Owner income$160k/yr

Owner income$160k/yrHow Much Can A Talent Acquisition Owner Make With $160K Base Pay

Fully Editable

Instant Download

Professional Design

Pre-Built

No Expertise Is Needed

Description

Owner income$160k/yr  Net margin-10% to 64%

Net margin-10% to 64% Revenue for target pay$250k/yr

Revenue for target pay$250k/yr Business difficultyHard

Business difficultyHard

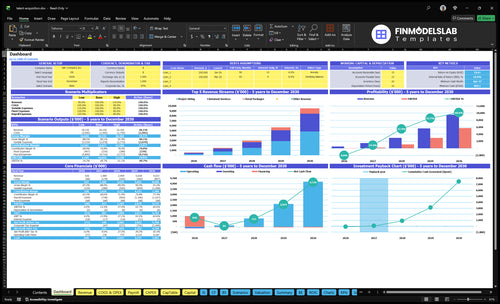

You’re not comparing this to a recruiter employee salary you’re planning owner income from a US talent acquisition company In this model, the owner role carries $160,000 in annual pay, while EBITDA moves from -$48,000 in the first year to $5773 million by Year 5 The scope covers revenue, margins, payroll, tools, reserves, breakeven, and pre-tax distribution logic

Owner income$160k/yrNet margin-10% to 64%Revenue for target pay$250k/yrBusiness difficultyHardWant to test your owner pay scenario?

Owner income calculator

Estimate owner take-home and target-pay gap from revenue, margin, costs, reserves, and target pay.

Planning note: Research-based planning estimate only, not guaranteed salary, tax advice, or owner distribution advice. Actual owner income depends on revenue, margin, payroll, taxes, reserves, and reinvestment.

Need the deeper owner income view for Talent Acquisition?

Yes—this Talent Acquisition Financial Model Template shows revenue, margin, costs, reserves, and owner take-home assumptions; open the model for the full forecast.

Owner-income model highlights

- Owner pay outputs

- Revenue and margin

- Scenarios and assumptions

What costs reduce talent acquisition business owner income?

Talent Acquisition owner income gets squeezed by direct software, candidate assessment/background fees, sales commissions, contractor fees, fixed overhead, payroll, marketing, and setup capex. In Year 1, gross margin is 87% after 8% direct software and 5% candidate fees, but contribution margin drops to 72% after 10% sales commissions and 5% contractor fees. Fixed overhead is $5,650/month, payroll grows from $285,000 in Year 1 to $1.175 million in Year 5, and setup capex totals $60,000 across launch items; How Much Does It Cost To Open, Start, Launch Your Talent Acquisition Business? helps frame those early cash needs.

Variable cost drag

- 8% direct software cost

- 5% candidate fees

- 10% sales commissions

- 5% contractor fees

Fixed cost pressure

- $5,650 monthly overhead

- Payroll: $285,000 to $1.175 million

- Marketing: $50,000 to $250,000

- Capex totals $60,000

Can a talent acquisition agency owner make more by hiring recruiters?

Yes—hiring recruiters can raise owner income, but only when each recruiter’s gross profit beats salary, commissions, tools, and your management time. In Talent Acquisition, staffing grows from 1 senior consultant and 5 recruitment consultants in Year 1 to 5 senior consultants and 4 recruitment consultants in Year 5, and EBITDA rises from -$48,000 to $5773 million. The catch is cash: it peaks at $809,000 in Month 16, so payroll and collection timing can still strain the business.

When hiring pays

- Gross profit must beat total recruiter cost.

- Year 1 starts lean: 1 senior consultant.

- Year 5 scales to 5 senior consultants.

- More hires can add operating leverage.

What can hurt cash

- Cash need peaks at $809,000.

- The peak hits in Month 16.

- More staff means more payroll pressure.

- Collections can lag billings and EBITDA.

How many placements does a talent acquisition agency need to make money?

Talent Acquisition can’t use one fixed placement count because the average fee per hire isn’t provided; use this formula: required placements = fixed costs + payroll + marketing + target owner pay divided by average fee × 72% contribution margin. Year 1 margin is 72% after 13% COGS and 15% variable costs, fixed overhead is $5,650/month, and breakeven lands in Month 8; track the hiring drivers with What Is The Most Critical Metric To Measure The Success Of Talent Acquisition For Your Business?.

Placement math

- Start with total monthly costs

- Add payroll, marketing, owner pay

- Use average fee per hire

- Divide by fee × 72%

Risk levers

- Fixed overhead: $5,650/month

- Breakeven timing: Month 8

- COGS: 13% of revenue

- Raise volume if fill rate drops

Want the six owner income drivers?

1

$50K-$250KPlacement Volume

A bigger marketing budget feeds the pipeline and gets the business to Month 8 break-even faster.

2

$140-$200Average Fee

Higher hourly fees lift revenue per search, and most of that extra revenue flows through to take-home.

3

40%-60%Client Quality

A shift toward retained work from 40% to 60% steadies cash flow and cuts churn risk.

4

15-40hRecruiter Output

More billable hours per engagement spread recruiter pay across more revenue and improve margin.

5

72%Delivery Cost

Year 1 contribution margin is about 72%, so small fee or delivery-cost changes move owner income fast.

6

$809KReserve Policy

A $160K CEO salary plus about $809K of minimum cash means early owner draws have to stay tight.

Talent Acquisition Core Six Income Drivers

Placement Volume

Placement Volume

Placement volume is the count of completed hires or billable engagements. It raises net fee revenue only when fill rate and delivery capacity hold. In this model, the mix shifts from 40% retained work to 60%, while project hiring falls from 60% to 40%, so more of each recruiter’s time turns into steadier revenue and higher revenue density per recruiter.

The owner’s take-home income improves when more searches close without adding unpaid work. The risk is chasing weak job orders that never fill, which lifts activity but not profit. More volume helps only if close rates, staffing, and cash timing stay tight.

- Track open orders and closed hires.

- Watch fill rate by service type.

- Limit weak, low-close job orders.

- Match recruiter load to capacity.

Measure Close Rate, Not Just Pipeline

Measure the funnel from job order to close: submitted candidates, interviews, offers, and fills. A higher count of open searches means little if the close rate falls or recruiters get overloaded. Better volume is the kind that turns into billed work, not extra screening time.

Set minimum rules for new orders, then forecast recruiter capacity before you accept more. Prioritize retained and tiered work, because the mix shift to 60% retained supports steadier revenue and less waste. What matters is revenue per recruiter, not activity for its own sake.

1

Average Fee Size

Average Fee Size

Average fee size is the hourly rate or package price you actually collect across retained services, project hiring, and tiered packages. Here’s the quick math: pricing moving from $150 to $170 per hour lifts retained revenue by 13.3%; $180 to $200 lifts project hiring by 11.1%; $140 to $160 lifts packages by 14.3%. That’s direct upside to gross profit if delivery cost per hour stays flat.

This driver depends on role mix, specialization, and client willingness to pay. Not every search supports premium pricing, so low-skill or commodity roles can cap fee size and squeeze owner pay if senior recruiter time rises faster than the rate increase. One clean rule: rate growth only helps when margin per engagement grows too.

Measure Fee Quality

Track realized fee by service line, not just quoted price. Split revenue into retained, project, and package work, then compare fee per billable hour against direct labor cost, contractor spend, and nonbillable time. If price rises but recruiter hours rise faster, the owner keeps less cash even when top-line revenue looks better.

- Watch realized rate by engagement type.

- Test price by role difficulty.

- Review margin after each closed search.

- Limit discounting on scarce roles.

For forecasting, use actual billable hours, mix, and delivery cost, then stress test a 10% fee increase versus unchanged delivery time. If the higher price does not improve contribution margin, the extra revenue may not reach owner distributions or salary.

2

Client Quality

Client Quality

Client quality is the mix of clients that close jobs fast, pay on time, and hire again. Here, retained services rise from 40% of allocation in Year 1 to 60% in Year 5, so revenue gets steadier than one-off project work. Weak clients slow feedback, waste search hours, and raise replacement risk, which cuts owner take-home by turning paid time into unpaid rework.

Track the accounts that pay off

Measure fill rate, repeat hiring, days to feedback, and replacement rate by client. The best accounts shorten search time and reduce unpaid work, while weak ones drag margin through stalled approvals and do-overs. If a client keeps forcing resets, the real cost is lower owner distributions, even when headline revenue looks fine.

3

Recruiter Productivity

Recruiter Productivity

When each recruiter does not cover their own cost, owner pay gets squeezed fast. Here, senior consultant headcount rises from 1 FTE to 5 FTE, and recruitment consultant headcount rises from 0.5 FTE to 4 FTE. Payroll grows from $285,000 to $1,175,000, a jump of $890,000 or about 4.1x.

The key input is gross profit, meaning fee revenue left after salary, commissions, tools, and oversight. If headcount grows faster than billable output, margin drops and cash gets tight before the owner can pay themselves. One clean rule: every recruiter has to fund their own seat before the team grows again.

Track Gross Profit per Recruiter

Measure billable hours, fill rate, and gross profit per recruiter every month. Tie each hire to the revenue they bring in, not just the searches they touch. If a recruiter is below target, fix job mix, pricing, or process before adding more staff.

What this estimate hides is timing. Payroll hits now, but placements and client cash can lag. Use a simple test: if a new recruiter does not cover their share of the $1.175 million payroll load, pause hiring and push more work to the highest-fee roles.

4

Delivery Cost Structure

Delivery Cost Structure

Delivery cost structure is what turns booked revenue into owner take-home. In Year 1, direct software is 8%, assessments are 5%, commissions are 10%, and contractors are 5%, or 28% before fixed overhead. Add $5,650 per month in overhead, and annual fixed cost is $67,800.

The key inputs are billable hours, placement volume, recruiter mix, and marketing spend. Marketing rises from $50,000 to $250,000, so revenue can grow fast while cash still stays tight. High revenue does not equal high owner income if commissions, contractors, and admin scale faster than gross profit.

Watch the full cost stack

Track gross margin by client and by recruiter. Here’s the quick math: every $100,000 of revenue leaves about $72,000 before fixed overhead, marketing, and admin, based on the stated 28% delivery cost rate. If that margin drops, owner pay gets squeezed fast.

Use a simple monthly dashboard: billable hours, commission %, contractor %, software %, assessment spend, marketing, and overhead. If marketing jumps but placements do not, trim spend or tighten client quality. Cash flow, not revenue, funds owner draws.

- Split costs by client and recruiter.

- Cap contractor use on low-margin work.

- Review commissions against gross profit.

5

Reserve And Reinvestment Policy

Reserve And Reinvestment Policy

Owner pay here comes from cash left after payroll, slow collections, guarantees, marketing, growth hiring, and setup costs. The key test is cash, not EBITDA: this model needs a $809,000 minimum cash balance by Month 16, with a 24-month payback and $60,000 of capex. That means early distributions stay low so the business can absorb payroll and guarantee shocks.

What this hides is timing risk. Even if EBITDA turns positive, delayed client payments can still squeeze cash, so the owner may not be safe to draw until reserves are built. One clean rule: if the cash reserve is below plan, distributions should wait.

Build the reserve before raising draws

Track monthly collections, payroll, guarantee payouts, marketing, hiring, and capex together. Use a simple cash forecast that starts with EBITDA, then subtracts working-capital drag and planned reinvestment, so you can see when cash, not profit, can fund owner pay.

- Watch cash balance every week.

- Cap distributions until reserve target hits.

- Stress test slow collections and delays.

- Hold back cash for hiring and guarantees.

If early revenue looks strong but collections lag, reinvest the excess instead of paying it out. That lowers short-term income, but it reduces the risk of a payroll miss, a guarantee call, or a forced equity injection later.

6

Compare low, base, and high owner income scenarios

Owner income scenarios

Owner income here changes with billable hours, pricing, and the mix of retained work versus project hiring. The same $160,000 salary can sit inside very different profit paths as staffing and overhead scale.

| Scenario | Low CaseCash risk | Base CaseScaling difficulty | High CaseReserve discipline |

|---|---|---|---|

| Launch model | This is the lower-earning path, anchored to Year 1 and a $160,000 owner salary. | This is the modeled path, anchored to Year 3 and a $160,000 owner salary. | This is the stronger-earnings path, anchored to Year 5 and a $160,000 owner salary. |

| Typical setup | Year 1 setup with $160,000 owner salary, about $493,000 revenue, -$48,000 EBITDA, and roughly -10% margin. | Year 3 setup with $160,000 owner salary, about $2.7 million revenue, $1.105 million EBITDA, and about 41% margin. | Year 5 setup with $160,000 owner salary, about $9.0 million revenue, $5.773 million EBITDA, and about 64% margin. |

| Cost drivers |

|

|

|

| Owner income rangeBefore owner reserves | $160,000 salaryIncome floor | $160,000 salaryPlan case | $160,000 salaryUpside case |

| Best fit | Use this to stress-test early cash needs and a slower client ramp. | Use this as the planning case for budget, hiring, and reserve targets. | Use this to test what stronger demand can support without starving cash. |

Planning note: These scenario ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions.

Related Products

- Talent Acquisition Porter's Five Forces Analysis

- Talent Acquisition BCG Matrix

- Talent Acquisition Business Model Canvas

- 7 Essential Financial KPIs for Talent Acquisition Services

- Talent Acquisition Business Plan Template in Pre-Written Word

- 7 Proven Strategies to Boost Talent Acquisition Profit Margins

- Running Costs for Talent Acquisition: How to Budget and Scale Operations

- Talent Acquisition Startup Costs: Plan $60k Setup And $809k Runway

- Talent Acquisition Financial Model Template in Excel

- How To Open A Talent Acquisition Business In 4 To 8 Weeks

- How to Write a Talent Acquisition Business Plan in 7 Steps

- Talent Acquisition Marketing Mix

- Talent Acquisition Marketing Plan

- Talent Acquisition Business Proposal

- Talent Acquisition PESTEL Analysis

- Talent Acquisition Pitch Deck Example Editable PPTX

- Talent Acquisition Business SWOT Analysis

- Talent Acquisition Value Proposition Canvas

Frequently Asked Questions

The model includes $160,000 in annual owner salary That is not the same as total take-home, because distributions depend on EBITDA, cash reserves, and reinvestment EBITDA is -$48,000 in Year 1, $213,000 in Year 2, and $1105 million in Year 3 under the researched assumptions