Owner income$14k/mo

Owner income$14k/moHow Much Specialty Hot Sauce Owners Make From 30K Bottles

Fully Editable

Instant Download

Professional Design

Pre-Built

No Expertise Is Needed

Description

Owner income$14k/mo  Net margin45%

Net margin45% Revenue for target pay$31.3k/mo

Revenue for target pay$31.3k/mo Business difficultyMedium

Business difficultyMedium

You’re trying to turn bottle sales into real owner pay, not just top-line revenue This covers $375,000 in first-year revenue from 30,000 bottles, listed production costs, gross margin, payment fees, operating cost gaps, reserves, and take-home logic for a US small-batch hot sauce business

Owner income$14k/moNet margin45%Revenue for target pay$31.3k/moBusiness difficultyMediumWant to test your owner pay?

Owner income calculator

Estimate owner take-home and the target-pay gap from revenue, margin, costs, reserves, and target pay.

Planning note: Research-based planning estimate only. It is not guaranteed salary, tax advice, or owner distribution advice.

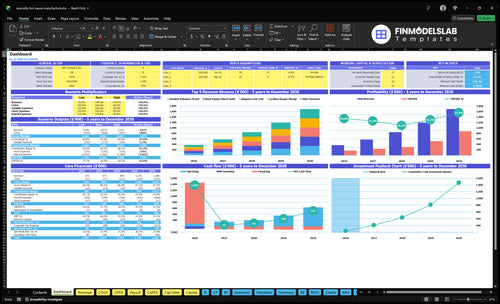

Can you check owner income in the Specialty Hot Sauce model?

Yes—this screenshot shows revenue, margin, costs, reserves, and owner take-home assumptions. Open the Specialty Hot Sauce Financial Model Template.

Owner-income model highlights

- Owner pay output

- Revenue and contribution

- Scenarios and assumptions

Can you make a living selling hot sauce?

Yes, Specialty Hot Sauce can pay a living, but only if contribution covers overhead, owner labor, reserves, and reinvestment. Here’s the quick math: the first-year case shows $375,000 in revenue and about $313,500 in contribution before unmodeled overhead, marketing, taxes, and reserves. The mature-year case shows 125,000 bottles at $13.50 each, or $1,687,500 in revenue and about $1,432,000 in contribution, so full-time income is possible if repeat orders, fulfillment labor, and cash timing hold.

First-year math

- $375,000 revenue

- $313,500 contribution

- Before overhead and taxes

- Local sales can fund cash flow

Mature-year math

- 125,000 bottles sold

- $1,687,500 revenue

- $1,432,000 contribution

- Scale needs repeat orders

How do wholesale and direct-to-consumer sales change hot sauce profit?

Specialty Hot Sauce usually makes better gross margin in direct-to-consumer sales because it keeps more net price per bottle, but wholesale can still win if volume is high enough to offset the lower net. For the cost setup behind that mix, see How Much Does It Cost To Open, Start, And Launch Your Specialty Hot Sauce Business?; the $1,250 first-year source price is only a list figure, not income.

DTC margin

- Keeps more net price per bottle

- Adds 28% payment processing

- Also adds shipping and packaging

- Returns and service cut margin

Wholesale tradeoff

- Moves more units

- Reduces net price through discounts

- Distributor margin and promos bite

- Judge by contribution margin and workload

Cost base

- $145 unit COGS in year one

- Add 20% production-linked costs

- Payment processing takes 28%

- Unmodeled channel costs still matter

Best test

- Compare net dollars per bottle

- Compare cash after fees

- Compare owner time per order

- Pick the mix that pays back

Should I make hot sauce myself or use a co-packer?

If Specialty Hot Sauce is tight on cash, make it yourself; if it’s hitting capacity, use a co-packer. This is a cash-flow and capacity call, not a universal rule. Here’s the quick math: the model puts commercial kitchen rental at 0.5% of revenue, co-packer overhead at 0.5%, production utilities at 0.3%, quality control testing at 0.3%, and equipment maintenance at 0.4%—about 2.0% total on those lines.

Make it yourself

- Saves cash upfront

- Uses founder time

- Limits batch volume

- Adds scheduling work

Use a co-packer

- Improves consistency

- Supports larger runs

- Needs inventory cash

- Fits stronger demand

Want the six drivers behind owner income?

1

30K-125KBottle Volume

Units rise from 30,000 in year 1 to 125,000 in the mature year, so this is the main lever on revenue and on how much fixed cost gets spread per bottle.

2

$12.50-$13.50Net Price

Net price moves from $12.50 to $13.50, and that extra dollar drops into gross profit if demand holds.

3

$1.45-$1.74Bottle Cost

Unit COGS is $1.45 before a 20% production-linked load, so small savings here compound across every bottle sold.

4

EditableChannel Mix

Direct, wholesale, events, marketplaces, and foodservice do not pay the same margin, so the sales mix can lift or cut take-home fast.

5

EditableMarketing CAC

CAC is editable, and if it climbs faster than order value, growth can look good on top line but still hurt owner cash.

6

$3.1K/moOverhead Scale

Office admin, insurance, software, and the rest of the fixed load run about $3.1K a month, and added scale costs decide how much EBITDA reaches the owner.

Specialty Hot Sauce Core Six Income Drivers

Bottle Sales Volume

Bottle Sales Volume

Bottle sales volume is the main revenue engine here: 30,000 bottles in year one works out to about 2,500 bottles per month, and 125,000 bottles in the mature year is about 10,417 per month. That unit flow sets the cash pool that can cover labor, shipping, marketing, overhead, and owner pay. If volume slips, income drops fast.

Profitable volume matters more than raw units. Repeat buyers, farmers markets, online sales, retail sell-through, and foodservice orders all help, but only if fulfillment, labor, inventory, and channel margin stay in control. Slow sell-through ties up cash in finished goods, so the owner can be “busy” and still not have enough profit to take home.

Track sell-through, not just shipments

Measure bottles sold by channel, sell-through rate, and days of inventory on hand. If monthly sales stay near 2,500 bottles but inventory keeps climbing, cash is getting stuck on the shelf instead of turning into owner income. That can delay reorders and shrink the draw available to the owner.

- Track monthly units by channel

- Watch inventory days each week

- Compare labor hours per bottle

- Test margin after fees and packing

Use the channels that move volume fast enough to keep stock fresh. A higher run rate only helps when each bottle turns into cash on time and the added sales do not create more labor than the margin can support.

1

Average Net Price Per Bottle

Average Net Price Per Bottle

Average net price is the cash kept per bottle after discounts, bundles, free shipping, wholesale cuts, platform fees, and distributor allowances. At 30,000 bottles, a $12.50 net price gives $375,000 in year-one revenue. At 125,000 bottles, a $13.50 net price gives $1,687,500. Shelf price doesn’t pay the bills; net cash does.

This driver shapes owner pay because every $1.00 drop in net price cuts mature-year revenue by $125,000. Even a $0.50 leak removes $62,500. The main inputs are list price, channel mix, discount depth, and shipping or fee policy, since they decide what stays in the business after the sale.

Protect Net Price

Track net dollars per bottle by channel, not just sticker price. Split direct online, events, wholesale, and foodservice, then record the cash kept after fees and allowances. A busy channel that nets less can still drag down profit and owner draw. Cash landed is the number that matters.

Test bundle depth, free-shipping thresholds, and wholesale terms with a simple rule: keep blended net price near $12.50 in year one and $13.50 in the mature year. Watch the gap between shelf price and banked cash each month, because that gap shows how much income is being given away.

- Track net price by order

- Separate channel deductions

- Limit blanket discounts

- Review shipping subsidies

- Model wholesale allowances

2

Sales Channel Mix

Sales Channel Mix

Sales channel mix changes how much of each bottle actually reaches the owner. Direct ecommerce can keep more net price, but payment fees, packaging, postage, customer service, and ad spend eat into it. Wholesale can raise unit volume, yet lower per-bottle contribution and stretch cash timing.

Events can create repeat buyers, but booth fees and owner time matter. Foodservice can create steadier demand, but larger packs or custom pricing can cut margin. The key measure is contribution after channel costs, not sales alone.

Track channel contribution

Build one view for each channel: units, net price, fees, freight, packaging, ad spend, labor, and days to cash. Then compare gross sales to cash contribution per bottle. If a channel sells fast but leaves little after costs, it can still reduce owner pay.

- Units by channel

- Net price after discounts

- Fees, freight, and packaging

- Labor time and cash timing

Use a simple test: contribution = revenue - channel costs. Review it monthly, and cut or reshape any channel that boosts volume but pulls down cash profit. If it doesn't create cash after fees, it doesn't pay you.

3

Cost Per Bottle

Cost Per Bottle

If your cost per bottle sits near $145, that number sets how much gross profit each sauce bottle can create before overhead. The disclosed product-level range of $135 to $155 means a $20 swing per bottle, which is huge once volume scales.

Here’s the quick math: at 125,000 bottles a year, every $1 change in unit COGS moves annual gross profit by $125,000. But gross margin is not owner pay; kitchen rent, co-packer overhead, utilities, quality control, maintenance, marketing, reserves, and taxes still come after that.

Track Bottle COGS

Measure COGS by batch and by bottle, not just in one monthly total. Break it into raw ingredients, glass bottles and caps, labels and seals, direct labor, and shipping packaging, then compare each run against the $135 to $155 band.

- Track ingredient yield loss.

- Track bottle and cap scrap.

- Track labor minutes per batch.

- Track freight per finished bottle.

- Track QC rejects and rework.

If production-linked costs run near 20% of revenue, watch kitchen rent, co-packer overhead, utilities, QC, and maintenance the same way you watch ingredients. If those inputs drift up, raise price, cut waste, or resize batches before owner draw gets squeezed.

4

Marketing Efficiency

Marketing Efficiency

Marketing efficiency is what turns paid ads, influencer seeding, samples, market booth fees, email repeat purchase, and discounts into profit. The model does not give marketing spend, so treat it as an editable assumption and test customer acquisition cost (what it costs to win one buyer), repeat purchase rate, and promo discount. Growth helps owner pay only when contribution after marketing still covers reserves and owner pay.

In specialty hot sauce, discounting can lift orders but cut cash fast. If a channel brings sales with weak repeat purchase or slow payback, it can raise revenue and still lower take-home income. Track payback by channel so paid ads and events do not outrun gross margin. More sales is not more pay if marketing eats the margin.

Track CAC and payback

Measure each channel by cost per new customer, repeat rate, and net revenue after discounts. Keep the math simple: channel sales minus marketing cost equals contribution, then compare that to fixed overhead and owner draw. If email repeat sales are cheap and paid ads are costly, shift budget toward the lower-cost source that still keeps contribution positive.

- CAC by channel

- Repeat purchase rate

- Discount %

- Payback period

5

Fixed Overhead And Production Scale

Fixed Overhead and Production Scale

Fixed overhead is the cost layer that sits between gross margin and owner pay: insurance, licenses, storage, ecommerce tools, bookkeeping, rent, payroll, and any owner salary. In this model, product COGS averages $145 per bottle and production-linked costs add 20% of revenue, but the full overhead is not provided, so take-home income can’t be sized from gross margin alone.

Scale helps only if contribution rises faster than cash gets trapped in batches. At 30,000 bottles a year, that’s about 2,500 a month; at 125,000, it’s about 10,417 a month. More volume can lower unit strain, but it also raises ingredient buys, finished-goods inventory, and the risk of slow retail cash coming in after the production run is already paid.

Track Overhead Before You Scale

Measure overhead as a monthly dollar amount and as % of contribution. Here’s the quick math: if a new batch adds sales but also adds storage, labor, and shipping delays, the owner only wins if cash left after $145 unit cost, 20% production-linked costs, and overhead still covers pay and reserves.

Track these inputs on every run: units produced, units sold, cash tied in inventory, owner hours, and payment timing. Watch the unit range from $135 to $155 COGS, then test whether larger batches reduce strain or just increase cash risk. Stable pay needs enough cushion for ingredient buys, production runs, and seasonal swings.

- Count overhead every month.

- Separate cash cost from unpaid labor.

- Watch inventory days on hand.

- Forecast batch cash before production.

6

Compare lean, base, and scaled hot sauce owner-pay scenarios

Owner income scenarios

Owner income changes fast here because volume, unit price, and variable costs scale together. These figures use contribution before overhead and reserves, so fixed costs can still pull take-home lower.

| Scenario | Low CaseLow Case | Base CaseBase Case | High CaseHigh Case |

|---|---|---|---|

| Launch model | This is the lower-income path with first-year scale and modest pricing. | This is the modeled middle path with steady Year 3 volume and pricing. | This is the stronger earnings path with mature-year volume and higher pricing. |

| Typical setup | Year 1 reaches 30,000 bottles at $12.50 each, with $375,000 revenue, $43,500 unit COGS, $7,500 production-linked costs, and $10,500 payment fees before overhead. | Year 3 reaches 65,000 bottles at $13.00 each, with $845,000 revenue and about $711,880 contribution before overhead and reserves. | In the mature year, volume reaches 125,000 bottles at $13.50 each, with $1,687,500 revenue and about $1,432,000 contribution before overhead and reserves. |

| Cost drivers |

|

|

|

| Owner income rangeBefore owner reserves | $313,500Low Case | $711,880Base Case | $1,432,000High Case |

| Best fit | Use this to stress-test early demand, thin margins, and slower sell-through. | Use this as the core planning case for a growing multi-flavor line. | Use this to test upside if demand, production, and distribution all hold up. |

Planning note: These scenario ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions.

Related Products

- Specialty Hot Sauce Porter's Five Forces Analysis

- Specialty Hot Sauce BCG Matrix

- Specialty Hot Sauce Business Model Canvas

- 7 Essential KPIs for Specialty Hot Sauce Founders

- Specialty Hot Sauce Business Plan Template in Pre-Written Word

- 7 Strategies to Increase Specialty Hot Sauce Profitability Now

- How Much Does It Cost To Run A Specialty Hot Sauce Business Monthly?

- How Much It Costs To Start A Specialty Hot Sauce Business With $43K+ CAPEX

- Specialty Hot Sauce Financial Model Template in Excel

- How To Open A Specialty Hot Sauce Business In 3 To 6 Months

- How to Write a Specialty Hot Sauce Business Plan in 7 Steps

- Specialty Hot Sauce Marketing Mix

- Specialty Hot Sauce Marketing Plan

- Specialty Hot Sauce Business Proposal

- Specialty Hot Sauce PESTEL Analysis

- Specialty Hot Sauce Pitch Deck Example Editable PPTX

- Specialty Hot Sauce Business SWOT Analysis

- Specialty Hot Sauce Value Proposition Canvas

Frequently Asked Questions

In the provided model, revenue starts at $375,000 in the first year from 30,000 bottles at $1250 It grows to $1,687,500 in the mature year from 125,000 bottles at $1350 Revenue is not owner income because COGS, fees, overhead, reserves, taxes, and reinvestment come first