Owner income$353k-$2.48M

Owner income$353k-$2.48MHow Much Does a Tibetan Singing Bowl Shop Owner Make? $353k–$25M

Fully Editable

Instant Download

Professional Design

Pre-Built

No Expertise Is Needed

Description

Owner income$353k-$2.48M  Net margin54%-70%

Net margin54%-70% Revenue for target pay$657k-$3.53M

Revenue for target pay$657k-$3.53M Business difficultyHard

Business difficultyHard

Based on the researched assumptions, Tibetan singing bowl shop owner income capacity ranges from about $353k in Year 1 to $2478M in Year 5 before taxes, debt service, and owner-specific reserves Revenue scales from $657k to $3528M, with direct cost assumptions improving from 14% to 11% of sales The shop breaks even in Month 3, but owner distributions should wait until inventory, payroll, and the $833k minimum cash need are covered Treat EBITDA as available pre-tax cash flow, not an automatic salary

Owner income$353k-$2.48MNet margin54%-70%Revenue for target pay$657k-$3.53MBusiness difficultyHardWant to test your owner pay target?

Owner income calculator

Estimate owner take-home and target-pay gap from revenue, margin, costs, reserves, and target pay.

Planning note: This is a researched planning estimate, not guaranteed salary, tax advice, or owner distribution advice. Actual owner income depends on revenue mix, margins, staffing, rent, taxes, debt, and reinvestment.

Want to see the owner-pay forecast?

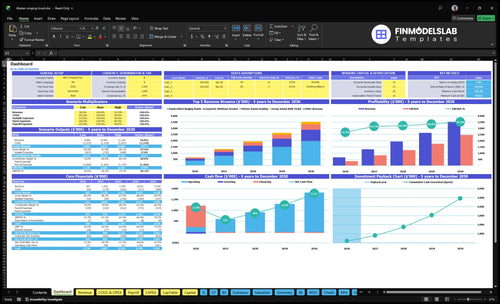

The dashboard shows revenue, EBITDA, breakeven, payback, and owner-income capacity; the assumptions tab covers visits per day, 310 operating days, pricing, sales mix, COGS, variable fees, payroll, rent, and startup spend. Open the Tibetan Singing Bowl Shop Financial Model Template.

Owner-income model highlights

- Owner take-home capacity

- Revenue and EBITDA

- Price and volume tests

How much revenue does a Tibetan singing bowl shop need to pay the owner?

The Tibetan Singing Bowl Shop can pay the owner only after it covers COGS, marketing, payment fees, rent, payroll, and cash reserves. At $657k in Year 1 revenue, or about $548k per month, it shows $353k in EBITDA before owner-specific deductions, so there is room for pay. Payroll starts at $138k a year, and owner pay should be funded after the inventory reserve and required cash, not set as an automatic salary.

Owner pay test

- $657k Year 1 revenue

- $548k monthly revenue run-rate

- $353k EBITDA before owner pay

- Pay owner after reserves

Cost gates first

- $65k fixed overhead monthly

- $138k annual payroll starts

- Cover inventory reserve first

- Keep required cash untouched

What margins matter most in a Tibetan singing bowl shop?

For a Tibetan Singing Bowl Shop, the margins that matter most are gross margin and the cash left after freight, slow stock, returns, and payroll. For a quick cost map, see What Are Operating Costs For Tibetan Singing Bowl Shop? Direct costs move from 14% in Year 1 to 11% in Year 5, so gross margin rises from 86% to 89%, but digital marketing at 5% and payment processing at 3% still take a real bite. A few points of margin loss can hit EBITDA hard because rent, payroll, and insurance stay fixed, and inventory cash timing can block distributions even when profit looks strong.

Margin watch

- 14% to 11% direct costs

- 86% to 89% gross margin

- 5% marketing spend

- 3% payment processing

Cash pressure

- Price for freight, returns

- Watch slow stock closely

- Cover fixed payroll each month

- Delay payouts if cash traps

Do singing bowl shops make more from retail sales or sound healing sessions?

A Tibetan Singing Bowl Shop starts with retail and sessions tied, but sessions become the larger sales stream over time; see How Do I Launch A Tibetan Singing Bowl Shop Business? for the launch setup. The plan shifts from 50% retail / 50% services in Year 1 to 30% retail / 70% services by Year 5. Compare contribution, not just revenue, because bowls carry sourcing and freight costs while sessions depend on bookings, room use, payroll, and no-shows.

Retail sales

- 50% of Year 1 sales mix

- Falls to 30% by Year 5

- Needs inventory cash upfront

- Hit by sourcing and freight costs

Sound sessions

- 50% of Year 1 sales mix

- Rises to 70% by Year 5

- Includes private, group, corporate work

- Payroll and no-shows drive margin

Want the six drivers behind owner income?

1

86%-89%Product Margin

High bowl margin keeps more of each sale in the business, so freight or discount creep hits owner take-home fast.

2

12-40/daySales Volume

More daily visits drive both retail and session revenue, and 310 open days makes traffic the main growth lever.

3

20%-25%Session Utilization

Filling private healing slots lifts high-value service income with little product cost, so empty sessions hurt profit.

4

$15-$25Upsells

Accessories and mallets add low-friction revenue to each order and raise average ticket without much extra labor.

5

$65K/moOverhead Load

Rent, staff, and support costs set the break-even line, so take-home only improves after volume clears the fixed load.

6

$833KCash Reserve

Cash and inventory turn matter because the model's minimum cash dips to $833K in Month 2, which can strain growth.

Tibetan Singing Bowl Shop Core Six Income Drivers

Product Gross Margin

Product Gross Margin

Tibetan singing bowl margin is driven by sourcing cost, freight, bowl size, quality tier, and retail price. With 14% direct costs in Year 1, gross margin is about 86% before marketing and payment fees, so each sale leaves room for owner pay if volume holds.

By Year 5, direct costs fall to 11%, lifting gross margin to 89%. That extra 3 points helps take-home income, but premium inventory can lock up cash before it sells. The real risk is not margin on paper; it’s slow stock and freight creep that shrink cash available for draws.

Protect Margin Early

Price each bowl from landed cost — purchase price plus freight — not just supplier cost. Track freight per unit, tier, and sell-through by bowl size so you can spot where margin is leaking. If a premium bowl sits too long, it can look profitable and still hurt cash flow.

Use a simple monthly review:

Check landed cost by tier.

Review slow stock older than 60 days.

Test price changes before reordering.

Keep the shelf mix tight so the owner’s profit draw is funded by sales, not by tied-up inventory.

1

Sales Volume And Conversion

Sales Volume and Conversion

Sales volume is the number of visitors who turn into buyers or booked sessions. In this model, visits rise from 12 per day in Year 1 to 40 per day in Year 5 across 310 operating days, so the shop goes from about 3,720 visits to 12,400. With modeled revenue rising from $657k to $3.528M, the real driver is not traffic alone; it’s how well each visit converts into units sold, session bookings, and revenue per visit.

That matters because rent and payroll are fixed. Here’s the quick math: if conversion slips, the shop still carries the same base costs, so owner pay gets squeezed fast. The key watchout is weak basket size or empty appointment slots. Track units sold, average order value, session bookings, and revenue per visit every week, not just monthly, so you can catch slow traffic before it hits cash flow.

Measure Revenue per Visit First

Start with revenue per visit, then split it by channel: in-store, website, local events, and wellness referrals. If you know visits, conversion rate, and average order value, you can forecast take-home income with much better accuracy. A small lift in conversion usually beats buying more traffic, because it raises revenue without adding much fixed cost.

Push the levers that matter: add clear upsells, tighten booking follow-up, and review which events and referral sources create paid orders. If the shop gets more foot traffic but the order count stays flat, owner profit will lag even as the place looks busy. That’s the hidden risk in this driver: busy does not always mean profitable.

2

Sound Healing Session Utilization

Sound Healing Session Utilization

Session revenue comes from private healing at $120, group tickets at $45, and corporate sessions at $500. The real driver is booked hours per practitioner, plus room fill and no-show control. If sessions make up 50% of Year 1 revenue and rise to 70% by Year 5, better utilization can lift owner pay fast, but empty slots still carry labor cost.

Here’s the quick math: revenue = private bookings × $120 + group tickets × $45 + corporate sessions × $500. The owner’s take-home improves when session hours are sold, not just scheduled. What this hides: if practitioner time is paid but the room is empty, payroll turns into a drag and profit drops even when posted prices look strong.

Track Booked Hours, Not Just Bookings

Measure show rate, booked practitioner hours, and revenue per available hour. Split the calendar by private, group, and corporate work, then compare each slot’s cash return. If one practitioner is paid for an open block, that’s direct margin leakage. Keep the schedule tight enough to protect payroll, but leave room for the higher-ticket $500 corporate work.

- Track no-shows by session type.

- Price peak slots higher.

- Match staffing to booked demand.

- Review empty hours weekly.

Use the mix shift from 50% to 70% revenue as a planning test. More service revenue can improve contribution, but only if the room stays full and practitioners stay busy. If corporate bookings are lumpy, forecast payroll against confirmed sessions, not hoped-for demand, so owner draws don’t depend on wishful scheduling.

3

Average Order Value And Upsells

Upsells Raise Average Order Value

Average order value means the average ticket per sale. In a Tibetan singing bowl shop, it rises when buyers add mallets, cushions, gift sets, or step up to a better bowl. With accessory assumptions moving from $15 in Year 1 to $25 in Year 5, and handcrafted bowl pricing rising from $250 to $295, each visit can produce more revenue without more rent or payroll.

Here’s the quick math: a $250 bowl plus a $25 accessory pack is a $275 basket before tax. Post-session purchases can lift revenue per visitor without much fixed cost, so more of that extra sales dollar can flow to profit and owner pay. What this hides: if add-ons are pushed hard or overstocked, cash gets tied up and margin can slip.

Track Attach Rate and Basket Mix

Measure attach rate first, which is the share of orders that include an add-on. Track visits, basket size, and the split between $250 base bowls, $295 premium bowls, and accessory bundles. If session guests buy more after guided visits, that is real uplift; if not, the shop is just moving product, not creating more income for the owner.

- Bundle mallet and cushion.

- Offer gift sets after sessions.

- Price add-ons by use.

- Watch margin on each bundle.

Keep upsells practical and tied to how customers will use the bowl, not pressure. Helpful add-ons can raise cash flow fast because they do not add much fixed cost, but weak bundle discipline can still hurt profit. The owner should test which add-on mix lifts revenue per visitor while keeping gross margin healthy.

4

Overhead And Staffing

Overhead And Staffing

$65k per month is the fixed overhead floor, or about $780k a year, before the owner earns anything. That includes $45k for rent, utilities, insurance, software, cleaning, and accounting. Payroll rises from $138k in Year 1 to $319k in Year 5, so a staffed shop needs much higher volume than an owner-run shop to protect take-home income.

Here’s the quick math: if sales do not outpace overhead, profit turns into cash burn. Owner-operated shops can keep more cash earl y, but once staff is added, every role has to pay for itself through more visits, more session bookings, or larger baskets. Separate required costs from optional growth spend and owner compensation.

Control payroll before hiring

Build the model from required costs only: $65k monthly overhead, $138k to $319k payroll, and owner pay. Track sales per visit, session fill rate, and labor as a share of revenue. If payroll rises faster than sales, the owner’s draw gets squeezed fast.

Set a hiring trigger tied to cash, not hope. Keep staff hours flat until new revenue can cover the next $10k to $20k of fixed cost with room left for profit. If that coverage is not there, delay hiring, trim nonessential spend, and keep the owner on the schedule longer.

5

Inventory Turnover And Cash Reserves

Inventory Turnover and Cash Reserves

When premium bowls move slowly, cash gets trapped even if gross margin looks strong. This driver includes inventory turns, days on hand, and the cash reserve needed to pay bills and buy the next batch. With $25k in initial master set inventory, $805k total capex, and minimum cash at $833k in Month 2, owner pay can lag the income statement.

Track inventory by bowl tier, sell-through, reorder point, and cash burn. A slow premium tier can delay distributions because the cash sits on the shelf, not in the bank. Here’s the quick math: if reserve cash drops below the monthly floor, pause owner draws until turnover improves and the next replenishment is funded.

Set Replenishment Rules Before Paying Yourself

Set a minimum stock level and aging trigger for each tier, then review it weekly. If a bowl tier is not moving, cap new buys, bundle it, or mark it down before it ties up more cash. This protects take-home income by keeping working capital free for rent, payroll, and the next order.

Keep a cash rule tied to the reserve floor: buy inventory only if the post-purchase balance stays above $833k in Month 2. That keeps the business from looking profitable on paper while owner distributions get delayed in real life.

6

Compare low, base, and high owner-income outcomes

Owner income scenarios

Owner income changes fast here because traffic, retail mix, and session volume all move the margin. Year 1 shows the downside, Year 3 the modeled base, and Year 5 the upside.

| Scenario | Low CaseDownside | Base CaseModeled | High CaseUpside |

|---|---|---|---|

| Launch model | This is the lower-earnings path based on Year 1 volume and the smallest operating base. | This is the modeled middle path using Year 3 volume and the planned operating mix. | This is the stronger-earnings path if traffic, corporate work, and repeat visits scale. |

| Typical setup | About 12 visits per day, 50% retail mix, $657k revenue, and $353k EBITDA, with reserve needs still in play. | About 25 visits per day, 40% retail mix, $1.945M revenue, and $1.253M EBITDA, with a broader service mix. | About 40 visits per day, 30% retail mix, $3.528M revenue, and $2.478M EBITDA, with more volume from services and contracts. |

| Cost drivers |

|

|

|

| Owner income rangeBefore owner reserves | $353kLow case | $1.253MBase case | $2.478MHigh case |

| Best fit | Use this to stress-test launch demand, payroll coverage, and cash runway. | Use this as the main planning case for budgeting, hiring, and lender talks. | Use this to test upside if the shop wins more recurring sessions and corporate deals. |

Planning note: These scenario ranges are researched planning assumptions, not guaranteed earnings, salary promises, tax advice, or distributions.

Related Products

- Tibetan Singing Bowl Shop Porter's Five Forces Analysis

- Tibetan Singing Bowl Shop BCG Matrix

- Tibetan Singing Bowl Shop Business Model Canvas

- What Are The 5 KPI Metrics For Tibetan Singing Bowl Shop?

- Tibetan Singing Bowl Shop Business Plan Template in Pre-Written Word

- How Increase Profits For Tibetan Singing Bowl Shop?

- What Are Operating Costs For Tibetan Singing Bowl Shop?

- Tibetan Singing Bowl Shop Startup Costs: $805K CAPEX Plan

- Tibetan Singing Bowl Shop Financial Model Template in Excel

- How To Open A Tibetan Singing Bowl Shop In 8 To 16 Weeks

- How To Write A Business Plan To Launch A Tibetan Singing Bowl Shop?

- Tibetan Singing Bowl Shop Marketing Mix

- Tibetan Singing Bowl Shop Marketing Plan

- Tibetan Singing Bowl Shop Business Proposal

- Tibetan Singing Bowl Shop PESTEL Analysis

- Tibetan Singing Bowl Shop Pitch Deck Example Editable PPTX

- Tibetan Singing Bowl Shop Business SWOT Analysis

- Tibetan Singing Bowl Shop Value Proposition Canvas

Frequently Asked Questions

The researched model shows $353k to $2478M of EBITDA from Year 1 to Year 5 That is owner-income capacity before taxes, debt service, and reserve decisions Revenue ranges from $657k to $3528M, so actual take-home depends on how much cash stays in inventory, payroll coverage, and reinvestment