Owner incomeUp to $72k

Owner incomeUp to $72kHow Much Can a Surgical Technologist School Owner Make? $72k–$276k

Fully Editable

Instant Download

Professional Design

Pre-Built

No Expertise Is Needed

Description

Owner incomeUp to $72k  Net margin7%–41%

Net margin7%–41% Revenue for target pay$995k

Revenue for target pay$995k Business difficultyHard

Business difficultyHard

You’re not estimating an employee wage here you’re estimating owner income from a US tuition-based training school In this five-year model, revenue grows from $995k in Year 1 to $2186M in Year 5, with reported EBITDA of $72k in Year 1 and $276k in Year 2 Owner take-home depends on cohort fill, tuition collected, payroll, lab costs, clinical coordination, reserves, debt service, and whether the owner takes a salary

Owner incomeUp to $72kNet margin7%–41%Revenue for target pay$995kBusiness difficultyHardWant to test your owner pay?

Owner income calculator

Estimate owner take-home and the target-pay gap from revenue, margin, costs, reserves, and target pay.

Planning note: Research-based planning estimate only. It is not guaranteed salary, tax advice, or owner distribution advice, and it does not model accreditation approval, student loan eligibility, or guaranteed enrollment.

Want the full forecast view for a Surgical Technologist Training School?

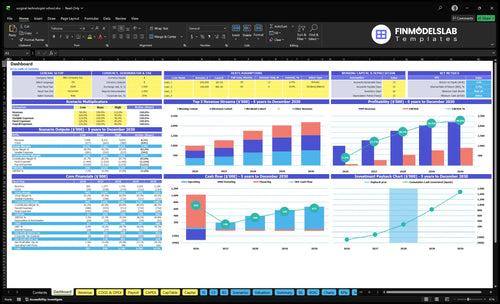

This screenshot shows revenue, margin, costs, reserves, and owner take-home assumptions in the Surgical Technologist Training School Financial Model Template. Open the model.

Owner-income model highlights

- Owner income is charted clearly

- Revenue spans $995k to $2.186M

- Scenarios test 65% to 92% occupancy

How much revenue does a surgical technologist school make?

A Surgical Technologist Training School makes about $995k in Year 1, growing to $2.186M by Year 5 in this model; for margin moves, see How Increase Surgical Technologist Training School Profits?. The catch: revenue is not owner income, since Year 1 EBITDA, or earnings before interest, taxes, depreciation, and amortization, is only $72k after payroll, supplies, marketing, clinical coordination, and overhead.

Revenue forecast

- Year 1: $995k revenue

- Year 2: $1.273M revenue

- Year 3: $1.754M revenue

- Year 5: $2.186M revenue

Main drivers

- Fill morning cohorts

- Fill afternoon cohorts

- Add weekend cohorts

- Protect tuition and fees

What affects surgical tech school profit margin?

Profit margin is tight in Year 1 because the school carries heavy program costs plus a big fixed payroll base. Here’s the quick math: direct program costs alone run 60% for medical consumables and lab supplies, 30% for student certification and insurance, and 20% for clinical site coordination, while marketing and recruitment add another 80%; if you want the KPI view, What Are The 5 KPIs For Surgical Technologist Training School Business? is the right place to track the pressure points.

Direct cost load

- Medical consumables and lab supplies: 60%

- Student certification and insurance: 30%

- Clinical site coordination: 20%

- Marketing and recruitment: 80%

Fixed overhead load

- Fixed overhead: $204k per month

- Program director: $115k

- Two lead clinical instructors: $85k each

- Admissions, career services, lab support

$322k of capex sits outside operating margin, so don’t mix it into the monthly profit view. That keeps the margin story clear: staffing is the biggest named cost, and the first-year model is driven more by seat fill and cost control than by one-time build-out spend.

Does a surgical tech school owner need to work in the business?

No, the financial model does not require the owner to work in the Surgical Technologist Training School. If the founder takes an operating role, cash burn can drop by covering some of the $115k program director, $170k two lead clinical instructors, $55k admissions coordinator, $65k career services manager, and $45k lab assistant costs. The tradeoff is real: workload rises, compliance risk rises, and growth still hinges on CAAHEP and ARC/STSA readiness, clinical placements, instructor supply, and student outcomes.

Owner works in the school

- Can lower payroll burn

- Covers key operating gaps

- Adds founder workload fast

- Raises compliance exposure

What limits growth

- CAAHEP readiness matters

- ARC/STSA expectations matter

- Clinical placements must hold

- Instructor supply and outcomes matter

What really drives owner income?

1

65%-92%Cohort Fill

More filled seats lift tuition revenue fast and spread the campus cost across more students.

2

$1.85K-$2.2KTuition Rate

Each small price move changes monthly cash because tuition repeats for every enrolled student.

3

$450KStaffing Mix

Instructor and program wages are the biggest controllable cost, so lean staffing protects operating profit.

4

$20.4K/moOverhead Load

Lease, utilities, insurance, software, and cleaning set the cash floor before the owner gets paid.

5

24-30Clinical Access

Accreditation and clinical placement control how big each cohort can get, so they cap revenue growth.

6

50%-80%Admissions Flow

Better lead-to-enrollment conversion cuts the cost to fill seats and keeps marketing from eating margin.

Surgical Technologist Training School Core Six Income Drivers

Cohort Enrollment And Seat Utilization

Seat Utilization

When more of the 63 seats are filled, tuition revenue rises and fixed costs get spread over more students. Year 1 capacity is split into 24 morning, 24 afternoon, and 15 weekend seats; at 65% fill, that is about 41 students, and the model supports about $995k in revenue. Empty seats still carry the lease, program director, insurance, and accreditation load.

By Year 5, occupancy is projected to reach 92%, or about 58 students. That lift matters because each filled seat adds monthly tuition while payroll and facility costs stay mostly fixed. If admissions quality slips, clinical slots tighten, or regulators cap intake, owner cash can stall even when demand looks strong.

Fill Seats Faster

Measure enrolled seats ÷ 63 each month, then break it out by morning, afternoon, and weekend starts. That shows where seats go empty and which cohort needs more leads, faster enrollment, or a better schedule mix. One empty seat is lost tuition; enough of them can wipe out the margin that pays the owner.

- Capacity: 63 seats total

- Mix: 24, 24, and 15 seats

- Fill: 65% to 92%

- Limits: clinical and compliance caps

Watch lead-to-enrollment rate, completion timing, and clinical capacity. If one cohort fills slower, rework start dates or class mix before adding spend. The goal is simple: keep seats filled enough to cover fixed costs, then turn the extra gross profit into payroll, reserves, and owner draw.

1

Tuition And Net Collected Revenue

Net Collected Tuition

This driver is the cash that actually lands, not just the tuition billed. Owner pay follows cash collected, so discounts, refunds, payment plans, bad debt, and slow collections can cut the money available for payroll, rent, and draws even when seats are full.

In Year 1, tuition is $1,850 a month for morning and afternoon cohorts and $1,950 for weekend; by Year 5 it rises to $2,100 and $2,200. Application fees add $150 to $200 per student, but late cash still presses EBITDA and reserve needs.

Track Collections, Not Just Enrollments

Measure cash collected ÷ tuition billed, refund rate, days to collect, and payment-plan default. Here’s the quick math: a full class only helps if students pay on time; otherwise the school can look busy and still run short on cash.

Set clear billing terms, get deposits before start dates, and review aging weekly. Keep a simple list of inputs:

- Monthly tuition by cohort

- Application fee cash

- Discounts and refunds

- Payment plan collections

- Bad debt write-offs

2

Instructor And Program Staffing Model

Staffing Cost Load

Payroll is the biggest named operating cost, so it hits owner pay fast. The listed Year 1 team totals $450k a year: $115k program director, two $85k lead instructors, $55k admissions, $65k career services, and $45k lab support. That cost only works if it protects enrollment, completion, clinical coordination, and job placement.

By Year 3, adding a third lead instructor and a second lab assistant lifts staffing to $580k. If the owner teaches or handles admissions, margin can improve, but that only lasts if quality and compliance stay strong. One bad cut in instruction or placement support can lower outcomes, hurt fill, and shrink cash available for owner draw.

Keep Payroll Aligned to Scale

Track staffing against seats, not hope. The key inputs are filled seats, instructor load, admissions volume, clinical handoffs, and placement results. If payroll rises faster than tuition collected, owner income falls even when the school looks busy.

- Measure seats per instructor.

- Watch cash collected monthly.

- Protect compliance and clinical roles.

- Test owner-led admin only short term.

Use role cuts only in non-core work. Do not trim instruction, clinical coordination, or outcomes support just to raise short-term take-home pay.

3

Lab, Equipment, Supplies, And Facility Costs

Lab Burn and Facility Cost

Hands-on training makes the lab a cost center, meaning it consumes cash before it creates revenue. Startup capex is $322k: $150k simulation equipment, $60k instrument sets, $45k furniture and AV, $35k workstations, $20k office setup, and $12k security. Ongoing lab supplies run at 60% of Year 1 revenue and 50% by Year 3, before the $125k monthly lease.

Here’s the quick math: if supplies take 60% of revenue, only 40 cents per tuition dollar is left for rent, payroll, and owner pay. The key inputs are seats filled, tuition collected, supply usage, and equipment replacement timing. Mixing startup equipment with consumables makes cash look stronger than it is.

Split Capex From Monthly Cash Burn

Track equipment, supplies, and lease in separate buckets. Keep the $322k startup capex out of monthly operating cash, then compare collected tuition against the $125k lease and supply burn. That shows the real cash left for owner draws and stops profit from being overstated by one-time purchases.

Watch supplies as a share of collected revenue. If that ratio stays near 60% in Year 1, there is little room for owner pay until fill rates improve and waste drops. Tight ordering, inventory counts, and schedule planning protect cash without cutting the hands-on model.

4

Accreditation And Clinical Placement Capacity

Accreditation and Clinical Seat Capacity

Accreditation readiness and clinical seat access can cap enrollment even when student demand is strong. In this model, fixed accreditation maintenance fees run $12,000 per month, and clinical site coordination costs start at 20% of Year 1 revenue before easing to 10% by Year 4. If reporting slips, partners are thin, or outcomes weaken, cohort growth slows and tuition upside gets delayed.

This driver is really about how many seats you can safely fill under the rules of the Commission on Accreditation of Allied Health Education Programs and the Accreditation Review Council on Education in Surgical Technology and Surgical Assisting. The key inputs are filled clinical seats, partner count, report quality, and graduate outcomes. Fewer seats means less revenue, but the same fixed fee still hits cash flow, so owner pay tightens fast.

Track Seats Before You Scale

Measure clinical seat fill rate, partner coverage, and on-time reporting each month. If site coordination stays near 20% of revenue in Year 1, treat it as a margin drag and forecast cash tightly. The goal is simple: keep clinical slots open enough to support cohort growth, but not so strained that delays, compliance gaps, or poor outcomes block new enrollment.

Use a seat-by-seat forecast. List these inputs:

- Filled seats by cohort

- Active clinical partners

- Monthly maintenance fees of $12,000

- Coordination cost rate at 20%, then 10%

- Outcome and reporting timeliness

5

Marketing, Admissions, And Placement Efficiency

Marketing, Admissions, And Placement Efficiency

Marketing only helps owner income when it turns into qualified enrolled students who stay. In this school model, digital marketing and recruitment cost runs at 80% of Year 1 revenue, then 70% in Year 2, 60% in Year 3, and 50% in Years 4 and 5, so weak conversion can wipe out margin fast.

The key inputs are lead volume, lead-to-enrollment rate, retention, and placement results. Add the $55k admissions coordinator and $65k career services manager, and owner pay depends on turning spend into filled seats, completed training, and job outcomes that keep referrals coming.

Track conversion, not traffic

Measure the path from inquiry to enrollment to placement. Here’s the quick math: if spend rises but seat fill and retention do not, cash gets tight; if spend is too low, seats stay empty and fixed costs still hit. Strong placement reputation supports referrals and steadier cohort fill.

- Track cost per qualified enrollment.

- Track retention by cohort.

- Track placement rate after graduation.

- Compare spend to seat fill.

6

Compare launch, base, and growth owner-income scenarios

Owner income scenarios

Owner income shifts with seat fill, tuition, and staffing. Early months are cash-tight, then draws improve as occupancy rises and marketing eases.

| Scenario | Low CaseCash-tight | Base CaseStabilizing | High CaseScale-constrained |

|---|---|---|---|

| Launch model | Owner draw stays tight in the launch year while cash is preserved for operations. | Owner draw improves as the school moves into steadier second-year operations. | Owner draw can rise in the mature year, but only after the model proves capacity and margin. |

| Typical setup | Year 1 runs at 63 seats, 65% occupancy, $995k revenue, and $72k EBITDA, with owner pay limited by reserves. | Year 2 reaches 68 seats, 75% occupancy, $1.273M revenue, and $276k EBITDA, with lower marketing at 70% and lab supplies at 55%. | Year 5 reaches 85 seats, 92% occupancy, $2.186M revenue, and weekend tuition up to $2,200, with EBITDA modeled before any owner distribution. |

| Cost drivers |

|

|

|

| Owner income rangeBefore owner reserves | $0 - $25kLaunch draw | $50k - $125kBase draw | $175k - $350kGrowth draw |

| Best fit | Use this to test the launch year when cash is tight and growth needs to stay funded. | Use this for a normal operating year with better cash flow but still real reinvestment needs. | Use this to test upside once the program is full and scale starts to strain staffing and clinical support. |

Planning note: Scenario ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions.

Related Products

- Surgical Technologist Training School Porter's Five Forces Analysis

- Surgical Technologist Training School BCG Matrix

- Surgical Technologist Training School Business Model Canvas

- What Are The 5 KPIs For Surgical Technologist Training School Business?

- Surgical Technologist Training School Business Plan Template in Pre-Written Word

- How Increase Surgical Technologist Training School Profits?

- What Are Operating Costs For Surgical Technologist Training School?

- Surgical Technologist Training School Startup Costs: $699K Cash Need

- Surgical Technologist Training School Financial Model Template in Excel

- How To Open A Surgical Technologist School In 9–18 Months

- How Do I Write A Business Plan For Surgical Technologist Training School?

- Surgical Technologist Training School Marketing Mix

- Surgical Technologist Training School Marketing Plan

- Surgical Technologist Training School Business Proposal

- Surgical Technologist Training School PESTEL Analysis

- Surgical Technologist Training School Pitch Deck Example Editable PPTX

- Surgical Technologist Training School Business SWOT Analysis

- Surgical Technologist Training School Value Proposition Canvas

Frequently Asked Questions

The researched model shows $72k of Year 1 EBITDA and $276k of Year 2 EBITDA before taxes, debt service, reserves, and distributions Revenue is much higher at $995k and $1273M, but payroll, supplies, clinical coordination, marketing, rent, and cash reserves absorb a large share