Stored Value Card Program Startup Costs: $12M Year 1 Marketing

Key Takeaways

- Legal setup needs $8k monthly, plus pre-launch work.

- Bank approval fees start high and need quotes.

- Tech costs split between setup, hosting, and processing.

- Staffing, insurance, and support drive ongoing runway.

Estimate Startup Costs with Calculator

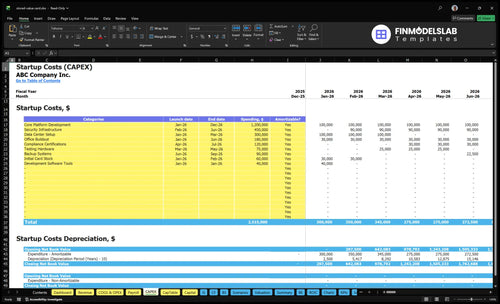

Startup CAPEX Calculator

Estimates capitalized startup assets only for a stored value card program, so you can size launch spend before adding payroll, marketing, or other operating cash needs.

Excluded funding needs This calculator includes only capitalized startup assets. It excludes payroll runway, marketing, deposits, reserves, collateral, cardholder funds, debt service, working capital, legal fees, sponsor bank fees, and other operating costs; keep the $575k monthly overhead and $12M Year 1 marketing anchor separate.

How does the Stored Value Card Program model show startup costs?

This Stored Value Card Program Financial Model Template financial model tab shows startup expense categories and CAPEX, launch timing, and depreciation/amortization. Open it and adjust assumptions.

Screenshot highlights

- CAPEX and startup costs

- Compliance and onboarding schedules

- Working capital and reserves

- Revenue and transaction costs

- Runway and funding need

What hidden costs come with launching a stored value card program?

Launching a Stored Value Card Program costs more than software and cards: the hidden bill is compliance, fraud, disputes, support, reserves, and runway, and your plan should start with How To Write A Business Plan For Stored Value Card Program? Legal and compliance setup is a pre-opening expense, reserves and collateral are funding needs, and transaction fees are ongoing operating costs. With fixed anchors of $4k insurance, $8k legal and compliance, $25k cloud hosting, $6k software licenses, and $575k total fixed overhead, cardholder funds are not normal operating revenue.

Hidden launch costs

- Compliance audits add setup cost.

- Fraud monitoring needs tools and staff.

- Dispute ops and support need readiness.

- $4k insurance and $8k compliance are fixed.

Funding buckets

- Reserves and collateral are funding needs.

- Cardholder funds are not operating revenue.

- Pre-launch payroll is working capital or pre-opening expense.

- Cloud at $25k and software at $6k raise fixed burn.

How much money do you need to start a stored value card program?

You need at least $2.52M to start a Stored Value Card Program, before capital expenditures, reserves, cardholder funds, missing staff, and variable fees; for ongoing KPI control, see What Five KPIs Should Stored Value Card Program Track?. Here’s the quick math: $1.2M marketing plus $690k fixed overhead plus $630k named executive payroll.

Funding needs

- Fund development and issuer approval

- Set up compliance and processor onboarding

- Buy card inventory and support tools

- Hold enough operating runway

Revenue inputs

- Earn $0.25 fixed commission per order

- Charge 2.75% variable commission

- Price sellers at $49, $149, $399

- Price buyers at $29, $99, $249

Why are stored value card programs expensive to launch?

A Stored Value Card Program is expensive to launch because you need more than software: you need sponsor bank due diligence, program approval, BIN access (Bank Identification Number access), network-rule review, processor coordination, legal review, AML/KYC controls, testing, transaction monitoring, and launch certification. Approval work and technical certification can overlap, but they are not the same as software development, and you can’t launch without the required bank, network, processor, and compliance sign-offs.

Launch costs stack fast

- 50% issuing bank fees in Year 1

- 40% card network fees in Year 1

- 20% payment processing fees in Year 1

- 15% customer support in Year 1

What takes time

- Legal and compliance review first

- Testing and certification before launch

- AML/KYC controls must be live

- Monitoring continues after go-live

Calculate Fuding Needs

Startup Cost Summary

This table summarizes startup CAPEX and excluded launch cash needs for the stored value card program across low, base, and high scenarios.

| Cost Category | Base Estimate | Main Cost Driver | CAPEX Calculator |

|---|---|---|---|

| Core Platform Development | $1,200,000 | Month 1-12 product build and integration scope | Yes |

| Security Infrastructure | $450,000 | Fraud controls, encryption, and security hardening | Yes |

| Data Center Setup | $300,000 | Core hosting and infrastructure setup capacity | Yes |

| Compliance Certifications | $120,000 | Regulatory testing, certification, and legal setup | Yes |

| Initial Card Stock | $60,000 | Card production and fulfillment launch volume | Yes |

| Working Capital Reserve | $4,987,000 | Operating cash needed through Month 28 breakeven | No |

Stored Value Card Program Core Five Startup Costs

Compliance And Legal Setup Startup Expense

Legal setup

A stored value card or prepaid card program needs pre-opening legal work plus ongoing monitoring. Budget for legal structuring, program agreements, AML policies, KYC procedures, consumer disclosures, privacy, escheatment, Regulation E, and state or federal review. A practical baseline is $8k per month, or $96k per year, for recurring compliance work.

What the budget covers

This cost covers counsel time to set the program rules and keep them current. Use separate inputs for launch work and monthly monitoring: scope of card type, funds flow, customer type, and bank sponsor model. That split matters because launch work is one-time, but compliance review keeps running.

- Split setup from monthly review

- Get quotes for each workstream

- Update for program changes fast

How to keep it tight

Don’t buy a one-size-fits-all license story. The right legal scope depends on structure, funds flow, card type, customer type, and bank sponsorship model. Keep the memo lean, reuse templates where counsel allows, and only pay for reviews that match the actual program design.

- Use scoped outside counsel

- Reuse approved templates

- Recheck after product changes

What drives the bill

The bill rises when the program adds more card types, more states, or more customer segments. It also rises when disclosures, disputes, AML/KYC, or privacy rules need fresh review. The cleanest estimate starts with the $8k monthly anchor and then adds separate quotes for launch-only legal work.

Sponsor Bank And Program Approval Startup Expense

Bank Setup

A sponsor bank is a real launch gate for a stored value card program. Budget for issuer due diligence, program approval, Bank Identification Number access, network rule review, processor coordination, contract review, and launch certification. Setup fees are quote-driven, so don’t force them into a generic tech line.

What It Covers

This cost pays for the bank’s onboarding work, not software build. It should capture legal, compliance, and operating review before launch, plus any testing tied to certification. Keep it separate from platform development so you can see what the bank charges versus what the product team builds.

- Due diligence and approval

- BIN access and rule review

- Contract and certification work

How To Budget

Use vendor quotes for setup, then model post-launch fees separately. The model assumes 50% issuing bank fee and 40% card network fee in Year 1, with pressure easing to 30% and 28% by Year 5. That gap matters because bank and network take-rates shape gross margin after launch.

- Separate setup from run-rate fees

- Model Year 1 and Year 5

- Test technical work, not ownership

Cost Control

Ask banks for a line-item quote, then compare scope, not just price. If certification requires technical testing, keep the bank fee in this bucket and the engineering work in technology. That split avoids double counting and makes it easier to see whether launch cost sits in the bank layer or the build layer.

Technology Platform And Processor Integration Startup Expense

Build cost

This startup cost covers the one-time platform build: card issuing setup, processor integration, admin tools, portal features, ledger, fraud rules, reporting, testing, security controls, and API work. Price it from vendor quotes and internal hours, then separate capitalizable implementation from recurring processor fees and transaction costs. The fixed operating base is $31k per month, or $372k a year.

Estimate it

Use implementation scope plus months of coverage. Add one-time configuration, then multiply recurring hosting and licenses by launch runway. Model variable payment processing at 20% in Year 1, easing to 12% by Year 5. The big question is whether virtual cards, physical cards, wallet support, and client-level controls are in scope.

- Separate build from usage fees.

- Quote API and test work.

- Confirm card types upfront.

Keep it lean

Trim spend by freezing scope early. Every extra card type or control layer adds build, test, and support time. Keep recurring fees out of the launch budget, and treat processor charges as operating cost. If the launch is narrow, you protect cash; if scope expands, reprice before you build.

Scope check

If virtual cards, physical cards, wallet support, or client-level controls are included, this line item changes fast because test cases, fraud rules, and support paths multiply. Lock the scope before coding starts, or the launch budget will understate both build time and the Year 1 cost base.

Card Production And Fulfillment Startup Expense

Card Build Cost

This cost covers physical card design, EMV chip or magstripe format, personalization files, packaging, shipping setup, inventory, and replacement cards. Price it from vendor quotes using unit count × unit cost, plus any artwork and setup fees. Keep it separate from transaction processing and ongoing support.

Volume Inputs

Start with buyer demand, not guesswork. Use $75 SMB orders, $250 mid-market orders, and $800 enterprise orders, then layer repeat demand of 35, 8, and 20 orders respectively. That tells you how many cards to prebuild, how much inventory to hold, and how much reissue stock to reserve.

Lower Waste

Keep the first run small, use standard packaging, and avoid custom card finishes unless demand is proven. The big mistake is overbuying inventory or building a heavy replacement policy too early. Ask for quotes by card type, branding level, shipping method, and personalization complexity, then compare per-card cost against expected repeat volume.

Set the Workflow

Budget the fulfillment workflow as a one-time launch task: file handling, card stock intake, quality checks, packaging rules, and shipping handoff. The estimate changes fast with branding, production volume, personalization depth, and replacement-card policy, so lock the process before launch and keep card inventory separate from processing fees.

Staffing Operations Risk And Support Startup Expense

Payroll Runway

Staffing for a stored value card launch is mostly working capital, not capex. Budget the $350k CEO salary and $280k CTO salary as a $630k annual anchor, then add compliance, ops, fraud, onboarding, and support before launch. Only capitalize work if it clearly meets accounting rules.

Runway Inputs

Here’s the quick math: take headcount salary, months of coverage, and the support burn rate. Use $630k a year for CEO and CTO pay, plus customer support at 15% of Year 1 revenue, easing to 8% by Year 5. Add $4k monthly insurance, or $48k a year, as fixed readiness cost.

Cost Control

Keep spend tight by staging hires, using clear support scripts, and training for disputes and escalation paths before go-live. That trims re work and avoids overtime. Don’t cut fraud monitoring or compliance leadership; those gaps get expensive fast. If onboarding and ticket handling stay structured, support can move toward the 8% Year 5 level instead of staying near Year 1.

Readiness Buffer

The real risk is underfunding the first 6–12 months. Insurance alone is $4k per month, and payroll starts before card volume pays back the team. Set aside launch documentation, client onboarding, and dispute handling time as pre-opening spend, then keep a clean escalation path so operations don’t stall when issues hit.

Compare 3 Startup Cost Scenarios

Startup cost scenarios

Launch cost jumps as you move from a pilot to commercial launch and then platform scale. More integrations, compliance work, staffing, and card volume drive the cash need far more than the first build.

| Scenario | Lean Launchpilot | Base Launchcommercial launch | Full Launchplatform scale |

|---|---|---|---|

| Launch model | Pilot launch with limited features, a controlled client count, fewer integrations, and lower physical card volume. | Commercial launch with a sponsor bank, processor, branded cards, compliance readiness, customer support, and a marketing plan. | Platform-scale launch with advanced integrations, higher volume, custom client tools, stronger fraud operations, and expanded staffing. |

| Typical setup | Keep the setup tight with core issuing, basic support, and a small marketing push. | Build the standard operating stack with card issuance, support, compliance, and acquisition spend. | Run a broader stack with deeper tech build, stronger controls, and more people on the floor. |

| Cost drivers |

|

|

|

| Planning rangeCAPEX only | $1.5M - $3MLow capex | $3M - $6MCore launch | $6M - $10MHigh capex |

| Best fit | Best for teams testing demand before a wider rollout. | Best for a funded launch that needs a workable operating model fast. | Best for companies aiming at multi-segment growth and heavier throughput. |

Planning note: Scenario ranges are researched planning assumptions from the model, not exact quotes.

Related Products

- Stored Value Card Program Porter's Five Forces Analysis

- Stored Value Card Program BCG Matrix

- Stored Value Card Program Business Model Canvas

- What Five KPIs Should Stored Value Card Program Track?

- Stored Value Card Business Plan Template in Pre-Written Word

- How Increase Profits Stored Value Card Program?

- What Are Operating Costs For Stored Value Card Program?

- Stored Value Card Program Financial Model Template in Excel

- How Much Stored Value Card Program Owners Make: Year 1 to Year 5

- How To Start A Stored Value Card Program In 4–9 Months

- How To Write A Business Plan For Stored Value Card Program?

- Stored Value Card Program Marketing Mix

- Stored Value Card Program Marketing Plan

- Stored Value Card Program Business Proposal

- Stored Value Card Program PESTEL Analysis

- Stored Value Card Program Pitch Deck Example Editable PPTX

- Stored Value Card Program Business SWOT Analysis

- Stored Value Card Program Value Proposition Canvas

Frequently Asked Questions

Budget at least $252M for the first operating year before CAPEX, reserves, cardholder funds, incomplete staffing, and variable fees That figure comes from $12M in Year 1 acquisition spend, $690k in annual fixed overhead, and $630k in named CEO and CTO payroll Treat it as a researched planning floor, not a quote