Ticket growth drives revenue more than seat count.

Weekend covers carry the model's highest volume.

Reservations and events smooth slow weekday demand.

Rent and payroll demand strong sales discipline.

HTML error: JSON must include a cards array.

Want to test your own tea room owner income?

Owner income calculator

Estimate owner take-home and target-pay gap from revenue, margin, costs, reserves, and target pay.

!

Planning note: Research-based planning estimate only. Actual owner income depends on revenue, margins, payroll, taxes, debt, and reinvestment. It is not guaranteed salary, tax advice, or owner distribution advice.

How does the Tea Room model show owner income?

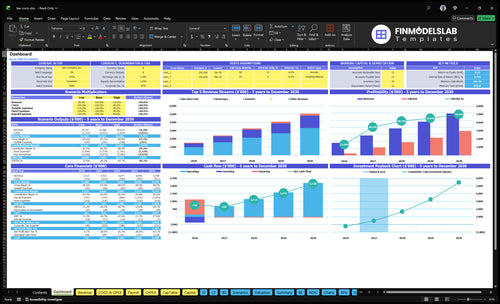

The dashboard in the Tea Room Financial Model Template shows revenue, profit, cash need, breakeven, payback, and owner pay assumptions. Charts and tables support scenario planning, not earnings promises. Assumptions cover menu pricing, traffic, labor, rent, events, retail tea sales, COGS, marketing, reserves, and target owner pay.

Owner income model highlights

Year 1 revenue: $163M

Breakeven: Month 4

Cash minimum: $626K

Payback: 17 months

EBITDA: $233K to $2,969M

How much revenue does a tea room need to pay the owner?

For the Tea Room, owner pay should be tied to sales, not salary averages: Year 1 needs about $93K a month before owner pay. Fixed expenses are $263K a month, payroll is about $51K, and variable costs run 17% of revenue, so the contribution margin is 83%. In plain terms, pay the owner only after the sales target, reserves, and debt are covered.

Year 1 cost base

$263K fixed expenses monthly

$51K payroll monthly

17% variable costs in Year 1

83% contribution after variable costs

Owner pay trigger

$93K monthly breakeven before owner pay

$773K fixed payroll and overhead base

Owner pay needs revenue above breakeven

Add reserves and debt service first

How much does a tea room owner make per year?

A Tea Room owner doesn’t have a fixed salary; the model shows owner take-home capacity through EBITDA, meaning earnings before interest, taxes, depreciation, and amortization. For What Is The Primary Goal For Tea Room's Growth And Success?, projected EBITDA is $233K in Year 1, $971K in Year 2, $1.596M in Year 3, $2.153M in Year 4, and $2.969M in Year 5, or about $19K–$247K per month before taxes, debt, reserves, and reinvestment. Early cash still matters because the model shows a $626K minimum cash need in Month 6.

Owner Earnings

$233K Year 1 EBITDA

$971K Year 2 EBITDA

$1.596M Year 3 EBITDA

$2.969M Year 5 EBITDA

Income Drivers

Grow daily sales volume

Raise average ticket size

Control labor scheduling

Protect food and tea margins

Which tea room profit margin matters most for owner income?

For a Tea Room, gross margin matters first, because every menu dollar has to clear food, beverage, and waste before labor and overhead; see How Much Does It Cost To Open And Launch Your Tea Room Business? for setup context. Year 1 COGS is 14%—10% food ingredients and 4% beverage ingredients—so gross margin is 86% before labor, while marketing and card fees add 3% of revenue.

Margin drivers

86% gross margin before labor

10% food ingredients in Year 1

4% beverage ingredients in Year 1

Brewed tea helps protect margin

Income risks

$612K payroll is the bigger swing

$18K monthly rent is fixed

Marketing and card fees add 3%

Portion control matters for pastries

Want the six drivers behind tea room owner income?

1

Ticket Mix

$35-$45

Midweek and weekend tickets set revenue per guest, so even small menu shifts raise take-home fast.

2

Covers

800/wk

More weekly covers spread fixed costs over more checks, and table turns decide how much demand you can serve.

3

Tea Events

High

Prepaid afternoon tea bookings and events lift cash collection and usually bring bigger tickets than walk-ins.

4

Gross Margin

86%

An 86% Year 1 gross margin leaves more cash after tea and food costs, so each sale keeps more profit.

5

Labor

$612K

Year 1 payroll of $612K is the biggest controllable cost, so scheduling and the owner's role matter a lot.

6

Rent Load

$18K

Monthly rent of $18K, inside $26.3K of fixed overhead, sets the breakeven floor and can crush income if demand slips.

Tea Room Core Six Income Drivers

Average Ticket And Menu Mix

Average Ticket And Menu Mix

Average order value (AOV) is the main revenue lever here: Year 1 is $35 midweek and $45 on weekends, rising to $40 and $50 by Year 5. A better menu mix lifts revenue per guest, so the same seat can earn more without adding tables. The mix starts at 65% food, 30% beverages, and 5% desserts, then shifts to 60% food and 35% beverages by Year 5.

Premium teas, afternoon tea sets, pastries, sandwiches, seasonal specials, and retail tea add-ons can push the ticket up, but pricing too far above guest value can slow sales. Here’s the quick math: if check size rises and guest count stays flat, revenue goes up first, then gross profit and owner pay follow. The risk is discounting too much or overpricing, which hurts repeat visits.

Measure Check Size By Daypart

Track midweek AOV, weekend AOV, and the share of tickets with add-ons. Watch whether premium teas and tea sets raise the check without hurting repeat visits. If guests buy food but skip beverages, the mix is weak. If beverage share moves from 30% to 35%, that usually supports better margin and cleaner revenue growth.

Price by daypart, not one flat menu.

Bundle tea with pastries or sandwiches.

Test retail add-ons at checkout.

Watch guest pushback on value.

1

Customer Count, Seats, And Table Turns

Customer Count And Table Turns

Year 1 weekly covers of 800 equal about 114 covers a day, and Year 5 rises to 2,210, or about 316 a day. The Friday-to-Sunday block drives the model: Year 1 has 150 Friday covers and 340 on Saturday and Sunday, so 490 weekend covers make up about 61% of the week. More covers lift sales and help spread rent and labor across more checks.

Tea rooms have longer dwell time than quick-service shops, so the limit is often seat turnover, not demand. If peak tea service holds tables too long, you hit a revenue ceiling even with strong traffic. The fix is simple: turn seats faster without rushing guests. That keeps revenue growing while protecting cash flow and owner pay.

Measure Seat Use, Not Just Foot Traffic

Track covers by daypart, average table time, and turn rate. Use reservations to smooth the Friday-Sunday rush, then compare planned seat time with actual seat time. If the room is full but sales stall, the problem is timing, not marketing.

Track Friday through Sunday separately.

Watch average dwell time by service period.

Measure no-shows and late arrivals.

Count covers per seat, per shift.

If tea service runs long, tighten seating windows for peak slots and protect slower hours for linger-friendly guests. Empty seats during the rush are lost revenue; overbooking is worse if it hurts reviews and repeat visits.

2

Afternoon Tea Reservations And Private Events

Afternoon Tea Reservations And Private Events

Prepaid demand is the core win here. Afternoon tea reservations, showers, birthdays, book clubs, seasonal events, and private tea parties can fill slow weekdays with larger party sizes and higher tickets than a normal walk-in. When deposits are collected up front, cash arrives before service, which helps the owner cover labor and plan the day with less guesswork.

The risk is overbooking the dining room. If too many private events block seats, walk-in service suffers and the room can look busy while total revenue quality falls. Fixed menus and portion controls protect margin, and better booking discipline improves cash flow, staffing, and the owner’s take-home pay.

Track Deposits And Seat Blocks

Measure deposit rate, no-show rate, average party size, booked weekday hours, and private-event check size. Those inputs show how much of the room is sold before the day starts, and how much labor to schedule. If bookings are confirmed early, the owner can staff to demand instead of reacting late.

Use fixed menus for these events, limit custom swaps, and keep some tables open for walk-ins. That helps protect the rest of the dining room while still selling off-peak hours. When private bookings rise, cash comes in sooner and labor hours work harder, which supports profit and owner pay.

3

Gross Margin And Cost Of Goods Sold

Gross Margin And COGS

This driver is the share of sales left after ingredients. In Year 1, food ingredients are 10% of revenue and beverage ingredients are 4%, so total COGS is 14% and gross margin is 86%. That means every $100 of sales leaves $86 before labor, rent, and owner pay.

The mix matters. Brewed tea usually carries stronger margin than prepared food, while pastries, sandwiches, dairy, sweeteners, packaging, and spoilage can push costs up if portions drift. If slow-moving items sit too long, waste cuts cash fast and lowers the draw you can pay yourself.

Protect the 86% gross margin

Track ingredient cost by category, not just total spend. Split tea, food, desserts, packaging, and spoilage so you can see which items protect margin and which ones drain it. Menu engineering, which means shifting sales toward higher-margin items, raises owner income without adding seats.

Measure recipe yield and portion drift.

Log spoilage from slow items.

Test brewed tea bundles first.

Reset specs when costs rise.

Here’s the quick math: if sales stay flat, a 1-point COGS drop adds 1 point to gross profit. So moving mix toward brewed tea and tightening portions can lift take-home pay even before traffic grows.

4

Labor Model And Owner-Operator Tradeoff

Labor Coverage Tradeoff

This driver is the payroll needed to cover the floor, the kitchen, and service. Year 1 payroll totals $612K across manager, chefs, kitchen staff, servers, bartenders, and dishwashers, then rises to $841K by Year 5 as traffic grows. Owner shifts can cut cash payroll, but unpaid labor is not the same as profit, so the real question is whether the schedule matches covers.

If staffing is too thin, you save labor dollars but risk burnout, slow service, and weak guest experience. Part-time staffing can fit peak tea hours and busy weekends better than a fixed full crew, and that usually improves cash available for owner pay when the labor plan follows demand instead of forcing it.

Track Covers, Then Staff to Them

Measure labor against daypart covers, not just total payroll. The key inputs are covers, peak-day volume, owner hours, and the mix of manager, kitchen, and service shifts. Here’s the quick math: if the schedule covers demand with part-time help, the owner keeps more cash for pay; if it misses peaks, service drops and the lost sales can outweigh the labor savings.

Track payroll by role weekly.

Match labor to Friday-Sunday peaks.

Use owner shifts only where needed.

Watch burnout and service quality.

5

Rent, Location, And Local Demand

Location Drives Sales Or Break-Even Pain

For a tea room, location affects owner income by changing how many covers and reservations you can sell against fixed costs. With $18K/month rent and $263K/month in total fixed overhead before payroll, the site has to pull enough traffic to carry $281K/month before labor. Good visibility, parking, walkability, nearby boutiques, tourism, and local demographics all help. Weak foot traffic does the opposite.

Here’s the quick math: if the lease only works with peak weekend volume, the owner’s draw gets squeezed fast. Strong local demand lifts sales without a matching jump in fixed cost, so more of each extra cover can reach profit. One clean rule: don’t sign for a “maybe busy” block if the rent only works on best-case Saturdays.

Track Traffic Before You Sign

Measure the inputs that prove demand: walk-by counts, parking ease, nearby offices and shops, weekend reservation volume, and the share of covers that come from repeat guests or nearby residents. Also test whether lunch, afternoon tea, and dinner all hold demand, not just weekends. If weekday traffic is thin, fixed costs stay the same and owner pay gets tighter.

Use a simple site test: compare expected covers to $281K/month in fixed load, then map sales by daypart. If visibility and foot traffic raise reservations enough to beat the rent step-up, the lease helps income. If not, the site just adds pressure. A location that fills seats on ordinary weekdays is worth more than one that only shines on holidays.

Track weekday covers and walk-ins.

Count nearby demand drivers weekly.

Watch reservation fill rates by daypart.

Stress-test rent against slower weeks.

6

Compare low, base, and high tea room owner income outcomes

Owner income scenarios

Owner income moves with covers, ticket size, and labor because rent stays fixed. These cases show how slow reservations or stronger event traffic change take-home potential.

Compare downside, base, and upside owner income.

Scenario

Low CaseCash risk

Base CaseStaffing difficulty

High CaseTarget-pay gap

Launch model

The low case assumes weaker covers and a softer ticket, so owner income stays near breakeven after rent and payroll.

The base case follows the model's Year 1 plan and lands at Month 4 breakeven with a 17-month payback.

The high case adds stronger covers, better beverage mix, and event bookings, so owner income steps up faster.

Typical setup

Weekday covers lag the plan, reservations move slower, and the same rent base stays in place while staffing still has to cover the floor and kitchen.

Year 1 revenue is about $1.63M, gross margin is about 86% before payroll, payroll runs near $612k, and fixed overhead is about $315.6k a year.

Weekend traffic runs above plan, beverages take a bigger share, event sales lift ticket size, and labor grows more slowly than volume.

Cost drivers

weaker covers

lower ticket

slower reservations

fixed rent pressure

payroll drag

modeled covers

standard ticket

86% gross margin

$612k payroll

fixed overhead

stronger covers

better beverage mix

event bookings

tighter labor

higher ticket

Owner income rangeBefore owner reserves

$0 - $90,000Thin draw

$233,000Modeled draw

$300,000 - $400,000Upside draw

Best fit

Use this to stress-test cash flow if traffic misses plan and the owner draw has to stay light.

Use this as the working case for budgeting, hiring, and lender-style planning.

Use this to test upside if bookings, repeat visits, and labor control all beat the base plan.

!

Planning note: Scenario ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions.

This model shows a minimum cash need of $626K in Month 6, so reserves are not optional That cash covers build-out timing, early payroll, rent, equipment, and ramp-up gaps Major startup spending includes $150K build-out, $120K kitchen equipment, and $60K furniture and fixtures

The researched model reaches breakeven in Month 4 and payback in 17 months That assumes Year 1 revenue of about $163M, weekly covers of 800, and average checks of $35 midweek and $45 on weekends If traffic ramps slower, breakeven moves out fast because rent and payroll are fixed

You don’t need retail tea sales to model base income here, but they can help owner take-home Retail add-ons can raise average ticket without using many extra seats The base model already depends on a strong menu mix, with beverages at 30% of Year 1 sales and rising to 35% by Year 5

Owner draws move most with customer count, average ticket, labor, rent, and gross margin In Year 1, payroll is $612K, rent is $18K per month, and COGS is 14% of revenue A small miss in covers hurts more than a small tea-cost increase because staffing and rent still get paid

Hire when service quality or table turns cap revenue, not just when the room feels busy The model grows from $612K payroll in Year 1 to $841K in Year 5 as covers rise If extra staff increases reservations, protects reviews, and keeps labor aligned with peak days, it can support owner income

Choosing a selection results in a full page refresh.