Owner income$406k

Owner income$406kHow Much Sustainable Paper Owners Can Make: $562M Before Pay

Fully Editable

Instant Download

Professional Design

Pre-Built

No Expertise Is Needed

Description

Owner income$406k  Net margin69%

Net margin69% Revenue for target pay$588k

Revenue for target pay$588k Business difficultyHard

Business difficultyHard

Key Takeaways

- Volume drives revenue, but capacity must keep pace.

- Product mix sets pricing power and margin dollars.

- Break-even sits near $46,800 monthly revenue before owner pay.

- Cash needs come before owner distributions.

Owner income$406kNet margin69%Revenue for target pay$588kBusiness difficultyHardWant to test your owner pay?

Owner income calculator

Estimate owner take-home and target-pay gap from revenue, margin, costs, reserves, and target pay.

Planning note: Research-based planning estimate only. It is not guaranteed salary, tax advice, or owner distribution advice.

How do you check owner income in the Sustainable Paper model?

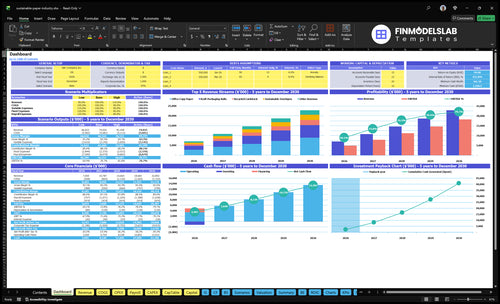

The dashboard shows revenue build, COGS, gross margin, variable expenses, fixed overhead, cash flow, scenarios, and owner income; charts run from $705M to $2,284M revenue and $562M to $1,983M operating profit. Open the Sustainable Paper Financial Model Template next.

Owner-income model highlights

- Owner pay output

- Revenue and margin charts

- Assumptions drive scenarios

What affects sustainable paper profit margins most?

Freight, commissions, and product mix hit Sustainable Paper margins the hardest. For the cost build, see What Is The Estimated Cost To Open And Launch Sustainable Paper Business?; first-year COGS is $557,500 on $705M revenue, so the real squeeze comes from the selling and delivery side.

Main cost drivers

- Recycled fiber sets the base cost.

- Pulp additives lift unit cost.

- Direct labor trims gross margin.

- Packaging and internal logistics add more cost.

Big margin swing points

- Logistics and distribution add 30% of revenue.

- Sales commissions add 25%.

- Notebooks sell at $700.

- Kraft packaging rolls sell at $20,000.

Can a sustainable paper business scale owner income?

Yes—Sustainable Paper can scale owner income if demand, production, fulfillment, and cash all keep up with volume. In the model, units rise from 220,000 in year one to 660,000 in year five, revenue grows from $705M to $2,284M, and operating profit before owner pay climbs from $562M to $1,983M, while fixed overhead stays flat at $486,000 a year.

What scales income

- 220,000 to 660,000 units

- $705M to $2,284M revenue

- $562M to $1,983M profit

- $486,000 fixed overhead stays flat

What can slow it

- More staff may be needed

- Equipment and storage costs rise

- Large accounts can stretch payment terms

- Inventory needs more working cash

Do sustainable paper manufacturers make more than resellers?

Yes, Sustainable Paper manufacturers can make more than resellers in this model, but only if production volume covers $40,500/month in fixed overhead; for demand context, see How Is Sustainable Paper Performing In Terms Of Customer Satisfaction And Market Reach?. The data supports a producer or converter model with 921% modeled year-one gross margin, while reseller profit cannot be calculated without purchase costs and channel margins.

Manufacturer case

- 921% modeled year-one gross margin

- $40,500/month fixed overhead burden

- Costs include labor, fiber, utilities

- Production risk stays in-house

Reseller case

- Profit cannot be calculated here

- Purchase costs are not provided

- Channel margins are not provided

- Distributors add volume, pressure price

Want the six drivers that matter most?

1

220KSales Volume

Year 1 output is 220,000 units, and that scale drives about $7.05M in sales before costs.

2

29xCustomer Mix

A bigger share of higher-price paper rolls lifts revenue per unit, because prices run from $7 to $200.

3

95%Gross Margin

Direct product cost is about 5% of sales, so gross margin sits near 95% before overhead and commissions.

4

3.0%Production Efficiency

Energy, water, maintenance, QA, and compliance total 3.0% of revenue, so tighter output protects take-home.

5

39.5K/moOverhead Control

Fixed overhead is $39.5K a month, and cuts there flow straight to profit.

6

N/AWorking Capital

Reserve policy is not modeled, so cash tied up in stock and receivables can trim owner take-home.

Sustainable Paper Core Six Income Drivers

Sales Volume

Sales Volume

Sales volume sets the income ceiling. This model grows from 220,000 units in year one to 660,000 units in year five, across office copy paper, kraft packaging rolls, recycled cardstock, notebooks, and envelopes. More cases, rolls, reams, and custom orders raise revenue only if production, warehouse handling, and fulfillment can keep up. If volume outruns capacity, the business can’t turn demand into profit fast enough.

Here’s the quick math: volume helps only when each order clears minimum order rules and ships on time. Order mix matters too, because small orders can add handling work without enough revenue. The main risk is chasing units faster than the plant and warehouse can process them.

Track Capacity First

Track booked units, shipped units, and open capacity by product line each week. Compare actual volume to the 220,000 to 660,000 unit path, and stop accepting orders that break minimum order rules or overload fulfillment. That protects margin and keeps cash moving instead of tying it up in backlogs.

Test the break point between standard orders and custom orders. If custom work slows production or warehouse flow, it can lift revenue but lower owner take-home. Keep one rule: sell only what you can make, store, and ship on time.

1

Customer Mix And Pricing

Customer Mix and Pricing

When the mix shifts toward kraft packaging rolls at $20,000 instead of notebooks at $700, average selling price and margin dollars move fast. Since the model does not show channel mix, use product mix as the pricing proxy. Higher-ticket B2B orders can lift gross profit per order, but low-price items need much higher unit volume to fund overhead and owner pay.

The key inputs are product mix, unit price, order count, and realized discount rate. Channel discounts and procurement pressure should be tracked separately, because they can cut cash price even when list prices look strong. One bad mix change can leave revenue flat while take-home income falls.

Track Mix by SKU, Not Just Total Sales

Measure revenue, units, and gross profit by line: $20,000 rolls, $5,500 copy paper, and $700 notebooks. Then watch which mix gives the most margin dollars per order. If a low-price line needs too much volume, it can crowd out capacity and squeeze cash flow.

Use a simple check: realized price after discounts, gross margin per order, and share of revenue from B2B items. If procurement pushes discounts down, reprice, tighten terms, or shift sales effort toward the higher-ticket mix that funds fixed costs and owner draw.

2

Gross Margin And COGS

COGS Squeezes Owner Pay

COGS (cost of goods sold) is the direct cost to make each paper order. In year one, the model shows $557,500 of COGS, made up of $346,000 in unit costs plus 30% of revenue-based production costs. Recycled fiber, pulp additives, direct labor, packaging, and internal logistics sit inside that line, so supplier price changes hit gross margin fast.

The owner’s take-home depends on what is left after COGS and then fixed overhead. If input prices rise and selling prices do not, gross profit shrinks and the business needs more sales just to keep the same draw. One clean rule: protect unit cost first.

Track the Cost Stack

Measure COGS by product line, not just in total. Split it into recycled fiber, pulp additives, direct labor, packaging, and internal logistics, then compare actuals with supplier quotes every month. If one input moves, test price changes on the highest-volume items first, because that usually protects owner income fastest.

- Track COGS per unit.

- Review supplier quotes monthly.

- Test price on big sellers.

- Watch margin by product line.

Build a quick gross-margin forecast before you approve discounts or new contracts. Use revenue, units sold, and production cost as % of revenue, then check whether gross profit still covers rent, software, marketing, and payroll. If the margin gap is tight, pause discounts, renegotiate inputs, or shift mix toward higher-margin paper.

3

Production Efficiency And Fulfillment

Production Efficiency And Fulfillment

Production efficiency is the margin guardrail. It covers direct mill labor, direct assembly labor, packaging, internal logistics, energy, water treatment, mill maintenance, quality assurance, and environmental compliance. In this model, logistics and distribution fall from 30% of revenue in year one to 20% in year five, so every $100 sold can keep $10 more in gross profit.

Here’s the quick math: if waste, handling, or rework stay high, that 10-point cost gap gets eaten up fast and leaves less cash for fixed overhead and owner pay. For in-house production, use the current cost lines; for outsourced converting, replace them with unit cost and fulfillment fields so margin reflects the real cost per order, not a blended estimate.

Cut Cost Per Order

Track labor hours per run, scrap rate, and cost per order before you push for more volume. That tells you whether higher sales are adding profit or just adding overtime, freight, and rework. Keep the cost stack visible so you can spot which step is hurting margin.

- Measure output per labor hour.

- Compare in-house and outsourced costs.

- Review low-margin orders weekly.

- Forecast fulfillment cost by volume.

If shipments miss spec or go out late, the business loses twice: wasted materials and weaker repeat sales. That shows up fast when fixed overhead is $40,500 per month, because every avoidable handling cost takes money away from owner draw.

4

Operating Costs And Labor

Fixed Overhead and Labor

Fixed overhead is the monthly cost that has to be paid before the owner sees cash. Here it is modeled at $40,500 per month, with $25,000 for factory rent and utilities, $5,000 office rent, $2,500 insurance, $1,200 software, $1,800 legal and accounting, $3,000 marketing, and $1,000 security. These costs sit outside COGS, so they directly cut into gross profit available for owner pay.

Here’s the quick math: at the year-one contribution margin, break-even before owner pay is about $46,800 in monthly revenue. If revenue lands below that line, the business is funding overhead out of gross profit and the owner draw gets squeezed fast. If revenue stays above it, the extra margin is what can fund distributions, reserves, and growth.

Track Overhead Against Break-Even

Watch monthly overhead as a share of revenue, not just the dollar total. Compare actual spend to the $40,500 base and reforecast every month against the $46,800 break-even mark. If factory rent, office rent, or marketing creep up, owner pay drops unless sales grow at the same pace. One clean rule: protect fixed cost discipline before adding discretionary spend.

Use a simple control sheet with three lines: overhead paid, contribution mar gin earned, and cash left for owner draw. If the business adds headcount, extra shifts, or more admin support, test the payback in revenue before committing. The goal is not just lower costs; it is making sure each extra dollar of overhead is covered by enough gross profit to keep cash available for the owner.

5

Working Capital And Reserves

Working Capital And Reserves

Cash for the owner is not the same as accounting profit. In this model, inventory, supplier deposits, receivables, equipment upgrades, and growth reserves can absorb cash, so owner distributions should wait until those needs are funded.

The cash squeeze gets larger as scale rises: modeled COGS moves from $346,000 in year one to $104M in year five. The model does not give a reserve percentage, tax rate, debt schedule, or customer payment terms, so you cannot set owner pay from profit alone.

Track Cash Before Owner Pay

Build a monthly cash forecast that separates profit from cash timing. Track inventory weeks, receivables days, prepaid supplier deposits, and planned equipment spending, then set a reserve before any owner draw. If terms stretch or stock builds, cash available to the owner drops fast.

Use a simple rule: fund operating cash, taxes, and replacement capex first, then pay the owner from leftover cash. One clean rule: no reserve, no draw. That keeps one late payment or machine upgrade from turning paper profit into a cash problem.

6

Scenario objective: compare low, base, and high owner-income planning cases

Owner income scenarios

Owner income changes with product mix, throughput, and logistics costs. Year 1, Year 3, and Year 5 show how the plant scales from the start-up mix to a steadier operating base.

| Scenario | Low CaseDownside | Base CaseModeled | High CaseUpside |

|---|---|---|---|

| Launch model | Year 1 is the lower earnings path, with the first operating mix and full overhead still in place. | Year 3 is the modeled case, with a fuller mix and steadier throughput. | Year 5 is the stronger earnings path, with higher throughput and better cost spread across the plant. |

| Typical setup | Revenue is about $7.05M from 220,000 units, with 92.1% gross margin, about $39.5k in monthly fixed overhead, and a leaner staff base than later years. | Revenue is about $14.66M from 440,000 units, pricing is slightly higher, gross margin is 92.3%, and the model carries the added marketing and logistics roles by Year 3. | Revenue is about $22.84M from 660,000 units, gross margin reaches 92.5%, and logistics plus commissions fall to 3.5% of revenue. |

| Cost drivers |

|

|

|

| Owner income rangeBefore owner reserves | $4.9M/yrYear 1 case | $11.2M/yrYear 3 case | $18.2M/yrYear 5 case |

| Best fit | Use this to stress-test the start year if sales ramp slower or operating costs run hot. | Use this as the main planning case for budgets, hiring, and lender talks. | Use this to test upside if demand stays strong and the factory runs closer to capacity. |

Planning note: These ranges are researched planning assumptions only, not guaranteed earnings, salary promises, tax advice, or distribution guidance.

Related Products

- Sustainable Paper Porter's Five Forces Analysis

- Sustainable Paper BCG Matrix

- Sustainable Paper Business Model Canvas

- 7 Essential Financial KPIs for Sustainable Paper

- Sustainable Paper Business Plan Template in Pre-Written Word

- Increase Sustainable Paper Profitability: 7 Actionable Strategies

- How to Manage Running Costs for Sustainable Paper Production

- How Much To Start A Sustainable Paper Business: $500K+ CAPEX

- Sustainable Paper Financial Model Template in Excel

- How To Start A Sustainable Paper Business In 3 To 9 Months

- How to Write a Business Plan for Sustainable Paper

- Sustainable Paper Marketing Mix

- Sustainable Paper Marketing Plan

- Sustainable Paper Business Proposal

- Sustainable Paper PESTEL Analysis

- Sustainable Paper Pitch Deck Example Editable PPTX

- Sustainable Paper Business SWOT Analysis

- Sustainable Paper Value Proposition Canvas

Frequently Asked Questions

The model shows $562M in first-year operating profit before owner pay, taxes, debt, reserves, and reinvestment That is the ceiling for planning, not take-home income With $705M revenue and 921% gross margin, distributions depend on how much cash must stay in inventory, equipment, receivables, and growth reserves