Owner income$115k

Owner income$115kHow Much Can a Disability Advocacy Owner Make? $115k Salary Model

Fully Editable

Instant Download

Professional Design

Pre-Built

No Expertise Is Needed

Description

Owner income$115k  Net margin-106% to 546%

Net margin-106% to 546% Revenue for target pay$488k

Revenue for target pay$488k Business difficultyHard

Business difficultyHard

A Social Security Disability advocacy business owner can model a $115,000 salary, but extra take-home depends on collected fees and cash reserves In this forecast, revenue rises from $488k in Year 1 to $3382M in Year 5, while estimated EBITDA moves from about -$52k to about $1846M before taxes, debt service, reserves, and distributions Here’s the quick math: Year 1 revenue of $488k less 27% variable costs, $296k payroll, $45k marketing, and $672k fixed overhead leaves a first-year operating loss Timing matters because claims, appeals, and fee processing can delay cash even when the pipeline looks strong

Owner income$115kNet margin-106% to 546%Revenue for target pay$488kBusiness difficultyHardWant to test your owner pay?

Owner income calculator

Estimate owner take-home and target-pay gap from revenue, margin, costs, reserves, and target pay.

Planning note: Research-based planning estimate only, not guaranteed salary, tax advice, or owner distribution advice.

Want to see owner income in the full forecast?

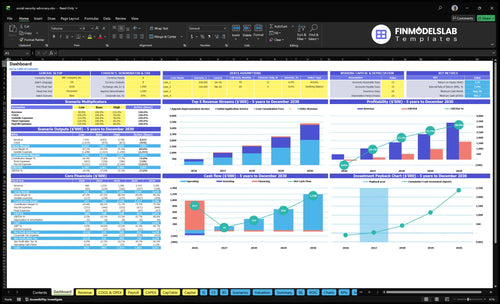

The Social Security Disability Advocacy Financial Model Template screenshot shows revenue, margin, costs, reserves, and owner take-home assumptions—open the model to review the full forecast.

Owner-income model highlights

- Owner take-home shown

- Revenue and margin trend

- Scenario tests timing

How much profit does a Social Security Disability advocacy business make?

A Social Security Disability Advocacy business can show an accounting loss early even when the owner is paid: this model has -$52k EBITDA in Year 1 and about $1.846M EBITDA in Year 5, before taxes, debt service, reserves, capex, and distributions; track the drivers in What Are The 5 KPIs For Social Security Disability Advocacy Business?. Profit is not owner pay here because $115k owner salary is already inside payroll.

Year 1 Math

- $488k revenue

- 27% variable costs

- $296k payroll

- $45k marketing

Cash Pressure

- Lead generation absorbs cash

- Case management adds labor

- Software and records cost money

- Delayed collections slow profit

How do Social Security Disability advocates get paid?

If you're sizing up How To Launch Social Security Disability Advocacy Business?, the money usually comes from hourly work and, in some cases, from past-due benefits after approval under Social Security Administration fee rules. Using $175 to $200 for initial application work, $225 to $260 for appeals, and $150 to $175 for consultations, the modeled fee rises to about $813 to $1,263 per matter. Check current fee limits and approval rules directly with the agency; this is business-model context, not legal advice.

Fee mix

- Hourly work drives cash flow.

- Initial work runs $175 to $200.

- Appeals run $225 to $260.

- Consults run $150 to $175.

Payment rules

- Some pay comes after approval.

- Past-due benefits can fund fees.

- Agency caps can limit collections.

- Verify rules before quoting clients.

Can a Social Security Disability advocacy business scale?

Yes—Social Security Disability Advocacy can scale, but only if intake, documentation, case work, and quality control grow with the case load. Here’s the quick math: payroll rises from $296k to $652k, and appeals stretch from 60 hours to 70 hours per matter. Training, medical-record follow-up, hearing prep, denials, appeals, and collection lag are the real bottlenecks. Owner-led firms can protect margin, but they also cap capacity.

What has to scale

- Intake must screen fast

- Documentation needs tight follow-up

- Case work needs trained staff

- Quality control must catch gaps

What slows growth

- Appeals take 70 hours per matter

- Payroll climbs to $652k

- Collection lag delays cash

- Owner-led capacity stays limited

Want the six income drivers?

1

$488K-$3.38MQualified Intake

More qualified claimants fill the pipeline, spread fixed payroll and rent, and lift owner pay fast.

2

$813-$1,263Fee Mix

A higher collected fee per closed case means each win covers more overhead and leaves more cash for the owner.

3

35%-45%Appeals Share

A bigger appeals share lifts the weighted fee, so each closed case can support more owner income.

4

27%-20%Margin Lift

Lower variable costs keep more of each fee after records, experts, referrals, and software are paid.

5

$296K-$652KPayroll Load

Payroll is the biggest scaling drag, so staffing efficiency decides how much new revenue turns into profit and owner pay.

6

$450-$360CAC Quality

A lower CAC means the larger $45K to $140K marketing budget buys more qualified cases for each dollar spent.

Social Security Disability Advocacy Core Six Income Drivers

Qualified Claimant Intake

Qualified Claimant Intake

Owner pay starts with signed qualified claimants, not raw inquiries. The key math is the move from inquiry to intake to signed representation agreement, because only qualified files create billable work. If intake screens out poor-fit cases early, the team spends less time on files with no fee potential and more time on matters that can produce collected revenue and profit.

Track inquiry-to-intake rate, qualified intake rate, signed representation agreements, and customer acquisition cost (CAC) by source. Here’s the quick logic: better source quality can support marketing rising from $45k to $140k while CAC improves from $450 to $360. Unqualified leads still burn staff time, so screening work history, claim stage, documentation readiness, and service fit protects margin.

Measure Signed-Case Quality

Build intake around a short qualify-or-reject screen before assigning case staff. Ask for work history, claim stage, medical records, and whether the client fits the service scope. That keeps intake from getting clogged with cases that cannot turn into fees, which helps cash flow and keeps owner pay tied to signed, usable matters.

Watch source quality by referral channel, not just lead count. If one channel sends more signed claimants at a lower CAC, it deserves more budget; if another sends noise, it steals time and raises labor cost. The goal is simple: fewer junk leads, more signed qualified claimants.

- Track signed agreements by source

- Review intake drop-off weekly

- Reject poor-fit cases fast

1

Approval And Appeal Mix

Appeal Mix Load

This driver is the mix of initial applications, appeals, and consultations. In Year 1, the mix is 50%, 35%, and 15%; by Year 5 it shifts to 55%, 45%, and 10%. Appeals take 60 hours in Year 1 and 70 hours in Year 5, versus 35 to 38 hours for initial applications, so a higher appeal share can lift fee upside but also slow cash and tie up staff.

No approval outcome is guaranteed, so this mix matters most when you track signed matters, case stage, and hours per file. More appeals usually mean more work before cash lands, which can squeeze owner pay if payroll rises faster than collections.

Track Hours by Stage

Measure signed cases, case stage mix, hours per appeal, and hours per initial application. Also watch how long cash takes to arrive on appeal-heavy files. If appeals move from 35% toward 45%, staff to the slower workflow before you add owner draws.

One clean check: more appeals need more working capital. Use stage-level time logs, then test whether the higher fee potential beats the extra labor and delay. If appeal prep keeps pushing files past normal billing cycles, tighten intake, document checklists, and staffing so the mix does not eat margin.

- Log hours by case stage.

- Track cash lag by file type.

- Forecast staffing before mix shifts.

2

Average Fee Collected Per Case

Average Fee Per Case

When you’re signing real cases, not just leads, average collected fee per matter is what turns work into owner pay. The model shows weighted fee rising from about $813 in Year 1 to $1,263 in Year 5, a gain of $450 or about 55%. That higher fee per successful matter gives more room for profit after payroll and overhead.

The fee mix drives the number: initial applications model at $613 to $760, appeals at $1,350 to $1,820, and consultations at $225 to $263. What this estimate hides: approval rates and exact contingency fee collections are not provided, so actual cash depends on case type, fee caps, past-due benefits, and when money is collected.

Track Fee Yield by Case Type

Measure collected fee per closed matter by initial application, appeal, and consultation. That tells you whether the firm is earning the assumed weighted average or slipping into lower-value work that drags down cash flow. Use one simple rule: if the mix shifts toward consultations, the average fee falls fast.

Watch fee agreements, allowed caps, past-due benefit size, and collection timing on every file. The useful inputs are case stage, signed agreement, billed amount, collected amount, and days to cash. If appeals collect closer to the $1,820 end, owner distribution capacity rises; if collections lag, profit can look fine on paper but stay tight in cash.

3

Fee Collection Timing And Cash Flow

Fee Collection Timing

Fee collection timing controls when booked work turns into spendable cash. This model hits its minimum cash point in Month 8 at $802k, while Year 1 EBITDA, or earnings before interest, taxes, depreciation, and amortization, is about -$52k before taxes and reserves. That gap matters because costs start early: $296k payroll, $45k marketing, and $672k fixed overhead.

Separate the booked pipeline from cash received. Longer claims, appeals, fee review, and denied matters push owner distributions later, so a file can look profitable and still leave the bank account tight. If reserves are thin, skip extra owner draws and protect working cash first.

Protect Cash Before Owner Pay

Track signed cases, billed work, and cash collected each month. Then compare collections by stage, because appeal-heavy work usually lags initial claims. Forecast the next 90 days from collection timing, not just booked revenue, so you can spot when cash will fall behind profit.

Set a reserve policy before any draw. Keep enough cash to cover early payroll, marketing, and overhead, then release owner pay only after the reserve target is met. If fee reviews or denied matters slow collections, tighten billing follow-up before raising distributions.

4

Staffing And Case-Management Efficiency

Case Workflow Efficiency

This driver is about how many claim files each staff member can move without hurting quality. Payroll is modeled to rise from $296k in Year 1 to $652k in Year 5, so payroll has to trail collected revenue or owner pay gets squeezed. The key inputs are active caseload per case manager, records turnaround, appeal prep time, intake completion rate, and rework rate.

With hourly billing, better workflow can lift billable throughput, but only if cases move cleanly through intake, evidence gathering, hearing prep, and storage. One slow step can turn into extra admin hours and delayed cash, so margin depends on tighter handling, not just fewer staff.

Measure throu ghput before adding headcount

Track active caseload per case manager, records turnaround, and appeal prep time every month. Also watch intake completion rate and rework rate; those show where staff time leaks. If intake is weak or files are messy, add checklists, medical record follow-up, hearing prep workflows, and secure storage before hiring more people.

Case-management software should reduce handoffs and missing docs, not just store files. The test is simple: if payroll grows faster than collected revenue, the workflow is too heavy for the case load. Keep staffing tied to billable files, not inquiries.

- Case manager caseload

- Records turnaround time

- Appeal prep hours

- Intake completion rate

- Rework rate

5

Marketing Cost And Referral Quality

Marketing Cost And Referral Quality

Owner income improves when marketing produces signed qualified claimants, not just inquiries. Spend rises from $45k in Year 1 to $140k in Year 5, while CAC improves from $450 to $360; that only helps if the cases are fee-producing. Weak leads still use intake time, software, and staff hours without enough collected fees.

Track cost per signed claimant, qualified lead rate, referral conversion, and collected revenue per channel. The inputs are simple: lead source, screening result, signed agreement, and fees actually collected. If paid search or community outreach brings volume but poor fit, it can raise work load and cut owner pay even when top-line lead counts look strong.

Measure Fee-Per-Channel

Judge each channel by collected-fee return, not raw lead count. Referral partners, local partnerships, paid search, content, and community outreach should each show a clear link from lead to signed case to collected revenue; if they do not, trim spend fast.

- Track signed claimants by source.

- Score qualified lead rate weekly.

- Measure collected revenue per channel.

- Reject vanity leads early.

6

Compare lean, base, and high-growth owner income cases

Owner income scenario table

Lower intake and a higher CAC can keep Year 1 owner pay close to salary, while Year 2 through Year 5 scale makes cash timing, staffing, and reserves the real swing factor.

| Scenario | Low CaseLow Case | Base CaseBase Case | High CaseHigh Case |

|---|---|---|---|

| Launch model | This is the lower owner-income path, where early intake stays slow and cash pressure limits pay flexibility. | This is the modeled path, where the business clears early pressure and owner income starts to track steady scale. | This is the stronger earnings path, where scale lifts owner income after the team and systems are in place. |

| Typical setup | Year 1 revenue is $488k, variable costs run about 27%, and EBITDA is about -$89k, so the owner mostly depends on the $115k CEO salary and cash reserves. | Year 2 revenue reaches $1.034M and Year 3 reaches $1.586M, with EBITDA improving from $198k to $528k as intake, staffing, and pricing scale. | Year 4 revenue reaches $2.335M and Year 5 reaches $3.382M, with EBITDA rising from $973k to $1.651M as volume, referrals, and staffing scale. |

| Cost drivers |

|

|

|

| Owner income rangeBefore owner reserves | $115k salaryLow Case | $198k - $528k EBITDABase Case | $973k - $1.651M EBITDAHigh Case |

| Best fit | Use this to test a slower start, tighter cash, and what happens if intake does not ramp fast. | Use this as the main planning case for budgeting, hiring, and reserve targets. | Use this to stress-test upside, capacity limits, and how much cash the owner can actually take out. |

Planning note: These scenario ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions.

Related Products

- Social Security Disability Advocacy Porter's Five Forces Analysis

- Social Security Disability Advocacy BCG Matrix

- Social Security Disability Advocacy Business Model Canvas

- What Are The 5 KPIs For Social Security Disability Advocacy Business?

- Social Security Disability Advocacy Business Plan Template in Pre-Written Word

- How Increase Profits In Social Security Disability Advocacy?

- What Are Social Security Disability Advocacy Operating Costs?

- Social Security Disability Advocacy Startup Costs: Plan Around $802K

- Social Security Disability Advocacy Financial Model Template in Excel

- How To Open A Social Security Disability Advocacy Business In 6-12 Weeks

- How Do I Write A Business Plan For Social Security Disability Advocacy?

- Social Security Disability Advocacy Marketing Mix

- Social Security Disability Advocacy Marketing Plan

- Social Security Disability Advocacy Business Proposal

- Social Security Disability Advocacy PESTEL Analysis

- Social Security Disability Advocacy Pitch Deck Example Editable PPTX

- Social Security Disability Advocacy Business SWOT Analysis

- Social Security Disability Advocacy Value Proposition Canvas

Frequently Asked Questions

The model includes a $115,000 annual owner salary Extra take-home depends on profit after reserves, taxes, debt service, and cash needs EBITDA is about -$52k in Year 1, then about $268k in Year 2 and $1846M in Year 5, before those deductions Don’t treat EBITDA as spendable cash