consulting model from Month 1 changes the math fast. In the provided forecast, wages start at $745K in Year 1 and rise to $2,835M in Year 5, while revenue scales from $138M to $791M. So the real test is not just growth; it’s utilization, pricing, sales pipeline, quality control, and reserve discipline.

Solo owner upside

- Lower payroll means less cash burn

- More revenue can stay with owner

- Simple teams need less management

- Faster decisions cut overhead drag

Staffed firm tradeoffs

- Year 1 wages start at $745K

- Year 5 wages reach $2,835M

- Revenue grows to $791M

- Cash needs and control get harder

What affects SOC 2 consulting profit margins?

High billing rates do not equal high owner income in SOC 2 Compliance Consulting; if you’re mapping How To Launch SOC 2 Compliance Consulting Business?, the margin gets squeezed fast. Year 1 pricing sits at $250/hour for readiness, $200/hour for retainers, and $300/hour for advisory, but costs also carry $745K wages, 12% platform licensing, 5% referral fees, 7% sales commissions, 3% travel, $186K fixed overhead, and $120K marketing rework. Weak evidence quality, slow client response, and under-scoped controls cut margin, while lower licensing, referral, and travel rates should help by Year 5.

Main cost pressure

- $745K Year 1 wages

- 12% platform licensing

- 5% referral fees

- 7% sales commissions

What lifts margin

- 3% travel stays low

- Cut $120K rework

- Improve evidence quality

- Scope controls tighter

What drives SOC 2 consulting owner income?

1

$13.5KAverage Client Value

Readiness, retainer, and advisory work together to lift lifetime value, so each sale adds more owner cash.

2

40hBillable Capacity

At 40 billable hours on readiness work, small gains in utilization and pricing flow straight into gross profit.

3

24 FTEDelivery Leverage

Adding consultants and analysts lets revenue scale, but every extra FTE has to earn more than its salary.

4

$2K/moRetainer Revenue

A $2K monthly retainer smooths cash and pushes more revenue past the first project into repeat income.

5

$4.5KSales Efficiency

With CAC at $4.5K, faster close rates and better lead quality keep more of each sale for the owner.

6

$519KCost and Reserves

Fixed overhead is about $186K a year, and the $519K cash floor means tight cost control protects pay and survival.

SOC 2 Compliance Consulting Core Six Income Drivers

Average Client Value And Pricing

Average Client Value And Pricing

Client value comes from the mix of readiness work, retainers, and advisory time. In Year 1, the model prices readiness at 40 hours × $250 = $10,000, retainers at 10 hours × $200 = $2,000 per month, and advisory at 5 hours × $300 = $1,500. Scope and client complexity set the real ticket, so underpricing control implementation can cut owner distributions fast.

Here’s the quick math: pricing is not the same as a CPA audit fee. Consulting covers gap analysis, policy work, and control setup, while audit fees sit outside this service line. The forecast implies about $518K in Year 1 revenue per acquired client, so small pricing misses scale into big profit leaks when hours slip past the estimate.

Price By Scope, Not Hope

Track three inputs on every job: readiness hours, retainer hours, and advisory hours. Also record client complexity, because the same SOC 2 project can take more time for a larger SaaS stack or a messier control environment. If scope expands, reprice before work starts, not after the invoice gets questioned.

One clean rule: if control implementation needs more than the planned hours, reset the fee or narrow the deliverable. That protects gross margin, keeps cash flow steadier, and makes owner pay more predictable. The goal is not just a higher rate; it’s a cleaner mix of project fees and recurring retainers.

- Track hours by service line.

- Separate consulting from audit fees.

- Reprice scope creep fast.

1

Billable Capacity And Utilization

Billable Capacity And Utilization

Utilization rate is billable hours divided by available hours, so it shows how much team time turns into revenue. In this model, readiness work falls from 40 hours in Year 1 to 32 hours in Year 5, while retainer work stays at 10 hours and advisory stays at 5 hours. Owner income improves when senior staff stay billable and the owner stops being the only growth gate.

If utilization drops, payroll stays fixed while revenue slips, and owner draw gets squeezed fast. If utilization runs too hot, burnout lifts rework and churn risk, which delays billing and weakens cash flow. Idle hours cost money, but overloaded hours can cost clients.

Keep Billable Time Near Capacity

Track available hours, billed hours, and rework hours each week. Split them by readiness, retainer, and advisory so you can see whether the business is moving from 40-hour project work toward steadier 10-hour and 5-hour work that supports cash flow.

- Measure owner billable share.

- Cap nonbillable admin time.

- Protect senior staff from overload.

Use this test: utilization = billable hours / available hours. If the owner is the main biller, growth stalls when delivery maxes out; if senior staff carry the work, the owner can sell, review, and keep scope tight. What this hides is quality drift: more hours billed do not help if rework or churn forces unpaid fixes.

2

Delivery Staffing And Leverage

Delivery Staffing And Leverage

SOC 2 consulting delivery margin depends on the staffing model. Year 1 payroll is $745K across the Managing Principal, senior consultants, analyst, account executive, and operations manager; by Year 5, payroll reaches $2835M. Hiring can raise revenue from $138M to $791M, but weak utilization or pricing still cuts percentage margin and leaves less cash for owner pay.

The inputs that matter are role mix, billable hours, utilization, pricing, and rework. If senior staff spend too much time on basic delivery, margin after labor falls and the owner’s draw gets squeezed fast.

Track Labor, Not Just Rates

Use employees for repeatable delivery and specialists for review. That keeps higher-paid people on control design, exception handling, and final checks, not template work. Track margin after labor by client and service line, because a strong billing rate can still miss if payroll sits idle.

- Watch utilization by role each month

- Separate delivery hours from review hours

- Price control work before scope expands

When utilization drops, payroll stays fixed and owner profit falls fast. When pricing is too low, the team can stay busy and still leave little distributable cash. Keep the mix lean enough to stay busy, but deep enough to protect quality.

3

Recurring Retainer Revenue

SOC 2 Retainer Revenue

Retainers smooth cash flow because the work repeats every month, so the owner is not waiting on one-off projects to fund payroll. With 10 hours × $200 = $2,000 per month in Year 1 and 10 hours × $240 = $2,400 per month in Year 5, the mix shift from 20% to 80% makes revenue more predictable and raises the chance of steady owner pay.

What matters is scope. Strong retainers cover evidence collection, control monitoring, policy updates, and audit readiness. If the scope is loose, the same hours turn into low-margin support work, which can push up rework and cut distributable profit fast.

Scope the Retainer

Track the inputs that set the monthly retainer: hours billed, hourly rate, retainer mix, and scope boundaries. Here’s the quick math: more retained hours at a higher rate means more recurring revenue, but only if the work stays tied to compliance tasks, not open-ended support.

Use a simple scope list in every agreement so the client knows what is included and what is extra. Measure how often retainer work drifts into ad hoc requests, because that is where margin leaks. A clean retainer should help cash flow first, then free the owner to pay themselves from stable monthly profit.

4

Client Acquisition And Sales Pipeline

Client Acquisition Efficiency

For SOC 2 consulting, client acquisition drives revenue consistency and owner time. With $120K in Year 1 marketing and $4,500 CAC, the model supports about 267 acquired clients; by Year 5, $400K and $3,500 CAC support about 1,143 acquired clients. If CAC falls and close quality stays high, more sales turn into owner income instead of more selling hours.

This driver includes marketing spend, lead volume, close rate, and fit in SaaS, fintech, healthcare technology, and B2B vendors that need SOC 2 reports for sales. Lower CAC helps only when those clients are the right fit; weak-fit wins create rework, slow billing, and pull the owner back into the pipeline.

Track CAC and close quality

Watch CAC, lead source, close rate, and owner sales hours. The quick math is simple: client count equals marketing budget ÷ CAC. A cheaper lead th at does not close still burns cash, and a bad-fit client can hurt margin more than it helps revenue.

- Track CAC by channel.

- Score fit before demos.

- Measure close rate monthly.

- Review owner sales hours.

5

Operating Costs, Quality, And Cash Reserves

Operating Costs, Quality, and Cash Reserves

When overhead runs at $155K per month and the model also lists $186K per year, the monthly run-rate is the cash planning anchor. Add 12% platform licensing, 5% referral fees, 7% commissions, and 3% travel, and more revenue does not automatically mean more owner pay.

Quality slips hurt twice: they create rework and push billing later. The minimum cash need is $519K in Month 8, and payback takes 33 months, so reserves are not optional if the owner wants steady draws.

Protect Margin and Cash

Track three numbers every month: rework hours, days to invoice, and cash on hand versus the $519K Month 8 need. Here’s the quick math: the listed variable costs add up to 27%, before fixed overhead. So if quality fixes keep repeating, they hit margin and delay cash at the same time.

- Measure rework by client.

- Invoice at each milestone.

- Separate scope changes fast.

- Hold cash for 33 months.

If collections slip, protect the reserve before owner distributions. That keeps payroll, delivery, and audit prep funded while the team cleans up issues that would otherwise erase profit.

6

Compare SOC 2 owner income scenarios without treating them as promises

Owner income scenarios

Owner income starts with salary in Year 1, then rises as retainers and utilization improve. Revenue can outpace owner draws because payroll, marketing, CAC, and reserves take cash first.

| Scenario | Low CaseDownside | Base CaseSteady | High CaseUpside |

|---|---|---|---|

| Launch model | Year 1 stays salary-led because EBITDA is still negative and cash needs are high. | By Year 3, owner income can add a limited draw after the business reaches positive EBITDA. | By Year 5, stronger utilization can support the largest owner draw, but only after reinvestment and cash reserves. |

| Typical setup | Revenue is $1.38M in Year 1, EBITDA is -$159K, the owner takes a $185K salary, and no distribution is assumed while cash stays protected. | Revenue reaches $4.262M in Year 3 and EBITDA rises to $652K, but payroll, commissions, travel, and reserves still keep distributions below top-line growth. | Revenue reaches $7.910M in Year 5 and EBITDA reaches $2.136M, with gross margin improving from 83% to 89% as licensing and referral fees fall. |

| Cost drivers |

|

|

|

| Owner income rangeBefore owner reserves | $185,000Income floor | Salary plus limited drawBase income | Salary plus larger drawUpside income |

| Best fit | Use this to stress-test the first operating year when growth is still absorbing cash. | Use this for a normal growth plan where the firm is profitable but still funding staff and working capital. | Use this to test upside if the firm scales smoothly and keeps cash needs under control. |

Planning note: These scenario ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions.

Related Products

- SOC 2 Compliance Consulting Porter's Five Forces Analysis

- SOC 2 Compliance Consulting BCG Matrix

- SOC 2 Compliance Consulting Business Model Canvas

- What Are The 5 KPIs For SOC 2 Compliance Consulting Business?

- SOC 2 Compliance Consulting Business Plan Template in Pre-Written Word

- How Increase Profits For SOC 2 Compliance Consulting?

- What Are Operating Costs For SOC 2 Compliance Consulting?

- SOC 2 Compliance Consulting Startup Costs: $519K Launch Budget

- SOC 2 Compliance Consulting Financial Model Template in Excel

- How To Start A SOC 2 Consulting Firm In 6 To 12 Weeks

- How To Write A Business Plan For SOC 2 Compliance Consulting?

- SOC 2 Compliance Consulting Marketing Mix

- SOC 2 Compliance Consulting Marketing Plan

- SOC 2 Compliance Consulting Business Proposal

- SOC 2 Compliance Consulting PESTEL Analysis

- SOC 2 Compliance Consulting Pitch Deck Example Editable PPTX

- SOC 2 Compliance Consulting Business SWOT Analysis

- SOC 2 Compliance Consulting Value Proposition Canvas

Frequently Asked Questions

The model starts with a $185K Managing Principal salary Profit distributions depend on EBITDA, cash reserves, taxes, and reinvestment In the researched case, EBITDA is -$159K in Year 1, $240K in Year 2, and $2136M in Year 5, so early take-home is salary-led